Published on

June 11, 2026

Markets are efficient - until they're not. Specific events like mergers, earnings reports, or regulatory decisions often disrupt pricing, creating temporary inefficiencies. These gaps occur because markets take time to fully process complex information, leaving opportunities for investors who act quickly.

Key Takeaways:

Understanding these inefficiencies can help investors better navigate short-term mispricings tied to specific, time-sensitive events.

Market inefficiency refers to the gap between an asset's current price and its true underlying value. These gaps occur when the market doesn't immediately adjust prices to reflect new information. While the Efficient Market Hypothesis (EMH) suggests that prices should always incorporate all available data, real-world factors like delays in information processing, structural barriers, and human biases often prevent this from happening.

As NYU Stern finance professor Aswath Damodaran explains:

"Market 'inefficiencies' can provide the basis for screening the universe of stocks to come up with a sub-sample that is more likely to have undervalued stocks." [6]

In short, these pricing discrepancies create temporary opportunities before the market eventually corrects itself.

Events such as mergers, earnings reports, or regulatory decisions introduce new information that markets take time to fully digest. Analysts often need days or even weeks to update their models, and retail investors may react even more slowly. When multiple events occur simultaneously, investor attention gets divided, further slowing the market's response and leaving room for gradual price adjustments.

Behavioral factors like anchoring also play a role. Investors may only partially adjust their expectations when new information is released, which can leave stocks undervalued for an extended period - even after strong earnings results.

Structural issues add to the delay. Factors like transaction costs, low liquidity in smaller stocks, or the difficulty of acquiring large positions without impacting prices can all prevent immediate corrections. These conditions allow arbitrage opportunities to persist even after the market is presented with fresh data.

Together, these dynamics create the conditions for inefficiencies that investors can potentially exploit.

The examples provided focus solely on U.S.-listed companies, operating under U.S. regulatory standards and involving dollar-denominated transactions. They include real-world cases like M&A activity, quarterly earnings surprises, SEC actions, and unique corporate events. Each example highlights a specific pricing anomaly tied to an actual event.

The aim here is to show how these inefficiencies play out in practice, rather than just presenting theoretical concepts.

Mergers and acquisitions often lead to temporary pricing discrepancies as markets rush to evaluate the likelihood of deals being completed. The difference between a target stock's trading price and the agreed-upon deal price - known as the merger arbitrage spread - highlights where markets might be misinterpreting the situation. Below, we explore a few specific M&A scenarios that showcase these pricing inefficiencies.

Hostile takeovers - where acquirers bypass a company's management - tend to result in wider spreads. This is due to increased risks, such as management opposition, financing challenges, and the potential for the deal to fall apart.

Take Spirit Airlines as an example. Despite JetBlue offering a higher hostile bid, Spirit's board favored a lower bid from Frontier Airlines, citing regulatory concerns [7]. This left the market grappling with two outcomes: a higher but riskier deal versus a lower but more straightforward one. Retail investors leaned toward the JetBlue offer, attracted by the potential upside, while institutional investors exercised caution, revealing how different players interpret the same risks in contrasting ways.

Regulatory scrutiny has become a key factor in driving spread mispricings. After the 2025 overhaul of the HSR Act, large-cap deals now face clearance timelines of 12–18 months [12]. This prolonged process keeps merger arbitrage spreads wide for extended periods, even when the deals themselves seem solid.

For instance, in early 2026, the Edwards Lifesciences/JenaValve Technology deal was terminated after a preliminary injunction blocked it [8][9][10]. The court applied a "pre-commercial innovation market" theory, arguing that both companies were the only ones conducting U.S. clinical trials for a specific heart valve device. This decision was made despite Edwards' competing product not being expected to hit the market until 2029.

"For large-cap companies, the 'quick deal' is effectively dead, replaced by a grueling process of narrative disclosures and exhaustive document production." - MarketMinute [8]

The costs of this regulatory environment are steep. Complying with Second Request investigations can now cost between $3 million and $15 million for mid-market deals, while civil penalties for missing HSR filing deadlines exceed $51,000 per day [11]. These expenses inflate merger spreads, making them appear larger than the actual probability of failure might justify.

