Published on

May 12, 2026

If you're a real estate investor looking to defer taxes on a property sale, transitioning from a 1031 exchange into a Delaware Statutory Trust (DST) could be a smart move. Here's why:

This strategy simplifies property ownership while maximizing tax deferral, but it requires careful planning to align with your financial goals.

A 1031 exchange, named after Internal Revenue Code Section 1031, allows real estate investors to sell one investment property and reinvest the proceeds into a "like-kind" property without immediately paying capital gains taxes. Here's how the code itself defines it:

"No gain or loss shall be recognized on the exchange of property held for productive use in a trade or business or for investment, if such property is exchanged solely for property of like-kind which is to be held either for productive use in a trade or business or for investment." - Internal Revenue Code §1031 [6]

It’s important to note that this is a tax deferral strategy, not a tax elimination. By deferring taxes, investors can reinvest the full proceeds, which helps grow their equity over time. Let’s take a closer look at the rules that make a 1031 exchange valid.

For a 1031 exchange to qualify, both the property being sold (called the relinquished property) and the one being purchased (the replacement property) must be used for investment or business purposes. Properties like personal residences or those intended for quick resale, such as fix-and-flip projects, don’t meet the criteria. The IRS interprets "like-kind" broadly, meaning you can exchange different types of investment properties - for instance, swapping an apartment building for a piece of industrial land [5].

Timing is critical. There are two strict deadlines to follow:

To simplify the identification process, many investors rely on the three-property rule, which allows you to list up to three potential replacement properties without worrying about their combined value [1].

Another key requirement is the use of a Qualified Intermediary (QI). The QI holds the proceeds from your sale in escrow to ensure you don’t have direct access to the funds. If the money touches your personal account, even briefly, the exchange is invalid [5][7]. The typical cost for QI services ranges from $800 to $1,500 [1].

When these rules are followed, the tax advantages of a 1031 exchange become a powerful tool for investors.

The financial benefits of a 1031 exchange are substantial. By deferring taxes, investors avoid paying up to 20% in federal capital gains taxes, an additional 3.8% Net Investment Income Tax (NIIT), and depreciation recapture taxes, which can be as high as 25% [1][7]. This means the entire proceeds from the sale can be reinvested, rather than just the after-tax amount.

To fully defer taxes, the replacement property must be of equal or greater value than the relinquished property, and all proceeds must be reinvested. Any leftover cash or reduction in debt (referred to as "boot") is immediately taxable [1][7].

For those who continue using 1031 exchanges throughout their lifetime, taxes can be deferred indefinitely. Additionally, heirs inherit the property at its current market value, potentially eliminating the deferred tax liability altogether [1][7].

Understanding these tax benefits is essential before diving into other investment options, like DSTs, which can further enhance the advantages of a 1031 exchange.

A Delaware Statutory Trust (DST) is a legal structure that allows multiple investors to own fractional interests in high-quality real estate. Think of it as a way to co-own premium real estate properties without the hassle of daily management. Thanks to IRS Revenue Ruling 2004-86, an investor’s share in a DST is treated as direct real estate ownership, making it eligible for a 1031 exchange.

"A DST is a legal entity formed under Delaware law that allows passive, fractional ownership in real estate while qualifying as 'like-kind' replacement property under Section 1031." - Mike Bonaventure, Chief Growth Officer, Bonaventure [3]

In a DST, a professional sponsor handles everything - leasing, maintenance, debt payments, and eventually selling the property. As an investor, you hold a fractional interest in the trust and receive your share of the income. However, you don’t have voting rights or management responsibilities.

To maintain 1031 exchange eligibility, DSTs must comply with seven strict IRS rules, often referred to as the "Seven Deadlies." These rules prohibit certain activities, such as taking on new debt, accepting additional capital after the offering closes, or making significant property upgrades beyond basic maintenance.

DSTs typically manage large, institutional-grade properties worth between $30 million and $100 million. These include assets like multifamily housing, industrial facilities, and net-lease retail spaces. The minimum investment is usually $100,000, making it accessible for 1031 exchange participants [4]. Additionally, DSTs utilize non-recourse, pre-arranged financing, which means your share of the debt satisfies 1031 debt-replacement rules without requiring you to personally qualify for a loan.

DST investments are illiquid, meaning there’s no active secondary market for selling your interest. Once you invest, you’re generally committed until the sponsor decides to sell the property. Holding periods typically range from 5 to 10 years [4][8].

When the property is sold, you have three main options:

Each choice has its own tax consequences, so your decision will depend on your financial goals when the sale occurs. This structure makes DSTs an attractive option for investors looking to maximize the benefits of a 1031 exchange.

