Published on

January 10, 2026

When companies merge, preserving and maximizing Net Operating Losses (NOLs) can significantly reduce future tax liabilities. NOLs, which occur when tax-deductible expenses exceed taxable income, are valuable assets in mergers and acquisitions. However, leveraging them requires navigating complex tax rules, including federal Section 382 limitations and varying state regulations.

Key Takeaways:

Action Steps:

Navigating these rules effectively can help companies unlock the full potential of NOLs while avoiding costly compliance issues.

5-Step Process to Maximize NOL Value After a Merger

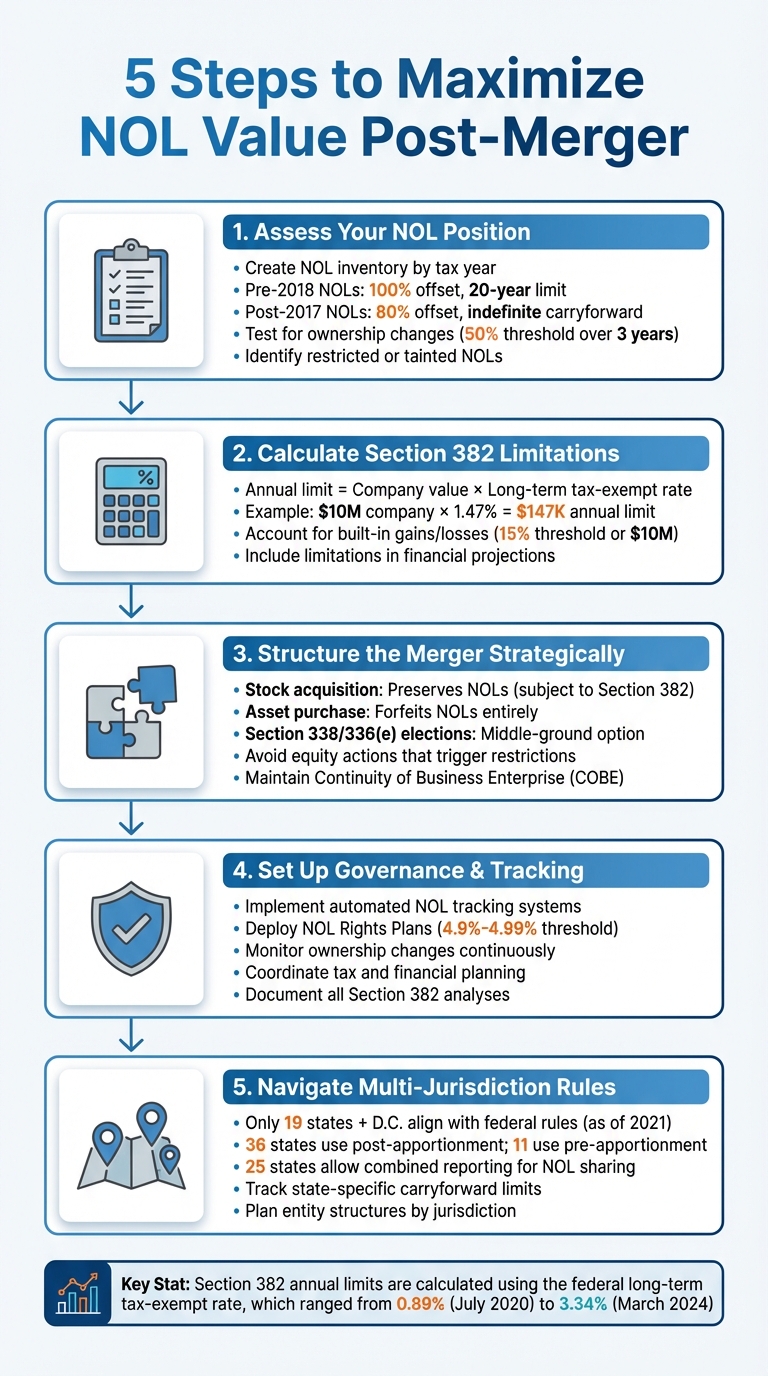

Start by documenting each Net Operating Loss (NOL) by tax year. Divide them into pre-TCJA (Tax Cuts and Jobs Act) NOLs, which allow a 100% offset with a 20-year carryforward period, and post-TCJA NOLs, which allow only an 80% offset but have an indefinite carryforward period [6][8].

Organize this inventory by entity and jurisdiction, keeping in mind that state-specific filing rules may vary [4]. Be sure to include related tax attributes, like disallowed business interest carryforwards under Section 163(j), as these are treated similarly to NOLs under Section 382 limitations [6][3]. Use data from sources such as Form 1120, Schedule K, and financial statements to ensure your inventory is as complete as possible [1][4].

