Published on

December 23, 2025

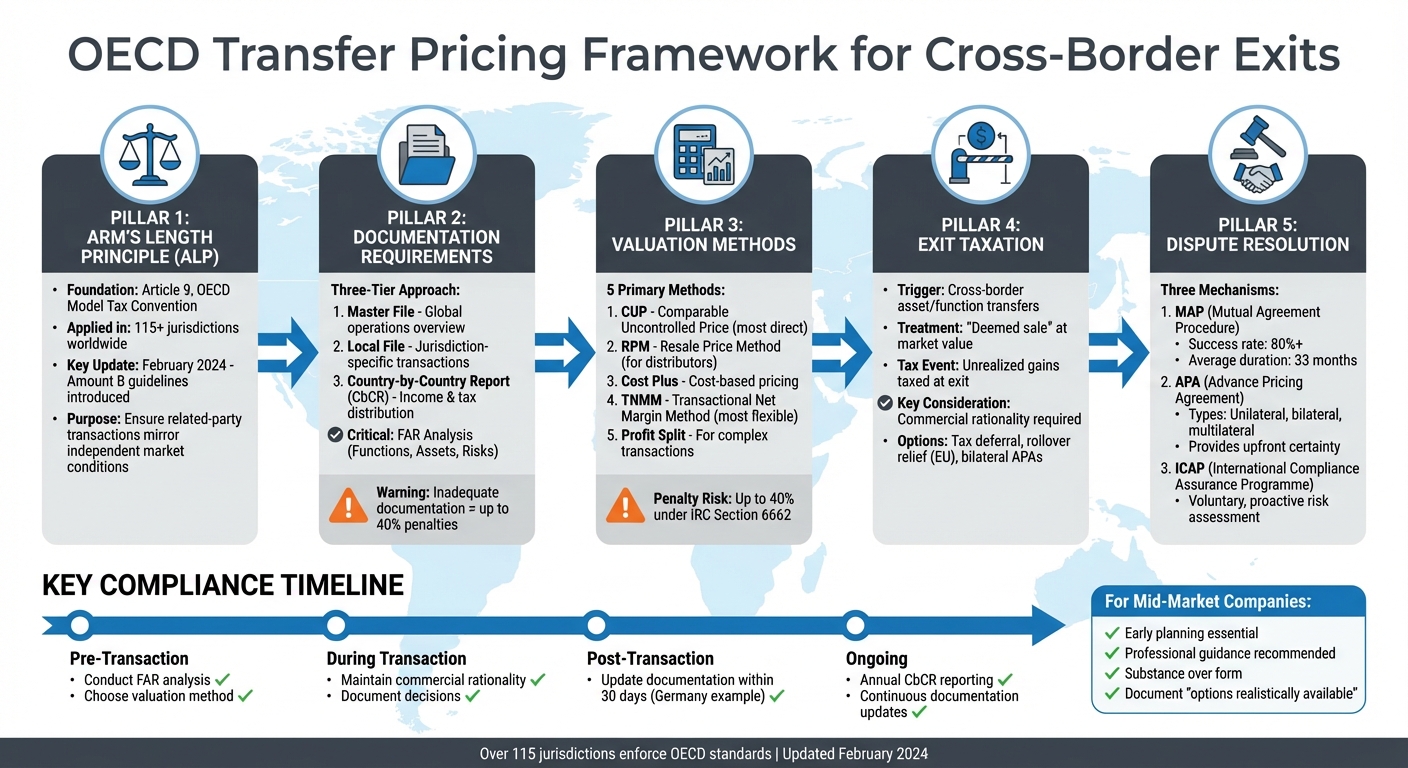

When businesses shift assets, functions, or risks across borders during an exit, transfer pricing is critical. It ensures transactions between related entities reflect market-based pricing, preventing tax disputes or double taxation. The OECD's Arm's Length Principle (ALP) underpins these rules, requiring related-party transactions to mimic independent market conditions. Over 115 jurisdictions enforce these standards, with updated guidelines introduced in February 2024 to simplify compliance for certain activities.

