Published on

June 11, 2026

When raising funds internationally, compliance with U.S. and global regulations is non-negotiable. Cross-border seed rounds, involving investors across countries, introduce complex legal and tax obligations. Key points to focus on:

Failing to meet these obligations can result in penalties, investor rescission rights, and due diligence issues in future funding rounds.

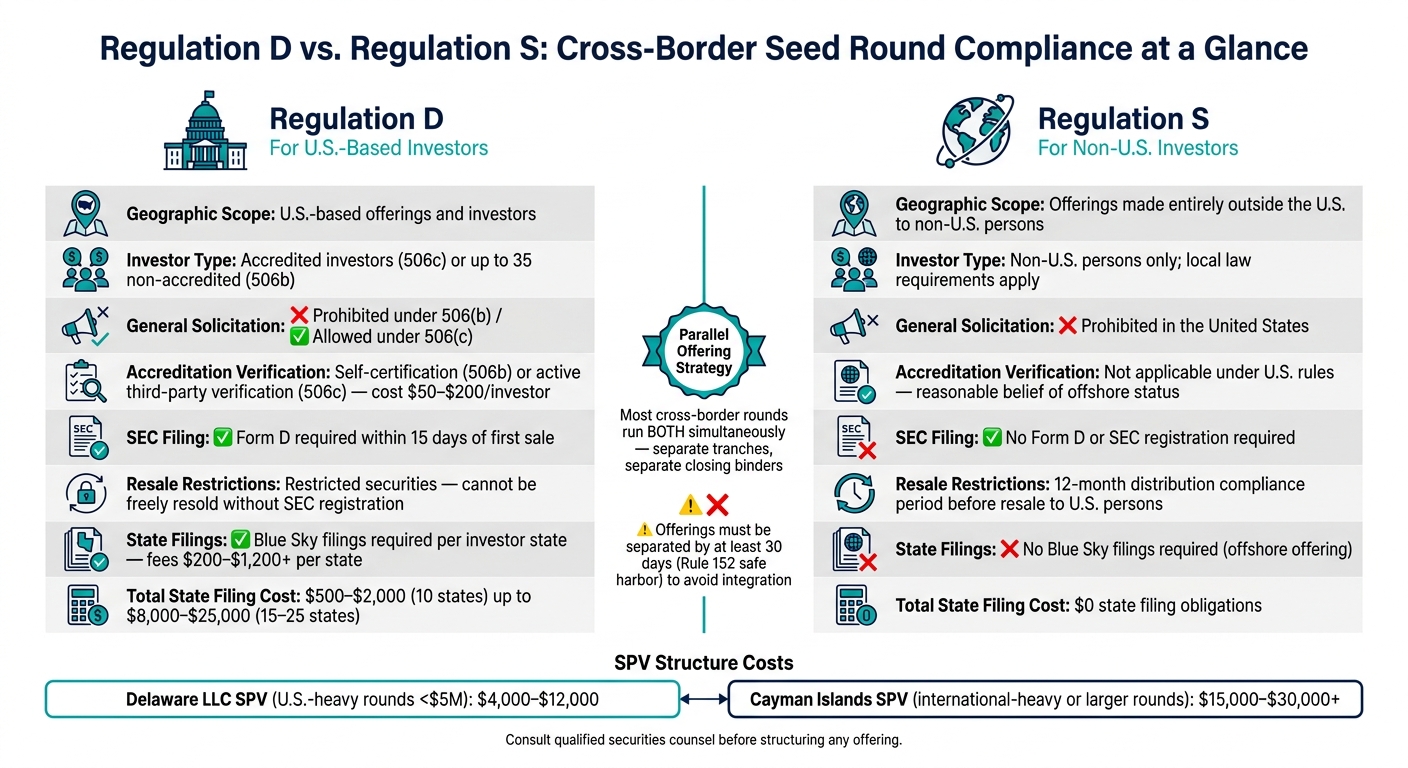

Regulation D serves as the primary legal framework for U.S. startups to raise capital without registering their securities with the SEC. Most seed rounds leverage either Rule 506(b) or Rule 506(c) under this regulation.