Once your NOL inventory is ready, you can begin analyzing potential ownership changes.

Ownership changes occur when 5-percent shareholders collectively increase their ownership by more than 50 percentage points over a three-year period [6][2]. To evaluate this, review your cap table and track all equity transactions during the designated timeframe [7][2].

Ownership calculations should be based on fair market value rather than just the number of shares, as different stock classes may carry different values [5][7]. Additionally, shareholders owning less than 5% individually may be grouped into a "public group", which can collectively be treated as a single 5-percent shareholder. This aggregation could potentially trigger an ownership change [7].

Once you've identified ownership changes, examine your funding history to determine if any restrictions might impact NOL eligibility. This step is crucial for structuring deals to maintain the value of your NOLs.

Spotting tainted NOLs is essential to preserving their tax value post-merger. Capital contributions made within the two years leading up to an ownership change are presumed to be part of a plan to sidestep Section 382 limitations. These contributions are excluded from the company's valuation under anti-stuffing rules [5][3]. Carefully review your funding history to pinpoint any such tainted capital.

If nonbusiness assets make up more than one-third of total assets, their fair market value must be subtracted from the Section 382 value [3]. Additionally, check for a Net Unrealized Built-In Loss (NUBIL) by comparing the fair market value of your assets to their tax basis. Any built-in losses recognized within five years after the merger will be treated as pre-change losses and subjected to the annual limitation [7][2].

To determine the annual Section 382 limitation, multiply the loss corporation's pre-change fair market value by the long-term tax-exempt rate [9][3]. Use the highest adjusted Federal long-term rate from the three months leading up to the ownership change [5][3].

Higher rates translate to a larger limitation. For example, the rate in July 2020 was 0.89%, while in March 2024, it was 3.34% [2]. Companies nearing an ownership change may strategically time the event during periods of higher rates to secure a larger annual net operating loss (NOL) usage limit [2].

If the annual limitation isn't fully used in a given year, the unused portion can roll forward to increase the following year's limit [5][3]. In the year of the merger, this limitation only applies to the taxable income generated after the date of the ownership change [5][3].

Once this is calculated, consider the role of built-in gains or losses in adjusting these limitations.

When a Net Unrealized Built-In Gain (NUBIG) exists - meaning the market value of assets exceeds their tax bases - the annual limitation can increase. If a pre-change asset is sold within the five-year recognition period, the Section 382 limitation for that year rises by the amount of the Recognized Built-In Gain (RBIG) [5][2][3].

"If the company's asset values are in excess of its adjusted tax basis... it may be able to increase its annual limitation by an additional amount over the five‑year period following the ownership change." - GHJ Advisors [2]

On the other hand, if a Net Unrealized Built-In Loss (NUBIL) is present, recognized losses are subject to it [5][3]. This includes depreciation or amortization tied to periods before the ownership change but recognized afterward. Importantly, NUBIG or NUBIL is treated as zero unless it exceeds the lesser of 15% of the fair market value of assets or $10,000,000 [5][3].

Once you've calculated the annual limitations, these figures should be incorporated into your financial projections. Start by calculating the combined Pre-NOL Cash Taxable Income, which involves summing the income statements and adjusting for acquisition effects [9].

It's critical to verify the expiration dates of the target company's NOLs. If the annual limitation multiplied by the remaining years until expiration is less than the total NOL balance, you'll need to adjust the financial model to reflect a write-down of the NOL asset [9]. For quarterly merger models, dividing the annual Section 382 limitation by four helps accurately offset quarterly taxable income [9].

"Section 382's ordering rules provide that applicable Section 382 limitations will free up business interest carryforwards prior to NOLs and other tax attributes." - Moss Adams [6]

When planning, it's essential to coordinate Section 382 limitations with Section 163(j) limitations. Business interest carryforwards often consume the Section 382 limitation before NOLs, which can have a significant impact on long-term tax planning and cash flow forecasts [6].

Once you've assessed the NOL position and its limitations, the next step is structuring the merger to protect and maximize the value of those NOLs.

The way a merger is structured has a direct impact on the preservation of NOLs. For instance, taxable asset purchases allow you to immediately offset gains from the sale of assets. However, this approach forfeits any unused NOLs entirely [10]. On the other hand, a stock acquisition keeps the NOLs intact, but they become subject to annual limitations under Section 382 [10].

