Published on

May 19, 2026

Selling your e-commerce business is just the beginning. What you do after the sale can determine how much of your earnings you actually keep. Tax planning is critical to avoid losing a significant portion of your proceeds to taxes. Here’s what you need to know:

Proper post-sale planning can save you 15–20% of your sale price. Work with tax experts to structure your deal, manage proceeds, and avoid costly mistakes.

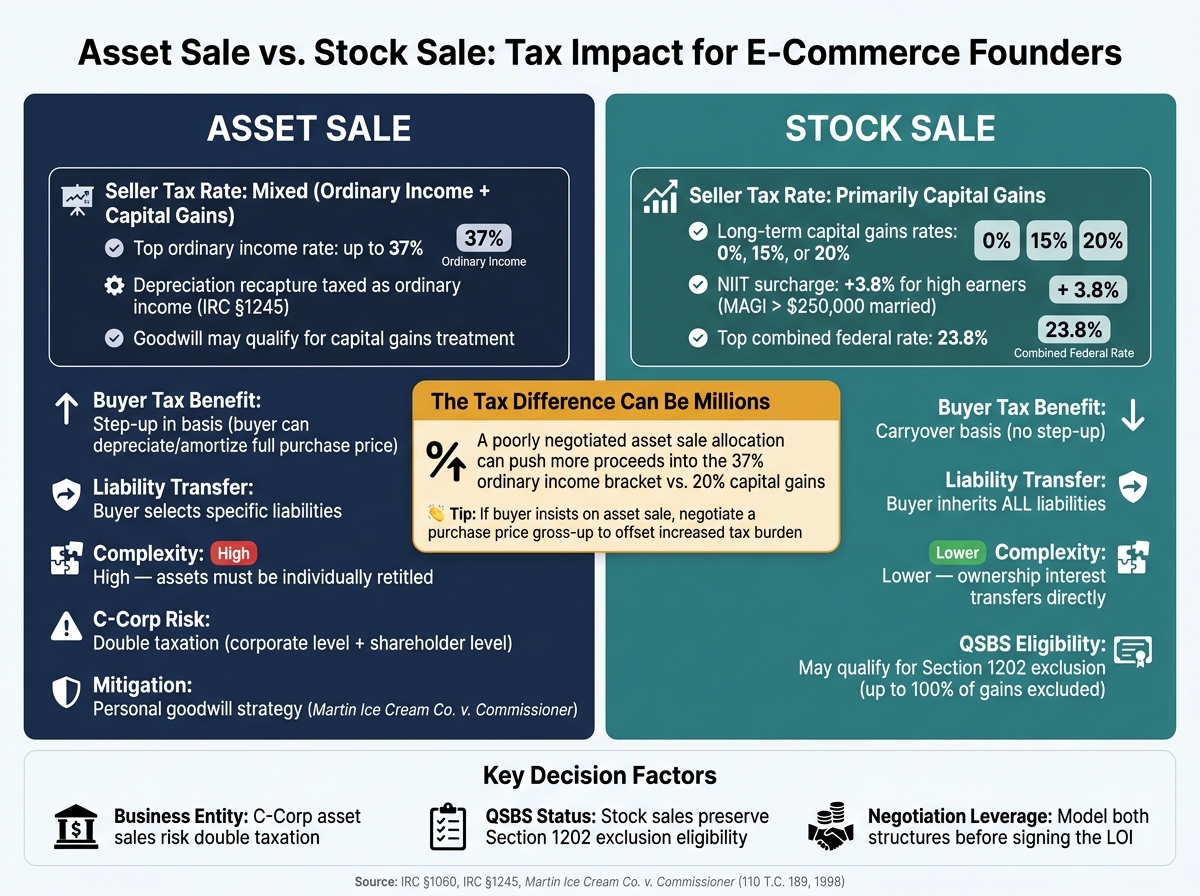

Asset Sale vs. Stock Sale: Tax Impact for E-Commerce Founders

The way your business sale is structured can significantly impact your after-tax proceeds. Two identical sales at the same price can lead to very different tax outcomes depending on whether the deal is set up as an asset sale or a stock sale. Below, we’ll break down how asset and stock sales, installment methods, and equity rollovers influence your tax obligations.

