Published on

July 2, 2026

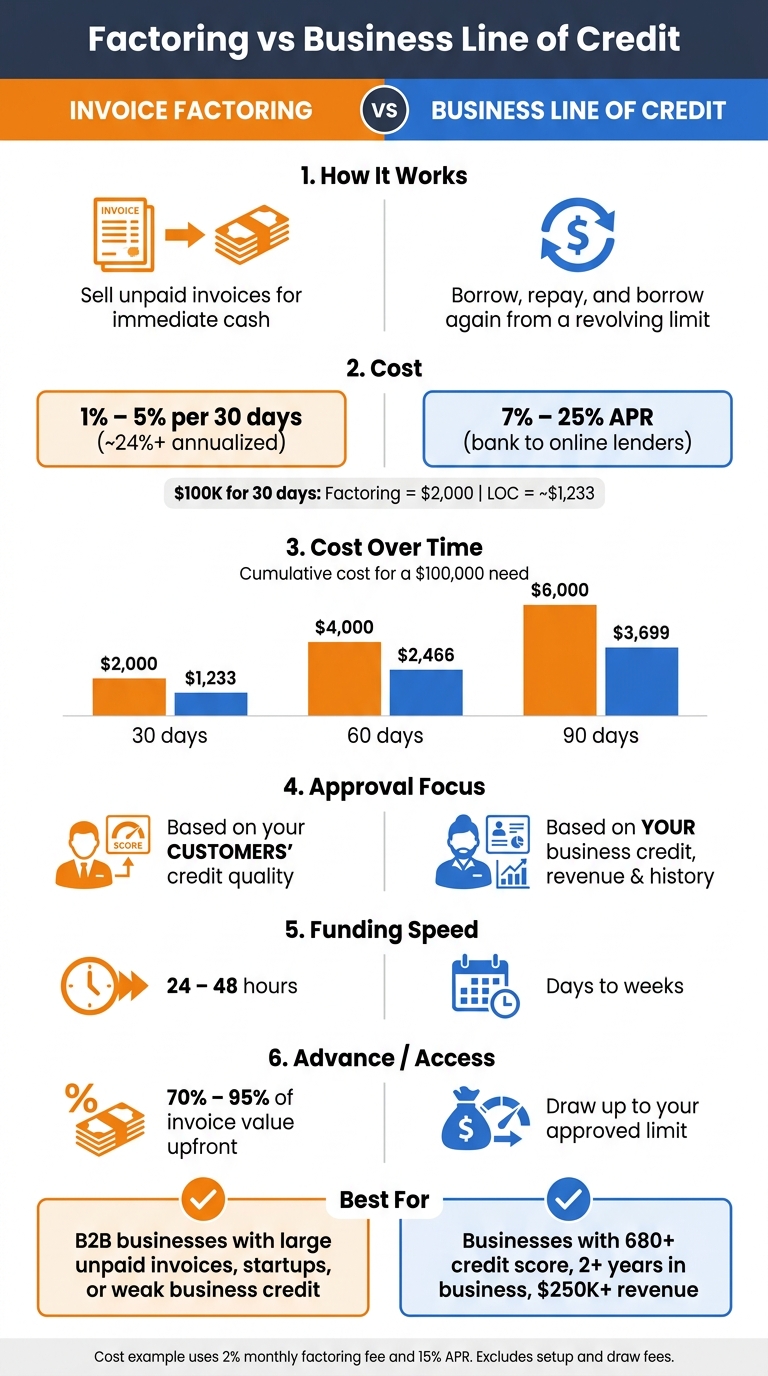

If you can qualify for both, a business line of credit usually costs less. In the example from the article, a $100,000 need costs about $1,233 for 30 days at 15% APR with a credit line, versus $2,000 with factoring at 2% per 30 days.

Here’s the short version:

My takeaway: if you need cash now and have solid B2B invoices, factoring can work. If you have strong financials and need repeat access to working capital, a fractional CFO can help you determine if a credit line will cost less over time.

Factoring vs Business Line of Credit: Cost & Qualification Comparison

| Criteria | Factoring | Business Line of Credit |

|---|---|---|

| How you get cash | Sell invoices | Borrow from a revolving line |

| Upfront access | Often 70% to 95% of invoice value | Draw what you need up to your limit |

| Cost style | Usually 1% to 5% per 30 days | Usually 7% to 25% APR; some lenders charge more |

| Cost over time | Goes up as customers pay later | Builds daily on the amount drawn |

| Approval focus | Your customers’ ability to pay | Your business credit and financials |

| Funding speed | Often 24 to 48 hours | Days to weeks, depending on lender |

| Customer contact | Factor may collect payment | You usually keep collections in-house |

| Best fit | Cash tied up in invoices | Repeat short-term cash needs |

For me, the choice comes down to cost, approval, and timing. That’s the whole decision in plain English.

