Published on

February 25, 2026

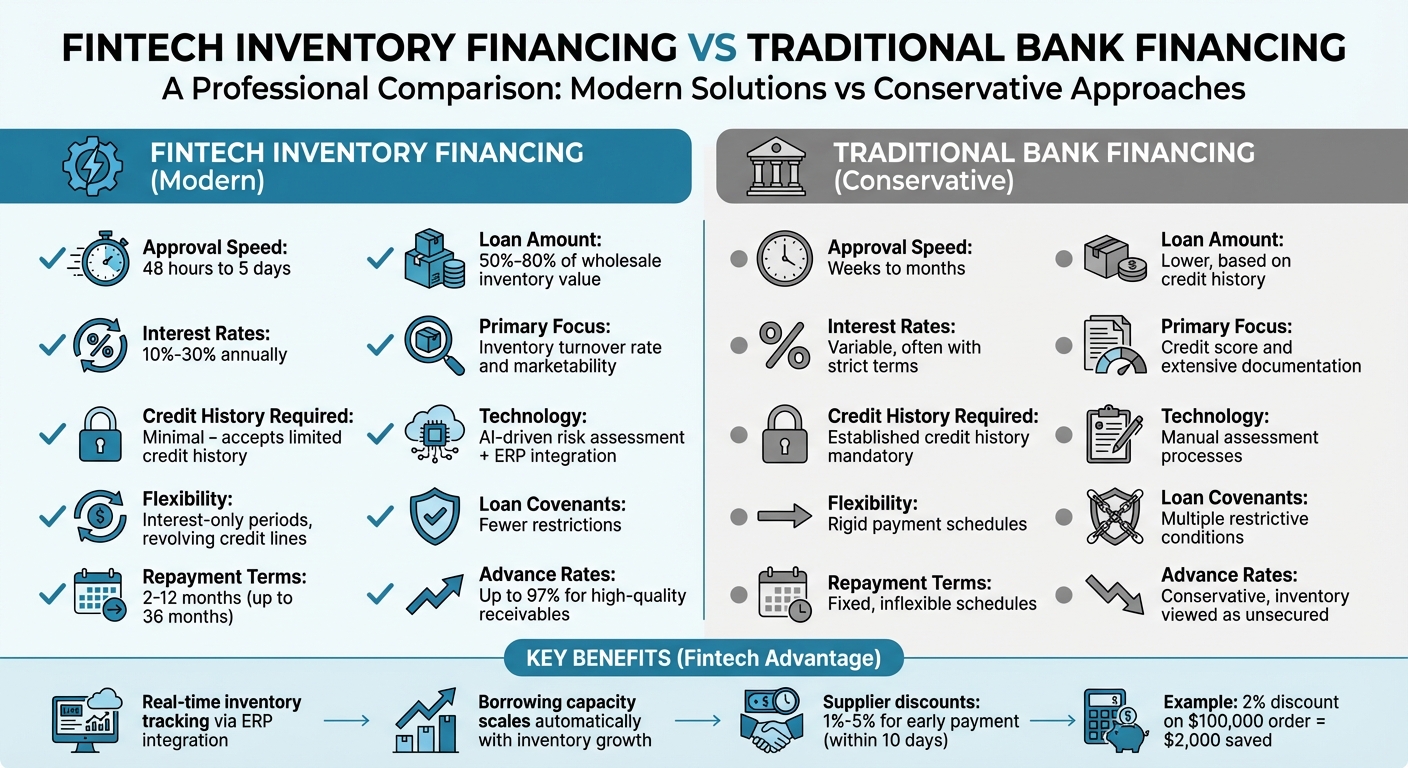

Fintech inventory financing is a way for businesses to secure loans or credit using their inventory - such as raw materials, work-in-progress, or finished goods - as collateral. Unlike banks, fintech lenders focus on the value and marketability of your inventory rather than your credit history. This method provides faster access to funds (typically within 48 hours to 5 days), making it ideal for manufacturers facing cash flow gaps or needing to scale operations.

This financing model helps businesses maintain liquidity, strengthen supplier relationships, and expand without draining cash reserves. By integrating fintech platforms with ERP systems, companies can track inventory in real time and optimize borrowing capacity. Pairing this with expert financial planning ensures that funds are used effectively to support growth and profitability.

