Published on

June 21, 2026

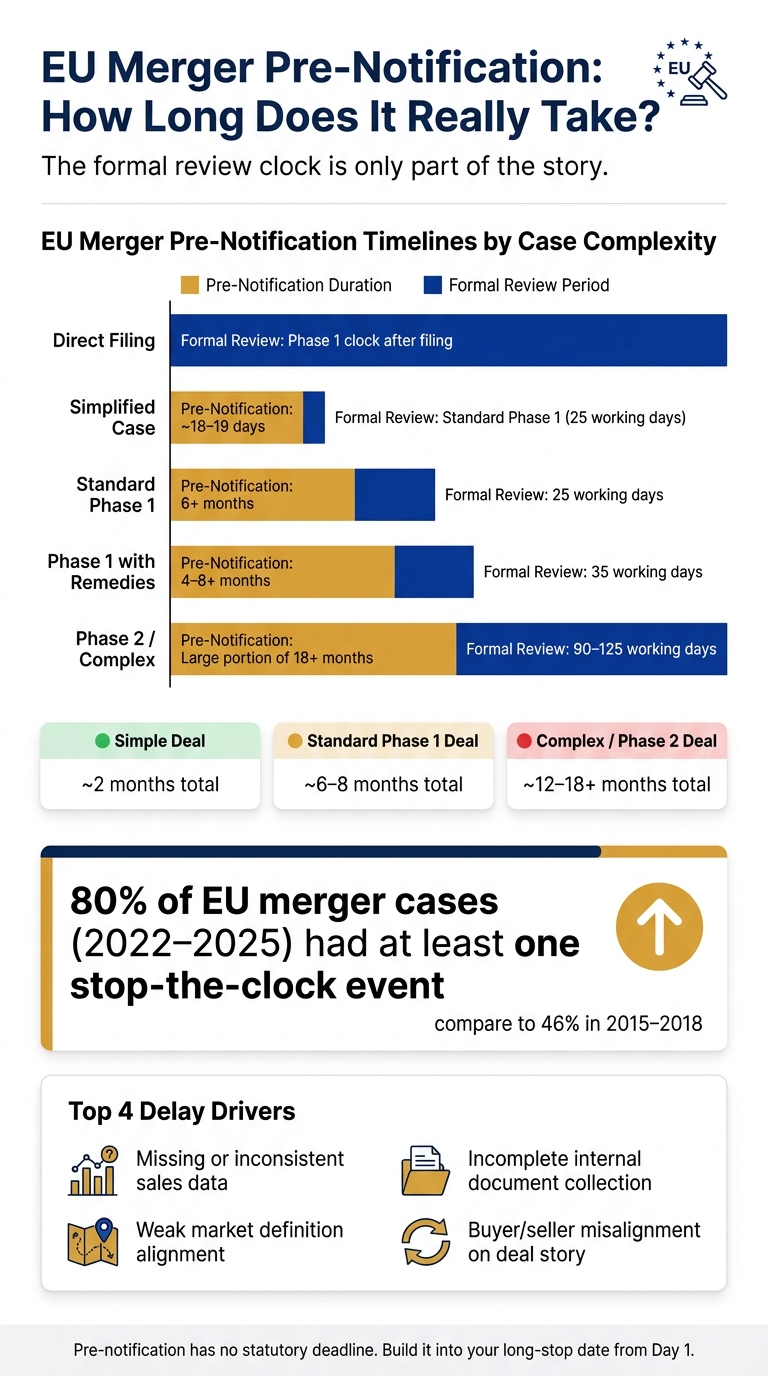

If you plan around the EU’s formal merger clock alone, your deal timeline can be off by months. I’d treat pre-notification as the part that usually sets the closing date, because it has no fixed deadline and can last from 1–3 weeks in simple cases to 6+ months in harder ones.