In a stock sale, you sell your ownership stake directly, and the IRS typically taxes the entire gain as a capital gain. This generally results in lower tax rates. On the other hand, an asset sale requires the purchase price to be allocated across various asset categories under IRC §1060. This allocation is important because some assets, such as equipment and inventory, are taxed as ordinary income instead of capital gains.

For e-commerce founders, assets like warehouse equipment and computer hardware are subject to depreciation recapture, which is taxed as ordinary income under IRC §1245. Meanwhile, goodwill often qualifies for capital gains treatment. Poorly negotiated allocations can push more of your proceeds into higher tax brackets.

"In an asset sale, a buyer can cherry-pick the assets it desires to purchase and can elect to exclude certain assets and liabilities. From a tax perspective, buyers benefit from receiving a step-up in basis in the acquired assets." - Cameron Warr, Holland & Hart [5]

Buyers typically prefer asset sales because the step-up in basis allows them to depreciate and amortize the full purchase price over time. This preference gives buyers leverage, so sellers should carefully model both structures before agreeing to a Letter of Intent. If a buyer insists on an asset sale, consider negotiating a purchase price gross-up to offset your increased tax burden.

If your business is a C corporation, asset sales can lead to double taxation - once at the corporate level when assets are sold and again at the shareholder level when proceeds are distributed. One way to mitigate this is through the "personal goodwill" strategy, established in Martin Ice Cream Co. v. Commissioner (110 T.C. 189, 1998). In this case, the Tax Court ruled that intangible assets tied to a founder’s personal relationships and expertise could be allocated directly to the individual, avoiding corporate-level tax on that portion [4].

| Feature | Asset Sale | Stock Sale |

|---|---|---|

| Seller Tax Rate | Mixed (Ordinary Income + Capital Gains) | Primarily Capital Gains |

| Buyer Tax Benefit | Step-up in basis | Carryover basis |

| Liability Transfer | Buyer selects specific liabilities | Buyer inherits all liabilities |

| Complexity | High (assets must be retitled) | Lower (ownership transfers) |

The timing of payments also plays a significant role in your tax liability. If you don’t receive the full purchase price upfront, you might qualify for the installment method under IRC §453. This method lets you spread out the recognition of gain over multiple years, aligning with the timing of payments. By doing so, you could avoid higher marginal tax brackets and reduce exposure to the 3.8% Net Investment Income Tax (NIIT).

Your taxable gain each year is calculated using a gross profit percentage, which divides the total gain by the contract price. This is reported on Form 6252. However, certain gains - like depreciation recapture and inventory gains - are not eligible for installment treatment. These amounts are taxed in full during the year of the sale, regardless of when you receive the cash [6][8].

Additionally, ensure that the interest rate on your installment note meets or exceeds the Applicable Federal Rate (AFR). Falling below this rate can trigger imputed interest rules under IRC §483, leading to additional tax complications [6][8].

Rollover equity can be a valuable tool in your exit strategy, allowing you to retain a stake in the business while deferring capital gains taxes on the rolled portion. This approach is common in acquisitions involving private equity buyers. Instead of cashing out entirely, you keep a percentage of ownership in the post-sale entity, deferring taxes until a future liquidity event [9][7].

To achieve this tax deferral, the transaction often needs to be structured as an F reorganization, which allows the buyer to treat the deal as an asset purchase while preserving the seller’s tax deferral on retained equity. In contrast, a Section 338(h)(10) election benefits the buyer but usually triggers immediate tax recognition for the seller on the rolled portion [9].

"From a tax standpoint, properly structured rollovers can defer recognition of gain on the rolled portion until a later exit. This deferral can be powerful, especially when combined with a subsequent liquidity event." - Matthew McNally, Managing Partner, Evolved LLC [7]

While tax deferral is appealing, retaining equity means you’re still tied to the business’s performance. If the acquiring company underperforms, the value of your retained shares could drop. Carefully weigh the tax advantages against the investment risks, and make sure you fully understand your governance rights and exit timeline before finalizing any rollover agreements [7].

