Published on

January 10, 2026

Managing seasonal inventory financing is all about balancing cash flow gaps caused by upfront inventory costs and delayed revenue. Here’s how you can handle it effectively:

Creating a flexible cash flow and inventory forecast that aligns with your seasonal demand is essential for navigating the challenges of timing and liquidity.

Managing seasonal inventory isn’t just about predicting sales - it’s about addressing the timing gap between when you pay suppliers and when you actually make sales. Suppliers typically need payment 30–90 days before you sell the goods[5]. For many retailers, the holiday season alone can account for up to 80% of their annual revenue[3]. That means you’ll need to allocate cash for inventory well ahead of the busiest time of the year.

"Seasonality isn't a sales forecast problem - it's a timing challenge", says the Zenstatement Intelligence Team[5].

To bridge this gap, implement a rolling 13-week cash flow forecast that updates weekly with data from sales, purchase orders, and operations[5]. This dynamic approach provides better visibility into cash outflows compared to static monthly forecasts, allowing you to align inventory planning with real-time cash flow projections.

This improved cash flow visibility lays the foundation for smarter, data-driven inventory management.

Instead of relying on industry averages, use multi-year sales data to uncover consistent seasonal trends[4]. One useful method is calculating a seasonality index by dividing each month’s average sales by the overall monthly average. An index above 1.0 signals higher-than-average demand[1]. Dive deeper by forecasting cash impact at the SKU cluster level, factoring in contribution margins, inventory turnover rates, and anticipated return rates, rather than taking a broad average across your catalog[5].

To handle unexpected demand surges or supply chain hiccups, plan for inventory levels that are 20% to 30% above your projections[4]. Additionally, track key metrics like Days Inventory Outstanding (DIO), broken down by product class, to identify SKUs that tie up liquidity. Keep an eye on your Cash Application Lag - the time it takes for cash from a transaction to hit your bank account[5]. These insights help pinpoint where your working capital is getting stuck during the seasonal cycle.

Once you’ve built robust forecasts, take steps to safeguard your liquidity against potential risks.

Use probabilistic simulations to model "Cash Flow at Risk" (CFaR) and identify the worst-case liquidity scenarios before the season begins[5]. This analysis helps determine the cash buffer you’ll need before committing to large purchase orders. Additionally, employ Return-Adjusted Revenue Forecasts (RARF) to account for expected returns by SKU class, ensuring your cash projections aren’t overly optimistic[5].

"You don't feel an inventory decision when it's made - you feel it two quarters later when the markdowns and cash gaps hit", warns the Zenstatement Intelligence Team[5].

Streamline your inventory by cutting low-performing SKUs that tie up cash unnecessarily[3]. Focus your most detailed weekly forecasts on Category A items - the top 4–5 SKUs that generate 89% of your annual value. For lower-value inventory, simpler forecasting methods will suffice[1]. This targeted approach keeps your process efficient while protecting the cash flow tied to your most critical products.

Once you've laid the groundwork with accurate cash flow forecasts, the next step is to align financing strategies with your seasonal business cycles.

After identifying gaps in your cash flow, consider financing options that adapt to your revenue fluctuations instead of locking you into fixed monthly payments. For instance, 60% of small retailers face cash flow challenges during peak seasons[7].

One flexible option is revenue-based financing, which adjusts repayments based on daily sales. This means smaller payments during slower months and larger ones during busy periods[6]. Another solution is purchase order (PO) financing, where lenders pay suppliers directly. Typically, this comes with a cost of 1.5% to 6% of the purchase order value for terms ranging from 30 to 90 days. This option allows you to secure inventory for high-demand periods without draining your working capital[7][2].

Revolving credit is another useful tool, giving you access to funds as needed while charging interest only on the amount you use[6][7]. Advance rates for revolving credit depend on factors like inventory turnover and industry risks. For example, consumer electronics businesses might get 60% to 70% of their inventory's wholesale value, while apparel businesses - due to seasonal risks - might see rates closer to 50% to 65%[7].