Key points include:

For mid-market companies, aligning with these principles reduces tax risks, audit exposure, and ensures smoother exits. Early planning and professional guidance are essential to navigate these complexities effectively.

OECD Transfer Pricing Compliance Framework for Cross-Border Exits

The Arm's Length Principle (ALP) ensures that transactions between related parties are priced as if the parties were independent and operating under similar conditions [7]. This principle is a cornerstone of international tax law, drawing its foundation from Article 9, Paragraph 1 of the OECD Model Tax Convention. The article states:

"[Where] conditions are made or imposed between the two [associated] enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises... may be included in the profits of that enterprise and taxed accordingly." [7]

In practice, this principle treats each entity within a multinational group as if it were a separate, independent business. The emphasis is placed on the specifics of the transaction - what is being transferred, who assumes the risks, and whether the agreed-upon pricing aligns with market realities. This approach is especially critical in cross-border exits, as it ensures profits are distributed fairly and reflect market-based pricing.

When applying the ALP in cases of cross-border exits, the goal is to confirm that the transaction structure mirrors what independent parties would agree to under similar conditions [7]. Tax authorities carefully examine these exit arrangements to validate that pricing is consistent with market standards. This is done through comparability analysis, comparing related-party transactions to those conducted between independent entities to ensure fairness.

Authorities don't just rely on written contracts - they also evaluate the actual behavior of the parties involved. This includes analyzing the functions performed, assets utilized, and risks taken, ensuring the pricing reflects genuine market conditions [7]. For instance, if a subsidiary takes on significant risks but lacks the financial capacity or control to manage them, tax authorities may adjust the profit allocation. The OECD Guidelines highlight this nuanced process:

"Transfer pricing is not an exact science but does require the exercise of judgment on the part of both the tax administration and taxpayer" [7].

On February 19, 2024, the OECD introduced an update to its Guidelines, incorporating Amount B under Pillar One. This update offers a streamlined method for handling baseline marketing and distribution activities [2]. The goal is to reduce compliance challenges for certain cross-border transactions while ensuring adherence to the Arm's Length Principle.

According to the OECD guidelines, identifying the value being transferred is a critical first step in any business restructuring. Chapter 9 describes business restructuring as the cross-border reorganization of commercial or financial relationships between related entities [9]. Whether a company is exiting a market or reorganizing its operations internationally, it’s vital to pinpoint what is actually being transferred - not just what’s outlined in contracts [10].

A key question to address is whether an independent party would expect compensation for an asset, a group of assets, or a terminated agreement. If the answer is yes, then arm's length pricing must be applied [10]. This principle applies to scenarios like transferring intellectual property, ending a distribution agreement, or converting a full-fledged subsidiary into a limited-risk entity.

When intangibles are part of the equation, the focus shifts to the DEMPE functions - Development, Enhancement, Maintenance, Protection, and Exploitation. Tax authorities prioritize these value-driving activities over mere legal ownership [10]. Accurately valuing these elements is essential to show that the transaction aligns with commercial realities.

Once a proper valuation is established, the next step is proving the transaction’s commercial rationality, which is critical for satisfying tax authorities. Tax administrations may reject restructurings that fail to reflect a clear, market-based arm's length price [10]. As the OECD Guidelines explain:

"An assessment may be necessary of the commercial rationality of the restructuring... [to determine] whether the transaction has the commercial rationality of arrangements that would be agreed between unrelated parties." [10]

To meet this standard, businesses must show that the restructuring serves a legitimate purpose beyond reducing taxes. For example, the legal structure of an entity should align with the location where real management and control occur. If key decisions are made in New York, but the entity is incorporated in a low-tax jurisdiction with little operational substance, this could raise red flags about residency and rationality. As Eversheds Sutherland emphasizes:

"Reorganizations must have a sound business rationale beyond tax savings, and any new entities or structures should carry real decision-making functions and risks, not just exist on paper" [5].

