Published on

April 2, 2026

Earnouts in M&A deals often defer part of the purchase price, tying payments to future business performance. These agreements frequently lead to disputes due to differing interpretations of performance metrics and their tax treatment. The main issue? Whether payments are taxed as capital gains (favorable for sellers) or ordinary income (beneficial for buyers). Misclassification by the IRS can result in unexpected tax liabilities, including penalties under Section 409A for deferred compensation.

Key points to consider:

Proper planning - such as clear payment terms, separate employment agreements, and compliance with tax rules - can reduce risks and ensure smoother transactions.

Purchase Price vs Compensation Treatment: Tax Implications for Earnout Payments

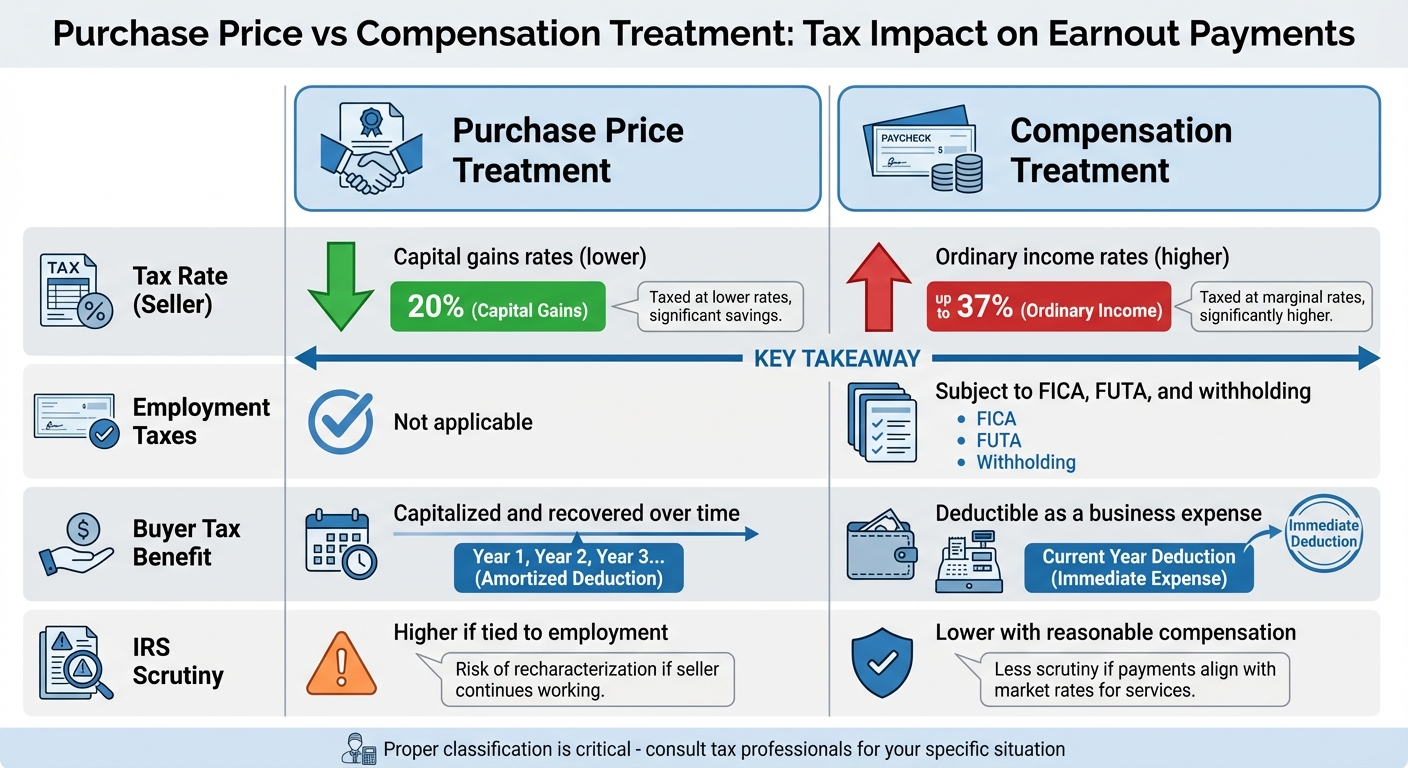

When it comes to earnout disputes, the core issue often revolves around how payments are classified - either as purchase price adjustments or as compensation for services. This distinction has a direct impact on tax rates for sellers and the timing of deductions for buyers. The IRS evaluates these payments using a facts-and-circumstances approach, determining whether they should be treated as part of the purchase price or as compensation. This classification can significantly influence tax outcomes.

For sellers, payments classified as part of the purchase price are taxed at favorable capital gains rates. On the other hand, if the payments are reclassified as compensation, they are taxed as ordinary income and subject to additional employment taxes like FICA and FUTA. Buyers, meanwhile, gain an immediate tax deduction if the payments are treated as compensation. However, if the payments are considered part of the purchase price, they must be capitalized and recovered over time through depreciation or amortization. Below, we’ll break down how these tax treatments affect both sellers and buyers.

