Published on

July 10, 2026

If I need to close U.S. enterprise deals, I usually start with SOC 2. If I need global buyer trust and a formal security program, I look at ISO 27001.

Here’s the short version:

This comes down to one question: what do my buyers want to see right now?

If I sell mainly in the U.S., SOC 2 is often the better first move. If I sell into EU, APAC, or large global firms, ISO 27001 may carry more weight. If I expect both, I can build one control base and map it to both frameworks.

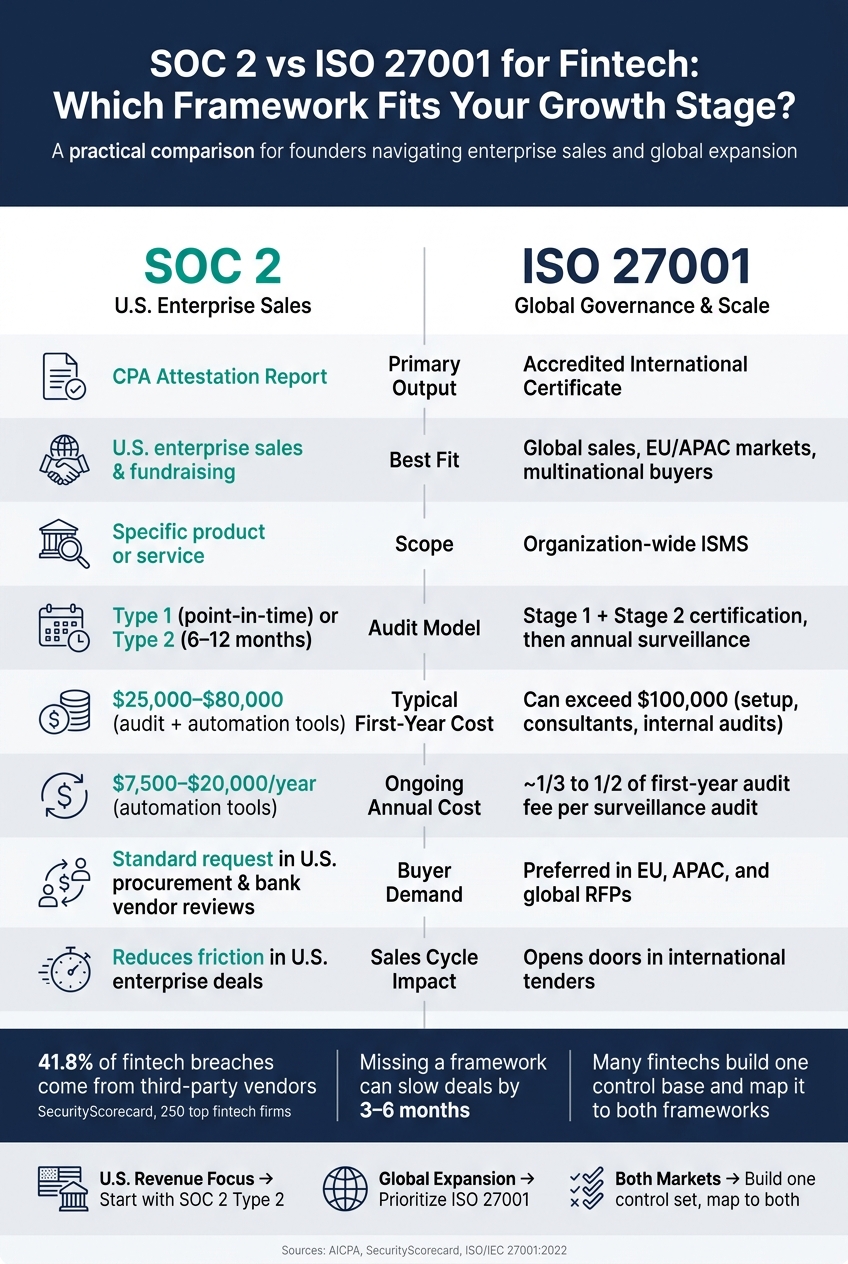

SOC 2 vs ISO 27001 for Fintech: Side-by-Side Comparison

| Criteria | SOC 2 | ISO 27001 |

|---|---|---|

| Main output | CPA attestation report | Accredited certificate |

| Best fit | U.S. enterprise sales | Global sales and governance |

| Scope | Specific product or service | ISMS scope across the company |

| Audit model | Type 1 or Type 2 | Stage 1, Stage 2, then yearly surveillance |

| Buyer focus | Control testing | Security management system |

| Typical first move for U.S. fintechs | Yes | Less often |

| Year-one cost | Usually lower | Usually higher |

So if I want the simple answer: SOC 2 helps with near-term U.S. revenue, ISO 27001 helps with global scale, and many fintechs end up doing both.

