Published on

May 12, 2026

When entering a partnership, planning how to exit is just as important as starting strong. Exit strategies help prevent disputes, financial losses, and operational challenges when a partnership ends. Common reasons for exiting include misaligned goals, market changes, or liquidity needs. Without a clear plan, businesses risk costly legal battles and diminished value.

Key strategies include:

To succeed, focus on clear financial records, defined exit clauses, and operational independence. Advisory services, like M&A experts or fractional CFOs, can simplify the process and boost outcomes. The right strategy depends on your goals, timeline, and the partnership’s health.

Exit strategies depend on various factors, including the goals of the partners, the nature of their relationship, and the overall health of the business. Here's a closer look at some of the most common approaches and what they entail.

An acquisition buyout happens when one partner buys out the other’s stake to take full control of the business. This is often the preferred route because it maintains the business as a functioning entity, potentially delivering a valuation 3–7 times higher than liquidation. As M&A attorney Alex Lubyansky explains:

"The financial math is unambiguous: a business is worth dramatically more as a going concern than as a pile of assets being sold to the highest bidder." [6]

Agreeing on a fair price is crucial. Common valuation methods include Discounted Cash Flow (DCF) analysis, EBITDA multiples (typically 2–5x for growth-stage companies), and independent appraisals [4][9]. Payments can take different forms: a lump sum (used in about 20% of cases), installments spread over 3–7 years, or earnouts tied to future revenue or EBITDA [4]. If installments are involved, securing a personal guarantee can help protect your interests.

If a structured buyout isn’t workable, partners may need to consider dissolving the business entirely.

Dissolution is often the last resort. In this scenario, the business shuts down, assets are sold, creditors are paid, and any remaining funds are divided among the partners. Financially, this is usually the least favorable option. It eliminates goodwill, damages customer relationships, and erases brand equity [6]. Assets sold during dissolution often fetch below-market prices, making this approach viable only when partners are deadlocked and no buyout solution is possible.

Dividing jointly developed intellectual property can also become a major sticking point. Without pre-established rules in the operating agreement, IP disputes can drag on long after the business has been dissolved [7][8].

A secondary sale allows a partner to exit by selling their stake to an outside investor, avoiding the need for a full acquisition or shutdown. Many partnership agreements include clauses like Right of First Refusal (ROFR) or Right of First Offer (ROFO). ROFR lets existing partners match any external offer, which can discourage potential buyers. ROFO, on the other hand, requires the selling partner to offer their stake internally before seeking external buyers [2].

Private equity or strategic buyers often scrutinize partnership agreements and cap tables closely. Unusual redemption rights or payment structures can complicate or even derail deals [9]. If selling to a third party isn’t practical, merging with a larger organization might be a better alternative.

Selling the partnership to a larger organization can sometimes be the simplest option. Strategic buyers, such as competitors, may pay a premium for access to market share, technology, or talent they can’t easily develop on their own. Before beginning merger discussions, it’s essential to normalize EBITDA by ensuring owner compensation reflects market rates. Buyers often flag non-standard arrangements - like family members on the payroll with inflated salaries - during due diligence, which can lead to price reductions [9].

Tag-along and drag-along rights also influence how mergers unfold. These rights are discussed further in the Legal and Risk Factors section [2].

A management buyout (MBO) is an exit option that keeps the business within the internal leadership team. In this scenario, the management team purchases one or more partner’s stakes. MBOs provide continuity, as the internal team already understands the business. However, financing can be a challenge, often requiring seller-financed installment payments [4].

For an MBO to succeed, the business must have scalable, well-documented systems in place. This reassures buyers that the company can operate smoothly without the departing partner. Additionally, this approach aligns incentives, as the seller has a vested interest in ensuring the transition goes well while the buyers avoid overburdening themselves with debt.

The success of any partnership exit often hinges on meticulous preparation. Whether you're selling your stake, bringing in new partners, or planning a buyout, every detail matters. Buyers and incoming partners will examine your business with a fine-tooth comb, and any gaps in your operations or records can lead to costly setbacks. As Alex Lubyansky, Esq. aptly states:

"The transition is where most buyouts succeed or fail." [4]

Clear and accurate financial records are non-negotiable when preparing for an exit. Buyers and investors need to trust the numbers you provide. Issues like inconsistent bookkeeping, undocumented related-party transactions, or irregular revenue recognition can quickly raise red flags and jeopardize the deal.

Start by conducting an intellectual property (IP) audit to confirm that all IP assets are owned by the business entity, not by individual partners [4]. Also, establish consistent normalization rules to properly account for one-time or non-recurring items [2].

If installment payments are part of the exit plan, keep a close eye on cash reserves and debt ratios to safeguard your financial interests throughout the process [4].