Understanding the true cost of capital is essential. To do this, convert factor rates into APR using this formula: APR ≈ (Factor Rate - 1) / Term in Years × 100. For example, a factor rate of 1.3 over six months translates to an APR of roughly 60% - much higher than the 7% to 18% APR on a traditional revolving line of credit[7].

Your rolling 13-week cash flow forecast can be a game-changer. Businesses that maintain this type of forecast are 40% more likely to avoid cash shortfalls[7]. Use these forecasts to secure financing ahead of time, reducing the stress of last-minute decisions during busy periods[3]. Additionally, if your suppliers offer early-payment discounts - like 2% off for paying within 10 days (2/10 Net 30) - a line of credit can help you take advantage of these savings, which often outweigh borrowing costs[7].

To safeguard your cash flow, secure financing during stable periods when your balance sheet is in good shape - not when you're already under pressure[3]. Start discussions with lenders 6–8 weeks before placing seasonal orders[4]. Keep in mind that lenders might decline applications if your inventory sits unsold for more than six months or if a single customer accounts for over 40% of your revenue[7]. Cleaning up your balance sheet ahead of time can improve your chances of approval.

Watch out for hidden fees that can inflate your financing costs. Also, ensure that the financing term matches your inventory turnover. For example, a U.S. auto dealership typically turns inventory every 60 to 70 days[7], so opting for a 12-month loan might unnecessarily tie up funds long after the inventory has been sold.

Getting your forecasting right starts with cleaning up your historical sales data. Take 6–12 months of sales history and strip out any anomalies, like one-time bulk orders or promotional spikes. Then, organize the data into consistent weekly or monthly periods for better clarity[1]. This step lays the groundwork for accurate predictions.

Once your data is cleaned up, it’s time to prioritize. Use ABC analysis to rank your SKUs based on their annual consumption value. Typically, Category A items - the top 70–80% of your inventory value - require close, weekly monitoring. Meanwhile, Category C items, which contribute the least, can be reviewed less frequently. This approach ensures your focus stays where it matters most.

To prepare for seasonal demand, calculate a seasonality index. This involves dividing each month's average sales by the overall multi-year average. Any value above 1 indicates higher-than-usual demand[1]. Multiply your baseline forecast by this index to estimate how many units you’ll need during peak seasons. For many retailers, the holiday period alone can drive up to 80% of their annual revenue[3].

To handle sudden demand spikes, calculate safety stock using this formula:

Safety stock = (Max daily sales × Max lead time) − (Avg daily sales × Avg lead time).

Then, determine your reorder point:

Reorder point = (Avg daily sales × Lead time) + Safety stock[1].

These calculations ensure you’re ordering at the right time and maintaining enough buffer inventory to avoid stockouts during busy seasons.

Once you’ve nailed down your inventory forecasts, the next step is figuring out which products to finance. Use margin data to map each SKU based on sales volume and profitability. This helps you identify best-sellers that deserve investment and weed out low performers that tie up your capital[3].

Don’t forget to factor in the total carrying cost - this includes warehouse fees and any interest from loans used to finance your inventory[3].

As Pursuit Lending explains, "Knowing these added costs will motivate you to keep a tighter control on unnecessary ordering"[3].

Leverage your inventory turnover data during supplier negotiations. If you can show strong sales performance for specific SKUs, you’ll have a better case for negotiating longer payment terms during slow periods or securing discounts for early payments when your cash flow is strong[3]. Plus, organized turnover data can improve your chances of getting financing, as lenders often consider these metrics when approving credit for seasonal inventory builds.

Heading into the peak season, businesses often face a significant cash crunch due to the upfront investment required for inventory. This can be particularly challenging for those working with international manufacturers, where deposits are typically required 4–6 months ahead of delivery, putting additional strain on working capital[2].

One way to ease this burden is by negotiating payment terms that match your revenue cycle. For example, you could arrange seasonal payment agreements where a small deposit secures production, and the remaining balance is deferred until after your peak sales period[2]. This approach helps ensure smoother cash flow management when it matters most.

Waiting too long to address cash flow needs can lead to reliance on expensive funding options like merchant cash advances or high-interest credit cards, which can significantly eat into your profit margins[3]. Instead, take proactive steps to secure liquidity buffers well in advance - ideally 3–6 months before the busy season. Establishing a revolving line of credit when your financials are strong ensures you have access to affordable funds when you need them most[3].

