Published on

July 10, 2026

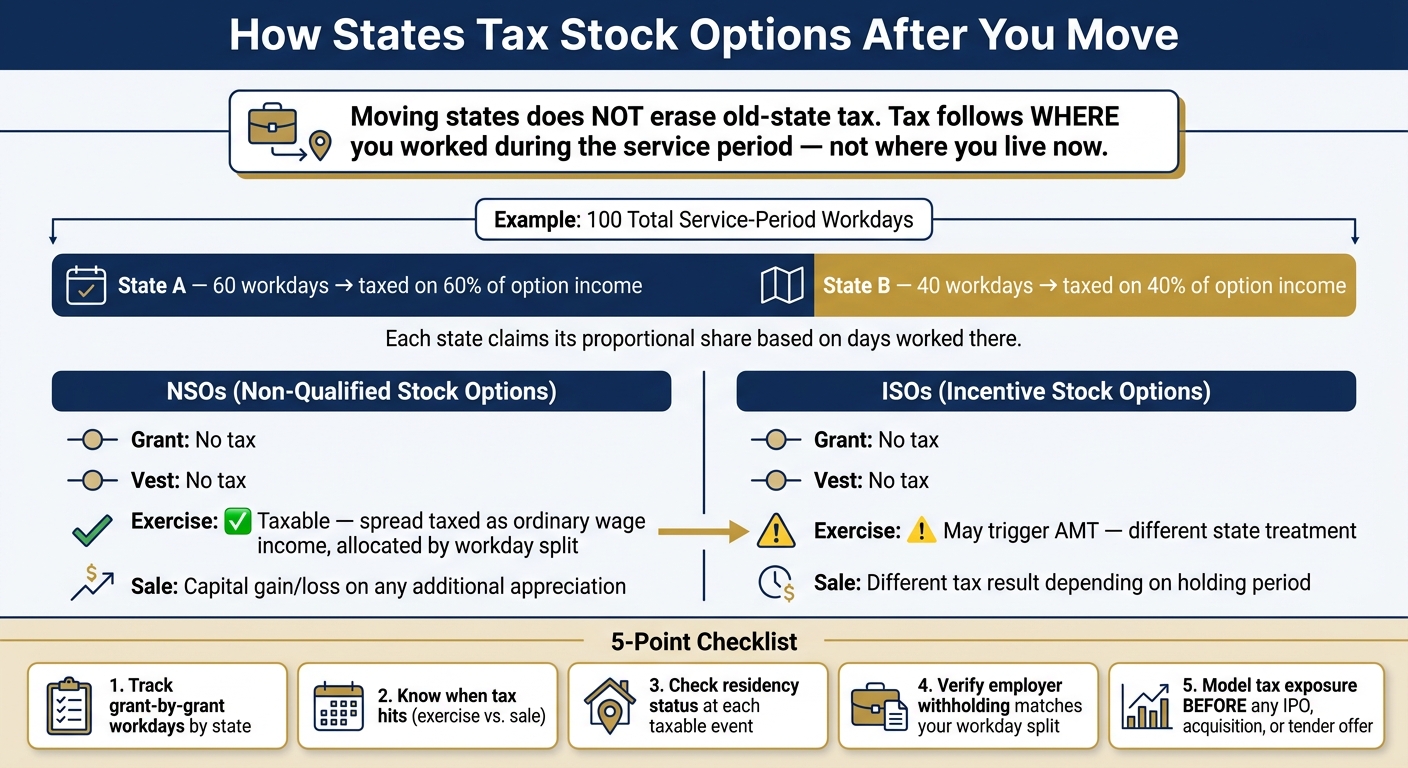

Moving to a new state does not erase tax tied to stock options you earned in your old state. In many cases, I need to look at where I worked during the service period, not just where I live when I exercise or sell.