Fintech vs Traditional Bank Inventory Financing Comparison

Fintech platforms have transformed the loan approval process, cutting down waiting times dramatically. Instead of enduring weeks - or even months - for approval, manufacturers can now secure capital in just days. Many fintech providers guarantee payouts within 48 hours [3], and some streamline the entire setup process to as little as 7 to 10 days [8]. By leveraging ERP integration and AI-driven analytics, these platforms quickly assess inventory value and associated risks.

Unlike traditional banks, which often view inventory as an "unsecured" risk and demand extensive documentation, established credit history, and broad collateral, fintech lenders take a different approach. They prioritize what truly matters: how quickly your inventory moves and its wholesale value. This means even businesses with limited credit history or a shorter track record can qualify if their stock demonstrates strong marketability. This flexibility allows manufacturers to act swiftly on opportunities - whether that’s purchasing raw materials ahead of a shortage or fulfilling a large retail order without depleting cash reserves.

In addition to quick approvals, fintech lenders provide competitive costs and adaptable financing terms.

Beyond speed, fintech inventory financing stands out by tailoring repayment schedules to align with a business's sales cycles. Unlike rigid payment plans, these structures often include interest-only periods, followed by a "bullet" payment once the inventory is sold [5]. This approach helps preserve working capital during the manufacturing phase, when cash flow is often tight. Revolving credit lines, another popular option, charge interest only on the amount borrowed [5]. Typical annual interest rates range from 10% to 30% [3], making them a more budget-friendly alternative to merchant cash advances, which can soar to APRs between 40% and 200% [3].

Quick access to funding can also unlock immediate savings. Many suppliers offer early payment discounts - typically 1% to 5% for payments made within 10 days [8]. These discounts can often outweigh the cost of financing. For instance, a 2% discount on a $100,000 order saves $2,000, which might exceed the interest paid on a short-term loan. Additionally, bulk purchasing enabled by ready capital lets manufacturers negotiate lower per-unit costs, further improving profitability.

Another key advantage is scalability. As your inventory or receivables grow, your borrowing capacity adjusts automatically [4]. There’s no need to reapply or renegotiate terms, which is a game-changer during seasonal peaks or periods of rapid growth. Fintech lenders also impose fewer loan covenants [4], giving businesses the freedom to allocate funds as needed without the restrictive conditions often tied to traditional bank loans.

Extended customer payment terms, such as Net-90 or Net-120, can strain supplier relationships, but fintech inventory financing offers a solution. By providing immediate liquidity, these platforms enable businesses to pay suppliers on time - even when waiting on customer payments. This reliability strengthens partnerships, positioning you as a dependable client. Over time, suppliers may reward this consistency with better pricing, volume discounts, or priority access to limited inventory.

Having access to capital also enhances your bargaining power. When you can pay upfront or place bulk orders, suppliers are more likely to offer favorable terms or priority treatment. This creates a ripple effect: reduced input costs improve profit margins, while stronger supplier relationships provide stability, helping businesses navigate market fluctuations more effectively. A real-world example is Pact, a sustainable e-commerce brand, which utilized a structured ABL solution from eCapital in 2025 to bridge cash flow gaps caused by extended customer payment cycles. This additional borrowing capacity allowed the company to manage both payables and growth simultaneously [4].

Fintech platforms take a different approach to inventory evaluation compared to traditional banks. Instead of relying on spreadsheets and rigid rules, they analyze SKU-level data to assess aging and borrowing bases accurately. This allows each product line to receive tailored advance rates. For instance, fast-moving consumer goods might qualify for 80% financing, while slower-moving specialty items may only receive 50%.

A critical metric here is the Net Orderly Liquidation Value (NOLV) - essentially, how much cash could be recovered if the inventory had to be sold quickly. This method factors in storage costs, selling expenses, and market fluctuations during liquidation. Bruce Sayer from eCapital explains, "The turnover rate, or how quickly inventory sells, is a critical factor in valuation. High-turnover inventory is generally more valuable to lenders because it represents a lower risk of becoming obsolete" [2].

Fintech platforms often integrate directly with your ERP or accounting systems. This real-time connection enables them to track sales, margins, and warehouse locations, reducing risks like "double financing", where the same inventory is used as collateral with multiple lenders. AI-driven risk scoring takes this a step further by continuously monitoring Key Risk Indicators (KRIs) and flagging any unusual activity. This automated system has led to a 10% increase in credit facilities due to better risk assessments, while frontline staff have seen a 20% boost in efficiency compared to manual processes [9]. These advancements enable more structured and adaptable financing options.