Performance metrics play a critical role in demonstrating your business's value. Buyers don't just want to see revenue figures - they want to understand the quality of that revenue. For growth-focused companies, metrics like Monthly Recurring Revenue (MRR), churn rate, and Net Revenue Retention (NRR) provide insight into long-term growth potential and risks.

Define these metrics clearly and calculate them consistently from the start. Discrepancies or unclear definitions can lead to disputes and erode trust during negotiations [2][4].

Operational independence can greatly enhance your negotiating position during an exit. A business that relies heavily on external systems, parent companies, or individual partners becomes a liability. Buyers want a self-sufficient operation, not a web of dependencies that will require costly adjustments post-sale.

"If the JV depends on parent systems, parent licenses, or parent-held customer contracts, exit becomes operationally expensive. That cost changes negotiating leverage later." - Umbrex [2]

To prepare, create an independence roadmap early in the partnership. Identify all critical dependencies - whether it's shared systems, permits, personnel, or customer contracts - and plan for their eventual separation. Make sure licenses and contracts are held directly by the business, not by a parent company or individual stakeholders.

If immediate separation isn't practical, a Transition Services Agreement (TSA) can temporarily bridge the gap. However, TSAs should be time-limited, priced transparently, and include clear steps for a clean exit.

Additionally, plan for a 30–90 day transition period to handle customer handoffs. This ensures revenue continuity and helps maintain the business's valuation [4].

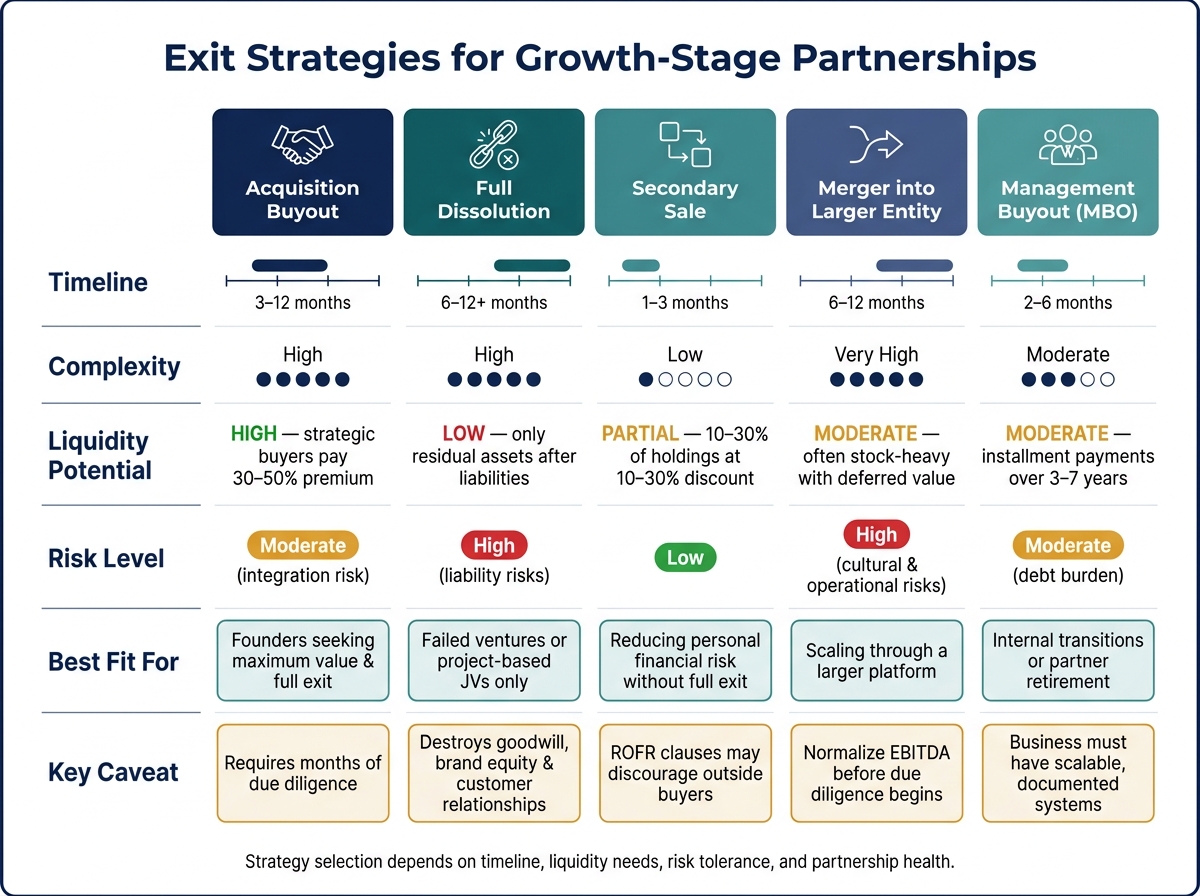

Exit Strategies for Growth-Stage Partnerships: Side-by-Side Comparison

No single exit strategy fits every partnership. The best choice depends on factors like your timeline, liquidity needs, risk tolerance, and the future direction of the business. By understanding the trade-offs of each option, you can make smarter decisions before emotions or market conditions force your hand.

