Published on

April 2, 2026

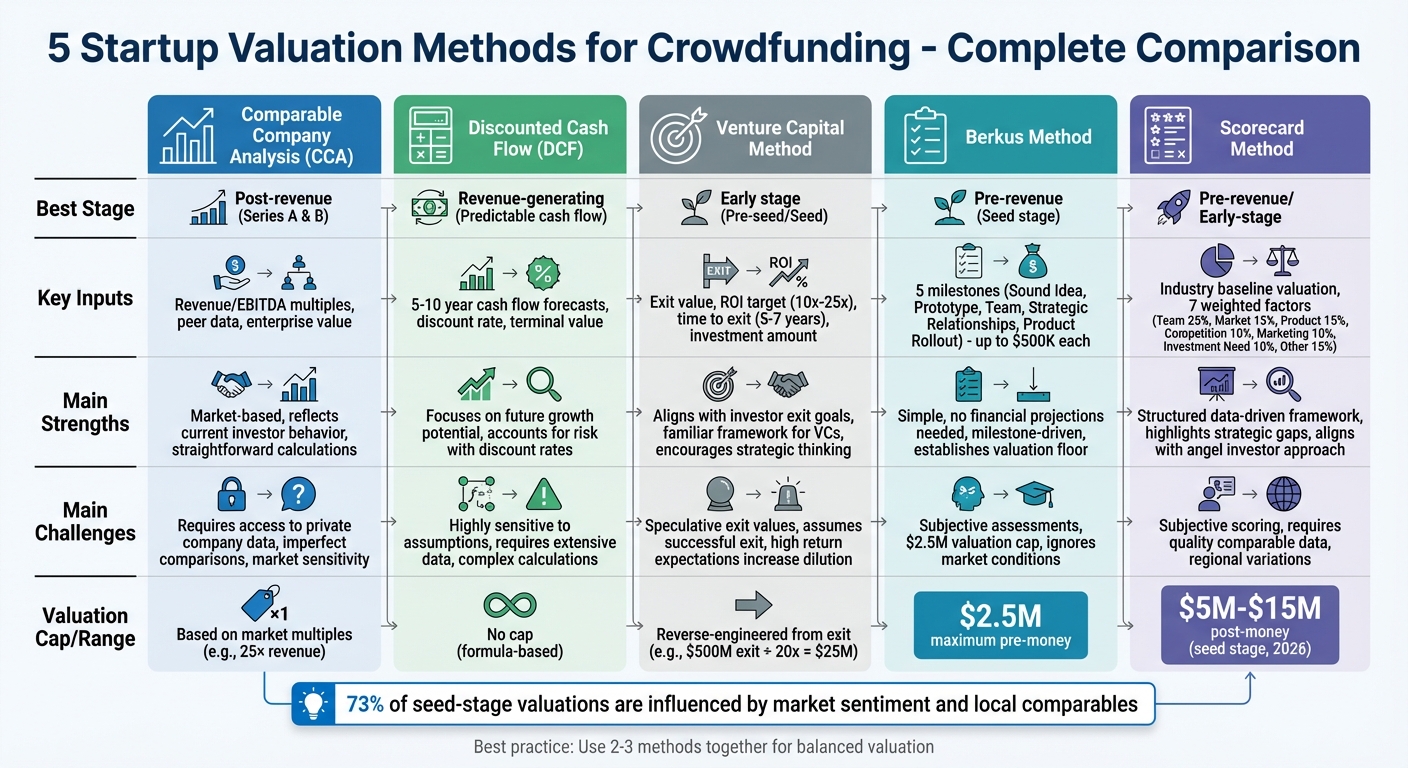

When valuing your startup for crowdfunding, choosing the right method is critical. A solid valuation helps you find the balance between attracting investors and retaining ownership. Here are five popular methods, each suited to different stages of growth:

Quick Comparison:

| Method | Best For | Key Inputs | Strengths | Challenges |

|---|---|---|---|---|

| Comparable Company Analysis | Post-revenue | Revenue/EBITDA multiples, peer data | Market-based, straightforward | Requires access to private data |

| Discounted Cash Flow | Revenue-generating | Cash flow forecasts, discount rate | Focuses on future earnings | Sensitive to assumptions |

| Venture Capital Method | Early stage | Exit value, ROI, investment amount | Aligns with investor goals | Speculative exit values |

| Berkus Method | Pre-revenue | Milestones like team, prototype | Simple and milestone-driven | Subjective and capped valuation |

| Scorecard Method | Early stage | Industry baseline, weighted factors | Structured, highlights strengths | Relies on comparable data |

Using multiple methods can strengthen your case by balancing qualitative and quantitative factors. Tailor your approach to your stage, industry, and investor expectations.

5 Startup Valuation Methods Comparison Chart for Crowdfunding

Comparable Company Analysis (CCA) is a practical way to estimate a startup's valuation in equity crowdfunding. It works by comparing your startup to similar companies in the market, offering a snapshot of what investors are willing to pay for businesses like yours. This method relies on existing market data to calculate valuation benchmarks. For instance, if a comparable company has a 25× revenue multiple and your startup projects $400,000 in annual recurring revenue (ARR), the valuation would be $10 million. [2]

CCA can be applied at various funding stages but is particularly useful for Series A and B startups with a proven product-market fit. [2] For pre-revenue startups, revenue multiples are applied to financial projections for the next 3–5 years. On the other hand, post-revenue companies can use actual trailing twelve months (TTM) data, which adds credibility to the valuation process. [2]

To conduct a CCA effectively, you’ll need the following:

Early-stage startups often focus on revenue multiples, as profitability might still be out of reach. Later-stage companies, however, can incorporate both revenue and EBITDA multiples into their analysis. [2]

Understanding the strengths and limitations of CCA helps refine its use in startup valuation.

| Pros | Cons |

|---|---|

| Market realism: Reflects current investor behavior [2] | Data challenges: Private company financials are often inaccessible without costly tools like Pitchbook [2] |

| Grounded in data: Anchors valuation in real market benchmarks [2] | Imperfect comparisons: Variations in team quality, geography, or growth rates can skew results [3] |

| Straightforward calculations: Easier to apply than models like Discounted Cash Flow when reliable data is available [2] | Market sensitivity: Valuations may reflect short-term market trends rather than long-term potential [2] |

For the most accurate valuation, prioritize comparables that closely match your startup in size and growth trajectory. You can also adjust the final multiple to account for qualitative factors like your team's expertise or proprietary technology. [2] [3]

The Discounted Cash Flow (DCF) method calculates your startup's current value by estimating future cash flows and adjusting them for risk and the time value of money. This approach is particularly suited for startups with a clear roadmap to profitability, as it focuses on future earnings potential rather than just historical data [1]. That said, research involving over 1,000 seed-stage deals revealed that 73% of early-stage valuations are influenced more by market sentiment and local comparables than by DCF models [4].

The formula for DCF is straightforward: DCF = Cash Flow / (1 + r)^n [1]. Here, r represents the risk factor, and n is the year number. For instance, a $200,000 cash flow in Year 1, discounted at a 20% rate, equals about $166,667. By summing up these discounted values over a 5-to-10-year period, you can determine your startup's total valuation. This method is all about future potential, making it distinct from models that focus on past or current data.

DCF works best for post-revenue startups with steady and predictable cash flows. For instance, SaaS companies often rely on consistent subscription revenue, which aligns well with this method. On the other hand, applying DCF to pre-revenue startups can seem overly speculative and may undermine credibility with investors [4].

To perform a DCF analysis, you’ll need several key pieces of data:

Forecasts should include revenue, expenses, and burn rate estimates. It’s critical to base these projections on real-world traction rather than overly optimistic assumptions. Accurate inputs not only strengthen your valuation but also build investor confidence in your growth story. Engaging a fractional CFO can help ensure these financial projections are both realistic and defensible.

| Pros | Cons |

|---|---|

| Focuses on growth potential rather than past performance | Relies heavily on assumptions - small changes in inputs can drastically affect results |

| Accounts for risk by incorporating industry-specific discount rates | Requires extensive data, which early-stage startups might not have |

| Links valuation directly to profitability and cost management | More complex than simpler methods like the Berkus or Scorecard models |

Running best-case, expected, and worst-case scenarios is a smart way to validate your assumptions. To avoid over-reliance on speculative forecasts, consider pairing DCF with other valuation methods, like the Scorecard or Berkus approaches, for a more balanced perspective.