A middle-ground option involves Section 338 and 336(e) elections, which let a stock sale be treated as an asset sale for tax purposes. This strategy works best when the seller can fully apply NOLs against the gain from the asset sale. Meanwhile, the buyer benefits from a step-up in tax basis and increased depreciation deductions, all without being constrained by Section 382 limits [11]. Additionally, selling unwanted target assets with unrealized built-in gains before closing allows the target company to use its NOLs to offset those gains - again, without triggering Section 382’s annual limitation [10].

By carefully selecting the right structure, you set the foundation for managing future equity events and operational adjustments.

Certain equity actions, like issuing or repurchasing stock, can impose further Section 382 limitations [6][1]. If raising capital is necessary, consider issuing “straight” preferred stock - non-voting, non-convertible, and without participation in growth - instead of common stock to avoid triggering an ownership change [10].

It’s also worth noting that the IRS may disallow tax benefits under Section 269 if they believe the primary purpose of the acquisition is tax avoidance. To counter this, ensure that your board-approved plans clearly document non-tax business reasons for the merger. Examples include enhancing supply chain security, expanding into new markets, or increasing borrowing capacity [12]. Acquiring a company in a completely unrelated business sector could raise red flags and increase the risk of a Section 269 challenge [12].

Once the deal structure and equity considerations are in place, the focus shifts to post-merger operations.

The way operations are aligned post-merger can significantly influence the speed at which NOLs are used. In states that permit combined reporting - about 25 states and the District of Columbia as of 2017 - losses can be shared among members of the combined group to offset income from profitable subsidiaries [4].

For federal NOLs, compliance with the Continuity of Business Enterprise (COBE) requirement is critical. This means the acquiring company must either continue the target’s historical business or use a significant portion of its assets for at least two years after the transaction. Failing to meet COBE requirements results in a zero annual NOL limitation [10]. Additionally, if an ownership change occurs mid-year, closing the books on the change date prevents the need for daily proration. This ensures that post-acquisition losses can be used without being subject to Section 382 limitations [11].

Once you've structured the deal strategically and completed the necessary Section 382 calculations, the next step is putting governance systems in place to safeguard your Net Operating Losses (NOLs). Even the most carefully preserved NOLs can be jeopardized by ownership changes or poor oversight without proper controls.

Relying on manual spreadsheets to track NOLs is risky. According to the Tax Executives Institute, manual tracking can lead to significant issues like time-consuming processes, Excel errors, and increased audit scrutiny [4]. Automating these processes with tax technology is a smarter approach. Automated systems can update state-specific rules and reduce the likelihood of human error.

Ownership changes should be closely monitored, especially after events like stock issuances, option transfers, or shifts in shareholder composition [14]. To ensure compliance, merger agreements should include cooperation clauses requiring stakeholders to provide historical shareholder data for Section 382 calculations [14]. Additionally, for state tax purposes, tracking NOLs by individual legal entities - rather than just on a group basis - is recommended, as some states don’t allow loss sharing among combined return members [4].

Accurate tracking is just the first step. To further protect your NOLs, establish governance policies that minimize risks. NOL rights plans are a key tool here. These plans discourage acquisitions that could trigger Section 382 limitations. Unlike traditional rights plans with thresholds of 10% to 20%, NOL rights plans typically set the threshold between 4.9% and 4.99% to align with the IRS definition of a 5% shareholder [13]. They usually last three years, mirroring the rolling testing period under Section 382. The Delaware Supreme Court has even recognized that protecting NOLs can be a valid corporate policy warranting defensive measures [13].

Boards should also have an exemption process in place to waive rights plan triggers for acquisitions that don’t threaten NOL value. Additionally, defining "Beneficial Ownership" broadly - taking into account both Section 382 constructive ownership rules and SEC Rule 13d-3 - can simplify ownership calculations [13]. Regular analyses of cumulative ownership shifts, conducted by tax advisors, will help monitor proximity to the 50% threshold [13].

To maximize the benefits of NOLs, tax and financial planning must work hand in hand. Tax and finance teams need to align their financial projections, as NOLs only provide value when they offset future taxable income [13]. SEC counsel should carefully review Schedule 13D/G filings to differentiate between economic ownership and group ownership [14].

Formal Section 382 analyses are crucial and should be completed well ahead of tax return deadlines. As Moss Adams points out, confirming the availability of NOLs without such an analysis is often difficult [6]. Under GAAP, companies must record deferred tax assets for NOLs. If Section 382 limitations make it unlikely that these assets can be utilized before they expire, a valuation allowance must be recorded to adjust the asset's value on the balance sheet [14].