Understanding how capital gains, QSBS rules, and cost basis impact your tax strategy is key to keeping more of what you earn, especially when planning the sale of your business.

The length of time you hold an asset determines how it’s taxed. If you sell equity within a year, the gain is taxed as ordinary income - up to 37%. Hold it longer, and you may qualify for lower capital gains tax rates of 0%, 15%, or 20%. For high-income earners, there’s also a 3.8% Net Investment Income Tax (NIIT) once your Modified Adjusted Gross Income exceeds $250,000 (for married filers). This pushes the top federal rate on long-term gains to 23.8%, which is still much lower than the potential 40.8% combined rate for short-term gains [10].

However, these favorable long-term rates are set to change. Starting in 2026, the top rate for high earners is expected to rise to 39.6%, with the combined rate (including NIIT) reaching 43.4% [10]. This upcoming shift has led many e-commerce founders to fast-track their exits before 2026 to lock in the current, lower rates.

"The difference between paying 5% and 45% effective tax on your life's work usually comes down to planning that starts two, three, or even five years before the closing date." - Tatyana, CEO, TotTax [10]

Now, let’s dive into how the Qualified Small Business Stock (QSBS) exclusion can help reduce your tax burden even further.

If your e-commerce business operates as a domestic C-corporation, you might qualify for the Section 1202 QSBS exclusion, which can exclude up to 100% of your capital gains from federal taxes [3]. To meet the criteria, the stock must be acquired directly from the company - not through a secondary market. Additionally, the company’s gross assets must not have exceeded $50 million at the time of issuance (or $75 million for stock issued after July 4, 2025), and at least 80% of its assets must be used in active business operations [3][13]. While e-commerce and retail businesses often meet these conditions, professional services like law and finance typically do not.

For stock issued on or before July 4, 2025, you must hold it for at least five years to claim the full 100% exclusion. For stock issued after that date, the One Big Beautiful Bill Act (OBBBA) introduces a tiered exclusion: 50% after three years and 75% after four years [11][13].

"Section 1202 rewards patient investors. You (or the person claiming the benefit) must hold the stock for more than five years before selling." - ecomcpa [3]

The exclusion cap for pre-OBBBA stock is the greater of $10 million or 10 times your cost basis. Post-OBBBA stock issued after July 4, 2025, has a higher cap of $15 million, adjusted for inflation [11]. However, some states, like California, don’t align with the federal QSBS exclusion and will tax the full gain at state rates, which can go as high as 13.3% [3][13].

If you sell before meeting the five-year holding period, you could use a Section 1045 rollover. This allows you to defer the gain by reinvesting the proceeds into another qualified small business within 60 days, provided you held the original stock for at least six months [3][11].

To fully benefit from QSBS, understanding your cost basis is critical. Let’s break down how to calculate and adjust it.

Your cost basis - the amount you initially paid for your stock - affects both your taxable gain and the maximum QSBS exclusion you can claim. For example, a founder with a $5 million cost basis could exclude up to $50 million in gains (10× basis), while someone with a near-zero basis would be limited to the flat cap of $10 million (or $15 million for post-OBBBA stock) [12][3].

For stock options, the clock for both the holding period and the cost basis starts only when the options are exercised and converted into shares - not when they’re granted [12]. Similarly, if you raised funds through SAFE notes, the QSBS holding period begins when the SAFE converts into preferred stock [12].

Keeping thorough records is essential. Maintain documentation like board consents, purchase agreements, and payment proofs to substantiate your cost basis.

When reporting the sale, use IRS Form 8949 with adjustment code "Q" to apply the Section 1202 exclusion. This ensures the IRS accounts for your basis adjustment and applies the correct exclusion amount [12].