The Venture Capital Method flips the usual valuation process on its head. Instead of starting with current metrics, it works backward from a startup's future exit value to determine its present worth. The key question here is: “What does this company need to sell for in 5 to 7 years to deliver the returns investors are looking for?” Michael Kaufman, Founder & Editor-in-Chief of VC Beast, sums it up perfectly:

"Startup valuations are reverse-engineered from fund economics, not derived from the company's current state." [3]

This approach is a favorite among early-stage investors because it aligns a startup’s valuation with the financial goals of eventual exits.

For startups without a long track record, this method offers a way to estimate value by focusing on the future. Here’s how it works: project the exit value, calculate the required return multiple, divide the exit value by that multiple to find your post-money valuation, and then subtract the current investment amount to determine your pre-money valuation. For instance, if you’re aiming for a $500 million exit in 7 years and investors expect a 20x return, today’s post-money valuation would be $25 million ($500M ÷ 20).

This method is ideal for startups in their early stages, especially those without significant revenue history. It’s a go-to framework for pre-seed and seed-stage founders (who should follow a seed round checklist after securing capital) who may not have much traction yet but show strong growth potential. Investors often consider it the "gold standard" for early-stage valuations because it prioritizes the company’s future promise over its current performance.

To apply the Venture Capital Method effectively, you’ll need these four key elements:

Investors generally aim for returns of 10x to 25x. However, it’s worth noting that only about 10% of investments in a typical portfolio achieve 20x or more, while 70% deliver less than the invested amount [5]. This explains why the required multiples are so high - they’re balancing risk and reward.

| Pros | Cons |

|---|---|

| Familiar framework for professional VCs, boosting credibility | Highly sensitive - small changes in exit value or return expectations can lead to big valuation swings |

| Straightforward formula without complex cash flow modeling | Assumes a successful exit, which might not reflect market uncertainties |

| Encourages strategic thinking about exit plans and market potential | High return expectations can lead to lower valuations and more founder dilution |

The Venture Capital Method aligns valuations with investor expectations, but it’s only as reliable as the assumptions you make about the exit. As Maxim Atanassov puts it:

"Startup valuation isn't really about a brilliant idea, a passionate team, or even early traction. It's about cold, hard math wrapped in a story of risks and rewards." [5]

To avoid relying too heavily on speculative exit values, consider running multiple scenarios - conservative, base case, and optimistic - and compare your projected exit multiples to recent acquisitions in your industry. This can help ground your assumptions in reality.

The Berkus Method offers a practical, milestone-focused approach to valuing startups, steering clear of speculative financial forecasts. This method, developed by venture capitalist Dave Berkus in the mid-1990s, is rooted in his observation that fewer than one in a thousand startups meet or exceed their projected revenues during the planned timelines [6]. Instead of relying on financial projections, the Berkus Method assigns specific monetary values to progress across five measurable milestones.

Here’s the breakdown: The method evaluates five key milestones - Sound Idea (addresses product risk), Prototype (reduces technology risk), Quality Management Team (mitigates execution risk), Strategic Relationships (lowers market and competitive risk), and Product Rollout or Sales (addresses financial or production risk). Each milestone can add up to $500,000 to the valuation, with a maximum pre-money valuation of $2.5 million [6]. By focusing on tangible progress, it bypasses complex financial models. Dave Berkus himself explains:

"Pre-revenue, I do not trust projections, even discounted projections." [8]

This method is ideally suited for pre-revenue startups, particularly those in the pre-seed or seed stages [6]. Once a company starts generating consistent revenue, the method becomes less relevant as investors shift their focus to revenue-based valuation models.

