Published on

May 15, 2026

If you're a MedTech founder or investor, understanding exit strategies is critical. The two main pathways - M&A (mergers and acquisitions) and IPOs (initial public offerings) - offer distinct benefits and challenges. Here's the breakdown:

Key Insights:

Quick Comparison:

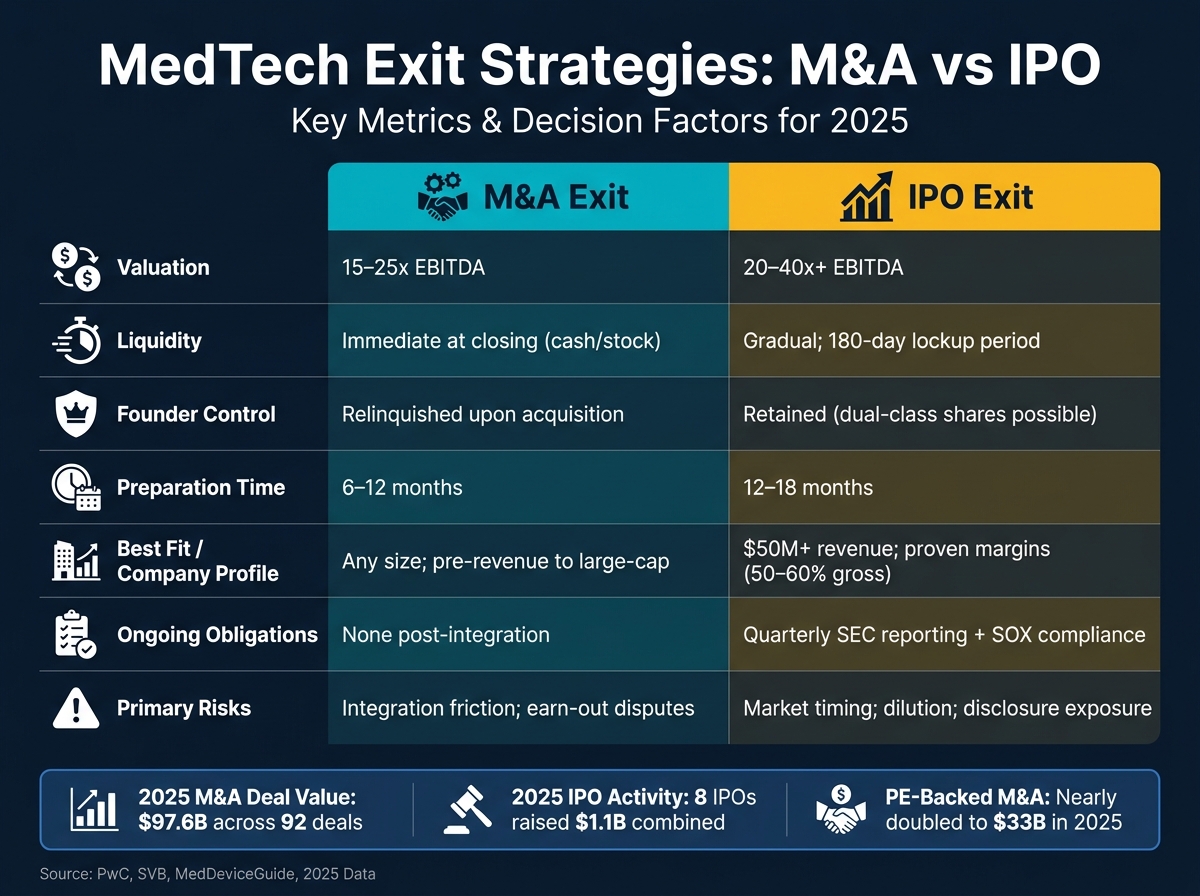

| Factor | M&A Exit | IPO Exit |

|---|---|---|

| Liquidity | Immediate (cash/stock) | Gradual (post-lockup period) |

| Valuation | 15–25x EBITDA | 20–40x+ EBITDA |

| Control | Relinquished | Retained (with public obligations) |

| Preparation Time | 6–12 months | 12–18 months |

| Best Fit | Any size, pre-revenue possible | $50M+ revenue, proven margins |

Whether you pursue M&A or an IPO, early planning, clean financials, and a clear regulatory strategy are essential for success.