Preserving the value of net operating losses (NOLs) requires carefully navigating the maze of federal, state, and local tax rules. While federal NOL rules are already intricate, state-level variations add even more complexity. Following a merger, businesses must contend with the tax codes of all 50 states. Annette B. Smith, Partner at PricewaterhouseCoopers LLP, explains:

"State net operating loss (NOL) rules generally differ from federal NOL rules, and state NOL rules often differ from one another. This lack of consistency can lead to confusion about a taxpayer's ability to utilize NOLs" [15].

This inconsistency highlights the need for precise planning at the state level to ensure NOLs are used effectively.

States handle NOL rules differently, with some automatically updating their rules to match federal law (rolling conformity) and others locking in rules as of a specific date (static conformity). As of 2021, only 19 states and D.C. align with federal provisions like the 80% deduction cap and indefinite carryforwards [17]. The remaining states have their own unique rules. For instance:

States also calculate NOLs differently. 36 states plus D.C. use post-apportionment rules, applying losses to income already assigned to the state, while 11 states use pre-apportionment rules, applying losses to total income before state activity is factored in [4]. Some states impose additional restrictions:

Where your business operates plays a critical role in NOL utilization. Most states require a nexus - a taxable presence - in the year the loss is generated to claim a carryover later [15]. Moving operations out of a state where you have significant NOL carryforwards could result in losing the ability to use those assets, potentially requiring a valuation allowance on your balance sheet [4].

Additionally, 25 states and D.C. allow or require combined corporate returns, enabling NOL sharing among group members [4]. However, in separate-filing states, NOLs are tied to individual entities. This means aligning profitable operations within the specific entity holding the loss is crucial.

To maximize NOLs in post-apportionment states, aim to increase the apportionment percentage in the year the loss occurs. In pre-apportionment states, focus on maximizing that percentage in the year the loss is used [4]. Using intercompany transactions at fair market value can also help shift income or apportionment factors to jurisdictions where NOLs are nearing expiration [4]. These strategies directly impact long-term state tax planning.

Effective state NOL planning requires forecasting effective tax rates for each jurisdiction. Under ASC 740, businesses must evaluate whether it is "more likely than not" that deferred tax assets will be realized, making this assessment on a state-by-state basis [4][18]. While 35 states follow federal Section 382 rules, which limit NOL use after ownership changes, many states lack clear guidance on applying these limitations to state-specific income adjustments [4].

Given the complexity and frequent changes in state rules, manually tracking NOLs across multiple jurisdictions is risky. Leveraging automated tax technology can help reduce errors and adapt quickly to changing regulations [4][19].

James F. Boyle, Director of the Master of Accountancy Program at the University of Scranton, underscores the importance of effectively managing this complexity:

"The corporate deduction for NOLs helps ensure corporations pay tax on their average profitability over multiple tax years" [4].

However, realizing this benefit depends on navigating the patchwork of state-specific regulations.

Preserving the value of Net Operating Losses (NOLs) after a merger requires careful financial planning, governance, and strategic M&A execution. Building on the importance of structured NOL analysis and compliance, Phoenix Strategy Group provides growth-stage companies with a comprehensive approach to safeguard NOL value.

Phoenix Strategy Group incorporates NOLs into financial models by calculating expected tax savings using a discount rate tied to future pre-tax income projections [10]. These models account for Section 382 limitations, which restrict how much taxable income can be offset by inherited NOLs. This cap is calculated by multiplying the target’s equity value by the long-term tax-exempt rate [10][1]. For instance, if a company is valued at $10 million and the applicable rate is 1.47%, the annual NOL limit would be approximately $147,000 [11]. By integrating these constraints into cash flow forecasts and tax planning, companies gain critical insights to inform their deal structures and post-merger strategies. This level of modeling lays the groundwork for strong governance practices that help preserve NOL value.

Protecting NOLs requires precise tracking and compliance mechanisms. Phoenix Strategy Group assists in implementing NOL Rights Plans, also called Tax Benefits Preservation Plans. These plans are designed to deter ownership changes by setting triggers - typically at 4.99% - that dilute the stake of any individual acquiring 5% or more of the stock without board approval [20]. Highlighting the importance of NOLs, Matthew J. Gardella of Mintz states:

"The value of their NOL carryforward may be one of their most valuable assets on their balance sheet" [20].

The firm also establishes monitoring systems to track cumulative ownership changes among 5% shareholders over a rolling three-year period, ensuring the 50% ownership change threshold under Section 382 is not breached [20][14]. Automated tools and thorough documentation, including valuation reports and acquisition agreements, bolster these protections and provide audit-ready records [4][1].

Beyond internal processes, Phoenix Strategy Group also focuses on deal structure optimization to maintain NOL benefits.