Here’s the short version:

If I were building a signing-to-closing plan, I’d assume:

The biggest causes of delay are usually internal: missing sales data, weak document collection, extra question rounds, and buyer/seller misalignment on market definition or deal story. The main fix is simple: start early, collect data before drafting, and run one shared workstream across legal, finance, and corp dev.

| Deal Type | Pre-Notification | Formal Review | What Usually Slows It Down |

|---|---|---|---|

| Direct filing | None or very short | Phase 1 clock after filing | Wrong filing route |

| Simplified | ~18–19 days | Usually standard Phase 1 | Missing support data |

| Standard Phase 1 | 6+ months in some cases | 25 working days | Data requests, document review |

| Phase 1 with remedies | ~4–8+ months | 35 working days | Remedy talks, market test |

| Phase 2 / complex | Can take a large share of total timeline | 90–125 working days | Stop-the-clock pauses, heavy RFIs |

So the takeaway is simple: the formal review period is only part of the story. If you want a closing plan that holds up, build pre-notification into your long-stop date, financing plan, and investor updates from day one.

EU Merger Pre-Notification Timelines by Case Complexity

Day 0 starts only when the Commission accepts a complete Form CO [3]. Until that point, the clock is shaped by case complexity, the quality of the draft, and how many feedback rounds you go through with DG COMP. That gap shows up first in simplified filings.

Some deals move fast. If a transaction has no horizontal or vertical overlaps - like certain joint ventures with no EEA turnover - the Commission allows a direct filing procedure. In those cases, parties can notify without pre-notification contacts [4].

For standard simplified cases, average pre-notification lasts about 18 to 19 days [4]. That sounds short, but it can slip if supporting data is missing or if the Commission has doubts about whether the deal fits the simplified track.

Once overlaps or vertical links enter the picture, the pace changes fast.

For deals with horizontal overlaps, vertical links, or conglomerate issues, pre-notification often runs more than 6 months. In some Phase I remedy cases, it has stretched to 8+ months [5].

The full process can get much longer in deeper investigations. In 2024, the total duration for Phase II cases - including pre-notification and formal review - went past 18 months on average [5]. And pauses in the review process are no longer rare: the stop-the-clock mechanism was used in 80% of cases between 2022 and 2025, up from 46% in the 2015–2018 period [5].

The table below shows the pattern pretty clearly: as complexity goes up, the pre-notification window tends to widen.

| Case Type | Indicative Pre-Notification Range | Data Burden | Typical Delay Drivers |

|---|---|---|---|

| Direct Filing | None (direct filing) [4] | Low (tick-the-box Short Form CO) | Misjudging eligibility for direct filing |

| Simplified | ~18–19 days [4] | Moderate | Incomplete supporting data; strict eligibility criteria |

| Standard Phase 1 (Unconditional) | 6+ months [5] | High | Extensive data requests; internal document review |

| Phase 1 with Remedies | ~4–8+ months [5] | Very High | Remedy negotiation; market testing |

| Phase 2 / Complex | Significant portion of an 18+ month total process [5] | Extreme | Stop-the-clock events; complex theories of harm |

Across all case types, the main thing deal teams can control is internal readiness. Procedure type gives you the starting point. Your data prep usually decides what happens in practice.

"While it may prima facie appear that less information will be submitted with the notification forms, in fact the amount of information and internal documents that notifying parties will have to collect has not materially decreased." - McDermott Will & Emery [4]

Procedure type sets the floor. Data readiness sets the timeline you actually live with.

Most delays come from one place: the parties aren't ready inside their own organization. Data doesn't line up, documents are missing, and teams use different ways to define the market. In practice, two things drive most of the slippage: weak data readiness and deal teams that aren't on the same page.

Form CO asks for detailed information, not rough estimates. That includes market definitions, horizontal and vertical overlap analysis, exact market shares, customer data, and internal documents such as board presentations and strategic plans. If finance and operations teams can't pull consistent numbers across business units, the Commission usually comes back with follow-up questions. And every new round adds more time.

The paperwork can get heavy fast. In more complex matters, completed Form COs can run past 1,000 pages, before you even count the annexes [2].

There is also more to disclose now. Since late 2023, parties must report 10%+ non-controlling stakes, cross-directorships, and pipeline products [1][4]. If no one maps those items before drafting begins, the result is pretty predictable: more questions, more back-and-forth, and a longer pre-notification period.