Bid revisions offer another example of M&A-related inefficiencies, often leading to market underreactions. A revised bid not only uncovers hidden value in the target but also reflects the acquirer's strategic discipline.

Between December 2025 and February 2026, Netflix initially agreed to acquire WBD's studio and HBO assets for $27.75 per share. However, Paramount Skydance entered with a hostile bid of $31.00 per share, offering a 40% premium over WBD's pre-deal price [14]. During this bidding war, Netflix's stock dropped by roughly 35% from late January to late February 2026, as investors worried about potential overpayment [13].

On February 26, 2026, Netflix Co-CEOs Ted Sarandos and Greg Peters declined to match the higher bid within two hours. Instead, they secured a $2.8 billion breakup fee, leading Netflix's stock to rebound by 18% over the next two sessions [13].

"Warner Bros was 'nice to have at the right price, not a must have at any price.'" - Ted Sarandos and Greg Peters, Co-CEOs, Netflix [13]

Investors who closely monitored the matching-rights window in the merger agreement were better positioned to anticipate the market's reaction, showcasing how attention to deal terms can provide a significant advantage.

Earnings announcements often reveal pricing gaps that stem from how investors interpret quantitative data. During earnings season, these gaps become a frequent source of short-term market mispricings, as investors sometimes misread - or take time to fully process - the numbers presented.

When a company delivers earnings that significantly beat or miss expectations, the market doesn't always adjust immediately. Instead, Post-Earnings Announcement Drift (PEAD) describes how a stock tends to continue moving in the direction of the earnings surprise for weeks - or even up to 90 days - after the initial report [18].

This lag is largely due to investor underreaction. Institutional managers may take time to adjust their positions, sell-side analysts update their models on staggered timelines, and smaller investors often require additional trading sessions to digest the news [16][18].

"Investors should view the initial post-earnings price move not as a completed adjustment, but as a directional signal for a broader capital reallocation process that typically takes an entire fiscal quarter to fully manifest." - Finexus [18]

This phenomenon is particularly noticeable in smaller, less liquid stocks, where limited analyst coverage and information gaps are more common. Research highlights that a long-short strategy based on earnings surprise deciles can yield a value-weighted return of 1.60% per month in illiquid stocks, compared to just 0.14% in highly liquid ones [17]. Historically, stocks in the top decile of positive earnings surprises have outperformed the market by an average of 3.5% to 5.0% over the 60 trading days following the announcement [18].

While underreaction explains the prolonged drift, misleading headline figures can create immediate mispricings that demand closer inspection.

Headline earnings per share (EPS) figures, though straightforward, often hide important details that lead to initial market mispricing.

Take Nvidia’s August 2024 earnings report as an example. The company announced record second-quarter revenues and earnings that far exceeded analyst expectations. Yet, the stock dropped 8% the next day, wiping out over $200 billion in market value [19]. Why? Concerns about slowing growth, supplier-driven margin pressures, and a $50 billion buyback announcement suggested the company was entering a more mature growth phase.

A similar case occurred in early 2026 with SoFi Technologies. Despite delivering a "beat and raise" quarter - surpassing expectations and raising full-year guidance - the stock fell 15% on the same day. Prepared remarks and segment-level data later revealed weaknesses that the headline EPS had failed to show, prompting an immediate market re-rating [20].

"The expectations game is an insidious one, where investors move the goal posts constantly, and more so, if you have been successful in the past." - Aswath Damodaran, Professor of Finance [19]

The lesson here? Don’t stop at the EPS headline. Management commentary often reveals the real story, whether it’s margin pressures, slowing customer growth, or changes in business mix that the headline number might obscure.

Interestingly, the opposite dynamic can also occur: an earnings miss paired with strong forward guidance can lead to an initial overreaction, followed by a recovery.

When companies report earnings misses, the market often reacts with an immediate sell-off - even when strong forward guidance suggests a more optimistic long-term outlook. This happens because headline EPS figures are structured data that algorithms can process almost instantly, while forward guidance - often delivered as unstructured commentary - takes longer for markets to fully digest [1][5].