As Pursuit highlights, "Projecting your funding needs and securing financing in advance will reduce your financing cost and boost your profitability"[3].

Additionally, plan for an inventory buffer of 20–30% to handle unexpected demand spikes or supply chain delays[7]. This not only keeps your operations running smoothly but also strengthens your position in supplier negotiations, helping you avoid last-minute purchases at inflated prices. Diversifying your supplier base is another smart move to reduce risks from regional disruptions during critical periods[2]. For businesses with international supply chains, tools like forward contracts or multi-currency accounts can help stabilize costs and protect against currency fluctuations during long production cycles[2].

For more insights on aligning supplier terms with cash flow needs, check out Phoenix Strategy Group.

Integrated FP&A systems bring the entire financial planning and analysis (FP&A) cycle full circle by turning accurate forecasts into actionable, real-time insights.

Relying on manual spreadsheets during seasonal peaks can leave businesses vulnerable to critical blind spots. In fact, over 60% of small retailers and wholesalers face cash flow challenges during peak buying seasons because their data is often weeks old by the time it reaches decision-makers [7]. Integrated FP&A systems solve this by instantly linking cash flow, inventory movement, and payment data - eliminating the delays caused by manual processes. These systems also incorporate real-time signals for settlements, returns, and chargebacks [5]. This means you’ll have access to current cash positions and near-term forecasts, giving you the clarity needed to address potential cash flow risks before they escalate.

Switching from static monthly reports to rolling 13-week liquidity forecasts is a game changer. These rolling forecasts update daily with the latest order and demand data [5][7]. Businesses using this approach are 40% more likely to avoid cash shortfalls and can often negotiate better terms with lenders thanks to their ability to demonstrate forward-looking financial insights [7].

"Seasonality isn't a sales forecast problem - it's a cash choreography problem." - ZenStatement [5]

Integrated systems streamline complex processes like invoice matching, reconciliation, and currency adjustments. By automating these workflows, businesses reduce data delays and prevent profit loss that often goes unnoticed in manual spreadsheets [5][9]. When finance and operations teams operate from a shared, centralized data source, inventory replenishment plans can align seamlessly with treasury’s liquidity forecasts [5][9]. This alignment allows businesses to treat large seasonal purchase orders as strategic investments. Using ROI models and risk-adjusted yield assumptions, you can determine which inventory purchases will deliver the best financial outcomes [5].

Real-time visibility into "cash-in-motion" equips CFOs to spot liquidity pressures weeks - or even months - before seasonal sales peaks [5]. By mapping cash sources, flows, and tracking points, businesses can close transparency gaps [5]. Weekly "cash reality checks" are another critical tool: compare expected cash with actual net receipts, and investigate any variances greater than 5% [5]. When SKU-level sell-through data is tied to the timing of cash collection, it becomes an invaluable early warning system for potential liquidity issues [5].

Phoenix Strategy Group specializes in helping growth-stage companies implement integrated financial systems that offer this kind of real-time visibility across their entire cash cycle.