To stay compliant, companies should keep intercompany agreements up to date, conduct fresh benchmarking studies, and document a clear narrative for the transaction. In Germany, for instance, transfer pricing documentation must now be submitted within 30 days of receiving a tax audit notification, a significant reduction from the previous 60-day timeframe [6].

Choosing the right valuation method is crucial for ensuring that exit pricing reflects the actual economic value of a transaction. According to OECD guidelines, accurately valuing exit transactions is key to achieving arm's length pricing. The OECD outlines five primary transfer pricing methods: the Comparable Uncontrolled Price (CUP) method, the Resale Price Method (RPM), the Cost Plus Method, the Transactional Net Margin Method (TNMM), and the Transactional Profit Split Method [1]. Each method serves a specific purpose, depending on factors like the type of asset, the reliability of market data, and the complexity of the transaction. Before deciding on a method, it’s essential to conduct a FAR (Functions, Assets, and Risks) analysis to understand the roles, assets, and risks of each party involved [15]. This step lays the groundwork for proving that the chosen method aligns with economic realities.

The CUP method is the simplest and most direct approach - when reliable comparable data is available. As the OECD describes:

"The CUP method compares the price charged for property transferred in a controlled transaction to the price charged in a comparable uncontrolled transaction with comparable circumstances" [11].

This method works best when direct market pricing data is accessible. For example, in exit transactions involving financial components - like guarantees or debt transfers - the CUP method is often the go-to choice. However, finding direct comparables can be challenging [4]. In such cases, companies may turn to alternative approaches, such as the yield method (evaluating the benefit to the borrower) or the cost method (assessing the cost to the guarantor) [4]. It’s worth noting that tax authorities heavily scrutinize the use of the CUP method. Under IRC Section 6662, companies may face a penalty of up to 40% if intercompany prices stray too far from the arm's length standard [14].

When comparable data is hard to find, alternative methods like RPM and TNMM come into play. The Resale Price Method (RPM) calculates transfer prices by starting with the final resale price to an independent buyer and subtracting an appropriate gross margin [13]. This method is particularly useful for exit transactions involving distribution or retail units that resell products without adding much value. RPM is often applied to ensure arm's length pricing for resellers.

The Transactional Net Margin Method (TNMM), on the other hand, focuses on net profit margins relative to a base - such as costs, sales, or assets [12]. As Prof. Dr. Daniel N. Erasmus of the OECD explains:

"TNMM is useful in situations where market data is scarce and accommodates variations in how companies organize their operations" [12].

This method’s adaptability makes it a popular choice for exit valuations involving service-based businesses or complex intangible assets. For instance, TNMM is a practical solution when gross profit data is unavailable or when dealing with unique business models. It uses financial ratios derived from comparable companies to establish arm's length pricing [13].

For mid-market businesses, the choice of method should align with the specifics of the exit. Use CUP when clear market benchmarks exist, RPM for straightforward distribution activities, and TNMM for more complex operations or when comparable data is limited [15]. Be meticulous in documenting your reasoning - failure to do so can result in penalties of up to 40% under IRC Section 6662 [14].

Accurate documentation is your safeguard against penalties and disputes. It plays a crucial role in ensuring a smooth and compliant exit strategy, linking valuation methods with audit risk management. For cross-border exits, detailed transfer pricing documentation is especially critical. The OECD framework - followed in over 115 jurisdictions worldwide [2] - can be the difference between a seamless transaction and an audit headache.

The OECD's documentation framework is built on three key components: the Master File, the Local File, and Country-by-Country Reporting (CbCR) [2][17].

For cross-border exits, your documentation must include a detailed FAR (Functions, Assets, and Risks) analysis. This analysis justifies arm's length pricing by explaining how functions, assets, and risks are allocated. It’s not enough to simply state which entity bears a particular risk - you need to explain how the risk is managed, who makes decisions about it, and whether the entity has the financial capacity to handle it [18]. As New Zealand's Inland Revenue highlights:

"If a company's documentation inadequately explains why its transfer prices are considered to be consistent with the arm's length principle, we are more likely to audit those transfer prices in detail" [18].