Fintech companies deal with transaction records, PII, account credentials, and API-connected systems. That alone puts them under more pressure from banks and enterprise buyers.

The reason is pretty simple: every connected system adds risk.

A SecurityScorecard analysis of 250 top fintech companies found that 41.8% of breaches came from third-party vendors.[14] So when banks and procurement teams review a fintech vendor, they’re not just looking at the company itself. They’re also looking at the risk that comes with its partners, tools, and outside services.

U.S. banking regulators like the OCC, FDIC, and Federal Reserve require banks to manage third-party risk with the same level of care as internal risk.[10][12] In practice, banks pass those demands down to fintech vendors through security questionnaires, contract clauses, and audit rights.[10][12] Enterprise procurement teams often go a step further and ask for a formal security review or an independent audit report before they onboard a new financial technology vendor.

When a fintech goes into an enterprise sales cycle without a formal framework, things can get messy fast. The team often has to build answers in real time, document controls, write policies, and respond to hundreds of procurement questions while the deal is still moving.

That can drag out the sales cycle by three to six months.[6][9]

A SOC 2 Type 2 report or ISO 27001 certificate can change that. Security teams at enterprise buyers see these frameworks as third-party proof that the company has put controls in place, which cuts down on follow-up questions and slows internal approval less often.[7][8]

Instead of debating security terms from scratch in every deal, the fintech can share a standard security package, such as:

That matters beyond sales. Security certifications can also help during fundraising and procurement because they show that the company is ready to move from pilot programs to full-scale enterprise deployments.[11][13] For many U.S.-focused fintechs, SOC 2 is usually the first step.

SOC 2 is an attestation report issued by an independent CPA firm under standards from the American Institute of CPAs (AICPA).[15][19][21] It is not a certification. Instead, it explains your control environment and shows whether those controls are properly designed at a single point in time (Type 1) or working as intended over a review period (Type 2). In the U.S., buyers often ask for it during vendor reviews. And that format matters, because buyers read an attestation report differently from a certification.

SOC 2 is based on five Trust Services Criteria (TSC): security, availability, processing integrity, confidentiality, and privacy.[15][18][21] Of those, security is the only required category. The other four are optional, and you should include them based on how your product works and what customers expect.[18][21][24]

In practice, the big scoping question is simple: Which systems touch customer financial data? That usually means cloud infrastructure, application services, data stores, deployment pipelines, plus access and incident response controls.[17][20] Third-party services are often addressed through a carve-out, with the provider’s own SOC 2 report covering that piece.

For many fintechs, Security, Confidentiality, and Privacy make the most sense.[5][21][24] If your platform promises uptime through SLAs or handles financial calculations that customers use for reporting, Availability and Processing Integrity can make the report far more useful in a buyer review.[15][21][26] After that, the next call is whether you need a point-in-time review or a report that tests controls over time.

The split between Type 1 and Type 2 is mostly about time. A Type 1 report confirms that your controls are properly designed and in place as of a specific date.[16][19] A Type 2 report covers a set review period, usually 6–12 months, and checks whether those controls worked as intended throughout that period.[19][22][2]

| Type 1 | Type 2 | |

|---|---|---|

| What it tests | Control design and implementation at a point in time | Control effectiveness over 6–12 months |

| Best for | Early-stage deals, investor data rooms | Enterprise sales, bank partnerships |

| Audit fees (CPA firm) | $15,000–$40,000 | $25,000–$60,000+ |

| Total first-year cost | Varies widely | $40,000–$80,000 (including internal team time) |

A readiness phase often takes 2–4 months for a mature company.[21][26][27] That work usually includes writing and approving security policies, tightening identity and access management with SSO, MFA, and role-based access, improving logging and monitoring, and running an internal gap review against the TSC. Internal team time from engineering, security, and operations can end up matching the audit fee itself, so founders should plan for both the invoice and the hours it takes to get ready.[20][26][27]

U.S. banks and enterprise procurement teams often ask for a SOC 2 Type 2 report during vendor due diligence.[23][25] They use it to check whether a fintech has a structured control environment, see where system boundaries sit, and judge residual risk in areas like access control, change management, and data protection.[23][27] If the report has few exceptions, it can cut down the flood of custom security questionnaires and help move internal approvals along faster.[23][25][27]

Reports older than 12 months are often treated as stale. So SOC 2 is basically an annual program, not a one-and-done project.[28] For fundraising, a completed Type 1 or a clean Type 2 report gives investors outside confirmation that security risks are being managed in a systematic way, not handled on the fly.[17][20][27] Advisory support can help line up SOC 2 planning with fundraising and enterprise sales timelines. The next call is whether SOC 2 by itself fits your market, or whether ISO 27001 is a better match for a broader buyer base.