The key distinction between the two rules lies in how startups can market their offerings. Rule 506(b) prohibits general solicitation, meaning you can only approach investors with whom you already have a pre-existing relationship. Under this rule, you can accept funds from an unlimited number of accredited investors and up to 35 sophisticated non-accredited investors. On the other hand, Rule 506(c) allows public advertising but mandates that all investors undergo independent verification to confirm their accredited status. Self-certification isn’t enough here, and the cost of third-party verification typically ranges from $50 to $200 per investor [5].

Startups must file Form D with the SEC via its EDGAR system within 15 calendar days of receiving their first committed investment (when a subscription agreement is signed, and funds are wired). This filing is necessary for all funding instruments, including SAFEs and convertible notes [5].

"Form D is not a pre-approval - it's a notice to the SEC that you're relying on a Regulation D exemption." - Promise Legal [5]

Failing to meet the filing deadline can lead to hefty penalties. For instance, in December 2024, a CEO and fractional CFO faced civil penalties of $175,000 and $85,000, respectively, for late filings [5].

For international fundraising efforts, Regulation S offers an alternative framework, complementing Regulation D for U.S.-based investors.

Regulation S provides a safe harbor for companies raising capital outside the United States. It applies to offerings made entirely offshore to non-U.S. persons and doesn’t require a Form D filing or SEC registration [4].

To qualify, the entire offer and sale must occur outside the U.S., with no marketing efforts targeting U.S. residents. Securities sold under Regulation S are subject to a 12-month lock-up period before they can be resold into U.S. markets, falling under Category 3 restrictions [4].

"If you're not offering shares to U.S. persons, and you structure things properly, you can tap global capital markets with fewer headaches and faster timelines." - Growth Turbine [4]

Federal compliance is just one piece of the regulatory puzzle. After submitting Form D to the SEC, companies must also address state-level requirements, often referred to as "Blue Sky" filings, for each state where an investor resides. While the National Securities Markets Improvement Act (NSMIA) prevents states from blocking Rule 506 offerings, they can still require notice filings, such as copies of Form D, along with filing fees. These filings are usually due within 15 days of the first sale to a resident in that state and are often processed through the NASAA Electronic Filing Depository (EFD), which supports about 40 states and territories [5][6].

Filing fees vary widely depending on the state. Here’s a quick look at some examples:

| State | Approximate Filing Fee | Notes |

|---|---|---|

| New York | $1,200 | Highest fee; requires offering memorandum |

| Texas | $300 | Active enforcement division |

| California | $300 + $50/investor | Requires annual renewal filings |

| Massachusetts | $300 | Requires Form U-2 consent to service of process |

| Florida | $200 | Flat fee |

| Delaware | $0 | No notice filing required for Rule 506 |

| Colorado | $0 | No notice filing required for Rule 506 |

If you’re raising funds from investors in about 10 states, total state filing fees typically range from $500 to $2,000. For larger rounds involving 15–25 states, the costs, including state fees and related services, can climb to between $8,000 and $25,000 [5][6]. In contrast, Regulation S offerings avoid state filing obligations entirely since they occur offshore.

Together, these federal and state requirements create the framework for compliance in U.S. and cross-border fundraising. Understanding these layers is essential for preparing the necessary documents and ensuring a smooth process for your seed round.

Regulation D vs. Regulation S: Cross-Border Seed Round Compliance Guide

Before diving into a cross-border funding round, it's crucial to understand the types of investors you're dealing with. In the U.S., an individual qualifies as an accredited investor if they meet one of two financial benchmarks: earning over $200,000 annually (or $300,000 combined with a spouse) for the past two years, or having a net worth exceeding $1 million, excluding their primary residence [8]. Additionally, since 2020, the SEC has broadened the definition to include licensed securities professionals holding a Series 7, 65, or 82 license, as well as officers and directors of the issuing company [8].

Interestingly, these financial thresholds have remained unchanged since 1982, meaning their real value has diminished over time due to inflation [8].

For non-U.S. investors, the rules are different. Under Regulation S, the focus shifts to determining whether someone qualifies as a "U.S. person." This includes individuals residing in the U.S. and entities organized under U.S. law [7]. However, if an investor is located outside the U.S. when placing their buy order and the offer isn't directed at anyone in the U.S., they can participate under Regulation S without triggering U.S. registration requirements [7].