Here’s a breakdown of five common exit strategies, evaluated on key factors that matter to growth-stage companies:

| Strategy | Timeline | Complexity | Liquidity Potential | Risk Level | Fit for Growth-Stage |

|---|---|---|---|---|---|

| Acquisition Buyout | 3–12 months | High | High - strategic buyers often pay a 30–50% premium [10] | Moderate (integration risk) | Ideal for founders seeking maximum value and a full exit |

| Full Dissolution | 6–12+ months | High | Low - only residual assets remain after liabilities are paid [2] | High (liability risks) | Suitable only for failed ventures or project-based JVs |

| Secondary Sale | 1–3 months | Low | Partial - typically 10–30% of holdings, often at a 10–30% discount to the last valuation [10] | Low | Useful for reducing personal financial risk without fully exiting |

| Merger into Larger Entity | 6–12 months | Very High | Moderate - often stock-heavy with deferred value [10] | High (cultural and operational risks) | Effective for scaling through a larger platform |

| Management Buyout (MBO) | 2–6 months | Moderate | Moderate - typically structured as installment payments over 3–7 years [4] | Moderate (debt burden) | Best for internal transitions or when a partner retires |

Some patterns stand out. Acquisition buyouts provide the highest immediate liquidity but require significant preparation, including months of due diligence and negotiations. On the other hand, secondary sales are quicker and less disruptive operationally but typically involve a discount and only allow partial liquidity. Full dissolution is rarely ideal for a viable business, as it often results in a loss of value rather than a gain [7][2].

For growth-stage companies, mergers can offer an opportunity to scale rapidly by leveraging a larger platform, but they come with high complexity and cultural risks. MBOs are a good option when management is capable, and the departing partner wants a smooth, relationship-friendly exit. However, liquidity in an MBO comes gradually due to installment-based payments.

The most important takeaway? Align the strategy with your actual situation, not just what looks good on paper. For instance, if you’re planning for a future private equity round, avoid options that complicate your cap table, like those involving ongoing royalty payments or complex redemption terms [9]. If you need liquidity now but aren’t ready to exit entirely, a secondary sale offers breathing room without severing ties.

This comparative framework helps lay the groundwork for understanding the legal and operational risks that will further shape your decision.

When planning a partnership exit, solid legal groundwork is just as important as selecting the right strategy. A well-prepared legal framework not only strengthens your negotiating power but also protects your interests throughout the process. Weak or poorly defined exit clauses can lead to disputes, litigation, and reduced exit values - especially for fast-growing companies. These legal safeguards also help address risks tied to market timing and operational dependencies.

Before initiating an exit, review your partnership agreement for key exit provisions. Common clauses include:

Research from Ankura shows that 60% of joint venture agreements include at-will exit rights. However, 98% of those agreements also impose restrictions, such as a Right of First Refusal (ROFR) or Right of First Offer (ROFO), to control sales to third parties [5].

Clear valuation methods - whether through independent appraisals, EBITDA multiples, or arbitration - are critical to avoiding price disputes that could derail your exit.

"Poorly structured exit provisions can also exacerbate partner animosity, trigger litigation, cause reputational damage, spawn high legal fees, and negatively impact exit prices." - Tracy Branding Pyle, Edgar Elliott, and James Bamford, Ankura [5]

Non-compete and non-solicitation clauses should be carefully defined in terms of geography, duration, and scope to ensure they hold up in court [4]. Additionally, if a departing partner has personal guarantees on loans or leases, those obligations don’t automatically end with their exit. Creditors must formally release or substitute the guarantees to avoid future complications [12].

Legal planning doesn’t stop at contracts - timing and market conditions also play a pivotal role in determining the success of an exit.

Exiting at the wrong time can be a costly mistake. For instance, the Goodyear and Sumitomo global tire alliance included a performance trigger: if the venture failed to capture at least 6% of the Japanese market, either partner could initiate an exit [5]. These kinds of milestones help reduce uncertainty and align expectations.

For companies without built-in triggers, it’s crucial to analyze factors like current market valuation multiples, revenue trends over the past 12 months, and any change-of-control provisions in debt agreements that might be triggered by an exit. The Revised Uniform Partnership Act (RUPA) allows for buyouts that preserve the business rather than forcing dissolution - provided the agreement is structured to support this [11]. Knowing which legal framework governs your partnership is essential to navigating these complexities.

Operational dependency is another significant legal risk during an exit. If your partner handles critical functions - such as IT, finance, or vendor relationships - their departure could leave major gaps, sparking disputes over responsibilities and liabilities.