MedTech Exit Strategies: M&A vs IPO Comparison 2025

The MedTech mergers and acquisitions (M&A) market is buzzing with activity. In 2025, deal value reached an impressive $97.6 billion, marking the highest level in over a decade. This momentum carried into 2026, with $26.6 billion across 37 deals in just the first quarter [5][8].

Large players are aggressively scaling in high-growth areas like neurovascular treatments, advanced diagnostics, and AI platforms. For instance, Boston Scientific's planned $14.5 billion acquisition of Penumbra (announced in January 2026) and Abbott's $21 billion acquisition of Exact Sciences (late 2025) highlight this trend [7]. Meanwhile, private equity firms are making their mark, with PE-backed deal value nearly doubling to $33 billion in 2025 [11].

Spinoffs and divestitures are also reshaping portfolios, accounting for one-third of 2025's deal value, or about $27 billion [7].

"Momentum is accelerating into 2026 as medtech companies deploy capital with greater precision, using acquisitions and divestitures to strengthen capabilities and position themselves for sustained long-term growth." - James Woods, Principal, US Medtech Leader, PwC US [5]

While M&A activity surges, the IPO market is following a slower, more selective path.

MedTech IPOs are making a cautious comeback. In 2025, 8 IPOs raised a combined $1.1 billion, a significant improvement over 2024, which saw just one offering that raised $112 million [6]. However, IPO activity still lags far behind M&A, which recorded 92 deals in the same year [6].

Public markets are favoring companies with established revenue and clear profitability paths. A standout example is Hinge Health's March 2025 debut on the NYSE (ticker: HNGE), where the company raised $437.3 million and opened at a 23% premium over its $32 IPO price. This reflects strong investor interest in tech-enabled care solutions with proven commercial success [6]. By Q1 2026, the IPO landscape remained narrow, with only one major offering raising $600 million on the Nasdaq [8].

The bottom line: IPOs are an option, but mainly for companies that have matured beyond the early-stage startup phase.

Broader economic and regulatory factors are playing a critical role in shaping MedTech exit strategies and valuations.

Interest rates and investor caution are closely linked. Higher rates have made investors more selective, especially in public markets. In 2024, two-thirds of late-stage venture rounds (Series C or later) were flat or down rounds, illustrating how challenging it has become to secure a premium valuation pre-exit [3]. While interest rates stabilized in late 2025, underwriters now insist on positive EBITDA and proven unit economics before greenlighting IPOs [10].

Regulatory pathways also impact valuations significantly. Companies with Pre-Market Approval (PMA) devices in 2024 secured a median upfront M&A payment of $550 million, far exceeding the $254 million median for 510(k)-cleared products [3]. However, PMA devices typically take longer to exit - 13.8 years on average, compared to 11.1 years for 510(k) devices [3]. Here's a quick comparison:

| Exit Metric (2024 Data) | PMA Devices | 510(k) Devices |

|---|---|---|

| Median Upfront M&A Payment | $550M | $254M |

| Median Total M&A Deal Value | $810M | $293M |

| Average Years to Exit | 13.8 years | 11.1 years |

| Commercial Status at Exit | Often pre-revenue | Revenue-generating |

Antitrust policy is another factor influencing the market. U.S. regulators are increasingly favoring structural remedies, like requiring divestitures, instead of outright blocking mergers. This shift gives larger acquirers more confidence to pursue significant deals, which is encouraging news for founders aiming for strategic exits [9].

These macro trends are setting the stage for how MedTech companies weigh M&A and IPO pathways.

In today's market, mergers and acquisitions (M&A) provide MedTech companies with a fast track to liquidity and strategic growth. M&A remains the dominant exit strategy in the MedTech sector. During the first half of 2025, M&A deals accounted for over 94% of all global digital health exits, with 107 transactions compared to just 6 IPOs [13]. This stark contrast highlights the advantages M&A offers over going public, though it also comes with its own set of challenges, particularly in regulatory compliance and integration.

One of the biggest perks of an M&A deal is immediate liquidity. Unlike IPOs, which often involve lock-up periods and exposure to market volatility, M&A transactions deliver cash or stock at closing. Additionally, strategic buyers frequently pay a "synergy premium", valuing the target company higher due to the added benefits it brings to their existing portfolio.

