Published on

December 26, 2025

A reverse 1031 exchange lets you buy a replacement property before selling your current one, helping you secure investments in competitive markets while deferring taxes. Here’s how it works and why it matters:

This strategy offers tax deferral and timing advantages but requires careful planning and professional guidance to avoid pitfalls.

Reverse 1031 Exchange Timeline and Process Steps

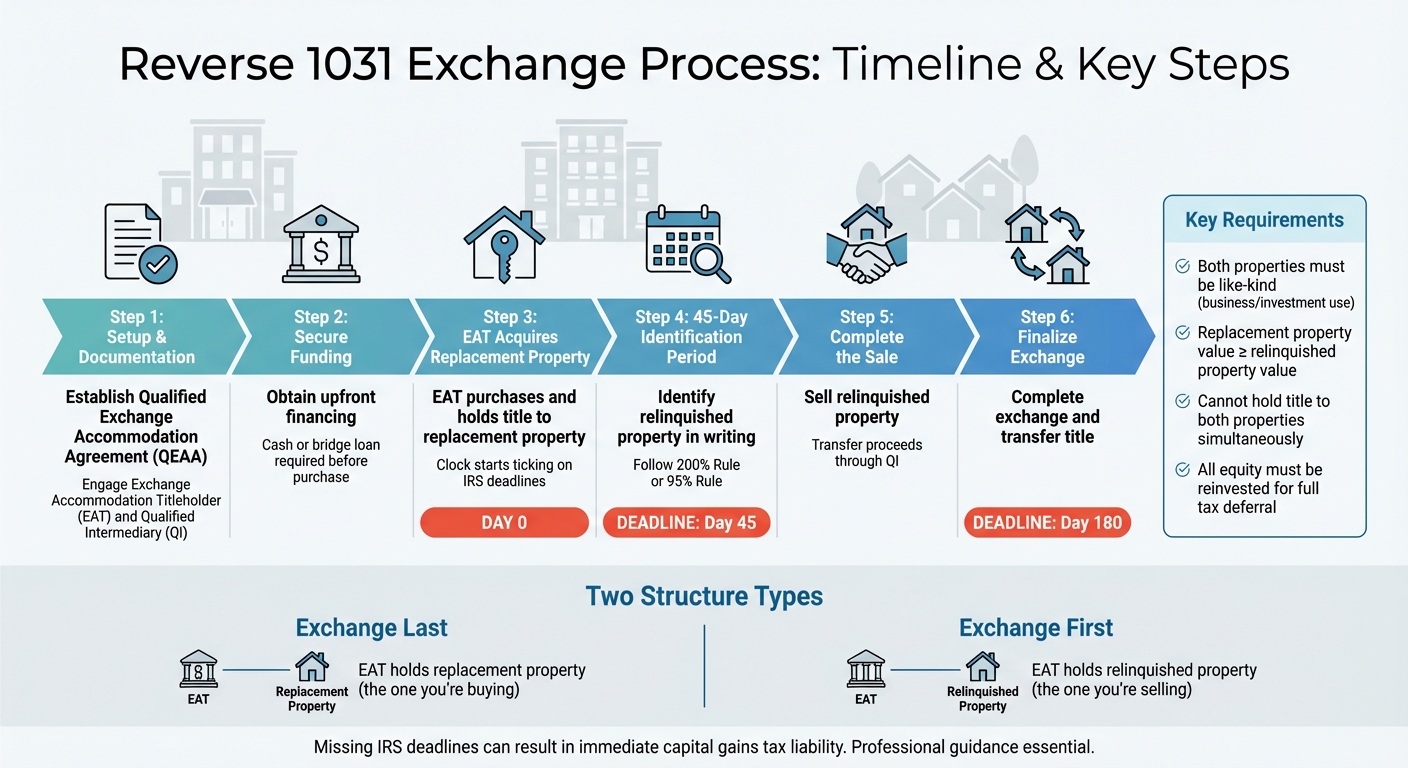

A reverse 1031 exchange is a carefully orchestrated process that hinges on strict adherence to IRS rules and deadlines. At the heart of this transaction is the Exchange Accommodation Titleholder (EAT), who temporarily holds the title to one of the properties to meet IRS requirements [11]. You’ll also need a Qualified Intermediary (QI) to oversee the exchange and ensure compliance with IRS safe harbor guidelines as outlined in Revenue Procedure 2000-37 [11].