Your documentation package should include signed intercompany agreements and a clear map of your global corporate structure. Make sure your financial ratios align with your annual statements to avoid drawing scrutiny. Avoid vague descriptions like "wholesale distributor" unless you provide detailed specifics about your local operations. Most importantly, stay proactive - update your documentation after any strategic change. The OECD underscores this point:

"Transfer pricing is an ongoing process, not a one-time documentation exercise" [18].

After any restructuring or strategic shift, reassess your facts and pricing immediately. This thorough approach to documentation is key to minimizing audit risks in cross-border exits.

Beyond compliance, good documentation is your best defense against audits. In jurisdictions following OECD standards, failing to prepare adequate documentation for significant transactions can lead to penalties of up to 40% for gross carelessness [18]. When your records are incomplete or unclear, the burden of proof shifts to you, making it harder to contest alternative pricing proposed by tax authorities.

To reduce audit risks, maintain detailed, up-to-date records that accurately reflect your current practices. Ensure local management verifies the accuracy of your Local File [18]. Document efforts to identify internal comparables before relying on external benchmarks [18]. Additionally, consider joining voluntary programs like the OECD's International Compliance Assurance Programme (ICAP). This initiative fosters multilateral risk assessments with tax authorities, helping you achieve greater tax certainty [2].

When businesses move assets or operations across borders, they often face exit taxes. For mid-market companies planning cross-border restructurings, understanding these taxes and how to handle disputes is crucial.

Exit taxes treat cross-border transfers as if they were a "deemed sale" at market value, taxing unrealized gains when assets or operations leave a tax jurisdiction [19]. As Eversheds Sutherland explains:

"Exit taxes are a major consideration whenever valuable assets, functions or even entire companies move across borders as part of a reorganization. Many jurisdictions impose a tax on unrealised gains when assets or business operations leave their tax net – effectively treating the move as a deemed sale at market value" [19].

Certain actions, such as relocating intellectual property (IP), shifting key functions, or restructuring agreements, can trigger taxable events [19][20]. Even changing a company’s legal headquarters may be treated as a "deemed liquidation" [19]. According to OECD Guidelines Chapter IX, tax authorities assess whether a "transfer of value" has occurred by comparing the company’s functions, assets, and risks before and after the move [20]. The arm’s length principle serves as the global benchmark for valuing these transactions, ensuring the pricing aligns with what independent parties would have agreed to under similar market conditions [20][2].

Failing to plan for these tax impacts early can derail a reorganization. Caroline Chua, Director of Transfer Pricing at KPMG Switzerland, highlights the importance of commercial justification:

"It needs to be analyzed whether on an individual-entity basis, it would be commercially justified for an independent party to enter into the restructuring transaction. The rationale is that an independent enterprise would only engage in the transaction if there were not more attractive options available" [20].

For complex or high-value exit transactions, businesses might consider negotiating a bilateral Advance Pricing Arrangement (APA) to resolve the exit tax valuation upfront and reduce audit risks [20]. Additionally, options like tax deferral or rollover relief may be available, especially for intra-group restructurings within the EU [19].

Given the immediate tax liabilities tied to exit taxes, addressing double taxation risks becomes essential.

Double taxation occurs when two countries claim tax rights over the same cross-border transaction, forcing businesses to pay taxes twice on the same income. To tackle this, mechanisms aligned with OECD transfer pricing standards help prevent duplicate taxation.

The Mutual Agreement Procedure (MAP), outlined in Article 25 of the OECD Model Tax Convention, is a key tool for resolving disputes when tax authorities disagree on arm’s length pricing [21][23]. MAP has been effective, resolving over 80% of transfer pricing cases [23]. However, it’s not a quick fix - resolutions take an average of 33 months as of 2018 [23].