It’s worth noting that even a single U.S.-based investor in a funding round can bring the entire offering under U.S. securities regulations [1].

Once you’ve classified your investors, structuring the offering to comply with various regulatory frameworks is the next step. The most effective way to raise funds from both U.S. and international investors is by running two parallel offerings: one under Regulation D for U.S. investors and another under Regulation S for non-U.S. investors [1]. This approach ensures each group of investors adheres to its own compliance rules and avoids unintentionally subjecting the entire round to U.S. registration requirements.

To implement this, founders often use separate tranches or set up distinct SPVs (Special Purpose Vehicles). For early-stage rounds under $5 million with a predominantly U.S.-based angel investor pool, a Delaware LLC SPV is a cost-effective option, typically costing between $4,000 and $12,000. For larger rounds or those with a primarily international investor base, a Cayman Islands SPV is more suitable, though pricier, with costs ranging from $15,000 to $30,000 or more [1].

However, timing matters. The integration doctrine can treat two offerings as a single one if they occur too close together. Rule 152 provides a 30-day safe harbor, meaning offerings separated by at least 30 calendar days are generally not considered integrated [8]. Failing to observe this gap could jeopardize your exemption entirely.

"The integration doctrine... can blow up your exemption if you're not careful." - Joe Wallin, The Startup Law Blog [8]

Once the structure is in place, it’s equally important to address transfer and resale restrictions tied to these offerings.

Both Regulation D and Regulation S come with specific resale restrictions that founders must clearly communicate to investors from the outset.

For Regulation D, securities are considered "restricted," meaning they cannot be freely resold unless registered with the SEC or an exemption applies [9]. Under Regulation S, non-U.S. investors face a 12-month distribution compliance period during which they cannot resell their securities to U.S. persons unless registered or exempted [7]. Ignoring these restrictions can lead to serious consequences, including the loss of the exemption and potential investor refunds [8].

"Break the rules, and you lose the exemption. That's not a fine - it can mean your entire offering was illegal, your investors can demand their money back, and you face potential liability." - Joe Wallin, Founder, TheStartupLawBlog.com [8]

Here’s a quick comparison of how the key rules differ across offering types:

| Feature | Rule 506(b) | Rule 506(c) | Regulation S |

|---|---|---|---|

| Target Investor | U.S. Accredited (+ up to 35 non-accredited) | U.S. Accredited only | Non-U.S. persons only |

| General Solicitation | Prohibited | Allowed | Prohibited in the U.S. |

| Verification | Self-certification usually suffices | Mandatory active verification | Reasonable belief of offshore status |

| Resale Limits | Restricted securities | Restricted securities | 12-month distribution compliance period |

| SEC Filing | Form D required | Form D required | No SEC filing required |

When raising funds internationally, it's not just about U.S. compliance - local filing and regulatory requirements in each jurisdiction can add layers of complexity. To avoid future headaches, founders must ensure their offerings are fully compliant in every relevant country. For U.S. state-level filing details, refer back to the earlier "Federal vs. State Filing Requirements" section.

"Every unfiled Form D, every state without a notice filing... becomes a liability that surfaces during due diligence for the next funding round." - Alex Lubyansky, Esq., Acquisition Stars [3]

Each country has its own unique rules. For instance, Germany requires notarized documents and registration with the Handelsregister (commercial register). India mandates approvals under RBI/FEMA regulations and compliance with Overseas Direct Investment (ODI). Israel involves obtaining an ITA tax ruling and addressing Section 104H rollover tax issues, while Singapore requires clearance from the IRAS and filings with ACRA [2].

| Origin Jurisdiction | Typical Legal Cost (2025–2026) | Timeline | Main Complication |

|---|---|---|---|

| UK | $30,000–$50,000 | 6–10 weeks | Section 431 elections, EMI schemes |

| Canada | $30,000–$45,000 | 6–8 weeks | T2057 rollover, option migration |

| Germany | $70,000–$120,000 | 12–20 weeks | Exit tax, notarization, Handelsregister |

| India | $80,000–$150,000+ | 16–30 weeks | RBI/FEMA approval, ODI compliance |

| Israel | $40,000–$70,000 | 8–12 weeks | ITA tax ruling, Section 104H rollover |

| Singapore | $35,000–$55,000 | 6–10 weeks | IRAS clearance, ACRA filings |

Once these obligations are addressed, founders must also consider how currency controls impact the transfer of funds.

