Published on

July 10, 2026

If I had to boil it down to one line: a 338(h)(10) can give the buyer an asset step-up without moving assets one by one, while a direct asset purchase gives the buyer more control over liabilities.

If you're comparing these two deal structures, here's the short answer:

In plain terms: if I were a buyer, I’d usually want the tax step-up and the cleanest risk profile I could get. If I were a founder or seller, I’d focus on after-tax cash, not just the headline price.

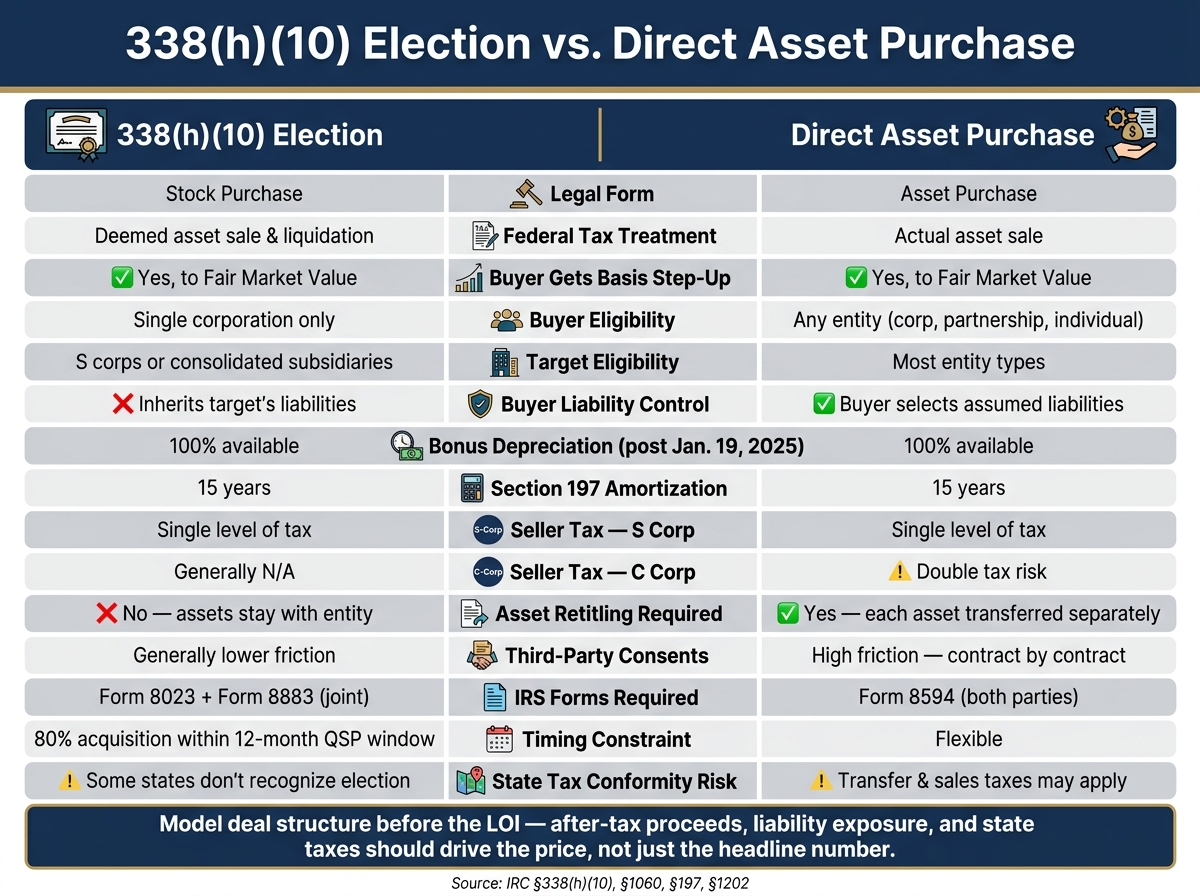

338(h)(10) vs Direct Asset Purchase: Key Tax & Deal Structure Differences

| Factor | 338(h)(10) | Direct Asset Purchase |

|---|---|---|

| Legal form | Stock deal | Asset deal |

| Tax result | Deemed asset sale | Actual asset sale |

| Buyer gets basis step-up | Yes | Yes |

| Buyer can limit liabilities | No, not in the same way | Yes, more control |

| Buyer eligibility | Single corporation only | Broadly open |

| Common target types | S corps, consolidated subs | Most entity types |

| Main friction point | Eligibility and liability carryover | Consents, retitling, assignments |

| IRS forms | 8023 and 8883 | 8594 |

My takeaway: the choice usually comes down to tax deductions, liability carryover, seller tax cost, and closing friction. That’s the lens I’d use before signing an LOI.