Things also slow down when buyer and seller tell slightly different stories. If they disagree on market definition or on how to explain the deal's effect on competition, the Commission tends to ask for more detail. Mixed or disputed descriptions usually lead to extra drafting rounds before the filing is treated as complete [1].

The drag gets worse when EU pre-notification is happening at the same time as other reviews. Foreign investment reviews and other parallel processes can add admin work and create timing clashes. If those tracks are not lined up from the start, one review can end up waiting for another, and the timetable starts to slip.

The deals that move fastest usually treat pre-notification as a managed workstream, not just a drafting task.

The fastest deals do the heavy lifting before the first draft goes to DG COMP. That early prep cuts down the usual back-and-forth later.

Start with EU dimension screening and overlap mapping as early as you can, including the alternative thresholds. Finance should pull 3 to 5 years of audited sales data by customer location, since turnover is allocated by customer location [2]. The team should also check whether the deal could face an Article 22 referral even if the filing thresholds are not met [6].

DG COMP also expects a large set of internal documents. That means it helps to gather board decks, minutes, strategy papers, and key emails as soon as the LOI is signed. If you wait, this step can drag on and slow everything else.

A single internal process helps legal, finance, and corporate development stay in sync. It also cuts down on duplicate work.

Use:

Repeated requests can lead to stop-the-clock pauses, so each response should have one clear owner. If too many people touch the same request, things get messy fast.

| Timing Bottleneck | Effect on Pre-Notification | Practical Mitigation | Internal Owner |

|---|---|---|---|

| Data collection | Delays Form CO drafting by weeks or months | Organize 3 to 5 years of audited financial and sales data by customer location early | CFO / Finance Team |

| Internal documents | Leads to repeated "incomplete" notices from DG COMP | Centralize board decks, minutes, and key officer emails in a searchable data room at the LOI stage | Corp Dev / Legal |

| Market mapping | Prevents use of the faster "Short Form CO" | Conduct preliminary overlap and vertical relationship screening before first contact | Legal / Strategy |

| RFI response delays | Triggers "stop-the-clock" suspensions | Use a single response tracker with clear sign-off rules | Legal / Finance |

Pre-notification is the most unpredictable part of EU merger control. So it needs to be part of deal timing from day one. In tougher cases, it also eats up a lot of senior management time. That means teams shouldn't treat it like admin. They should treat it like its own workstream.

That pressure on timing is exactly why deal teams need to map out best-case, base-case, and worst-case closing scenarios before signing. A simple case may take about 2 months end to end. A standard Phase 1 matter can take around 6–8 months. And a complex or Phase II deal can stretch to 12–18+ months. If the deal is complex, build your model around at least 18 months of total process time.

There’s also a financing angle here. With 80% of cases between 2022 and 2025 involving at least one stop-the-clock event [5], lenders and investors need an early heads-up that the final closing date may shift. Long-stop dates, bridge financing, and investor updates should all reflect that uncertainty.

Pre-notification has no statutory deadline, and timing now tends to run longer than it did in prior years. Build that uncertainty into long-stop dates, bridge financing, and investor updates. Pre-notification is the variable that breaks closing calendars, so treat it that way.

The formal EU merger review clock starts when the notifying parties file a complete Form CO with the European Commission. That filing kicks off the Phase I investigation.

Any pre-notification talks happen before that point and do not count toward the official review clock. Once the Commission accepts the formal notification, the review moves on a set timetable measured in working days, with weekends and Commission public holidays left out.

Check whether the transaction fits the Commission’s simplified procedure thresholds and categories. This usually applies to deals where the parties work in different markets, or where their combined shares are very low in markets that overlap.

Key criteria include:

The parties need to back this up with evidence, usually during mandatory pre-notification discussions with the Commission.

Before you contact the Directorate-General for Competition (DG COMP), put together a draft Form CO or the other notification template that fits your deal.

The point of pre-notification is simple: make sure the filing is accurate, clear, and substantially complete. That means you should be ready to do more than send over a draft and wait.

Expect to provide:

Think of pre-notification as a working session, not a box-ticking step. If your draft is thin or key data is missing, the process can slow down fast. A solid draft gives the case team what they need and makes the back-and-forth much easier.