If SOC 2 documents controls, ISO 27001 formalizes the system behind them.

ISO/IEC 27001:2022 is the international standard for an Information Security Management System (ISMS).[29][30] For fintechs, that means a risk-based system for people, processes, and IT that follows the Plan-Do-Check-Act model to protect confidentiality, integrity, and availability. For fintech firms dealing with vendor reviews, bank partnerships, and cross-border sales, this gives you a governance layer that buyers in international markets already know and respect.

The first big call is the certification scope: which assets the ISMS covers, including the systems, data, and processes it governs. A tighter scope can lower cost and complexity. A broader one does the opposite.[31]

After scope is set, Clause 6 calls for a formal risk assessment. That means identifying threats and vulnerabilities tied to in-scope assets, then judging their effect on confidentiality, integrity, and availability.[31]

From there, you build a Statement of Applicability (SoA). This document maps which controls apply to your organization and why. The 2022 version of ISO 27001 includes 93 controls across four domains:[30]

For fintechs, the controls that tend to matter most include access management, encryption, data backup, and supplier relationships.

The road to certification usually starts with a gap assessment. Then comes ISMS implementation, followed by two formal audit stages. Stage 1 is a documentation and readiness review. Stage 2 checks whether the ISMS is working in day-to-day practice.[31]

Implementation often takes 3 to 12 months, and first-year costs can range from a few thousand dollars for a small do-it-yourself rollout to more than $100,000 with outside consultants.[31] That’s a wide range, but it reflects how much scope, staffing, and outside help can change the price.

After initial certification, ISO 27001 runs on a three-year cycle. You complete Stage 1 and Stage 2 in year one, then go through surveillance audits in years two and three to keep the certificate active. Those annual surveillance audits usually cost around one-third to one-half of the original first-year audit fee.[31]

| Audit Phase | Timing | Purpose |

|---|---|---|

| Stage 1 Audit | Year 1 | Documentation and readiness review |

| Stage 2 Audit | Year 1 | Formal certification of ISMS effectiveness |

| Surveillance Audits | Years 2 & 3 | Annual check-ups to maintain certification |

ISO 27001 carries weight with multinational enterprise buyers and global partners because it is an international standard.[29][31] For a U.S. fintech moving into other markets, certification shows that security governance is documented and repeatable.

The ISMS structure also helps on the inside. It’s not just a badge for procurement teams. It gives your company a working system for reviewing risk and keeping security tied to daily operations. Because the framework requires organizations to revisit risk assessments at least once a year, or whenever major changes hit business processes, IT systems, or regulations,[31] it helps keep controls lined up with how the business actually runs.

For fintechs that are scaling fast, that matters. New products, new vendors, and new markets can change risk in a hurry. ISO 27001 gives teams a way to keep up without treating security like a one-time project.

That structure makes ISO 27001 useful, but the next question is whether it fits your buyer base better than SOC 2.

Both frameworks help calm buyer and investor concerns. But they do different jobs when you're trying to fundraise or close enterprise deals. The main tradeoffs come down to audit load, buyer trust, and how fast deals move.

SOC 2 is a system-level attestation. A CPA firm checks whether controls for a defined service or platform meet the AICPA Trust Services Criteria. ISO 27001 is a certification that your ISMS meets the standard.

| Dimension | SOC 2 | ISO 27001 |

|---|---|---|

| Primary output | CPA attestation report | Accredited certification |

| Scope boundary | Specific service or platform | Organization-wide ISMS |

| Control model | Flexible and outcome-focused against the Trust Services Criteria | Risk-based; controls are selected and justified through the risk assessment and Statement of Applicability |

| Audit structure | Type 1 is point-in-time; Type 2 covers 6–12 months of operation | Stage 1 and Stage 2 certification, then annual surveillance audits |

| Maintenance cadence | Annual Type 2 cycle is the common enterprise expectation | Annual surveillance audits, with full recertification every 3 years |

This difference matters in practice. SOC 2 is usually tied to the product or service a customer is buying. ISO 27001 looks at the management system around security across the company. Put simply: SOC 2 looks closer at the service, while ISO 27001 looks closer at how the company runs security.