Currency controls often complicate cross-border fundraising. For example, India’s RBI/FEMA and ODI requirements can stretch closing timelines to 16–30 weeks and drive legal costs beyond $150,000 [2]. Similarly, Germany’s exit tax rules and mandatory notarization can extend the process to 12–20 weeks [2].

Interestingly, many leading U.S. funds - such as Index, Accel, Founders Fund, a16z crypto, and Sequoia - have adjusted their approach. Instead of requiring an immediate Delaware flip, they now wire seed capital directly into non-U.S. entities, including those in the UK, Canada, Germany, Israel, and Singapore [2]. Founders can use a side letter to commit to restructuring at a later stage, usually during Series A. This approach allows the round to close and funds to transfer without triggering an expensive reorganization mid-fundraise.

"The Delaware flip is no longer a prerequisite for a non-US founder raising a US seed round in 2026. Index, Accel, Founders Fund, a16z crypto, and Sequoia all wire into UK, Canadian, German, Israeli, and Singaporean entities at seed." - Causo Hub [2]

For founders facing strict currency controls, planning for extended timelines and higher costs is essential. Additionally, negotiating with lead investors to cover part of future flip costs - typically between $20,000 and $30,000 - through a side letter can alleviate financial pressure [2].

Given the complexities of cross-border fundraising, local legal expertise is indispensable. While U.S. corporate counsel can handle federal and state filings, they’re not equipped to manage jurisdiction-specific issues like Germany’s exit tax, India’s FEMA filings, or the UK’s Section 431 elections. Local attorneys are crucial for navigating tax events and regulatory filings that may arise during cross-border restructuring.

Even something as seemingly straightforward as a side letter can create unforeseen tax liabilities under local laws if not carefully reviewed. As one expert points out:

"Get the side letter wording reviewed by a tax lawyer in your home jurisdiction before signing, not just by your corporate counsel." - Causo Hub [2]

Firms like Orrick, Wilson Sonsini, and Cooley specialize in coordinating cross-border seed rounds and can connect founders with trusted local counsel in key regions.

For founders tackling these regulatory challenges, combining expert legal guidance with smart financial planning is a game-changer. At Phoenix Strategy Group, we help growth-stage companies navigate the complexities of cross-border fundraising and ensure compliance every step of the way.

Getting the paperwork right is a must for any cross-border funding round. Errors or missing documents can cause delays and even lead to legal trouble later on.

For every cross-border raise, several core documents are essential: subscription agreements (the main contract between the company and the investor), investor accreditation questionnaires (to confirm an investor's accredited status under Regulation D), and restrictive legends on stock certificates or book entries (to indicate that the securities are unregistered and come with resale restrictions). Additionally, filing Form D with the SEC is mandatory within 15 calendar days of the first sale. Importantly, this 15-day clock starts when an investor signs a SAFE or subscription agreement, not when funds are deposited into your account [10].

To avoid delays, secure SEC EDGAR access early on by completing the Form ID process. Since the notarization and verification steps can take over a week, any delay in obtaining EDGAR credentials could mean missing the 15-day filing deadline [10].

Once these documents are in place, a structured approach to closing ensures smoother compliance.

A thorough closing binder is critical for due diligence. This binder should include all subscription agreements, investor questionnaires, transfer confirmations, and filing receipts, organized by investor and jurisdiction. Institutional investors and acquirers often look for gaps, such as missing Form D filings or state Blue Sky notices. Any oversight in these areas could lead to rescission rights, allowing investors to demand their money back [3].

Good recordkeeping builds on the federal and state filing processes. For Rule 506 offerings, state notice filings can cost anywhere from $5,000 to $15,000 [3]. If you're working with a large group of investors, filing in all 50 states upfront can help you avoid missing a jurisdiction. Late filings are far more expensive to fix, with remediation costs often reaching $15,000 to $40,000 in legal fees and penalties [10].