To mitigate this risk, preparation is key. Inadequate documentation of processes, a lack of Transition Service Agreements (TSAs), or unclear role redistribution can lead to delays, legal conflicts, and reduced exit values [5]. Addressing these issues early ensures smoother transitions and complements the financial and operational preparations outlined earlier in this guide. Together, these steps create a solid foundation for a successful exit.

Navigating a partnership exit can be challenging, even with a solid strategy in place. The process often involves financial modeling, legal coordination, and operational restructuring - all of which can overwhelm growth-stage companies. Advisory services step in to simplify these complexities, helping businesses manage the transition effectively.

Valuation disagreements are one of the most common roadblocks in partnership exits. Advisors help avoid these conflicts by creating objective valuation frameworks. Whether through independent appraisals or revenue-based formulas, these frameworks establish a clear foundation for negotiations before they even begin [1].

Financial modeling is another critical element of a successful exit. Tools like cash flow forecasting and Integrated Financial Models, offered by firms like Phoenix Strategy Group, provide leadership with a clear understanding of the company’s financial health after the transition. This insight is essential for structuring funding mechanisms that allow remaining partners to sustain operations post-exit [1].

"Legal counsel for partnerships and joint ventures help secure optimal profits within a protective legal framework." - Neufeld Legal [1]

In addition to valuation and modeling, fractional CFO services can ensure financial clarity throughout the process.

For many growth-stage companies, hiring a full-time CFO during an exit isn't feasible. A fractional CFO can fill this gap, offering high-level financial expertise without the full-time commitment. Services like those from Phoenix Strategy Group provide critical support, helping companies monitor key performance indicators, develop accurate forecasts, and make informed decisions under tight timelines.

A crucial part of exit planning is demonstrating operational independence. Advisors focus on building what the Exit Planning Institute refers to as Structural Capital - the systems, processes, and documentation that enable a business to operate efficiently without daily involvement from partners [3]. This not only boosts market value but also makes the company more appealing to potential buyers or new partners.

"The Four Cs are the Levers you can use to significantly increase the value of your Business. They are Human Capital, Structural Capital, Customer Capital, and Social Capital." - Exit Planning Institute [3]

Strong cash flow, detailed processes, and clean financial records go beyond operational efficiency - they become key assets during an exit. Companies that invest in these areas early, with the guidance of advisory services, position themselves for smoother transitions and better outcomes aligned with their strategic goals.

When it comes to exit strategies, there’s no one-size-fits-all solution. Each growth-stage partnership comes with its own financial, operational, and strategic nuances, making it crucial to craft a plan that fits your specific circumstances. The ideal strategy depends on your current financial standing, the dynamics with your partners, and your long-term vision after the exit.

A successful exit starts with early and thorough preparation. This includes defining clear exit triggers, agreeing on valuation methods, and ensuring operational independence. Think of your exit plan as similar to a financial model - something to develop early, revisit regularly, and refine as needed.

Partnering with seasoned advisors can make a world of difference. For instance, Phoenix Strategy Group provides specialized services like M&A advisory, fractional CFO support, and FP&A assistance. Their expertise helps simplify the process, minimize risks, and ensure you're well-prepared for the complexities of a transition.

Ultimately, the goal isn’t just to exit - it’s to exit successfully. This means preserving value, maintaining important relationships when possible, and setting your business up for future opportunities. By combining a thoughtful strategy, diligent preparation, and expert support, growth-stage partnerships can navigate exits with confidence and achieve positive outcomes.

The right exit strategy hinges on your partnership’s setup, objectives, and unique situation. Some common options include partner buyouts, which allow for a smooth transfer of ownership, or pre-planned exits that work well for joint ventures with a clear timeline. Adjusting equity splits or restructuring ownership are also ways to position a partnership for future opportunities. It's wise to work with legal and financial advisors to customize a plan that fits your circumstances.

Determining a fair buyout price starts with a well-defined valuation process that takes into account the company’s overall value, individual contributions, associated risks, and its future prospects. To achieve this, businesses often rely on one of three common valuation methods:

Equally important is ensuring transparency through proper documentation. This includes detailed valuation reports and clearly outlined terms that all parties agree upon. To make the process smoother, consulting with financial or legal experts can be invaluable. They can help structure the payment - whether as a lump sum or in installments - and negotiate terms that ensure fairness for everyone involved.

Before initiating an exit from a growth-stage partnership, it’s essential to plan carefully right from the beginning. Start by defining your exit strategy early on. This means setting clear governance structures and agreeing on the ultimate goals to prevent conflicts over diverging interests or shared control.

Take a proactive approach by preparing legal, financial, and operational frameworks in advance. This preparation helps you address potential challenges and ensures the transition is smooth, preserves value, and avoids unnecessary delays or emotional roadblocks along the way.