The tax treatment of earnout payments depends on several factors. For instance, payments that align with sellers' equity stakes and are not tied to continued employment are more likely to be treated as purchase price adjustments. In contrast, payments linked to ongoing services may be reclassified as wages.

Here’s a quick comparison of the key features of purchase price versus compensation treatment:

| Feature | Purchase Price Treatment | Compensation Treatment |

|---|---|---|

| Tax Rate (Seller) | Capital gains rates (lower) | Ordinary income rates (higher) |

| Employment Taxes | Not applicable | Subject to FICA, FUTA, and withholding |

| Buyer Tax Benefit | Capitalized and recovered over time | Deductible as a business expense |

| IRS Scrutiny | Higher if tied to employment | Lower with reasonable compensation |

The 1994 Lane Processing Trust v. United States case highlights the risks of misclassification. In this case, the 8th Circuit Court of Appeals ruled that payments to employee-owners after a $30 million asset sale were wages, not sales proceeds. This led to unexpected FICA and FUTA tax liabilities for the trust [3].

To reduce the risk of reclassification, it’s essential to provide selling shareholders who remain employed with a separate, market-rate salary for their post-closing work. Additionally, structuring earnout payments based on valuations of similar businesses can help support their classification as purchase price adjustments.

Earnouts classified as deferred compensation must comply with Section 409A of the Internal Revenue Code. If they don’t, sellers face immediate taxation, a 20% penalty, and interest charges [1]. Julie M. Bradlow, a Partner at DarrowEverett LLP, explains:

"Deferred payments of performance-based compensation also implicate Section 409A of the Code, which imposes significant consequences, including upfront taxation and penalties, to nonqualified deferred compensation arrangements that do not comply with, or are not exempt from, its strictures." [1]

Compliance with Section 409A involves adhering to strict timing rules. These include when deferral elections must be made, when payments are triggered, and how schedules are structured. Proper planning is critical to avoid costly penalties and ensure smooth handling of earnout disputes. Engaging a fractional CFO can provide the necessary financial oversight to navigate these complexities.

The timing of earnout payments plays a crucial role in determining tax consequences. For payments treated as part of the purchase price, sellers can often use the installment method. This allows them to defer gain recognition until payments are received, spreading the tax burden over multiple years [3].

However, timing issues become more complex when interest is involved. The IRS typically requires that part of deferred payments be treated as interest, which is taxed as ordinary income. If the agreement doesn’t specify a market interest rate, the IRS will impute one, reclassifying a portion of the payments. Additionally, installment receivables exceeding $5 million at year-end trigger an extra imputed interest charge [2].

When earnout payments are classified as wages, the timing of the payment leads to immediate tax obligations, including income tax withholding and employment taxes like FICA and FUTA. This can create cash flow challenges, especially if reclassification happens years after the transaction, as seen in the Lane Processing Trust case [3].

For earnouts involving restricted stock that vests based on future performance or employment, Section 83 rules dictate when income is recognized. This can significantly impact the timing of tax liabilities for both sellers and buyers, underscoring the importance of tailored tax strategies to minimize potential burdens.

When it comes to earnout disputes, how you structure the settlement can make a big difference in your tax bill. By focusing on characterization, timing, and jurisdiction, you can reduce tax liabilities while staying within federal and state guidelines.

One of the first decisions is whether earnout payments will be treated as a deferred purchase price (taxed at 20% as capital gains) or as compensation (taxed at up to 37% as ordinary income) [4]. This distinction can lead to significant savings, especially in middle-market transactions where earnouts often make up 10% to 30% of the total purchase price [4].

To preserve capital gains treatment, the purchase agreement must clearly state that the earnout payments are part of the business sale and not tied to continued employment. As M&A attorney Alex Lubyansky explains:

"The purchase agreement should state that the earnout is consideration for the sale of the business and not conditioned on continued employment" [4].

If you’re staying with the company post-sale, it’s important to document any employment or consulting compensation separately. This ensures the IRS doesn’t treat the entire earnout as disguised wages. Make sure you’re paid market-rate compensation for your services under a separate agreement to avoid recharacterization issues.

For asset sales, pay attention to Section 1060 allocation. Earnout payments allocated to goodwill often qualify for capital gains treatment, while allocations to other assets may not [4]. When resolving disputes, adjusting these allocations might improve tax outcomes for both parties. Including anti-offset provisions in your settlement can also protect against buyers reducing earnout payments to cover indemnification claims, ensuring consistent tax reporting and safeguarding the settlement’s integrity [4].

The installment method under IRC Section 453 is a useful tool for managing tax liabilities. It allows sellers to defer taxes on earnouts treated as purchase price until payments are actually received [5]. Instead of paying taxes upfront on money you haven’t received, this method spreads the tax burden over several years.

However, if the earnout exceeds $5 million, you’ll face an interest charge on the deferred tax liability. This charge is calculated at the federal short-term rate plus 3% [5]. To avoid overpaying, you can use the look-back method, which calculates deferred tax only as payments come in. This ensures you’re not paying interest on funds you may never receive. Also, the first $5 million of payments received after the sale year is exempt from interest charges, improving cash flow [5].