Where you live when your business deal closes plays a major role in determining your tax obligations. States like California, New York, and New Jersey treat capital gains as ordinary income, which can push combined federal and state tax rates above 50% for high-income earners. On the other hand, states such as Florida, Texas, and Nevada don’t impose state income tax, making them attractive for tax planning.

| State | Top Capital Gains Rate | Treatment |

|---|---|---|

| California | 13.3% | Taxed as ordinary income |

| New York | 10.9% | Taxed as ordinary income |

| New Jersey | 10.75% | Taxed as ordinary income |

| Washington | 7.0% | Special tax on gains over $250,000 |

| Florida | 0% | No state income tax |

| Texas | 0% | No state income tax |

| Nevada | 0% | No state income tax |

For example, if you’re selling a business for $30 million, moving from California to Florida before the sale could save you about $4.3 million in state taxes. On a $50 million deal, the savings jump to over $6.6 million [16]. Clearly, choosing the right residency before selling your business can make a huge difference in your tax burden.

However, changing your address on paper isn’t enough. States rely on "domicile tests" to determine where you're a resident. These tests consider factors like how much time you spend in the state, properties you own, business connections, and even where your family lives [15].

"The state of residency at the time of the sale can influence your state tax liability. Some states have strict 'domicile' tests to determine whether you're subject to their income tax laws." - Reed Brown, CMI Director, State & Local Tax [14]

Timing is also critical. For tax purposes, the date a contract is signed - rather than the closing date - is what matters. Moving after signing but before closing won’t help [16].

If your business operates across multiple states - whether through warehouses, remote employees, or fulfillment centers - you might owe taxes in more than one state, regardless of where you live.

States establish "nexus", or taxable presence, based on physical factors like having a warehouse in the state or economic factors such as exceeding sales thresholds. Once nexus is established, a state can claim a share of your sale proceeds through apportionment rules. Some states base taxes on where customers are located (market-based sourcing), while others tax income based on where the work was done [17].

Stock options can make things even trickier. States like California and New York may tax stock option income based on where it was earned, even if you’ve since moved. For instance, if you spent five years building your business in California before relocating to Texas, California might still tax a portion of your gains [16].

"State tax traps derail deals not because they are always enormous in dollar value, but because they inject uncertainty at the exact moment buyers want certainty." - Zaid Butt, CPA and Partner, Evolved, LLC [17]

To avoid surprises, it’s wise to conduct a SALT (State and Local Tax) nexus study before putting your business on the market. Identifying all states where you have tax obligations can help prevent issues during buyer due diligence, which could otherwise delay or complicate the deal [17].

If your business sale involves installment payments, each payment will be taxed in the year it’s received, based on your residency at that time.

For example, if you move to a no-tax state like Florida after the sale, you might avoid state taxes on future installments. However, staying in a high-tax state like California means each payment will be taxed at the full state rate as it’s received.

There’s a catch: some states, including California, claim the right to tax installment payments even after a founder moves, if the underlying gain was sourced to their state. Consulting a tax attorney familiar with these rules can help you avoid costly surprises later on [16].

Navigating state tax rules can get complicated. For personalized advice on managing these tax implications during your business exit, reach out to the experts at Phoenix Strategy Group.

Next, we’ll dive into strategies for effectively managing your sale proceeds.

Once you’ve considered how state residency affects your tax obligations, it’s time to focus on strategies for handling the proceeds from your sale. For e-commerce founders navigating the post-exit landscape, these approaches can help reduce tax burdens and safeguard wealth for the future.

When a sale generates a large amount of taxable income, the IRS expects taxes to be paid as the income is received. This means you’ll likely need to make quarterly estimated tax payments to avoid penalties. A reliable way to stay compliant is by following the IRS "Safe Harbor" rule: pay at least 110% of your previous year’s tax liability in quarterly installments. This ensures that even if your current year’s tax bill is higher, you won’t face underpayment penalties.

For deals involving earnouts or seller notes, the same principle applies - spread your estimated payments across multiple tax years, not just the year the deal closes.

"If part of your purchase price is deferred (earnouts, seller notes), there are ways to structure these for tax efficiency. But they need to be planned upfront - not figured out at closing." - EcomCPA [1]

To stay ahead, work with a tax professional to calculate your liability and ensure timely payments in April, June, September, and January. Beyond making these payments, exploring strategic asset transfers can further reduce your tax exposure.