"Strategic acquirers... are willing to pay more because the asset is worth more inside their portfolio." - MedDeviceGuide [12]

M&A also shifts significant risks to the acquiring company. Once the deal is finalized, the acquirer takes on responsibilities such as navigating regulatory hurdles, scaling manufacturing, and entering global markets. For the seller, this means relief from these complex and often costly challenges. On top of that, the acquired company gains access to the buyer's established infrastructure, including global sales teams, distribution channels, and quality management systems - resources that could take years to build independently.

Despite the clear benefits, M&A is not without its hurdles. Regulatory due diligence often becomes a stumbling block. Buyers use detailed evaluation frameworks, and issues like repeated FDA 483 observations, open warning letters, or unresolved EU MDR compliance gaps can derail a deal or lead to escrow requirements that reduce the payout [12].

"Regulatory due diligence is not a formality - it is a deal-shaping exercise that directly affects valuation, deal structure, and the go/no-go decision." - Ran Chen, Global MedTech Expert [12]

Another risk is valuation compression. If a company has an insufficient financial runway or has failed to meet key clinical milestones, buyers may reduce their offers. Timing is also critical - M&A opportunities can disappear quickly, and failing to align with a buyer's strategic priorities could result in a less favorable deal. Finally, integration can be disruptive. Many acquirers require full absorption into their systems, which can complicate operations and affect team morale post-transaction [12].

Proper preparation can help mitigate these risks and improve the chances of a successful outcome.

Preparation is crucial for achieving a favorable exit. Experts recommend starting the process 12–18 months in advance to address documentation gaps and align milestones with potential acquirers' needs [14]. As market conditions tighten, being proactive is more important than ever.

Key steps include:

Additionally, companies should establish a clear reimbursement pathway supported by solid clinical data.

"A cleared device without a reimbursement pathway is commercially stranded." - Ran Chen, Global MedTech Expert [12]

For pre-revenue companies, demonstrating how their device reduces hospital costs, lowers readmission rates, or enables outpatient care can significantly enhance valuation.

The table below summarizes the key advantages and challenges of M&A for MedTech companies:

| Factor | Detail | What It Means for MedTech Operators |

|---|---|---|

| Faster Liquidity | Cash or stock delivered at closing with no lock-up period | Founders and investors realize gains without relying on public market timing |

| Synergy Premium | Buyers pay for the added value your asset brings to their portfolio | Valuations may exceed what standalone financials would suggest |

| Risk Transfer | Acquirer assumes regulatory, manufacturing, and commercialization risks | Relieves founders of these burdens |

| Infrastructure Access | Immediate access to buyer’s quality systems, sales force, and channels | Speeds up product adoption through established networks |

| Regulatory Due Diligence | Compliance issues like FDA 483s or MDR gaps can derail deals | Maintaining a clean compliance record is critical for securing a premium valuation |

| Valuation Compression | Unmet clinical milestones or weak runway may lower offers | Early preparation and milestone alignment are key to strong negotiations |

| Integration Disruption | Full absorption into acquirer’s systems may disrupt operations | Post-close transitions can challenge team and operational continuity |

While mergers and acquisitions (M&A) have traditionally been the dominant route for MedTech exits, IPOs offer a unique alternative for companies that have achieved substantial growth and want to maintain their independence while tapping into public capital markets. After a long hiatus, the MedTech IPO market has shown signs of revival. In October 2024, Ceribell, a company specializing in neurological diagnostics, raised over $207 million through its IPO. This was followed by Beta Bionics in January 2025, which raised approximately $212 million - nearly doubling its original $114 million target. Kestra Medical joined the trend in March 2025, raising $202 million. These successful offerings highlighted a renewed sense of investor confidence in the MedTech sector. [18]

"Because the gap in IPO activity was so prolonged - just over three years - the quality of most mature medical device companies is extremely high." - Scott Blumberg, CFO, Ceribell [18]

IPOs provide an opportunity to raise substantial capital - often hundreds of millions in a single transaction. This influx of funds can fuel research and development, geographic expansion, and even acquisitions, all while allowing founders to retain control. Public markets tend to value scalable platforms, especially those leveraging AI or machine learning to enhance patient outcomes. [17] With MedTech earnings projected to grow at an annualized rate of 9.6% through 2029, public investors are increasingly drawn to the sector. [16]

Unlike pharmaceutical companies, which often face the "patent cliff" challenge, MedTech businesses benefit from recurring revenue models. By building installed bases of devices, they generate steady income from consumables and services - a business model that investors view as reliable and sustainable. [16] For example, Ceribell's IPO success was driven by strong fundamentals: the company reported 2023 revenues of $45.2 million with gross margins of 85%, and its stock price climbed 52% by early 2025. [4] However, the potential rewards of going public come with significant challenges.