With a Section 338(h)(10) election, the buyer keeps the legal form of a stock purchase but gets the tax treatment of an asset sale.

Here’s the basic idea: the buyer acquires the target’s stock. But for federal tax purposes, the target is treated as if it sold its assets at fair market value and then liquidated.

That election is only available in a narrow set of cases. A single corporate buyer must acquire at least 80% of the target’s vote and value within 12 months. The target also has to be either an S corporation or a consolidated subsidiary, and both sides must file IRS Form 8023.

One big catch: even though the tax result looks like an asset sale, the deal is still legally a stock sale. So the buyer takes on the target’s liabilities, including liabilities that may not be known at closing.

A direct asset purchase gets to a similar tax result, but it does so through an actual transfer of assets.

In this structure, the buyer picks the assets it wants to buy and takes on only the liabilities it agrees to assume. That can matter a lot. It gives the buyer more control over risk, instead of inheriting the whole company by default.

The buyer also gets a fair market value basis in the acquired assets. That can increase future depreciation and amortization deductions. The purchase price must be allocated under Section 1060, and both parties report that allocation on IRS Form 8594.

The tradeoff is practical, not just tax-related. Because this is a real asset transfer, titles, contracts, and other items often need to be assigned one by one. That can slow down the closing and make the process more complicated.

This is where the choice can stop being a choice.

A Section 338(h)(10) election comes with hard limits. If the buyer is a partnership, an LLC taxed as a partnership, or an individual, the election is not available.

A direct asset purchase is open to most buyers and most target entity types. It’s also common when the buyer wants to keep liability exposure tighter, since a Section 338(h)(10) election does not fully remove the target’s past liabilities.

| Feature | Section 338(h)(10) Election | Direct Asset Purchase |

|---|---|---|

| Legal Form | Stock purchase | Asset purchase |

| Federal Tax Treatment | Deemed asset sale and liquidation | Actual asset sale |

| Buyer Eligibility | Must be a single corporation | Any entity (corp, partnership, individual) |

| Target Eligibility | S corporations or consolidated subsidiaries | Broadly available to most entity types |

| Basis Step-Up | Yes, to fair market value | Yes, to fair market value |

| Asset Transfer | Automatic via stock transfer | Separate transfers of titles and contracts |

| Election Required | Yes - joint IRS Form 8023 | No special election required |

These mechanics shape who gets the tax upside and who carries the risk. State tax treatment may not match the federal result. And those structural differences can lead to very different tax outcomes for buyers and sellers.

Once the deal structure is locked in, the next issue is pretty simple: who gets the tax upside, and who ends up carrying the risk?

Under both structures, the buyer gets a step-up in asset basis to fair market value. That step-up creates future depreciation and amortization deductions, which is the main tax upside for the buyer.

For most tangible property acquired after January 19, 2025, bonus depreciation is 100%. Section 197 intangibles still amortize over 15 years [1].

The split comes with liabilities. In a direct asset purchase, the buyer can choose which liabilities to assume. In a Section 338(h)(10) deal, the target entity stays in place, so the buyer takes on its liabilities [1].

That difference matters. A buyer may accept more liability exposure in exchange for tax deductions, and that tradeoff can affect the seller's after-tax result.

Seller tax treatment changes a lot based on entity type.

S corporation sellers usually face a single level of tax under either structure [1]. C corporation asset sales can create double tax: once at the corporate level, and again when the proceeds are distributed [1].

That's why the Section 338(h)(10) election is often used for S corporations or consolidated subsidiaries. It can give the buyer a step-up while helping the seller keep single-level tax treatment [1].

QSBS holders need to model this with care. A deemed asset sale can reduce or wipe out the Section 1202 exclusion. The OBBBA also increased the QSBS exclusion cap to the greater of $15 million (indexed after 2026) or 10 times the shareholder's basis [1].

There's another piece sellers can't gloss over: ordinary income recapture. Some assets can trigger recapture taxed at higher rates than long-term capital gains. So the sticker price may look good, but the cash the seller keeps can come in lower than expected.

Federal treatment is only part of the story.

States vary a lot in how they handle federal elections, and some don't recognize a Section 338(h)(10) election at all. So a deal that has one level of tax for federal purposes can still create corporate-level tax at the state level [1].

A direct asset purchase can also bring transfer taxes and sales taxes, depending on the states involved. Franchise taxes and apportionment rules may change how much gain gets taxed and which state gets to tax it. It's smart to model the federal and state hit together before anything gets signed.