When it comes to 1031 exchanges, timing and diversification can be tricky to navigate. This is where Delaware Statutory Trusts (DSTs) step in, offering solutions that traditional property ownership often can’t match. By addressing the challenge of finding suitable replacement properties quickly, DSTs bring added benefits that go beyond just meeting IRS requirements.

One major advantage of DSTs is their ability to defer both federal and state capital gains taxes, as well as depreciation recapture. On top of that, heirs often benefit from a step-up in basis upon inheritance, which can wipe out the deferred tax liability entirely [3][1].

But the perks don’t stop there. DSTs open doors to high-quality, diversified assets that might be out of reach for individual investors. Think Class A apartments or medical offices - premium properties that are typically reserved for institutional players. Plus, DSTs allow for exact-dollar reinvestment, eliminating the risk of taxable boot [1][2][3].

Another standout feature is diversification. With a single exchange, investors can spread their capital across various property types and locations. For instance, an investor with $1 million could allocate funds like this: 35% to Sunbelt multifamily properties, 25% to net-lease retail with investment-grade tenants, 20% to industrial distribution, and 20% to medical offices. This kind of sector and geographic diversification would be nearly impossible to achieve through direct ownership [1].

These benefits become even more compelling when you compare DSTs to traditional property ownership.

Here’s a side-by-side look at how DSTs stack up against direct property ownership:

| Feature | DST | Direct Property Ownership |

|---|---|---|

| Management Effort | Minimal - professional sponsor handles everything | High - owner manages tenants, repairs, and leasing |

| Liquidity | Low - illiquid with 5–10 year hold periods | Moderate - owner decides when to sell |

| Tax Deferral | Preserved via 1031 exchange | Preserved via 1031 exchange |

| Income Potential | Steady - historical cash-on-cash returns of 5%–9% annually [3] | Variable - depends on occupancy, market, and management |

| Debt Liability | Non-recourse - no personal guarantee required [3][1] | Often recourse - owner personally qualifies for the loan |

| Diversification | High - spread across multiple assets and sectors [3][1] | Low - capital concentrated in one or two properties [1] |

"DSTs provide a path to defer capital gains taxes while eliminating active management responsibilities." - Thomas Wall, Partner, Anchor1031 [1]

The choice between DSTs and direct ownership often boils down to priorities. DSTs offer efficiency, professional management, and broad exposure, making them an attractive option for investors looking to simplify their portfolios or diversify across markets. For those weary of the hands-on demands of property management, DSTs provide a streamlined, tax-deferred exit strategy.