IPOs expose companies to a much broader and often volatile investor base. Once public, companies are under constant scrutiny, with founders shifting from answering to a small board to being accountable to thousands of shareholders. Public markets demand consistent performance, and missing a single revenue target can lead to sharp valuation declines.

The 2022 IPO cycle serves as a cautionary example. Virax Biolabs saw its stock price plummet 93% below its August 2022 high within months of listing. Similarly, Tenon Medical raised $16 million but faced harsh market reactions due to its limited revenues of $414,000 against $10.4 million in losses. By the end of 2022, none of the MedTech companies that went public were able to maintain their initial float price. [15]

"Missing revenue projections by even a quarter can result in penalties in the form of lower valuations, making potential IPO candidates hesitant to take the risk." - Patrick Nugent, Partner, FLG Partners [4]

Beyond financial performance, companies face substantial compliance and transparency demands. Public companies must meet SEC reporting standards, maintain SOX-compliant internal controls, and disclose sensitive information such as financials, intellectual property, and regulatory communications - data that competitors can exploit. For companies incorporating AI in their devices, additional scrutiny arises around AI governance, device security, and the defensibility of their technology against generic models. [10][17]

Given the challenges, thorough preparation is essential for a successful IPO. The expectations for IPO readiness have significantly increased. Institutional investors now look for companies with a revenue run rate of around $50 million, gross margins between 50%–60% with a clear path to exceed 70%, and at least two to three years of audited financials compliant with PCAOB standards. [4][18] Additionally, regulatory milestones like FDA clearance (510(k) or PMA) and a well-defined reimbursement strategy with CPT codes and payer engagement are considered essential by underwriters. [12]

Operational readiness is equally important. For example, Hinge Health spent two years conducting internal mock earnings calls before its 2025 IPO to ensure the team could consistently "beat and raise" expectations. This kind of preparation - gearing up for the realities of public company life - often separates successful IPOs from those that falter.

"Public markets reward readiness, not ambition alone. Underwriters and institutional buyers price that gap during diligence, not after." - Qubit Capital [21]

| Category | Requirement |

|---|---|

| Financials | ~$50M revenue run rate; 50–60% gross margins; 3+ years of audited financials [4][18] |

| Regulatory | Valid FDA 510(k) or PMA; EU MDR transition complete; clean FDA inspection history [12] |

| Operations | ISO 13485 certification; mature QMS; manageable CAPA backlog; complete Design History Files [12] |

| Governance | Independent board of directors; audit committee; SOX compliance framework [19][20] |

| Strategy | 10+ patents for valuation premium; established CPT reimbursement codes; clear ESG agenda [15][17] |

| Market (Nasdaq) | $50M minimum market cap; $4 minimum bid price; 1.25M publicly traded shares [20] |

Let's dive deeper into how M&A and IPO strategies stack up against each other.

One of the most noticeable distinctions lies in how and when founders and early investors receive their payouts. With M&A, liquidity is immediate - shareholders get paid as soon as the deal closes. On the other hand, IPOs require patience. Founders and early investors are typically subject to a 180-day lockup period post-listing, after which they can gradually sell their shares. It’s worth noting that about 40% of life sciences M&A deal value often includes earn-outs, meaning part of the payout depends on achieving certain regulatory or commercial milestones [22].

Valuations also differ significantly. High-growth MedTech companies aiming for IPOs can achieve valuations in the range of 20–40x EBITDA, while M&A deals usually settle between 15–25x EBITDA. The latter often includes strategic synergies brought by the acquiring company. However, the higher valuation of IPOs comes with added risks, such as exposure to market sentiment, macroeconomic factors, and the pressure of meeting quarterly earnings expectations.