These added state-level costs often turn into negotiation points around price and indemnities.

| Tax Factor | Direct Asset Purchase | Section 338(h)(10) Election |

|---|---|---|

| Buyer basis step-up | Yes, to FMV | Yes, to FMV |

| Bonus depreciation (post-Jan. 19, 2025) | Available | Available |

| Section 197 amortization period | 15 years | 15 years |

| Seller tax - S corporation | Single level | Single level |

| Seller tax - C corporation | Double tax risk | Generally N/A (used for S corporations or subsidiaries) |

| Buyer liability exposure | Buyer generally assumes only selected liabilities | Buyer indirectly assumes target liabilities |

| State conformity risk | Transfer and sales taxes may apply | State may not recognize the election |

Buyers push for asset-sale tax treatment for a simple reason: it gives them tax deductions after closing, which can cut taxable income. That tax upside often shapes both the price and the deal terms.

Intangibles usually amortize over 15 years under Section 197, and most tangible property can produce immediate bonus depreciation.

There’s also a risk angle. In a direct asset purchase, the buyer can choose which liabilities to take on and which ones to leave behind. That choice can lower post-close exposure in a very direct way.

Founders often push back on asset-sale treatment because it may lead to a bigger tax bill and can shrink QSBS value. So this usually turns into a price discussion, not just a tax structuring issue.

The usual answer is a price gross-up. The buyer increases the headline purchase price to make up for the seller’s added tax cost. Earnouts and indemnities can also help close the gap, depending on two things: the buyer’s tax shield in the model and the seller’s after-tax proceeds after the gross-up.

Once the economics are locked in, execution becomes the next hurdle.

Asset purchases usually mean retitling every transferred asset and getting third-party consents for contracts. Stock deals often sidestep much of that hassle. In a 338(h)(10) deal, the assets stay inside the entity, so contracts usually do not need to be reassigned. The tradeoff is clear: the buyer takes on the target’s past liabilities.

The filing rules matter too. Asset deals use Form 8594. A 338(h)(10) deal requires Forms 8023 and 8883, and both sides need to use the same allocation. Buyers should also run a Section 382 study on any target NOLs.

A 338(h)(10) deal comes with a hard timing rule as well: the buyer must satisfy the 80% qualified stock purchase test within 12 months.

| Execution Factor | Direct Asset Purchase | Section 338(h)(10) Election |

|---|---|---|

| Third-party consents | High friction; contract-by-contract | Generally lower; stock transfers usually avoid most assignment consents |

| Asset retitling | Required for all transferred assets | Not required; assets stay with the entity |

| Historical liability exposure | Buyer generally avoids | Buyer inherits target's liabilities |

| IRS filing | Form 8594 (both parties) | Form 8023 + Form 8883 (joint election) |

| Buyer eligibility | Any entity or individual | Must be a single corporation |

| Timing constraint | Flexible | 80% acquisition within 12-month QSP window |

The right structure comes down to a simple tradeoff: tax savings vs. liability protection.

A 338(h)(10) election can give the buyer asset-sale tax treatment while keeping the deal in stock form. That matters when contracts, licenses, or regulatory approvals make a direct asset transfer hard or impractical. A direct asset purchase gives the buyer tighter control over which liabilities it takes on, but it also means each asset and title has to be transferred one by one.

That tradeoff should be weighed against buyer eligibility, liability exposure, and state tax treatment.

Model the deal structure before the LOI so after-tax proceeds, liability exposure, and state taxes are built into the price from the start.

Confirm buyer eligibility early. Model after-tax outcomes before the LOI. And tie the deal structure to the broader exit plan, not just the headline price.

Check whether the target is an S corporation or a U.S. corporate subsidiary of a parent company. The deal also needs to meet the qualified stock purchase test. That means a corporate buyer must acquire at least 80% of the target’s stock within a 12-month period.

This option usually isn’t available when the buyer is an individual or a partnership. And the election has to be made jointly by the buyer and seller.

A stock sale usually leaves the seller with more after-tax cash.

Why? Because it's usually taxed once at the capital gains rate. That helps the seller avoid the double tax that can show up in an asset sale.

An asset sale works differently. It can trigger depreciation recapture, which may be taxed at higher ordinary income rates. And if the seller is a C corporation, the deal can be taxed at both the corporate level and the personal level.

A 338(h)(10) election is an exception worth noting. Even though it changes how the deal is treated for tax purposes, the seller still gets a single layer of tax.

A direct asset purchase often makes more sense when the buyer wants to cherry-pick assets and leave certain liabilities behind. That’s the big draw: the buyer can choose what comes over and what stays with the seller.

By contrast, a 338(h)(10) is legally a stock sale. So even though it can get asset-sale tax treatment, the buyer still steps into the company and, in practice, takes on all existing liabilities.

A direct asset purchase is also required when the buyer is an individual or a partnership. A 338(h)(10) is only available to corporate buyers, so those buyers don’t get that option.

If the target has valuable NOLs, a stock purchase is usually the better path than either a direct asset purchase or a 338(h)(10).