Donating a portion of your company shares before the sale closes is another effective strategy for reducing taxes. By contributing appreciated shares to a Donor-Advised Fund (DAF), you can avoid capital gains tax on the donated shares and claim a charitable deduction based on their fair market value (FMV).

For instance, in a $60 million sale, donating 10% of shares (valued at $2 million) before closing could result in a tax benefit of $717,800. In contrast, donating the same $2 million in cash after the sale would yield a much smaller benefit of $344,000 [18].

"Charitable planning must occur before a binding sale agreement is in place. When a deal is effectively locked in, transferring assets may no longer produce the intended tax benefits." - Matthew McNally, Managing Partner, Evolved Tax [7]

Timing is everything. The donation must be completed before signing a binding sale agreement. Since many charities cannot accept privately held stock directly, DAFs are often the best vehicle for these contributions. To claim the deduction, you’ll also need a qualified valuation and a completed IRS Form 8283 [18].

Charitable Remainder Trusts (CRTs) offer another route. With a CRT, you can sell business shares without triggering immediate capital gains, receive an income stream over time, and get a partial charitable deduction [19].

After using charitable donations to lower your taxable income, reinvesting your remaining proceeds can help you defer taxes and create long-term financial growth. Several reinvestment strategies are worth considering:

| Strategy | Tax Benefit | Deadline |

|---|---|---|

| Qualified Opportunity Zone (QOZ) | Defers taxes with potential for tax-free growth after 10 years | 180 days from sale |

| Section 1045 Rollover | Defers QSBS gains into new qualifying stock | 60 days from sale |

| Equity Rollover | Defers gain recognition until a second exit | At closing |

| Installment Sale | Spreads tax liability over payment years | N/A |

Qualified Opportunity Zones (QOZs) are particularly appealing. Reinvesting capital gains into a QOZ fund within 180 days allows you to defer taxes, and if you hold the investment for at least 10 years, any gains generated within the fund can become tax-free [19].

For those selling Qualified Small Business Stock (QSBS) before reaching the five-year holding period, a Section 1045 rollover provides another option. By reinvesting proceeds into another qualifying small business within 60 days, you can defer taxes and restart the holding period clock [3]. These strategies often require precise timing, so close collaboration with your CPA, transaction attorney, and financial advisor is key.

"Tax strategies should enhance a good deal, not rescue a bad one. If complexity outweighs benefit, simplicity may be the better choice." - Matthew McNally, Managing Partner, Evolved [7]

For tailored advice, the team at Phoenix Strategy Group can help you evaluate these strategies and ensure you don’t miss critical deadlines or leave money on the table.

Keeping accurate records and seeking expert guidance after selling your business can simplify tax reporting while helping you secure long-term financial benefits.

After the sale, certain documents are critical for tax reporting. These include the Purchase Agreement, LOI (Letter of Intent), closing statement, and any documents related to profit and loss (P&L) adjustments. These records are the foundation for understanding the legal and financial terms of the transaction.

One particularly important document is IRS Form 8594, which reports how the purchase price is allocated across asset categories. It's crucial for both the buyer and seller to file identical allocations on this form.

"When both sides file the same allocation, you avoid mismatch notices and keep the audit trail clean." - Dylan Gans, Baton Market [20]

Discrepancies between buyer and seller filings can trigger an IRS audit. To avoid this, keep an evidence file with supporting documents like valuations and asset records.

| Document Category | Specific Records to Retain | Purpose |

|---|---|---|

| Transaction Docs | Purchase Agreement, LOI, Closing Statement | Establishes the deal's structure and legal framework |

| Tax Forms | IRS Form 8594, Form 1045 (for rollovers) | Reports asset allocation and gain deferrals |

| Asset Records | Basis schedules, FMV appraisals, inventory lists | Differentiates capital gains from ordinary income |

| Equity Records | Stock certificates, option exercise dates | Verifies QSBS eligibility and holding periods |

| Financials | Accrual-based P&Ls, normalized P&L notes | Supports "add-backs" and reflects profitability |

| Legal | Non-compete agreements, supplier contracts | Justifies allocations to specific intangibles |

With these records in order, you'll be better equipped for accurate tax filings and to claim future deductions.