Control is another major factor. In an M&A exit, founders typically relinquish control, although some may negotiate advisory roles or other employment terms as part of the deal. IPOs, however, allow founders to maintain a degree of control, especially if they implement dual-class share structures. But this control hinges on the company’s ongoing performance in the public market.

"Exit vehicles are simply different modes of transportation to the same place." - Leslie Trigg, CEO, Outset Medical [23]

For a clearer snapshot of these differences, refer to the comparison table below.

The decision between M&A and IPO often boils down to three factors: company size, business model, and risk tolerance.

Scale is a critical consideration. IPOs are increasingly reserved for companies generating at least $30–$50 million in annual revenue. The most successful recent IPOs, like Medline’s December 2025 offering, which raised $6.26 billion and saw a 41% surge in share price on its first day, typically feature large, private equity-backed companies with proven profitability [2]. In contrast, smaller or earlier-stage companies - especially those with limited product diversification - often find M&A a more accessible and practical option.

The business model also plays a significant role. Companies with predictable, recurring revenue streams, such as those offering SaaS subscriptions, consumables, or service contracts, tend to perform better in public markets. Investors value the stability of consistent cash flows. On the flip side, businesses with uneven revenue cycles, like capital equipment companies, or those carrying substantial clinical risk, often lean toward M&A. A strategic acquirer can absorb these risks more effectively within their broader portfolio.

"Watching Omada and Hinge redefined the blueprint of what it could take to be a public company - emphasizing profitability or clear paths to profitability, not just revenue growth." - Sasha Kelemen, Healthcare Investment Banking Director, Baird [2]

Ultimately, aligning the exit strategy with the company’s stage and market conditions is crucial. The table below captures these considerations succinctly.

| Factor | M&A Exit | IPO Exit |

|---|---|---|

| Best for | Any size; pre-revenue to large-cap [2] | Revenue >$50M or very high growth [2][4] |

| Valuation basis | Strategic premium (15–25x EBITDA) [2] | Public market premium (20–40x+ EBITDA) [2] |

| Liquidity | Immediate (with possible earn-outs) [2][22] | Gradual; subject to lock-up periods [2] |

| Founder control | Usually lost upon acquisition [2] | Retained; dual-class shares possible [2] |

| Preparation time | 6–12 months [2] | 12–18 months [2] |

| Ongoing obligations | None post-integration [2] | Quarterly reporting, SOX compliance [2] |

| Primary risks | Integration friction, earn-out disputes [1] | Market timing, dilution, disclosure exposure [1][24] |

| Typical company profile | Early-stage, single-product, or capital equipment | Recurring revenue, diversified portfolio, proven margins [4] |

MedTech companies often pour their energy into product development and securing regulatory approvals, leaving financial groundwork as an afterthought. Unfortunately, this oversight can come back to haunt them when it's time to plan an exit.

"Pre-IPO planning is not a path. It is a platform." - Louis Lehot, Partner, Foley & Lardner LLP [27]

This principle holds true for mergers and acquisitions (M&A) as well. Companies that maintain clean financial records, have audited financials, and document their intellectual property thoroughly are not just prepared for an IPO - they also become more appealing acquisition targets. They gain the upper hand in negotiations, as highlighted by this insight:

"Every week of additional due diligence is leverage in the wrong direction." - Foley Ignite [27]

A 2026 survey revealed a striking disconnect: while 60% of private equity sponsors believe their portfolios have IPO potential, fewer than 20% of portfolio CFOs are actively preparing for it. Even more concerning, only 30% of CFOs feel their financial systems are ready for the demands of public markets [27]. This lack of readiness can lead to undervalued deals or even failed transactions.

Laying this financial groundwork is critical and sets the stage for the detailed preparations that follow.

Preparing for an IPO is no small feat. It typically requires 18–24 months of preparation, including two to three years of PCAOB-audited financials, SOX-compliant internal controls, and a functioning investor relations team [25]. For a newly public company with $200M–$500M in revenue, annual compliance costs can range from $4.5 million to $6 million. These expenses cover SOX compliance, external audits, and legal fees [26].

M&A preparation, while faster, still requires diligence. Deals can close within 3 to 9 months of initial contact, but companies must have their financial house in order. This includes an organized cap table, well-documented intellectual property, a polished Confidential Information Memorandum (CIM), and financial models that clearly highlight synergy value for potential buyers [25][26]. Any disorganization - whether in IP documentation or equity structures - can derail deals during due diligence.