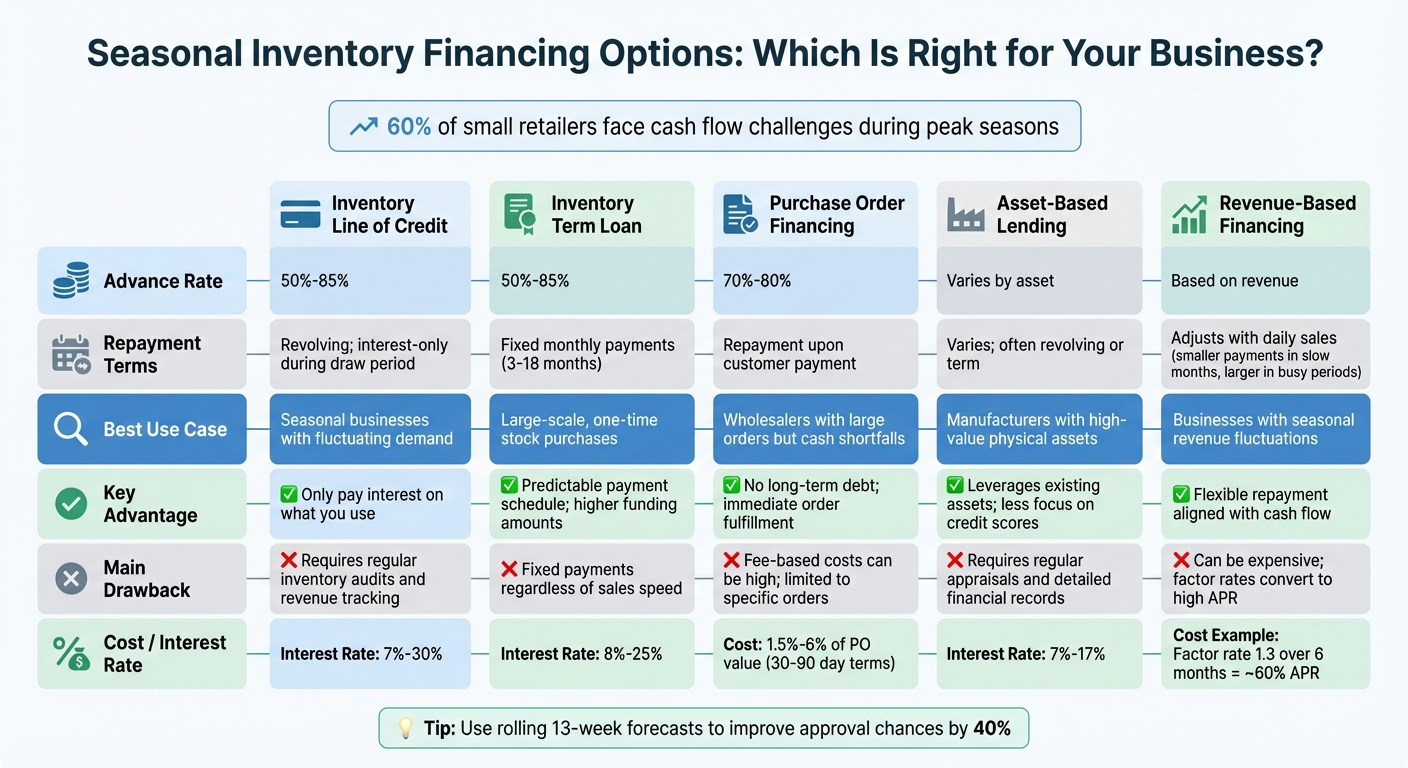

Seasonal Inventory Financing Options Comparison Chart

Selecting the right inventory financing option depends on factors like your cash flow patterns, the size of your purchases, and how quickly you turn over inventory. Each financing type offers unique terms, repayment structures, and costs tailored to different business needs.

Inventory lines of credit provide flexibility, letting you draw funds as needed and pay interest only on what you use. Interest rates range between 7% and 30% [8]. However, this option requires regular inventory audits and consistent revenue tracking [8].

Term loans deliver a lump sum upfront, making them ideal for large, one-time inventory purchases, especially before busy seasons. Payments are fixed, with terms spanning 3 to 18 months and interest rates from 8% to 25% [8]. While the predictable payment schedule aids budgeting, you’ll need to meet your monthly obligations regardless of how quickly your inventory sells.

The table below breaks down key differences in terms, use cases, and benefits for each financing option:

| Financing Option | Advance Rate | Repayment Terms | Best Use Case | Key Advantage | Main Drawback |

|---|---|---|---|---|---|

| Inventory Line of Credit | 50%–85% [8][11] | Revolving; interest-only during draw period | Seasonal businesses with fluctuating demand | Only pay interest on what you use [8][10] | Requires regular inventory audits and revenue tracking [8] |

| Inventory Term Loan | 50%–85% [8][11] | Fixed monthly payments (3–18 months) [8] | Large-scale, one-time stock purchases | Predictable payment schedule; higher funding amounts [8][10] | Fixed payments regardless of sales speed [8] |

| Purchase Order Financing | 70%–80% [2] | Repayment upon customer payment [8] | Wholesalers with large orders but cash shortfalls | No long-term debt; immediate order fulfillment [8][2] | Fee-based costs can be high; limited to specific orders [8] |

| Asset-Based Lending | Varies by asset [8] | Varies; often revolving or term [8][12] | Manufacturers with high-value physical assets | Leverages existing assets; less focus on credit scores [8][12] | Requires regular appraisals and detailed financial records [8] |