The process kicks off with a written Qualified Exchange Accommodation Agreement (QEAA), which sets the legal groundwork [11]. Since this strategy involves purchasing a property before selling another, you’ll need to secure full funding upfront, either through cash or bridge financing [8]. During this interim period, the EAT may lease the property back to you under a triple net lease, allowing you to manage it while also reporting any related income and expenses [13].

The EAT plays a critical role by serving as the temporary legal owner of either the replacement property or the relinquished property, depending on the structure you choose. In an "Exchange Last" setup, the EAT holds the replacement property you’re acquiring. In an "Exchange First" arrangement, it holds the relinquished property you’re selling [12].

This step is necessary because IRS rules prohibit you from holding title to both properties at the same time. The EAT satisfies the requirement for "qualified indicia of ownership" by holding legal title while you maintain beneficial ownership and control [8]. As attorney Gary B. Shulman from Levun, Goodman & Cohen, LLP explains:

"Under Section 1031, the taxpayer cannot own or hold title to both the relinquished property and the replacement property at the same time or the exchange will fail." [11]

It’s worth noting, however:

"The need for an EAT makes a reverse 1031 process pricier than a typical forward 1031 exchange." [11]

This means you’ll need to account for higher administrative and legal costs when planning your budget. With the EAT’s role established, the process moves forward under strict IRS timelines.

Once the EAT acquires the replacement property, the clock starts ticking. You have 45 days to formally identify, in writing, the property you plan to relinquish [11]. This is essentially the reverse of a forward exchange, where replacement properties are identified instead. Then, within 180 days of the EAT’s acquisition of the replacement property, you must sell your relinquished property and complete the exchange [11].

When identifying properties, you can follow one of two rules:

Additionally, both the relinquished and replacement properties must be like-kind (used for business or investment purposes), and the replacement property must have a value equal to or greater than the relinquished property to achieve full tax deferral [11]. Missing these deadlines or requirements could result in losing the tax-deferral benefits, so working closely with tax professionals to ensure timely and accurate documentation is essential [8].

The reverse 1031 exchange structure isn’t just a clever way to manage real estate transactions - it also comes with some appealing tax perks. One of the biggest benefits is the ability to defer capital gains taxes when selling a property. By treating the sale as a nonrecognition event, you avoid paying those taxes right away. This essentially gives you access to interest-free reinvestment capital, allowing you to reinvest your full equity into new opportunities and grow your wealth over time [3][14]. Plus, if you hold onto the replacement property until your passing, your heirs could benefit from a "stepped-up basis" to the current market value, potentially erasing the deferred tax liability altogether [14]. Below, we’ll dive into how tax deferral and timing flexibility can strengthen your investment strategy.

One standout advantage of a reverse 1031 exchange is the ability to reinvest your entire equity position into a new property without triggering an immediate taxable event. To fully defer taxes, the replacement property must match or exceed the fair market value and equity of the property you’re selling [1][14]. For example, if you sell a property for $800,000 with $200,000 in equity, the new property needs to be worth at least $800,000, with a minimum $200,000 equity investment. This deferral strategy ensures that all your equity stays intact, giving you the financial flexibility to acquire higher-value or more profitable properties. It also opens the door to diversifying your portfolio, consolidating your assets, or upgrading to properties with better cash flow [15][16].

By keeping more capital in play, you can accelerate your portfolio’s growth. As 1031 Specialists explains:

"By deferring taxes, investors can potentially grow their real estate portfolios at a faster rate and increase their long-term wealth." [10]

Beyond tax deferral, reverse exchanges offer a major advantage in terms of timing. This flexibility helps protect your investments and reduces exposure to market risks. Michael Torhan, Tax Partner at EisnerAmper, highlights this benefit:

"The benefits of a reverse 1031 exchange are generally a function of a taxpayer's ability to close on replacement property without having to first sell a property." [3]

This timing advantage allows you to lock in current market prices for your replacement property before selling your existing asset. That means you’re shielded from potential price increases that could complicate your plans. Without the pressure of an immediate sale, you also gain stronger negotiating power, which can lead to better offers on the property you’re relinquishing [8][9].

Additionally, the 45-day identification period gives you time to choose which property to sell, helping you align sale proceeds for optimal tax deferral. While the property is held by an Exchange Accommodation Titleholder (EAT), you can even make improvements or renovations to boost its value before officially transferring the title [6][7]. This added flexibility ensures you’re in the best possible position to maximize your investment.