The Berkus Method evaluates five critical components, each contributing up to $500,000 [6]:

| Pros | Cons |

|---|---|

| Straightforward and doesn’t require financial modeling | Highly subjective - different evaluators might assign varying values to the same milestone |

| Avoids reliance on uncertain financial forecasts | The $2.5 million cap may not suit startups in high-growth or capital-intensive industries |

| Provides a defendable valuation floor based on tangible progress | Ignores broader market conditions and the total addressable market |

| Turns investor instincts into a structured process | Oversimplifies the complexities of a business |

The Berkus Method works best as a starting point for early-stage negotiations, establishing a baseline valuation. To get a fuller picture of a startup’s worth, combining it with other methods like the Scorecard Method or Comparable Company Analysis can be helpful. Up next, we’ll dive into the Scorecard Method, which refines valuations through comparative analysis.

The Scorecard Method, often called the Bill Payne Valuation Method, bases your valuation on real-world market data. Instead of assigning fixed dollar amounts to milestones, this approach begins with the average pre-money valuation of similar startups in your industry and region. From there, adjustments are made based on how your company measures up across seven weighted factors [9] [4]. This method is particularly helpful for startups where financial data is scarce. As Maxim Atanassov, Founder of Future Ventures, explains:

"The scorecard valuation method doesn't just spit out a number - it gives you a framework to understand what drives your value in the eyes of angel investors." [9]

The process starts by establishing a baseline valuation (e.g., $4 million for a SaaS startup in New York). Then, adjustments are made using scores for seven factors: Management Team (25%), Market Opportunity (15%), Product/Technology (15%), Competitive Environment (10%), Marketing/Sales Strategy (10%), Need for Investment (10%), and Other Factors (15%). Each factor is scored relative to the average: 100% represents an average score, scores above 100% indicate above-average performance, and below 100% reflects weaker performance. The weighted scores are then multiplied by the baseline to calculate the valuation. This structured approach makes it a strong choice for early-stage startups.

This method is particularly effective for pre-revenue or very early-stage startups, where traditional financial models like DCF aren't practical [9] [7]. Once a company starts generating consistent revenue, investors typically shift to revenue-based valuation methods, reducing the relevance of the Scorecard Method. At this stage, many founders utilize fractional CFO services to manage complex financial modeling and growth strategies.

To use this method, you'll need two key components:

The Management Team carries the most weight at 25%, reflecting the investor belief that execution is often more critical than the idea itself [9]. As of 2026, seed-stage valuations generally range from $5 million to $15 million post-money, depending on the sector and the founders' track record [7].

| Pros | Cons |

|---|---|

| Provides a structured, data-driven framework instead of arbitrary numbers [9] | Scoring can be subjective, with potential for founder bias or inflated self-assessments [9] |

| Highlights strategic gaps (e.g., team weaknesses) before pitching to investors [9] | Relies heavily on finding recent, high-quality data for comparable startups in your specific sector and region [9] [7] |

| Aligns with the approach angel investors often use - 73% of seed-stage valuations are influenced by market sentiment and local comparables [4] | Valuations can vary significantly by region (e.g., a $5M valuation in San Francisco might only be $2M in Cleveland for the same business) [9] |

To get the most out of the Scorecard Method, document your reasoning for each score and revisit your assessment quarterly to reflect changing market conditions [9]. Up next, check out the comparison table to determine which valuation method aligns best with your goals.

Choosing the right valuation method depends heavily on your startup's stage of development. Here's a breakdown of key methods, their ideal applications, required inputs, advantages, and challenges:

| Valuation Method | Ideal Stage | Key Inputs | Pros | Cons |

|---|---|---|---|---|

| Berkus Method | Pre-revenue / Seed | Quality of idea, prototype, management team, strategic relationships, product rollout | Straightforward; avoids reliance on financial projections; reduces investment risk | Limits valuation to $2M–$2.5M; relies on subjective judgments |

| Scorecard Method | Pre-revenue / Early-stage | Average industry valuation, team strength, market opportunity, product/tech, competitive environment | Compares against market standards; provides a structured approach to non-revenue factors | Requires reliable comparable data; subjective factor weighting |