"The meaningful distinction isn't between different types of information, but rather it's between structured and unstructured form. The easy, numbers-based underreaction got competed away first. The harder, language-based underreaction survived." - Lihong, Author of The Logbook [1]

For example, in May 2026, Coinbase reported a revenue miss of 31% relative to expectations, leading to a modest 2.5% stock decline. The muted reaction was due to light institutional positioning and market focus on an upcoming regulatory milestone (OCC trust bank approval) rather than quarterly transaction fees [20]. Similarly, Affirm Holdings reported Q3 adjusted EPS of $0.37 - well above the consensus estimate of $0.27 - but still saw its stock drop 5%. Investors were more concerned with slower growth implied by the company’s forward guidance and awaited a larger catalyst at an upcoming investor forum [20].

These examples underscore the importance of context. The numbers tell part of the story, but understanding the broader picture often requires digging into management’s remarks and forward-looking statements.

Regulatory decisions often arrive unexpectedly, and when they do, markets tend to overreact. This overreaction creates a gap between the initial shock and the eventual price correction, leading to inefficiencies. Let’s dive into how antitrust rulings, FDA surprises, and SEC actions contribute to these market disruptions.

Antitrust enforcement in the early 2020s added layers of regulatory risk, impacting corporate valuations and slowing down deal activity. For example, stricter Hart-Scott-Rodino (HSR) rules implemented in February 2025 pushed merger filings to a five-year low of just 89 in March 2025. These new rules demanded an additional 68 to 121 hours of preparation per filing, creating a significant bottleneck for companies [21][23].

A standout case occurred in November 2025, involving GTCR and Surmodics. The FTC challenged their merger, citing potential price increases of 28% for Biocoat products and 13% for Surmodics products - arguments based on outdated revenue data. Judge Jeffrey Cummings dismissed the FTC's claims, highlighting their failure to consider recent bidding data and production constraints. Once the deal was approved, the temporary mispricing caused by the FTC's challenge was corrected [22].

By February 2026, a federal court in Texas overturned the controversial 2024 HSR rules. The Ferguson-led FTC chose not to appeal, signaling a shift in approach:

"The era of 'blocking for the sake of market structure' has been replaced by a pragmatic, remedy-focused approach that is actively fueling a surge in multi-billion dollar mergers." - MarketMinute, Dow Theory Letters [21]

This decision had an immediate impact. Domestic merger values jumped nearly 40% year-over-year in Q1 2026, as investors began factoring in shorter timelines and fewer regulatory hurdles [21]. These examples highlight how regulatory actions can introduce volatility and create opportunities for savvy investors.

FDA decisions often lead to sharp, unpredictable stock movements. Before a PDUFA date, biotech stocks typically gain 20–40% as investors anticipate approval. But the actual announcement can go either way [24].

Take uniQure (QURE) in March 2026. After the FDA raised concerns about data integrity for its Huntington's disease therapy, AMT-130, the company’s stock plummeted 42%, from $15.63 to $9.03. Just days later, shares rebounded 51% to $21.55 after Dr. Vinayak Prasad, the FDA official critical of the drug, unexpectedly resigned. This dramatic swing happened in less than a week, driven entirely by a personnel change [26].

Another example is Compass Pathways (CMPS). On April 20, 2026, shares surged 42% (from $6.66 to $9.46) after President Trump signed Executive Order 14401, which directed the FDA to accelerate research into psychedelic drugs. Jefferies analyst Andrew Tsai summarized the market's reaction:

"President Trump is providing an official stamp of validation to the class in the form of an executive order, reassuring us that the FDA/HHS/White House's support of psychedelics is real/actionable." [25]

These cases underscore that FDA-related stock movements aren’t just about clinical outcomes. Personnel shifts, executive orders, and policy changes can be just as impactful, creating opportunities for investors who can anticipate or react to these surprises.

When the SEC announces an investigation or a company issues a restatement, the market often overreacts. For “Big R” restatements - where prior financials are declared unreliable - stocks typically drop 15% to 40% immediately and underperform the broader market by 5% to 15% annually for the next two to three years [27].