For businesses seeking more certainty, Advance Pricing Agreements (APAs) are a proactive solution. APAs provide clarity on transfer pricing arrangements before transactions occur and can be unilateral, bilateral, or multilateral [22]. Multilateral APAs, in particular, are ideal for complex exit transactions involving multiple jurisdictions. As the OECD explains:

"Multilateral MAPs and APAs provide greater tax certainty by bringing together multiple jurisdictions to determine the taxation of multinational enterprises' transactions" [22].

Starting in 2024, all members of the Inclusive Framework will report annual statistics on bilateral and multilateral APAs, offering greater transparency for businesses [22].

Another option is the International Compliance Assurance Programme (ICAP), a voluntary program designed for multinational enterprises (MNEs). ICAP facilitates open discussions between MNEs and tax administrations, offering a coordinated risk assessment to avoid future disputes [22]. For transparent businesses, this program provides a way to address potential issues before they escalate.

Finally, the OECD’s BEPS Action 14 establishes minimum standards for dispute resolution, including peer reviews to ensure jurisdictions effectively implement MAP mechanisms [22]. Reviewing these peer review reports can help businesses assess the efficiency of a jurisdiction’s MAP process, guiding them in choosing the most effective dispute resolution strategy.

For mid-market businesses, navigating OECD transfer pricing compliance during cross-border exits can be a daunting task. Unlike large multinationals with dedicated tax teams, these companies often lack the internal resources to manage the complexities involved. Yet, the risks are substantial - errors can lead to audits, double taxation, and disputes that could jeopardize an otherwise smooth exit. This highlights the importance of a carefully tailored approach to exit structures and the value of expert guidance.

It's essential to align your exit structure with agreements that would hold up in an independent market. Following OECD principles and documentation standards, ensure your strategy is grounded in economic reality. The OECD places a strong emphasis on analyzing "options realistically available" to all parties at the time of the transaction [4]. This means your operational practices must align with your legal agreements. Tax authorities often scrutinize actual business conduct more closely than written contracts. If there's a mismatch, expect increased attention [4][8].

With over 115 jurisdictions adopting Country-by-Country Reporting (CbCR) as a baseline standard, maintaining thorough documentation is non-negotiable. For companies with basic marketing and distribution activities, the OECD's Amount B offers a streamlined method [2].

When dealing with intra-group debt or capital movements, consider the "halo effect" - how being part of a larger group influences a subsidiary’s credit rating and borrowing capacity. For example, if market interest rates fall, evaluate whether an independent borrower would refinance under similar conditions [4]. As EY points out:

"Transfer pricing analysis is highly dependent on facts and circumstances that may vary significantly between taxpayers" [4].

Make sure that entities earning financing income or holding assets have enough operational substance to justify their profit allocation [4]. Given the intricacies involved, seeking specialized advisory services is often a smart move.

OECD guidelines offer flexibility by listing factors to consider rather than setting rigid rules [4]. While this flexibility is helpful, it also opens the door to interpretation challenges that professional advisors are well-equipped to address. Advisors can help businesses implement compliant structures and avoid risks like tax authorities reclassifying long-term loans as short-term debt or equity, which increases audit exposure [4]. As EY cautions:

"Loan recharacterization has the potential to be a significant source of controversy, because there are many ways in which a particular loan could have been structured, and it could be difficult to prove, after the fact, how unrelated parties would have decided to borrow or lend" [4].

Advisors conduct in-depth functional analyses to identify the true bearer of investment and financial risks, reducing the likelihood of profit reallocations due to limited operational substance on the lender’s side [4]. They also help bridge gaps between OECD guidelines and local laws, such as US Treasury Regulations, which can otherwise lead to double taxation and complex resolution processes [4].