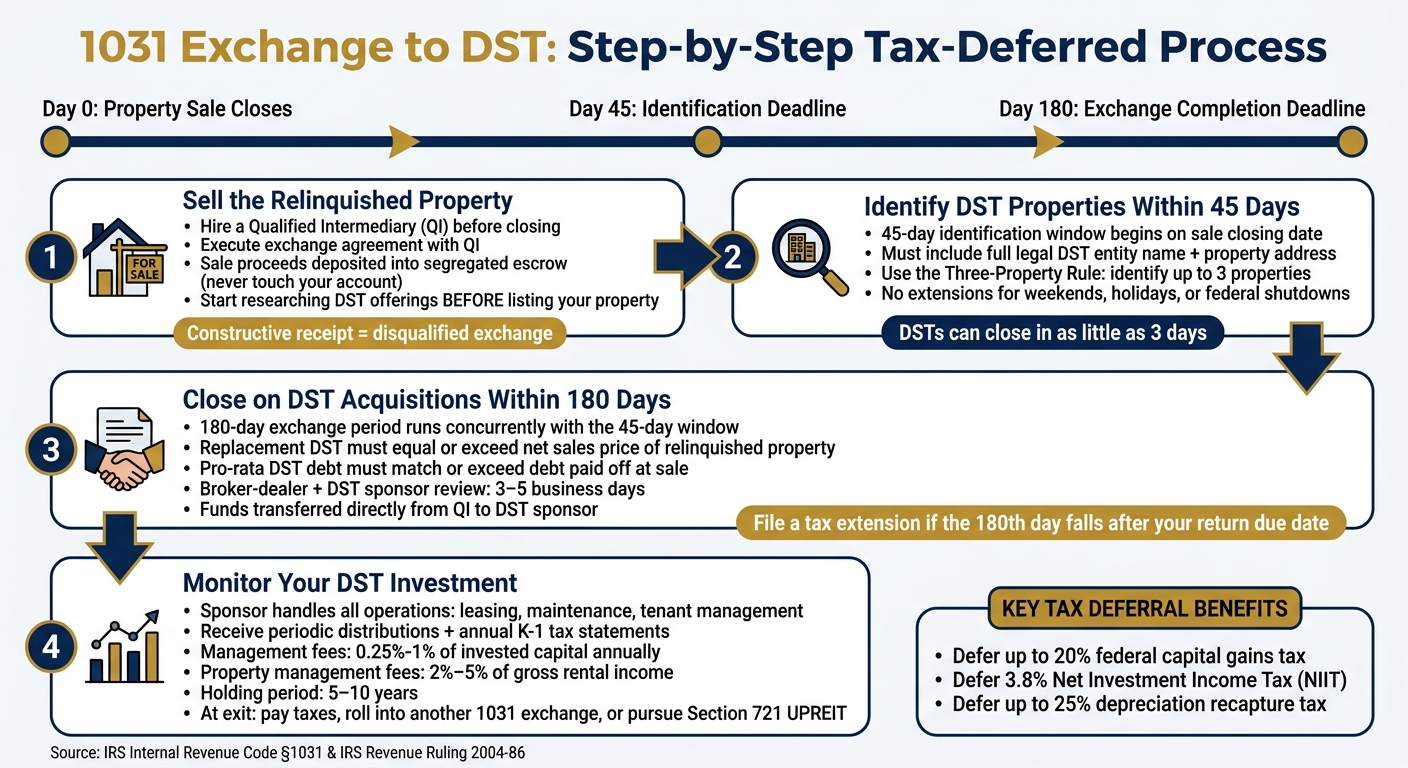

1031 Exchange to DST: Step-by-Step Tax-Deferred Process

Navigating a 1031 exchange into a Delaware Statutory Trust (DST) requires precision and adherence to strict timelines. Missing even one step can jeopardize the tax-deferred benefits. Here’s how the process unfolds:

The first step is to hire a Qualified Intermediary (QI) to handle the transaction. Before closing the sale, execute an exchange agreement with the QI to ensure the sale proceeds are deposited directly into a segregated escrow account. This step is crucial to avoid "constructive receipt", which would disqualify the tax deferral[1].

"The DST exchange timeline is rigid by design. The only flexibility is before it starts." - Wealthstone Group[10]

Start researching DST offerings early - ideally before listing your property. Once the title transfers, the 45-day identification period begins, and available DST options can change quickly. With the sale process handled by your QI, you can focus on identifying replacement properties that meet DST criteria.

After selling your property, the next step is to identify eligible DST replacement properties. This must be completed within 45 days of the sale, and the identification must include the full legal name of the DST entity and the property address. Keep in mind, this deadline is firm - weekends, holidays, or federal shutdowns don’t grant any extensions[1].

Most investors use the Three-Property Rule, which allows you to identify up to three potential properties regardless of their value[1].

"DSTs can close as quickly as three days after your intermediary receives funds from your sale." - Thomas Wall, Partner, Anchor1031[1]

This quick closing is one reason DSTs are often used as backup options. Once your DST properties are identified, the focus shifts to closing the acquisition within the 180-day timeline.

The 180-day exchange period begins on the same day your property is sold, running concurrently with the 45-day identification window[1]. To secure full tax deferral, the replacement DST must meet two key conditions:

After submitting your choice, the broker-dealer and DST sponsor typically complete their review in 3–5 business days[9]. Here’s a quick summary of the critical requirements:

| Criteria | Details |

|---|---|

| 180-Day Deadline | The earlier of 180 calendar days post-sale or your tax return due date (including extensions)[1] |

| Value Requirement | The replacement DST must equal or exceed the net sales price of the relinquished property[1] |

| Debt Requirement | Your pro-rata DST debt must match or exceed the debt paid off at sale[1] |

| Fund Handling | Proceeds are transferred directly from the QI to the DST sponsor; you never handle the cash[9] |

If the 180th day falls after your tax return due date, filing for an extension is necessary to maximize the exchange period[1]. Once the acquisition is complete, your focus shifts to monitoring your DST investment.

After closing, your involvement becomes minimal. The DST sponsor takes on all operational responsibilities, including leasing, maintenance, and tenant management. Your role is to monitor the investment, which typically involves receiving periodic distributions and annual K-1 tax statements.

Management fees generally range from 0.25% to 1% of your invested capital annually, while property management fees add another 2% to 5% of gross rental income[1]. Most DSTs have a holding period of 5 to 10 years, after which the sponsor sells the property. At that point, you can either pay taxes on the gains or roll the proceeds into another 1031 exchange to continue deferring taxes.

DST investments come with appealing benefits, but they also involve trade-offs that investors must carefully evaluate before committing funds.

While the tax advantages and operational simplicity of DSTs are attractive, the associated fees can significantly impact returns. Upfront costs typically range from 7% to 15%, broken down as follows:

Additionally, sponsors often charge a disposition fee when the property is sold, as they are prohibited from taking promote or waterfall profit splits. The minimum investment required usually falls between $25,000 and $100,000 for 1031 exchange investors.