Both reverse and forward exchanges allow you to defer capital gains taxes, but the key difference lies in the order of transactions. In a reverse exchange, you purchase the replacement property before selling the original one. This reversed sequence introduces more complexity, higher costs, and greater risk.

Your decision between these two methods often depends on market dynamics and your financial readiness. Forward exchanges are ideal when you have the luxury of time and flexibility. On the other hand, reverse exchanges are particularly advantageous in competitive markets where desirable properties are snatched up quickly. However, reverse exchanges demand upfront capital or bridge financing since the proceeds from the sale of your original property aren't available to fund the new purchase. These differences go beyond logistics - they carry distinct financial risks and rewards.

While both exchanges aim to defer the same taxes, the process for each is quite different. Here's a side-by-side comparison:

| Feature | Forward 1031 Exchange | Reverse 1031 Exchange |

|---|---|---|

| Sequence | Sell the old property first, then buy the new one | Buy the new property first, then sell the old one |

| 45-Day Rule | Identify potential replacement properties | Identify the property you plan to sell |

| 180-Day Rule | Deadline to finalize the purchase of the replacement property | Deadline to complete the sale of the original property |

| Title Holding | A qualified intermediary holds the sale proceeds; you take title to the replacement property | An Exchange Accommodation Titleholder (EAT) holds title to one property to avoid dual ownership |

| Financing | Sale proceeds fund the purchase | Requires upfront funds or a loan before selling the original property |

| Cost | Standard intermediary fees apply | Higher fees due to EAT setup and legal complexities |

| Depreciation | Begins when the replacement property is acquired | Cannot be claimed while the EAT holds the title |

| Main Risk | Difficulty in identifying a replacement property within the time limit | Risk of failing to sell the original property within the time frame |

Understanding these differences can help you navigate the tax deferral process and evaluate the operational demands of each type of exchange. As Levun, Goodman & Cohen, LLP explains:

"The need for an EAT makes a reverse 1031 process pricier than a typical forward 1031 exchange." [11]

If you're considering a reverse exchange, it's essential to ensure you have the financial resources and a clear plan to sell the original property within the 180-day window. Without these, the added costs and risks may outweigh the benefits.

Reverse 1031 exchanges can offer appealing tax advantages, but they’re not without risks. Missteps can lead to unexpected tax liabilities, making it essential to understand the potential pitfalls. Let’s break down some of the key risks, starting with boot and taxable gains.

Boot, or non-like-kind property, includes cash, personal property, or debt relief you might receive during an exchange [20][4]. The IRS treats boot as taxable income, so even if most of your exchange qualifies for tax deferral, any boot received will still result in taxes owed.

In reverse exchanges, boot risks can become particularly complicated. Since you purchase the replacement property before selling the original one, you might not know the final sale price of the relinquished property [11]. Boot can also arise from differences in mortgage amounts. For example, if your original property has a $500,000 mortgage but you assume only $400,000 on the replacement property, the $100,000 difference is considered taxable mortgage boot [14]. Additionally, using proceeds from the sale to pay off a loan, cover certain closing costs, or handle prorated property taxes can also trigger boot [20].

To sidestep these issues, you might consider contributing outside cash to cover a lower mortgage amount or paying non-qualifying costs out of pocket instead of using exchange funds [14][20]. As Michael Torhan, Tax Partner at EisnerAmper, explains:

"The receipt of cash or mortgage boot in an exchange could generate gain to a taxpayer." [3]

While the Exchange Accommodation Titleholder (EAT) structure helps maintain tax deferral, it comes with its own set of drawbacks. When the EAT holds title to the replacement property, you can’t claim depreciation deductions because, for tax purposes, you aren’t considered the legal owner during that time [3]. Under a Qualified Exchange Accommodation Arrangement (QEAA), the EAT is treated as the beneficial owner, meaning any tax benefits tied to ownership - like depreciation - belong to the EAT.

If your reverse exchange spans two tax years, this lack of depreciation deductions can increase your taxable income during the holding period [3]. Michael Torhan highlights this issue:

"While the EAT owns the replacement property, the taxpayer is not entitled to claim depreciation on such property because it is not deemed to own it for tax purposes." [3]

Careful planning is essential to manage the potential tax impact during this period.