Regardless of the exit strategy, one thing is clear: companies need audit-ready financials long before the exit process begins. Waiting until three months before filing an S-1 or starting an M&A process leaves little room to address any gaps.

Given the complexities of exit preparation, expert guidance can make all the difference. Phoenix Strategy Group partners with growth-stage MedTech companies to establish the financial systems that drive successful exits. Their services include fractional CFO support, advanced FP&A systems, bookkeeping, data engineering, and targeted M&A advisory. These tools provide the financial transparency and credibility that investors and buyers demand.

Whether it's M&A preparation - creating integrated financial models, assembling due diligence documents, and setting up KPI frameworks - or IPO readiness - building rigorous reporting systems, forecasting processes, and governance structures - Phoenix Strategy Group ensures companies are ready to seize opportunities when market windows open.

| Exit Goal | Financial Action Required | Timeline to Implement |

|---|---|---|

| M&A readiness | Audit-ready financials, organized cap table, documented IP, refined CIM | 6–12 months before process |

| IPO readiness | PCAOB audits, SOX controls, investor relations, board governance | 18–24 months before S-1 |

| Maximize valuation | Audited financials, eight-quarter forward projections, Rule of 40 score ≥40% | Ongoing; 2+ years out |

| Preserve optionality | Integrated financial model, KPI framework, fractional CFO | Start immediately |

| Accelerate due diligence | Audit-ready books, documented contracts, clean IP portfolio | 24 months before exit |

When it comes to choosing between M&A and IPOs, each path has distinct advantages. M&A provides a quicker route to liquidity, often closing within 6–12 months, and offers more predictability. However, founders may need to give up control in the process. IPOs, on the other hand, can deliver higher valuations and long-term access to capital, but they require significant preparation - typically 12–18 months - and come with ongoing public market obligations. Companies aiming for an IPO generally need revenues in the $30 million to $50 million range and gross margins between 50% and 60%. Public market valuations often fetch premiums of 20–40x EBITDA, compared to the 15–25x EBITDA seen in strategic acquisitions [2].

As highlighted in this analysis, timing and aligning your strategy with market conditions are critical. In today’s market, profitability holds more sway than pure growth. Regulatory compliance, clean financial records, and a strong quality management system are essential, regardless of the chosen path.

For MedTech founders, early and proactive exit planning is vital. Start by auditing your CAPA backlog, securing intellectual property, and stress-testing financial models to meet the expectations of buyers and investors. If an IPO is your goal, consider following examples like Hinge Health, which spent two years preparing through internal mock earnings calls to build the operational discipline required for public markets [2].

Investing in robust financial systems now sets the stage for future success. Phoenix Strategy Group specializes in helping growth-stage MedTech companies prepare for these pivotal moments. From audit-ready accounting and KPI frameworks to integrated financial models and M&A advisory, they ensure founders are equipped to seize the right opportunity when it arises.

To figure out if your company is ready for an IPO, start by evaluating its current stage of development, revenue growth trajectory, and overall risk profile. It’s essential to have solid financial reporting systems, strong governance structures, and strict adherence to regulatory requirements. Investors are drawn to MedTech companies that demonstrate clear clinical progress, operational maturity, and strong clinical validation.

Recent IPO trends highlight that high-performing MedTech firms with these characteristics are particularly appealing to investors. To position your company for success, prioritize operational readiness and ensure your market strategy aligns with both investor expectations and regulatory demands.

When it comes to MedTech mergers and acquisitions, there are several red flags that can complicate or even derail deals. These include valuation gaps, regulatory challenges, and due diligence concerns.

These challenges highlight the importance of careful planning and thorough evaluation in MedTech M&A transactions.

Timing an exit in the MedTech field requires careful consideration of several factors, including market conditions, regulatory risks, and overall volatility. It's crucial to keep an eye on market stability, shifts in investor sentiment, and trends in regulatory policies. The best opportunities often arise when investor demand is strong, market volatility is low, and the regulatory landscape is favorable.

To maximize value and reduce potential risks, align your timing with M&A cycles or open IPO windows, as these periods typically offer more favorable conditions for exits.