Set an internal "Day 10" alert after the first investor signs. This gives you a five-day cushion to gather all necessary data and file Form D before the federal deadline [10]. If your offering stays open, remember to file an amended Form D annually on the anniversary of the original filing.

"Missing [the Form D] deadline triggers compliance issues that surface during institutional due diligence, later financing rounds, or acquisition negotiations - often killing deals that took months to structure." - James Wright, Author, Angel Investors Network [10]

Understanding the differences between Regulation D and Regulation S is essential for compliance in cross-border funding rounds. Proper documentation not only ensures regulatory compliance but also clarifies the distinct obligations under each framework.

| Feature | Regulation D (U.S. Focus) | Regulation S (Foreign Focus) |

|---|---|---|

| Geographic Scope | U.S.-based offerings and investors | Offerings made outside the U.S. to non-U.S. persons [8] |

| Filing Requirement | Form D within 15 days of first sale [10] | Generally exempt from U.S. registration/filing [8] |

| Investor Eligibility | Accredited (506c) or limited non-accredited (506b) [10] | Non-U.S. persons; local law requirements apply [8] |

| General Solicitation | Prohibited under 506(b); allowed under 506(c) [10] | Prohibited in the United States [8] |

| Accreditation Verification | Self-certification (506b) or "reasonable steps" (506c) [10] | Not applicable under U.S. rules [8] |

Most cross-border seed rounds involve parallel offerings - using Regulation D for U.S. investors and Regulation S for foreign investors. Each tranche should be documented separately, and keeping these investor groups distinct in your closing binder isn't just smart - it’s a compliance necessity to maintain the exemptions.

When navigating cross-border seed rounds, it's essential to follow specific filing rules to avoid future headaches. Make sure Form D and Blue Sky filings are submitted on time, and keep your Regulation D and Regulation S tranches completely separate. For foreign investors, ensure the offering is conducted entirely offshore, collect IRS Form W-8BEN-E to prevent a 30% FATCA withholding, and screen all participants against the OFAC Specially Designated Nationals list before accepting their investment [11].

One often-missed issue is how a growing remote team can impact compliance. If employees in new states receive equity, this could trigger additional Blue Sky analysis under Rule 701, which increases your compliance workload [3].

These requirements highlight why professional guidance is critical.

"The gap between when startups start issuing securities and when they engage securities counsel creates a compliance deficit that compounds over time." - Alex Lubyansky, Esq. [3]

The rules for cross-border raises are complex, covering SEC regulations, CFIUS reviews, FATCA reporting, and even local foreign registration requirements. Managing this while scaling a business can feel overwhelming. Phoenix Strategy Group helps founders align their capital strategy with compliance needs, ensuring you meet filing deadlines, properly structure your investor base, and maintain a clean compliance record heading into Series A.

Take proactive steps to avoid compliance pitfalls. Start by auditing past rounds to ensure all filings were completed on time. Engage local counsel early for foreign fundraising efforts, and consider negotiating side-letter terms tied to key milestones instead of fixed dates. Many firms, including Index, Accel, and Sequoia, now accept these milestone-linked side letters, which can save you anywhere from $30,000 to $120,000 in early legal fees [2].

The 15-day Form D deadline starts ticking based on whichever of these two events happens first: when the issuer secures a binding commitment from an investor, or when the investor is irrevocably committed to the investment. This timeline is designed to ensure adherence to regulatory rules for reporting seed funding activities.

To keep Regulation D and Regulation S activities separate, it’s crucial to maintain a clear distinction between them. Regulation S covers offers and sales made outside the U.S. to non-U.S. persons, while Regulation D is focused on U.S.-based investors.

Key steps to ensure compliance include:

By carefully coordinating these efforts, you can ensure both regulations are followed properly without risking compliance issues.

The most common reasons for delays in cross-border seed closings include state Blue Sky filing requirements, specific investor filings required by certain jurisdictions, and the timing involved in completing legal and tax compliance steps. If these issues aren't handled quickly, they can push the timeline back by weeks - or even months.