Reverse exchanges come with strict IRS deadlines, and missing them can result in immediate capital gains taxes on the entire transaction. Extensions are rarely granted, except in cases like federally declared natural disasters [18][19].

Failing to meet these deadlines could lead to capital gains taxes of up to 20%, along with depreciation recapture taxed at higher ordinary income rates [17][18]. One of the biggest risks is not selling your original property within the 180-day window. To avoid this, consider conducting a market analysis and identifying potential buyers before closing on the replacement property [19]. As Prof. Chad D. Cummings, CPA, Esq., wisely notes:

"If you think hiring a professional is expensive, wait until you hire an amateur." [19]

Engaging a Qualified Intermediary (QI) and an Exchange Accommodation Titleholder (EAT) early in the process can help ensure all legal structures are in place and deadlines are met [18].

Reverse 1031 exchanges offer a powerful way for investors to defer taxes and maintain flexibility by securing a replacement property before selling the original one. This approach not only locks in favorable pricing but also ensures that your full equity remains intact for reinvestment. By deferring capital gains taxes, depreciation recapture, and state taxes, you can keep 100% of your equity working for you, creating opportunities for greater wealth growth over time [2][1].

However, navigating the complexities of reverse exchanges requires careful planning and expert support. From managing the intricacies of the EAT structure to adhering to strict IRS deadlines, there are plenty of moving parts. Missteps, such as triggering boot-related liabilities, can lead to significant tax consequences. As Michael Torhan, Tax Partner at EisnerAmper, points out:

"Since there are multiple parties involved in any 1031 exchange including accountants, attorneys, and QIs, upfront and coordinated consultation with all advisors is recommended to achieve a successful exchange" [21].

To ensure a smooth process, you'll need to work closely with Qualified Intermediaries, tax advisors, and lenders who understand the unique challenges of reverse exchanges. With federal capital gains taxes potentially reaching 37% [22], the stakes are high, and even small errors can result in significant financial setbacks.

Expert guidance is essential for success. Firms like Phoenix Strategy Group (https://phoenixstrategy.group) provide fractional CFO services and financial advisory solutions to help align your tax strategies with your broader investment goals.

When executed correctly, reverse 1031 exchanges preserve your capital and provide strategic advantages. Partnering with qualified professionals ensures you can maximize the benefits while minimizing the risks.

A reverse 1031 exchange carries distinct challenges due to its intricate process and the strict rules set by the IRS. Since it requires purchasing the replacement property before selling the original one, the arrangement involves an Exchange Accommodation Titleholder (EAT) and a qualified intermediary to manage the title and funds temporarily. Any errors in this setup could result in the exchange being disqualified, triggering immediate capital gains taxes.

The IRS also enforces the same 45-day identification window and 180-day exchange period as a traditional 1031 exchange. If selling the original property takes longer than expected, you risk missing these deadlines, which would cancel the tax deferral opportunity. On top of that, reverse exchanges often come with higher legal and intermediary fees, as well as more complicated financing arrangements. These factors can drive up costs and eat into the potential tax savings.

Because of the complexity involved, there’s also a greater chance of mistakes in the paperwork or documentation, which could attract IRS scrutiny and lead to penalties. To reduce these risks, seeking advice from experienced professionals is strongly advised.

An Exchange Accommodation Titleholder (EAT) is a third-party entity that temporarily takes legal ownership of a property during a reverse 1031 exchange. This arrangement ensures that the taxpayer doesn’t simultaneously hold both the replacement and relinquished properties, which would conflict with IRS safe-harbor rules. Typically, the EAT holds the title through a special-purpose entity, such as a single-member LLC, allowing the investor to defer capital gains taxes.

Using an EAT provides investors the ability to purchase the replacement property before selling the relinquished one, offering more control over timing. While the usual 45-day identification period and 180-day completion period remain in effect, the EAT alleviates market-timing challenges by "parking" the replacement property. Additionally, the EAT collaborates closely with a Qualified Intermediary (QI) to ensure all IRS regulations are met, preserving the tax-deferral benefits of a reverse 1031 exchange.

If you miss the 45-day identification deadline or the 180-day closing deadline in a reverse 1031 exchange, the transaction won’t qualify for tax deferral under IRS regulations. Instead, it will be treated as a taxable sale, and you’ll be required to pay capital gains taxes on the property right away.

To prevent this, it’s essential to stick to the IRS's strict timelines and collaborate with knowledgeable professionals who can help you navigate the process.