Alternatively, you can opt out of the installment method and recognize the full fair market value of the earnout in the year of sale. However, this comes with risks. As McDermott Will & Schulte LLP cautions:

"If a seller elects out of the installment method and does not receive the full amount estimated as the fair market value... the seller is not permitted to recompute the amount of income recognized in the year of sale" [5].

This option only makes sense if you’re confident you’ll receive the full payment, as uncollected amounts would leave you with only a capital loss.

After fine-tuning payment characterization and deferral strategies, it’s essential to address both state and federal tax obligations. While federal tax treatment often takes center stage, state tax rules can vary widely. Structuring payments as capital gains usually works better in most states, but you’ll need to consider factors like where you and the buyer are located, where the business operates, and where services are performed.

For earnouts tied to restricted stock that vests based on future performance, Section 83 rules dictate when income is recognized, influencing both federal and state tax timing [1]. If the earnout is reclassified as deferred compensation, ensure compliance with Section 409A to avoid immediate taxation and a 20% penalty [1].

To streamline dispute resolution and ensure consistent tax reporting across jurisdictions, consider including a binding independent accountant’s determination in the settlement [4]. You might also want to add acceleration triggers, which make the remaining earnout payable immediately in cases like a change of control or termination without cause [4]. This simplifies tax compliance by consolidating payments into a single tax year while protecting your financial interests.

In Lane Processing Trust v. U.S., the IRS reclassified earnout payments from capital gains to ordinary income. Why? The payments were tied to the seller's employment duration and prior salary levels rather than the actual value of the business being sold [1]. This reclassification led to a much higher tax bill since ordinary income is typically taxed at a higher rate than capital gains.

This case highlights the importance of the "origin of the claim" theory from Arrowsmith v. Commissioner. Payments stemming from the sale of a business - rather than ongoing services - can qualify for capital gains treatment [1]. To ensure this, it’s crucial that earnout payments are tied to equity ownership and not contingent on continued employment or performance.

Let’s look at a seller with a $200,000 basis in a $1,000,000 sale. Using the installment method, an 80% gross profit ratio means $240,000 of a $300,000 payment would be taxable. However, by electing out of the installment method, the seller can recognize the gain based on the fair market value of the contingent right at the time of closing [2].

This approach speeds up basis recovery, which can significantly reduce the tax burden in the early years - critical for sellers who need cash flow during that period. Sellers can also request an alternative basis recovery method that doubles the speed of basis recovery, further easing their tax obligations in those early years [2].

These case studies reveal several important tax planning strategies:

These lessons underline the importance of careful planning and structuring to minimize tax liabilities and avoid costly disputes.

Handling earnout disputes requires careful planning. The classification of payments plays a huge role in determining your tax outcome. Payments treated as purchase price qualify for capital gains taxation, which sellers prefer, while buyers often push for compensation treatment to gain deductibility [2].

Timing matters too. Using the installment method allows you to spread out gain recognition, while opting out can speed up basis recovery when it makes sense. But if the agreement lacks a clear maximum price or time frame, you could face a default 15-year basis recovery period, delaying tax benefits unnecessarily [2]. Setting a maximum sales price by the end of the year simplifies things and provides clarity.

Compliance with Section 409A is another critical factor. As Julie M. Bradlow, Partner at DarrowEverett, explains:

"Deferred payments of performance-based compensation also implicate Section 409A of the Code, which imposes significant consequences, including upfront taxation and penalties" [1].

Proper structuring is key to avoiding these penalties and ensuring smooth transactions.

These strategies highlight why having expert guidance is essential when dealing with earnout disputes.

The tax complexities tied to earnout disputes are not something you should tackle alone. Joseph E. Hunt IV, Partner at Morse, points out:

"Buyers and sellers may have adverse interests in the character of the payments, so advance planning and careful negotiation is recommended" [2].

Experienced advisors can help balance these conflicting interests through strategic planning and negotiation.

Phoenix Strategy Group specializes in M&A advisory services tailored for growth-stage companies navigating these challenges. Their expertise includes structuring transactions, managing basis recovery strategies, and ensuring compliance with regulations like Section 409A. They also provide fractional CFO support and financial modeling to address imputed interest rules and IRS recharacterization risks. Engaging professionals early in the process - before finalizing your earnout agreement - helps lock in favorable tax outcomes and avoids future disputes.

To have an earnout taxed at capital gains rates, tie it to business performance metrics rather than personal services. It's essential to document everything properly, ensuring the payments are treated as part of the purchase price rather than compensation. This strategy allows you to benefit from the lower capital gains tax rates, which typically range from 15% to 20%.

An earnout can lead to Section 409A penalties if it is considered deferred compensation but does not align with IRS regulations. This misstep may result in hefty tax penalties. To sidestep these complications, it’s crucial to structure the earnout correctly and ensure it adheres to the relevant tax requirements.

Yes, using the installment method for an earnout can help spread income over several years, which may reduce immediate tax obligations. This approach ties tax recognition to the actual payments received, offering better cash flow management. However, it’s essential to structure and document the arrangement correctly to stay compliant with tax regulations and make the most of this method.