Your tax obligations don’t end with the sale year. It’s essential to track carryforwards like charitable contributions, net operating losses, and Qualified Small Business Stock (QSBS) records for future filings. For QSBS, retain original stock certificates and records of exercise dates.

If your sale involved installment payments, seller notes, or earnouts, you’ll need to report income on a year-by-year basis. Each payment triggers taxable income, and the breakdown between capital gains and ordinary income depends on the initial deal terms [1][20]. Keeping a detailed schedule of these payments - and cross-checking them with your closing statement - helps ensure accuracy and prevents missed deductions.

Even with well-organized records, working with experienced advisors is key to ensuring tax compliance and maximizing post-sale benefits. A CPA can handle your tax filings and ensure forms like IRS Form 8594 are accurate. Tax attorneys can address complex legal issues, including indemnification clauses and state-specific requirements, while financial advisors can help you manage and invest sale proceeds in the most tax-efficient way.

"Selling your e-commerce business is likely the largest financial transaction of your life. The difference between a prepared seller and an unprepared one isn't small - it's often 20–40% of the final outcome." - EcomCPA [1]

A coordinated team of professionals ensures your records are accurate and integrates them into a broader tax strategy. Whether your transaction involved an asset sale, stock sale, installment terms, or rollover equity, understanding the structure shapes all future tax decisions. For instance, teams like Phoenix Strategy Group specialize in connecting deal structures to long-term financial strategies, offering both M&A advisory and financial planning support.

In short, the work you do after closing - keeping records and collaborating with the right advisors - can have just as much impact as the steps you took before the sale.

Selling your e-commerce business is a big milestone, but what happens after the sale can have just as much impact on your financial future. As EcomCPA explains: "The difference between a well-structured and poorly-structured exit can be 15–20% of the purchase price - after tax" [1]. On a $10 million exit, that’s the difference between keeping an extra $1.5–$2 million or losing it to taxes.

From the strategies outlined earlier, three key principles stand out: Deal structure is the foundation. Whether your transaction is classified as an asset sale or a stock sale determines how your gains are taxed, whether QSBS exclusions apply, and how installment payments are treated. State residency is more important than many founders realize. For instance, living in a state like California, which doesn’t recognize the federal QSBS exclusion, can mean paying full taxes on gains [3]. Together with strategic reinvestment and meticulous recordkeeping, these factors are crucial for long-term financial planning.

Some actionable takeaways include structuring your deal to minimize taxes, using QSBS exclusions to reduce taxable gains, and considering a Section 1045 rollover to defer taxes when reinvesting [3].

"Your post-exit tax strategy matters almost as much as the exit itself." - Kristopher Jones, Founder, Legacy Advisors [2]

Post-exit tax planning isn’t just about filing taxes once - it’s a multi-year strategy. By spreading income over several years, timing charitable contributions wisely, and maintaining detailed records for carryforwards and installment payments, you can amplify your financial benefits. Working with a team of professionals is essential to make the most of these opportunities. For expert guidance, consider consulting firms like Phoenix Strategy Group.

The moment your sale closes is when effective post-exit tax planning truly begins.

Planning to transition from an asset sale to a stock sale? It's smart to start preparing at least two to three years before your planned exit. This early groundwork can significantly influence tax outcomes and give you more room to maneuver during negotiations. By consulting with experts early on, you can fine-tune your approach to match your financial objectives.

To show you've changed your residency before a sale for state tax purposes, take concrete steps like updating your voter registration, opening bank accounts in your new state, filing taxes there, and cutting ties with your previous state. Make sure to keep thorough records, including location data, and start these actions well before the sale. Consistency in showing a permanent relocation is key, as it's up to you to prove the change.

An installment sale could be a good fit for your situation. With this method, you receive payments over a period of time rather than all at once. This allows you to spread out income and report gains gradually. By doing so, you may smooth out your taxable income and even reduce your overall tax bill - especially if it's arranged before the deal is finalized.