Factoring is pretty simple: you sell an unpaid invoice to a factoring company, often called the factor, and get most of that cash upfront.

In most cases, the factor sends you 70% to 95% of the invoice's face value within 24 to 48 hours after you submit it [5][1][4]. The rest is the reserve. The factor holds that amount until your customer pays the invoice directly to them. After that happens, the factor sends you the reserve minus its fee.

That fee usually falls between 1% and 5% per 30-day period [5][1]. Some factors also offer non-notification arrangements, but they usually cost more [5][1][6].

A business line of credit works more like a reusable pool of funds. The lender gives your business a maximum limit based on things like revenue, credit score, and profit. You borrow only what you need, when you need it.

The big detail is this: interest accrues only on the outstanding balance, not on the full credit limit [3][1]. And once you repay what you used, you can draw from that amount again.

Bank lines often come with rates from 7% to 15% APR, while online or alternative lenders may charge 15% to 40% APR [1][6]. Banks may also charge an unused line fee of 0.25% to 0.50% annually on the amount you didn't use [1]. Unlike factoring, your customers stay out of the process.

These two tools solve different cash-flow problems.

There's also a scaling difference. Factoring capacity tends to grow with your invoice volume, while a credit line usually grows only if the lender approves an increase [1][2]. That difference plays a big part in why the costs don't look the same in the next section.

Factoring often costs 1% to 5% of the invoice value for every 30 days the invoice stays open, plus wire or ACH fees, lockbox or servicing fees, setup fees, monthly minimums, and termination fees [7][1][5]. On top of that, many providers add transaction and service charges.

The main thing that moves cost is time. Factoring fees stack by 30-day periods, so the longer your customer takes to pay, the more you spend. A 2% monthly fee on a $100,000 invoice costs $2,000 after 30 days and $4,000 after 60 days. That's why your average Days Sales Outstanding (DSO) matters so much when you're trying to estimate the full cost.

A line of credit works differently. You pay interest only on the amount you draw. Typical rates fall between 7% and 25% APR, while online or alternative lenders may charge 10% to 40%+ APR [7][1][6]. There can also be extra fees, including an origination fee of $500 to $5,000 depending on facility size, an annual renewal fee, a per-draw fee, collateral monitoring fees, and late fees [1].

Banks may also charge a 0.25% to 0.50% annual unused-balance fee on the part of the line you don't use [1]. Still, because interest builds daily only on what you've borrowed, line-of-credit costs usually scale in a more predictable way than factoring fees.

Put simply: the longer the wait between sending an invoice and getting paid, the more factoring can stretch past the cost of a credit line.

For a $100,000 short-term cash gap, duration changes the math in a big way. Using a 2% monthly factoring fee and a 15% APR line of credit, the table below shows the base cost of a $100,000 draw over 30, 60, and 90 days. It does not include setup, draw, renewal, or unused-balance fees [7][6].

| Payment Timing | Factoring Total Cost | Line of Credit Total Cost |

|---|---|---|

| 30 days | $2,000 | ~$1,233 |

| 60 days | $4,000 | ~$2,466 |

| 90 days | $6,000 | ~$3,699 |

Factoring cost = 2% × $100,000 per 30-day period. LOC cost = $100,000 × 15% APR × (days/365).

So even with the same $100,000 need, a 30-day gap and a 90-day gap can lead to very different dollar costs. A 2% monthly fee works out to about 24% annualized, which can be higher than many line-of-credit rates [7][6].

Cost isn't the whole story, though. Approval rules and how fast your customers pay often decide whether the lower-cost option is even on the table.

The biggest difference comes down to who gets judged.

With factoring, approval depends mostly on your customers' credit. The factor wants to know whether your customers are likely to pay valid invoices. Your own profit, time in business, or weak credit history matters less. That’s why factoring is often open to startups, companies with poor credit, or businesses growing faster than cash flow can keep up with [6][1].