The Archer-Daniels-Midland (ADM) case in January 2026 demonstrates how cooperation can mitigate financial damage. The SEC accused ADM of inflating its Nutrition segment through improper intersegment transactions. Despite the severity of the misconduct, the company faced a relatively modest $40 million penalty. Analysts attributed this to ADM’s proactive steps, including conducting an internal investigation and canceling executive bonuses for implicated leaders, a move often recommended by a fractional CFO to restore fiscal accountability [28].

"The $40 million fine is relatively modest compared to some previous enforcement penalties... They're trying to send a message to other companies that even if the facts look bad, you do the right thing at the company and we'll be easier." - Francine McKenna, Author of The Dig [28]

The takeaway? When a company announces an SEC investigation, the market often prices in the worst-case scenario. Investors who evaluate the company’s level of cooperation - such as voluntary disclosures or executive pay adjustments - may identify recovery opportunities before the final settlement is reached.

Event-Driven Market Inefficiencies: Key Data Points & Patterns

Bankruptcies, spin-offs, and special distributions often create chaos in the market, leading to forced selling and temporary price dislocations. These scenarios can reward investors who dive deeper into the details that most others ignore.

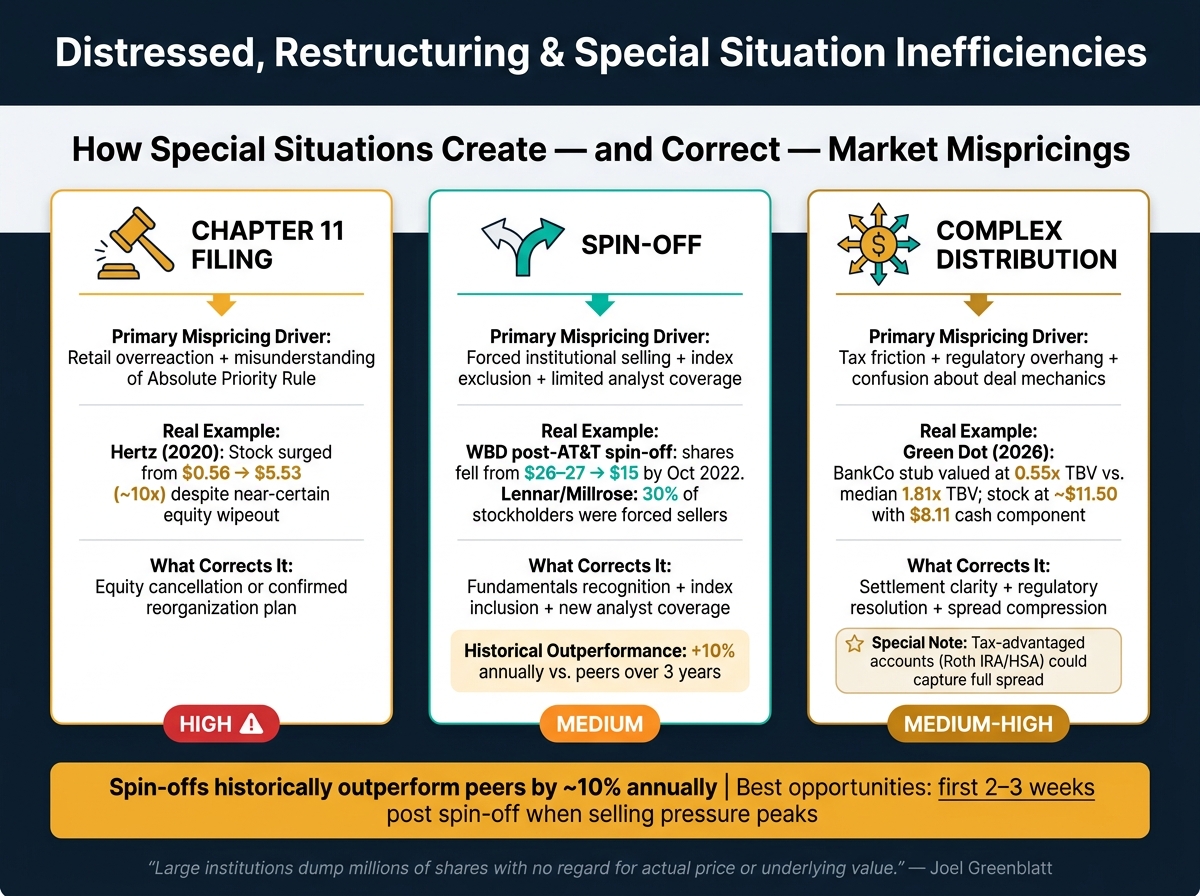

Chapter 11 filings often lead to common investor mistakes, especially among retail participants. Many view low share prices as a bargain without understanding the Absolute Priority Rule under Bankruptcy Code § 1129. This rule mandates that senior creditors must be fully paid before equity holders receive anything. In most cases, equity is completely wiped out.

Take Hertz as an example. After filing for Chapter 11 in May 2020, its shares dropped to $0.56. However, fueled by social media hype, the stock skyrocketed to $5.53 by June 8, 2020 - nearly a 10x jump - despite the equity being almost certainly worthless [29]. This wasn't about fundamentals; it was a misunderstanding of bankruptcy law combined with retail enthusiasm.

Moving on, spin-offs present a different kind of market inefficiency.

Spin-offs often lead to mispricings, not because of the underlying business but due to structural reasons. When a spin-off occurs, investors who hold shares in the parent company may end up with shares in a business that doesn't align with their investment strategy.

For instance, when AT&T spun off WarnerMedia to merge with Discovery in April 2022, AT&T’s dividend-focused investors suddenly found themselves holding shares in Warner Bros. Discovery (WBD), a leveraged company that didn’t pay dividends. This mismatch led to significant selling, driving WBD shares from $26–$27 at the start to $15 by October 2022 [31].