Here’s the short version:

A simple way to think about it: if I earned an option over 100 workdays, and 60 days were in one state and 40 in another, those states may each claim 60% / 40% of the income tied to that award.

| What matters | Why it matters |

|---|---|

| Where I worked | Often controls which state can tax the option income |

| When tax hits | NSOs and ISOs can be taxed at different points |

| My residency at the time | My new state may tax income while I live there |

| Employer withholding | May not match the split I need on my returns |

| Grant-by-grant records | Help me allocate income and back up the filing |

Bottom line: I can’t judge state tax on stock options by my current address alone. I need to track grant, vesting period, exercise, sale, and state-by-state workdays before any liquidity event or big transaction.

How Stock Options Are Taxed After Moving States

A move doesn't change the basic sourcing rule: states tax option income based on where you worked during the service period. After you move, your old state and your new state may each tax part of that income, either as resident income or nonresident income. That's why workday records matter so much. They're the main input for allocating the income.

Keep a grant-by-grant record of service-period workdays by state. That split drives how much option income each state can tax.

In practice, you'll use those records to divide the option spread between your resident and nonresident state returns after the move. Once you have the workday split, the next step is figuring out when tax is triggered for NSOs and ISOs.

After you move, timing still matters. But in many cases, the state where you earned the equity matters more than where you live now.

NSOs are usually not taxed at grant or vest. State tax usually shows up when you exercise.

At exercise, the spread - fair market value minus your strike price - is treated as ordinary wage income. That spread is then allocated based on service-period workdays in each state.

ISOs don’t work the same way.

ISOs can trigger AMT at exercise, and the tax result at sale can look very different from NSOs. Because of that, state tax treatment can also split off from the NSO path.

The tax treatment at sale is separate from the tax result at exercise. When you sell, split the amount already taxed as compensation from any later gain.

So if you sell after moving, the sale itself may be taxed one way, while the spread taxed at exercise may still follow a different state rule.

After you’ve assigned workdays by state, use that split to check your withholding.

Your employer’s state withholding should line up with your workday allocation. If it doesn’t, that’s a red flag. And it’s much easier to catch that before you file than after.

Here’s the basic idea:

That side-by-side check helps you spot mismatches early.

If you're heading toward an acquisition, tender offer, or IPO, model your state tax exposure now, not after the deal closes. Use the workday split from the earlier sections to run the numbers before anything is final. An exit that happens later doesn't wipe out the state where the award was earned.

Once you have the state workday split, use it before you exercise or sell. Go grant by grant. Estimate the income each exercise creates, then estimate the cash you'll need for withholding and any estimated tax payments. That gives you a working tax estimate before the deal terms are locked in.

If the deal is more involved, bring in tax advisers early and compare a few scenarios before closing. Phoenix Strategy Group can help model cash flow, tax impact, and M&A timing before a transaction.

State tax follows where the grant was earned, not just where you live now. Good records and early modeling help you put a price on that tax before the deal closes.

Yes. States can tax the same stock option income in different ways.

One state may tax it based on where you worked during the grant-to-vesting or grant-to-exercise period. Another may tax it based on your residency when the liquidity event happens.

That’s where things can get messy. If you move, your former state may tax part of the income, and your new state may tax it too. Some states offer tax credits to help offset the overlap, but double taxation can still happen if you don’t plan ahead.

After moving states, keep clear day-by-day records so you can split equity income correctly for state taxes. Many states use a workday ratio to figure out how much tax applies, so you need to track where you worked each day from the grant date through vesting or exercise.

Hold on to records like:

These documents can back up your state tax allocations, help you claim credits if two states tax the same income, and support your position if you’re ever audited.

NSOs are usually taxed as ordinary income when you exercise them. If you move before that happens, states often split that income based on where you worked between the grant date and the exercise date.

ISOs are trickier. Exercising them can trigger AMT, and the tax treatment at sale can vary from state to state. After a move, careful workday tracking matters because you may still have trailing state tax duties or even face possible double taxation.