Purchase order financing covers 70% to 80% of a specific order’s value [2]. The lender pays your supplier directly, making it a great choice for fulfilling large seasonal orders when cash is tight. Meanwhile, asset-based lending allows you to use a variety of collateral - like inventory, accounts receivable, or equipment - making it a solid option if you have valuable assets but limited liquidity. Interest rates for this type of financing typically range from 7% to 17% [8].

Managing seasonal inventory financing requires careful planning to balance upfront expenses with delayed revenue streams. The FP&A strategies discussed earlier can help you time inventory purchases, marketing expenses, and payment settlements effectively, minimizing the risk of cash shortages during peak periods.

Using tools like rolling 13-week forecasts, assessing SKUs based on profit margins and turnover, and securing financing aligned with your cash cycle can significantly reduce financial risks. By incorporating models such as Cash Flow at Risk (CFaR), businesses can anticipate worst-case scenarios and prepare accordingly before they occur [5].

The results of these efforts become evident over time. Inventory decisions often impact financial performance two quarters later, either as markdowns or cash flow challenges [5]. This is why FP&A support is particularly critical for growth-stage companies navigating seasonal fluctuations. External expertise can bring advanced forecasting methods, clean up inconsistent data, and establish liquidity buffers to manage unexpected demand surges or supplier disruptions.

For businesses aiming to implement such strategies, Phoenix Strategy Group provides specialized FP&A services. Their offerings include advanced forecasting, cash flow modeling, and strategic oversight to ensure real-time insights into seasonal performance. With their support, companies can adapt quickly to shifting market conditions, turning seasonal challenges into opportunities for steady growth.

To manage cash flow effectively for seasonal inventory, start by reviewing 2–3 years of historical sales and inventory data. This helps pinpoint seasonal patterns and trends. With this information, build a straightforward 12-month cash flow model in a spreadsheet. Include key elements like projected sales, costs, operating expenses, and any financing needs. To make the model more accurate, apply seasonal multipliers to account for fluctuations during peak and slower periods.

Keep a close eye on cash inflows and outflows, particularly during high-demand times, and update your forecast monthly to reflect current conditions. If your forecast indicates potential cash shortages ahead of peak seasons, consider securing financing options, such as a credit line or an asset-based loan, well in advance. This proactive strategy helps ensure you have the funds needed to maintain liquidity and meet inventory demands throughout the year.

To bridge cash flow gaps during busy seasons, businesses have several financing options designed to meet seasonal demands.

For businesses with significant inventory, asset-based lending (ABL) allows borrowing against the value of that inventory. Similarly, floor-plan financing is useful for high-value, trackable items like vehicles or equipment. Another option, inventory consignment financing, shifts upfront costs to suppliers until the goods are sold, easing immediate financial pressure.

Maintaining a disciplined cash reserve can also serve as a no-cost buffer for routine expenses. Phoenix Strategy Group can assist in identifying the right mix of financing solutions to match your seasonal needs and long-term growth plans.

To make smarter seasonal inventory decisions and reduce financial risks, start by diving into 2–5 years of historical sales data. Look closely at monthly or weekly sales trends to identify patterns, like spikes or dips during specific times of the year. These insights can help you build a demand forecast that aligns with your business’s growth expectations.

Once you’ve got your forecast, connect your inventory purchases with financing options, such as asset-based loans or credit lines. Borrow only what’s necessary to cover peak seasons. Don’t forget to maintain safety stock to account for unexpected demand shifts. Regularly track key metrics like inventory turnover and cash flow to ensure your strategy stays on track. By updating your forecast each season with real sales data, you can fine-tune your approach, avoiding both overstocking and running out of stock.