Similarly, the Lennar / Millrose Properties spin-off in March 2026 followed a familiar pattern. Lennar’s S-11 filing revealed that 30% of its stockholders were index funds or institutional investors required to sell Millrose shares immediately, as the new entity didn’t qualify for major indices [30]. Joel Greenblatt summed it up well:

"The result [of a spin-off] is that large institutions and index funds dump millions of shares into the market with no regard for the actual price or underlying value of the business." [30]

The data supports this. Over a three-year period, spin-offs have historically outperformed peers by about 10% annually, with parent companies outperforming by around 6% annually [31][32]. The best opportunities typically arise within the first two to three weeks after the spin-off, when selling pressure is at its peak.

Special distributions, with their intricate deal structures, also create unique pricing inefficiencies.

Special situations involving complex distributions - where cash, stock, and new entities are issued simultaneously - often confuse investors, leading to mispricing.

A good example is the Green Dot Corporation case from late 2025 to 2026. Green Dot announced that Smith Ventures would privatize its fintech business for $8.11 per share in cash, while its banking unit would merge into a new public entity ("BankCo"). In March 2026, the stock was trading around $11.50, implying that BankCo’s equity stub was valued at just 0.55x TBV, far below the median of 1.81x TBV [15]. This discount stemmed partly from a Federal Reserve consent order and partly from taxable arbitrage desks demanding a higher premium to offset immediate tax liabilities on the cash component. However, investors holding shares in tax-advantaged accounts like Roth IRAs or HSAs could capture the full spread, avoiding the tax-related discount [15].

Here’s a quick summary of how these inefficiencies arise and what typically corrects them:

| Situation Type | Primary Mispricing Driver | What Corrects It |

|---|---|---|

| Chapter 11 Filing | Retail overreaction; misunderstanding of Absolute Priority Rule | Equity cancellation or confirmed reorganization plan |

| Spin-Off | Forced institutional selling; index exclusion; limited analyst coverage | Recognition of fundamentals; index inclusion; new analyst coverage |

| Complex Distribution | Tax friction; regulatory overhang; confusion about mechanics | Settlement clarity; regulatory issues resolved; spread compression |

The scenarios discussed in this article don’t just apply to hedge funds or arbitrageurs - they’re also highly relevant for growth-stage companies planning major actions like fundraising, acquisitions, or public disclosures.