Manufacturers often rely on inventory-backed revolving credit lines. These allow businesses to draw funds against 50%–80% of their wholesale inventory value [3]. Borrowers can withdraw funds as needed, repay, and borrow again, with interest accruing only on the amount used. As inventory levels change, borrowing capacity adjusts automatically.

Receivables financing is another option, turning outstanding invoices into immediate cash. This can be structured as either an accounts receivable loan (where invoices act as collateral) or factoring (where invoices are sold outright at a discount). For businesses with highly creditworthy customers, advance rates can go as high as 97% [10]. Dynamic discounting provides additional flexibility, letting businesses pay suppliers early in exchange for discounts, helping to manage cash flow more effectively.

For larger purchase orders, Purchase Order (PO) financing comes into play. This funding is specifically for buying inventory to fulfill confirmed orders from creditworthy customers. Often, the lender pays the supplier directly to ensure the funds are used correctly. Asset-Based Lending (ABL) is another option, leveraging a mix of inventory, accounts receivable, equipment, and other assets to maximize credit access. This is particularly useful for manufacturers with a variety of collateral. Once financing is secured, repayment plans are tailored to match sales performance.

Repayment schedules are designed to align with a business's sales cycles. Many arrangements include interest-only periods during manufacturing or storage, followed by principal payments once the inventory is sold. Revolving credit lines only charge interest on the borrowed amount, with annual rates typically ranging from 10% to 30% [3].

Repayment terms generally range from 2 to 12 months, though some agreements can extend up to 36 months depending on the type of inventory and its turnover rate [1]. Revenue-based repayment models offer even more flexibility by tying payments directly to daily sales. This means payments decrease during slower periods, helping businesses avoid cash flow issues during seasonal downturns or unexpected market shifts. This flexibility ensures operations can continue smoothly without draining financial reserves.

Implementing fintech inventory financing requires a structured approach. Here's how to get started and make the most of this financing option.

Start by analyzing your inventory metrics. This includes calculating your inventory turnover ratio, which can help you secure better financing terms. Additionally, identify seasonal demand peaks to manage cash flow more effectively [1][3][7].

Consider your product mix when evaluating financing options. Items that are stable and non-perishable often make the best collateral. Typically, financing covers 50% to 80% of the wholesale value, though some providers may go as high as 90% [6][1][7]. Don’t forget to factor in carrying costs, such as warehousing, insurance, and management expenses, to ensure financing aligns with your budget [6]. Lastly, determine the purpose of the financing - whether it’s to take advantage of bulk discounts, fulfill large orders, or smooth out seasonal cash flow fluctuations [11][3].

Once you have a clear understanding of your inventory and funding needs, the next step is finding a fintech provider that matches your operational requirements.

Choosing the right fintech partner is crucial. Start by checking system compatibility - the platform should integrate smoothly with your ERP and accounting systems via APIs or native connections. This ensures real-time inventory tracking and eliminates data silos [12].

Examine the provider’s offerings, including advance and interest rates (usually between 10% and 30% annually), repayment terms, and any associated fees [3][7]. For example, in March 2025, Celtic Capital provided a California-based superfood manufacturer with a $2.25 million accounts receivable line of credit, a $376,500 equipment loan, and a $2 million inventory line of credit. This financing package helped the company stabilize operations and continue growing despite financial challenges [7]. Look for providers who tailor their solutions to your industry’s seasonal trends [4].

After selecting a provider, the focus shifts to integrating systems and tracking performance.

System integration is key to leveraging fintech inventory financing effectively. Connect the fintech platform to your ERP and supply chain systems to automate data sharing and track inventory aging schedules [4]. This real-time data sync helps you monitor how financed inventory moves through the sales cycle, aiding repayment decisions [12]. Establish a consistent schedule for collecting and reporting data to keep information actionable [13].

Keep an eye on essential metrics such as inventory turnover rates, cost of funds (total interest relative to borrowed amounts), and repayment timelines [12][15]. Set up automated alerts for anomalies, like sudden drops in turnover or unexpected spending, so you can act quickly [13]. Provide shared dashboards for finance, operations, and supply chain teams to streamline decision-making and align purchases with available financing [12]. Run quarterly scenario simulations to evaluate revenue, repayment, and growth under different conditions, and adjust strategies as needed [14]. To avoid covenant breaches during slower revenue periods, maintain a liquidity buffer equal to at least one month’s average repayments [14].