"In a 1031 Exchange, the proceeds from the sale of one real estate investment can be used to purchase a like-kind investment... if investors are not careful, fees can eat into those benefits." - Paul Getty, President and CEO, FGG1031

It's crucial to review the Private Placement Memorandum (PPM) thoroughly to understand the fee structure before making a decision.

One of the biggest challenges with DSTs is their lack of liquidity. Exiting early is difficult because there’s no active secondary market for DST interests. While selling to another accredited investor is possible, finding a buyer can be tough, and such sales often require accepting a steep discount - anywhere from 20% to 50% off the book value.

"DST interests are illiquid; secondary market sales are rare and typically require 20–50% discounts to book value." - Thomas Wall, Partner, Anchor1031

Market risks also pose challenges. Interest rate fluctuations, economic downturns, and tenant credit issues can all affect a DST’s performance. Furthermore, IRS Revenue Ruling 2004-86 restricts DST sponsors from raising new capital, refinancing debt, or reinvesting sale proceeds. This limits their ability to respond to adverse market conditions. Investors who may need access to their funds within 5 to 10 years should carefully consider these risks. Choosing between a DST, direct property ownership, or an outright sale requires a thoughtful approach.

Each exit strategy comes with its own set of advantages and limitations regarding taxes, management responsibilities, liquidity, control, and fees. Here's a breakdown of the key differences:

| Feature | 1031 DST Investment | Direct Property Ownership | Outright Sale |

|---|---|---|---|

| Tax Treatment | Deferred via 1031 exchange | Deferred via 1031 exchange | Immediate capital gains tax |

| Management | 100% passive | Active and hands-on | None (asset is sold) |

| Liquidity | Very low (typically a 5–10 year hold) | Moderate (market dependent) | High (immediate cash access) |

| Control | None; sponsor makes all decisions | Full control over decisions | N/A |

| Fees | High upfront fees (7–15%) | Standard closing costs | Brokerage commissions only |

The most suitable option depends on your financial goals. If you prioritize passive income and long-term tax deferral, and you’re comfortable locking up your capital for several years, a DST could work well. On the other hand, if maintaining control or having the flexibility to sell on your own timeline is more important, direct property ownership may be a better fit. For those who need immediate liquidity, an outright sale provides quick access to cash but comes with an immediate tax obligation. Carefully assessing these factors ensures that a DST aligns with your broader investment strategy.

A 1031 exchange into a Delaware Statutory Trust (DST) offers investors a way to defer taxes, shift away from active property management, and maintain their equity. Thanks to IRS Revenue Ruling 2004-86, DST interests qualify as like-kind replacement properties. This means investors can enjoy the full tax deferral benefits of a traditional 1031 exchange without facing immediate capital gains taxes or depreciation recapture. It’s a combination of tax advantages and passive investment opportunities that can open up new possibilities.

One of the most appealing aspects of this strategy is the potential for ongoing tax deferral through sequential exchanges. By continuing the process, taxes can be deferred indefinitely. And when the investor passes away, their heirs often receive a step-up in basis, which may effectively erase decades of deferred gains.

DSTs also simplify the often-complicated exchange process. They help investors navigate the strict 45-day identification deadline, which is a hurdle in nearly 30% of traditional 1031 exchanges [2]. Since DSTs are pre-structured and stabilized, transactions can be completed in as little as three to five business days - much faster than the 60–90 days typically needed for a direct property purchase.

However, it’s important to consider the trade-offs. DSTs come with higher fees, limited liquidity, and less control over the investment. As Mike Bonaventure, Chief Growth Officer at Bonaventure, wisely noted:

"DSTs - like any investment strategy - offer significant benefits alongside notable risks critical for informed investment decisions." [3]

If you own investment property and meet specific requirements, you might qualify to complete a 1031 exchange into a Delaware Statutory Trust (DST). DSTs are considered like-kind property, allowing for tax deferral, and they’re a great option for investors looking for passive management. That said, DSTs are generally illiquid and are usually available only to accredited investors. Be sure to consult a qualified professional to determine if you meet the eligibility criteria.

To steer clear of taxable "boot" in a 1031 exchange when investing in Delaware Statutory Trust (DST) interests, it's crucial to reinvest all sale proceeds into like-kind property of equal or greater value. Additionally, the debt on your new investment must match or exceed the debt on the property you sold.

Timing is everything here. The IRS has strict deadlines you must follow:

Careful planning and working with a qualified intermediary can make all the difference, ensuring you comply with IRS rules and achieve full tax deferral.

When a DST is sold, the proceeds typically face capital gains taxes unless they are reinvested to maintain a tax-deferred status. To achieve this, you can reinvest into a like-kind property using a 1031 exchange. This process requires meeting specific deadlines: you have 45 days to identify a replacement property and 180 days to complete the transaction. By adhering to these rules, you can defer taxes by moving into another qualifying property or DST investment. However, if the deadlines are missed, the gains become taxable.