For mid-market businesses, partnering with professional advisors early in the exit planning process can be a game changer. Firms like Phoenix Strategy Group (https://phoenixstrategy.group) specialize in fractional CFO services and M&A advisory tailored for growth-stage companies. Their comprehensive approach - combining financial modeling, cash flow forecasting, and strategic planning - helps businesses structure transactions that comply with OECD standards while minimizing tax risks. Without in-house expertise, mid-market companies can benefit significantly from early engagement with advisors to ensure their documentation and strategies hold up under regulatory scrutiny.

Navigating cross-border exits demands a solid grasp of OECD transfer pricing principles to sidestep costly mistakes. At the heart of this is the arm's length principle, which acts as the global benchmark for valuing transactions between related entities. Following these guidelines is critical to reducing the risk of economic double taxation - a common issue when two countries disagree on how a cross-border transaction should be compensated [3][16]. With over 115 jurisdictions now enforcing Country-by-Country Reporting as a baseline standard [2], multinational transactions are under more scrutiny than ever.

For mid-market businesses, the stakes are even higher. The OECD highlights this challenge:

"For taxpayers, it is essential to limit the risks of economic double taxation that may result from a dispute between two countries on the determination of the arm's length remuneration for their cross-border transactions with associated enterprises" [3].

Failing to maintain proper documentation can lead to reclassification of exit structures, creating additional risks [4].

To address these challenges, businesses must prioritize substance over form when structuring exit transactions. Tax authorities are increasingly focused on whether entities receiving profits have the necessary substance - such as personnel and decision-making capabilities - to justify those allocations. Conducting a thorough functional analysis is key to proving that an entity is equipped to manage the associated risks. Additionally, the OECD's emphasis on "options realistically available" underscores the need to document why a specific exit structure was chosen over other viable alternatives [4].

Recent global tax updates add another layer of complexity. Changes to the OECD Transfer Pricing Guidelines, including the February 2024 guidance on "Amount B" for baseline marketing and distribution activities [2], reflect ongoing efforts to balance simplified compliance with rigorous oversight. These updates, combined with the practical risks discussed earlier, highlight the need for an integrated approach. Early engagement with professional advisors can make all the difference, helping businesses avoid drawn-out tax disputes and ensuring a smoother exit process.

Investing in proper planning, robust documentation, and expert advice ensures your exit strategy aligns with both economic realities and regulatory expectations. For tailored solutions, visit Phoenix Strategy Group.

The Arm’s Length Principle is an internationally accepted guideline that mandates transactions between related entities - like subsidiaries and parent companies - be priced as though they were conducted between independent, unrelated businesses. This approach helps ensure profits are distributed fairly and accurately across different countries.

When it comes to cross-border business exits, applying the Arm’s Length Principle becomes especially important. It helps prevent challenges such as double taxation or conflicts with tax authorities. By following this principle, businesses align with global standards like those outlined by the OECD, making the exit process more seamless and compliant.

To align with the OECD transfer pricing guidelines during a cross-border exit, mid-market businesses should prioritize a few critical steps:

Focusing on these areas can help businesses manage the complexities of transfer pricing and reduce potential tax exposure during an exit.

Cross-border asset transfers can bring about notable tax challenges, as tax authorities often scrutinize whether the transfer price aligns with an arm’s-length value. If the price is set too low, the source country might impose extra corporate taxes or withholding taxes on the perceived gains. Conversely, an inflated price could lead to double taxation, where both jurisdictions tax the same economic benefit. The OECD Transfer Pricing Guidelines stress the need for precise pricing to avoid disputes and potential penalties.

To tackle these challenges, businesses should prioritize thorough documentation and careful planning. Employing recognized valuation methods, such as comparable transaction analysis or discounted cash flow models, helps validate the transfer price. Securing an Advance Pricing Agreement (APA) or utilizing a Mutual Agreement Procedure (MAP) with tax authorities can also provide clarity and reduce the risk of adjustments. Additionally, structuring the transaction wisely - like timing it in line with tax treaties or adjusting the asset’s basis - can significantly lower tax exposure. Phoenix Strategy Group offers specialized support in these areas, providing expert valuations, detailed documentation, and strategic advice to ensure a seamless and tax-efficient process.