| Venture Capital Method | Series A / B / Exit Planning | Projected exit value (terminal value), required ROI (e.g., 10x), anticipated future dilution | Aligns with investor goals; emphasizes the ultimate exit strategy | Based on speculative exit multiples; overlooks near-term progress |

| Discounted Cash Flow (DCF) | Revenue-generating / Predictable cash flow | 5–10 year cash flow forecasts, discount rate, terminal value | Highlights long-term value and growth potential | Highly sensitive to assumption changes; impractical for early-stage startups |

| Comparable Company Analysis | Later-stage / Active markets | Revenue/EBITDA multiples of similar companies, recent acquisition data, user metrics | Reflects real-world market transactions; easily defensible to investors | Access to private deal data can be limited; startups rarely have perfect comparables |

Interestingly, market sentiment and local comparable data influence as much as 73% of seed-stage valuations [4]. For pre-revenue startups, methods like the Berkus and Scorecard approaches are particularly effective. On the other hand, revenue-generating companies can leverage Comparable Company Analysis or DCF to showcase their progress and validate their value.

Using multiple valuation methods not only strengthens your case with investors but also ensures a more balanced and accurate reflection of your startup's potential. This approach lays a strong groundwork for attracting funding, especially in crowdfunding scenarios.

Choosing the right valuation method isn’t just about running numbers - it’s about shaping your crowdfunding journey and determining how much equity you’ll give up to secure funding. Woosung Chun, CFO of DualEntry, explains it well:

"At the earliest stages, you're not selling future cash flows - you're selling the credibility of your trajectory" [1].

A realistic valuation, grounded in market conditions, builds trust with investors. On the flip side, an overly optimistic figure can lead to down rounds and erode confidence if your startup doesn’t deliver as promised.

To create a strong valuation, consider using a mix of two or three methods. This approach helps validate your assumptions and balances both qualitative and quantitative factors. Pre-revenue startups can focus on qualitative strengths by using the Berkus or Scorecard methods. Meanwhile, startups with revenue can rely on Comparable Company Analysis or DCF to highlight measurable progress. Combining these methods not only strengthens your case but also equips you for more complex funding discussions.

For startups navigating intricate cap tables or advanced funding rounds, expert advice can make all the difference. Phoenix Strategy Group offers fractional CFO services and financial modeling expertise to help startups choose the right valuation methods. Their support includes crafting detailed financial projections, tailoring valuation strategies for your stage and industry, and preparing investor presentations that foster trust and align with your funding goals.

The right valuation method for your startup largely depends on where you are in your growth journey. If you're in the early stages and don't have much financial history to show, methods like market comparables or the venture capital method are commonly used. These focus on your growth potential and the size of your target market.

On the other hand, if your startup is more established with steady revenue and predictable cash flow, methods like discounted cash flow (DCF) or market comparables make more sense. These approaches rely on actual financial performance and industry standards to determine value.

When choosing a discount rate for Discounted Cash Flow (DCF) analysis for startups, it's crucial to account for the high levels of risk and uncertainty they face. For startups, discount rates often range from 15% to 25% or more, reflecting their volatile nature. In contrast, mature companies generally operate with lower rates, typically around 7% to 10%.

To determine the appropriate rate, consider factors such as the risk profile, growth potential, and current market conditions. It's also helpful to adjust the rate based on the company’s stage of development and use scenario modeling to better capture the specific risks involved. This tailored approach ensures the discount rate aligns with the unique challenges and opportunities of the business.

When combining valuation methods, the goal is to merge techniques like market comparables and financial disclosures (such as discounted cash flow) to achieve a more balanced result. Start by using a market comparables analysis to establish a baseline. This gives you a sense of how similar companies are valued in the market. From there, refine your assessment by incorporating financial data and projections, like cash flow forecasts.

It's important to adjust for key factors such as growth rates, company size, and current market conditions. By blending the strengths of each approach, you can create a valuation that's both thorough and reliable.