While fintech inventory financing addresses immediate cash flow needs, financial advisory services - like fractional CFO support, financial modeling, and exit planning - can help businesses achieve long-term growth. These services complement the liquidity provided by inventory financing, ensuring that your growth strategies align with your financial capabilities and lead to improved valuation over time.

Fractional CFOs bring predictive analytics into play to align financing with your cash flow needs. They analyze factors like inventory turnover, seasonal demand, and supplier payment terms to determine the best times and amounts for borrowing. This approach minimizes risks such as borrowing too early or too late, which could result in missed opportunities like bulk purchase discounts. Additionally, fractional CFOs often negotiate supplier terms - typically between 60 to 120 days - to ensure repayment schedules align with your overall cash flow, keeping operations smooth and efficient [16].

Once flexible financing is secured, financial models become essential tools for guiding strategic decisions. These models allow growth-stage manufacturers to simulate various scenarios before making significant inventory investments. For instance, a manufacturer can test how a 15% rise in supplier costs or a 30-day delay in customer payments might impact their financial health. By integrating the Income Statement, Balance Sheet, and Cash Flow Statement, these models provide a clear picture of how inventory acquisitions (assets) and financing obligations (liabilities) will affect cash flow. Sensitivity analyses further help businesses explore how different interest rates or repayment structures could influence long-term profitability [16].

Phoenix Strategy Group specializes in helping manufacturers build scalable operations that enhance valuation, particularly in preparation for future exits. They focus on creating value through measures like internal controls and scalable bookkeeping practices. Rapid growth fueled by inventory financing can strain operations, so these advisory services ensure businesses remain on track. Tools like the Acquisition Readiness Scorecard help manufacturers assess their financial health and identify whether inventory debt might impact valuation. Scenario planning also provides clarity on how changing market conditions could affect repayment capabilities, giving manufacturers the insights they need to plan effectively [16].

Fintech inventory financing provides a way to free up cash tied to inventory without relying on traditional banks. With funding available in as little as 48 hours [3], businesses can tap into scalable revolving credit while keeping inventory levels optimized. This flexibility helps manage payment terms and navigate supply chain shifts with ease. As Bruce Sayer from eCapital explains, "Inventory financing not only addresses the immediate need for liquidity but also facilitates strategic growth initiatives, making these businesses more agile and responsive to market changes" [2].

However, the benefits go beyond improving cash flow. Pairing this type of financing with strategic financial planning can amplify its impact. Professional advisory services, like those offered by Phoenix Strategy Group, provide tools such as fractional CFO services, financial modeling, and growth planning. These services ensure borrowed funds are used effectively - whether it's negotiating supplier discounts, investing in automation, or preparing for future growth opportunities.

By combining flexible financing with expert advisory support, businesses can quickly seize market opportunities while maintaining financial discipline. This approach turns inventory from a financial burden into a strategic asset that drives business expansion.

The key takeaway is clear: leveraging fintech solutions alongside expert guidance transforms inventory financing into a powerful tool for growth. With the right structure and advice, businesses can turn inventory challenges into a competitive edge, setting the stage for long-term success.

High-value, easily identifiable items often serve as collateral in financing arrangements. This includes assets like vehicles, heavy equipment, and inventory that can be appraised and audited. Lending structures such as asset-based lending and floorplan financing frequently center around these types of inventory.

To set up inventory financing, start by linking crucial financial data from your ERP or accounting system. Pay close attention to details like inventory valuation, transaction histories, and account structures - including inventory levels, cost basis, and turnover rates. Additionally, bring in data from your general ledger, accounts receivable, and accounts payable. This integration allows for precise evaluation of inventory value and cash flow, enabling real-time reporting and better-informed financing decisions.

Lenders tackle challenges with slow-moving or at-risk inventory by using financing tools like floorplan financing. This approach allows lenders to keep ownership of the inventory until it’s sold, which helps minimize the risk of obsolescence. They also rely on methods such as SKU rationalization - streamlining product offerings - and demand forecasting to ensure inventory levels align with market needs. To further manage risks, lenders may enforce stricter audits or tighten borrowing terms, ensuring the inventory remains a reliable form of collateral while still supporting manufacturers' cash flow.