When growth-stage companies announce funding rounds, partnerships, or acquisitions, their valuations can shift almost instantly. Investors quickly assess the likelihood of success, which directly impacts the company’s cost of capital. For example, deals requiring regulatory approval typically take around 150 days to close and succeed 78% of the time, while friendly cash deals close in just 75 days with a 92% success rate [2]. If your deal falls into a riskier category, investors will factor that into their valuation, whether you’re prepared or not.

Forced-flow events, like Nvidia’s 3% drop on May 29, 2026 - caused by MSCI index rebalancing - can temporarily disrupt valuations before prices stabilize again [4]. For growth-stage companies nearing index inclusion thresholds or undergoing restructuring, understanding this dynamic is critical. Knowing when forced selling ends could mean the difference between reacting with panic or seizing an opportunity.

At this stage, limited analyst coverage can also delay how quickly the market processes new information. This lag creates risks, especially during fundraising or M&A processes, when investors or acquirers might anchor to outdated valuations. These examples highlight why having advanced financial models is crucial to avoid event-driven valuation missteps.

To handle these challenges, precise financial modeling is a must. It’s about understanding who is trading your stock, why they’re trading, and when the pressure will ease - this level of precision is non-negotiable.

"A manager who cannot describe the forced flow precisely - who is selling, why they must sell, when the selling stops - they are underwriting a narrative, not a mechanism." - Resonanz Capital [33]

Specialized advisory services, such as those offered by Phoenix Strategy Group, can help simplify these complex situations. They transform event-driven uncertainties into actionable insights by calculating deal probabilities, testing capital structures against potential delays, and structuring earnings disclosures to minimize information gaps. The ultimate aim? To ensure that when a significant event occurs, your financial data tells a clear and credible story - fast enough to avoid the prolonged mispricing issues that have impacted other companies highlighted in this article.

The examples in this article highlight a recurring theme: markets are often slow to respond. Whether it's an earnings surprise, a merger announcement, or a regulatory decision, prices rarely adjust fully on the first day. Research shows that about 40% of the total price response to a significant earnings surprise happens after the first 48 hours [5]. This delayed adjustment can continue for as long as 60 trading days.

M&A events follow similarly predictable patterns. For example, target companies in mergers typically see gains of +20% to +35% in Cumulative Abnormal Returns (CAR), while acquiring firms experience losses ranging from -1% to -6% [3]. The structure of the deal matters greatly - friendly, cash-based deals close 92% of the time within 75 days, while hostile takeovers succeed only 65% of the time and often take around 180 days to finalize [2].

"Relying solely on the day-one reaction to an earnings beat often means leaving a significant portion of the total return on the table." - Finexus [5]

For growth-stage companies, timing and communication play a critical role. The way key data is presented - such as the number of quantitative details included in a press release - can significantly influence how quickly the market reacts. Announcements with fewer standout details tend to result in longer periods of price drift, which can delay market understanding [5]. This can be particularly risky during fundraising or M&A processes, where swift comprehension is crucial for achieving optimal business valuations.

To tell the difference between mispricing and actual bad news, it's crucial to look at the market's reaction in context. For instance, if a stock experiences a sharp price increase following an acquisition announcement but quickly drops back down, this could point to mispricing rather than a lasting shift in value.

You can use tools like event studies to compare actual returns against expected ones or to evaluate abnormal returns. Additionally, sudden price gaps or reactions that seem out of sync with the company's fundamentals often suggest mispricing. On the other hand, a steady decline in price might indicate genuine negative news impacting the stock.

When trading merger arbitrage spreads, the key deal terms to focus on are the offer price, deal probability, and time to close. These elements play a crucial role in shaping the spread, influencing the risk of the deal falling through, and determining potential returns. Grasping these factors is essential for evaluating the trade's risk versus reward and making smarter investment choices.

Growth-stage companies can avoid valuation drift by actively managing market expectations and increasing transparency. Sharing clear details about growth plans, financial projections, and strategic goals helps ensure investors have a realistic understanding of the company's trajectory. In addition, maintaining proactive investor relations, providing thorough disclosures about synergies and strategic efforts, and delivering consistent messaging can reduce uncertainty. This approach helps stabilize investor perceptions and minimizes the potential for event-driven inefficiencies following major announcements.