A credit line is the opposite. The lender looks at your business, not your customers. That usually means your financial performance, credit score, debt load, and operating history all get reviewed. Banks often want 2+ years in business and a 680+ credit score. Alternative lenders may accept lower scores, but they usually charge more [1][6]. So yes, a credit line can cost less - but only if you can get approved.

| Approval factor | Factoring | Credit line |

|---|---|---|

| Underwriting focus | Credit quality of customers and validity of invoices | Business financial performance, credit score, debt load, and operating history |

| Documentation required | A/R aging reports, invoices, customer contracts | Financial statements, tax returns, bank statements |

| Time to approval | Often within 24–48 hours once invoices are verified [1] | Days for alternative lenders to weeks for banks [1] |

| Funds available | 80% to 95% of eligible invoices | Revolving limit tied to borrowing base |

| Who collects from the customer | Customers may remit directly to the factor | Business usually keeps control of invoicing and collections |

Once approval is handled, the next thing that hits your wallet is timing.

With factoring, you usually get most of an approved invoice up front. Then, when your customer pays, the rest gets released after fees are taken out [1]. There’s a simple upside here: availability tends to grow with sales. More eligible invoices usually means more cash access, and you often don’t need to go back through a new approval process each time [5][2].

A credit line works in a more fixed way. Your limit is set at approval and tied to a borrowing base, often a percentage of eligible receivables or other collateral. Not every invoice counts. Older invoices, especially those more than 90 days past due, disputed invoices, or receivables tied to one customer that make up more than 30% to 50% of total A/R can shrink what you’re able to draw [1][2].

So while factoring can expand as sales grow, a credit line usually stays put unless the lender agrees to revisit it. If you want more room later, you’ll often have to go through underwriting again.

This is where the math starts to shift.

With factoring, fees usually climb the longer your customer takes to pay. Some factors tack on extra charges after the first 30 days [1]. In plain English: slow-paying customers can make an already pricey option cost even more.

A credit line behaves differently. If customers pay late, you may need to keep the line outstanding for longer, so interest keeps building each day on the balance. But the rate itself usually doesn’t jump in the same way factoring fees can.

There’s one more twist. Non-notification factoring tends to cost more, usually with a 0.25% to 1% premium added to the standard fee [1].

That’s why payment timing matters so much. The easier approval that comes with factoring can be helpful, but if customers drag their feet, the extra cost can pile up fast.

Factoring makes sense when speed matters more than price and a bank line isn't available. It's often a fit for B2B companies with big receivables, especially in staffing, trucking, and construction. Staffing agencies are a good example: they often pay workers weekly but don't get paid by clients until later [6].

That timing gap can get painful fast. So when receivables are growing faster than bank access, factoring can help fill the gap [1][2].

If you can qualify for both options, cost usually becomes the deciding factor.

If you qualify, a credit line is usually the lower-cost option. It also lets you keep invoicing and collections in-house. That's a key difference from standard factoring, which usually notifies the customer [1][5].

For businesses with stable revenue, steady payment cycles, and bank-friendly financials, a revolving credit line is often the better long-term tool. That usually means a 680+ credit score, 2+ years in business, and $250,000+ in annual revenue [1].

Here’s the simple breakdown.

| Business situation | Better fit | Why |

|---|---|---|

| Urgent cash need with large unpaid B2B invoices | Factoring | Faster access, especially when customer payments are slow |

| Strong financials and repeat short-term borrowing needs | Credit line | Lower borrowing cost and more control over collections |

| Weak business credit but creditworthy customers | Factoring | Approval often depends more on customer credit than company credit |

| Stable operations with predictable cash conversion | Credit line | Flexible revolving access can be cheaper over time |

| Keep collections and customer contact in-house | Credit line | Business usually keeps invoicing and collections in-house |

The right pick comes down to how fast you need cash, what it costs, and what you can qualify for.

Maybe. It comes down to your industry and how the deal is set up.

In trucking, staffing, and construction, factoring is common and usually creates little friction.

In fields where it’s less common, a factor collecting payment directly can make customers think your business is under financial stress. A non-notification setup keeps things private, but it usually costs more.

With a business line of credit, your repayment doesn't change if customers pay late. That means you take on the risk of slow payment or nonpayment.

Invoice factoring works differently. It's built to deal with late customer payments.

With recourse factoring, you may need to buy back an unpaid invoice.

With non-recourse factoring, the factoring company may take the loss instead, but you'll usually pay higher fees for that tradeoff.

It comes down to what the provider looks at.

A business line of credit is usually tied to your company’s financial health. In many cases, that means a credit score of 680+, at least two years in business, and a profitable track record.

Factoring works differently. It leans more on your customers’ creditworthiness than your own. So even if you’re a startup, you may still qualify if you have clean, undisputed B2B or B2G invoices and clients with solid credit that pay on net terms.