Phoenix Strategy Group’s M&A advisory services ensure that transactions align with long-term tax objectives while addressing risks under Section 382 and Section 269. The team identifies potential ownership changes that could trigger Section 382 limitations and mitigates Section 269 risks, which arise when the IRS perceives an acquisition as being primarily for tax avoidance rather than legitimate business purposes [1][21][12]. To counter such challenges, the firm documents valid business reasons for acquisitions - such as liability protection, supply chain stability, or operational synergies [21][12].

Additionally, Phoenix Strategy Group secures professional valuations at the time of acquisition, as these figures directly determine annual NOL usage limits under Section 382 [1]. They also weigh the advantages of stock sales (which preserve NOLs within certain limits) against asset sales (which may convert NOLs into a stepped-up asset basis). Their expertise extends to navigating state-specific rules on nexus, apportionment, and filing methods [4][11]. After closing, the firm continues to monitor ownership percentages to ensure that subsequent equity raises do not unintentionally trigger new Section 382 limitations [1].

Preserving net operating losses (NOLs) after a merger requires a combination of thorough pre-merger preparation, immediate post-merger actions, and ongoing oversight. Start with comprehensive pre-deal due diligence. This includes confirming the origination dates, expiration timelines, and any restrictions tied to the NOLs [23][1]. The structure of the transaction plays a critical role - stock purchases often allow for NOL carryforwards, subject to Section 382 limitations, while asset purchases typically eliminate NOLs at the entity level [23].

Once the merger is complete, the focus shifts to post-merger analysis. Conducting a Section 382 study is essential to determine the annual NOL offset. This calculation depends on the target company's valuation and the federal long-term tax-exempt rate [22][1]. Obtaining a professional valuation at the time of acquisition is key to establishing the annual NOL cap. As Jennifer Crawford, CPA and Manager at Stephano Slack LLC, explains:

"Net operating losses may not be the outcome businesses aim for, but with careful planning, they can provide lasting tax advantages" [24].

Ongoing monitoring is equally important. Keep a close eye on 5% ownership changes to prevent triggering new Section 382 limitations [1][20]. Incorporate both federal and state NOL rules into your broader tax strategy to ensure you’re maximizing the benefits across different jurisdictions [24].

Additionally, maintain detailed documentation, including historical tax returns, supporting schedules, and valuation reports, to safeguard your NOL usage during potential IRS audits [23][1]. You can also integrate NOL planning with other tax attributes, such as R&D credits or unused business interest expense carryforwards, to optimize cash flow [1]. This proactive approach ensures NOLs are available to offset future income, particularly when tax rates increase [22][24].

Expert guidance can make all the difference. Firms like Phoenix Strategy Group specialize in helping growth-stage companies navigate these complexities. Their services include integrated financial modeling, governance strategies, and M&A advisory, ensuring that NOLs are preserved throughout the transaction process and incorporated into long-term tax planning. These strategies are designed to align with your business goals, ensuring NOL value is retained and maximized during and after the merger.

Section 382 sets restrictions on how much of a target company’s net operating losses (NOLs) the acquiring company can apply to offset taxable income after a merger. The annual limit is determined by multiplying the target company’s equity value before the ownership change by a rate provided by the IRS.

If the NOLs exceed this annual cap, the excess cannot be used in that tax year, which may push back the timeline for utilizing the full amount. Careful tax planning is crucial to make the most of these NOLs while staying within the boundaries of Section 382 rules.

Federal Net Operating Loss (NOL) rules come with specific guidelines. For example, losses generated in 2021 and beyond cannot be carried back, but they can be carried forward indefinitely. However, there's a catch: deductions are capped at 80% of taxable income. On the other hand, state NOL rules vary widely. Some states allow carrybacks, others restrict carryforward periods, and many don't follow the federal 80% limitation. These differences create a patchwork of rules that can limit how and when NOLs are applied.

Grasping these distinctions is key to effective tax planning, particularly after a merger. The variations can influence both the timing and value of NOL usage. To navigate this maze and ensure compliance, it's essential to work with experienced professionals who can help craft the right strategy.

To comply with net operating loss (NOL) rules after a merger, businesses need to take a few essential steps. First, it's critical to maintain the target company’s operations to align with IRS Section 382 limitations. A careful Section 382 analysis should be conducted to track ownership changes and identify any restrictions on how the NOLs can be used.

Another useful strategy is adopting an NOL rights plan, often referred to as a "poison pill", to safeguard the loss attribute. Collaborating closely with tax advisors is equally important to ensure compliance, file accurate tax returns, and provide any required disclosures to the IRS. By staying on top of these measures, companies can make the most of their NOLs while meeting all regulatory guidelines.