SOC 2 is often cheaper to start with. ISO 27001 tends to cost more in year one because the buildout and certification scope are broader.

| Cost factor | SOC 2 | ISO 27001 |

|---|---|---|

| External audit/cert fees | Lower initial cost | Higher initial cost |

| Annual ongoing costs | Lower ongoing cost | Higher ongoing cost |

| Common buyer request | A current SOC 2 Type 2 report | An ISO 27001 certificate and scope statement |

| Sales friction | Reduces friction in U.S. enterprise and bank procurement | Opens doors in EU, APAC, and global tender processes |

In the U.S., missing a SOC 2 Type 2 report can lead to deeper vendor questionnaires or even knock you out of a competitive bid.[3][32] ISO 27001 often has similar pull in international RFPs and with multinational buyers that use standard vendor risk programs.[4][33]

That’s why the buyer request itself tells you a lot. If your pipeline is heavy with U.S. enterprises, SOC 2 often gets asked for first. If you're dealing with global procurement teams, ISO 27001 can carry more weight.

For fintechs chasing near-term U.S. revenue, SOC 2 is often the faster route to buyer trust. For companies that need formal governance and international standing, ISO 27001 sends a stronger signal. If both matter, the order usually matters too: SOC 2 first to help open U.S. enterprise deals, then ISO 27001 to formalize governance and support global growth.

| Business goal | Better fit | Why |

|---|---|---|

| U.S. enterprise sales | SOC 2 Type 2 | Standard request in U.S. procurement workflows |

| Seed–Series B fundraising | SOC 2 Type 2 | Shows enterprise readiness and helps reduce security objections |

| Global expansion in EU/APAC | ISO 27001 | More recognized internationally and often preferred in non-U.S. tenders |

| Selling to global banks | Both | Large banks may want ISO 27001 for governance and SOC 2 for technical depth |

| Long-term compliance maturity | ISO 27001 | ISMS structure supports continuous improvement and board-level governance |

This overlap is why many fintechs start with one framework, then map the same control base into the other. Once that overlap is clear, the choice becomes pretty practical: which one helps your next stage of growth first, or whether your team has enough bandwidth to build toward both at the same time.

After you compare SOC 2 and ISO 27001, the next step is simple: which one helps revenue move sooner? This isn’t just a security call. It’s a sales call too.

Start with buyer demand and deal timing. If your next target is near-term U.S. enterprise sales, SOC 2 is often the better first move. If your next push is international growth, ISO 27001 tends to fit better.

Before you commit, run a gap analysis and a focused risk assessment on the systems that store or process customer financial data. That gives you a clear view of what’s missing and where the risk sits. From there, use the same core controls as your base and pick the framework that lines up with your next sales cycle.

The goal is straightforward: choose the framework that removes the next sales objection with the least delay. Use SOC 2 when speed matters most. Add ISO 27001 when governance and scale start to matter more. It also helps to finish the audit before major enterprise pilots, bank RFPs, or fundraising diligence. Once that base is set, ISO 27001 can come later as an extension of the same control set, not as a second, separate program.

Once the framework decision is made, timing becomes the next issue. You have to weigh it against runway and deal deadlines. A five-figure audit can be worth it if it helps unlock a much larger enterprise contract. But that only works if the business can absorb the cost without putting pressure on cash.

That’s why compliance is just as much a financial planning issue as it is a security one.

Phoenix Strategy Group can model audit cost against expected revenue, line up timelines with fundraising, and cut down manual evidence work.

When the choice is close, this rule of thumb helps:

If you expect to end up with both, build one control set from the start. That lets you reuse evidence, monitoring, and policies across frameworks instead of doing the same work twice.

In plain terms, SOC 2 asks whether your controls are operating well. ISO 27001 asks whether you have a management system that keeps those controls operating well over time. Prove the controls first, then formalize the system.

For most early-stage U.S. fintech companies, SOC 2 Type I is the best place to start.

It’s widely seen as a must-have for U.S. enterprise B2B sales, and you can usually finish it in one to three months.

From there, you can build out your program without starting from scratch. SOC 2 and ISO 27001 share about 70% of their controls, so a lot of that work carries over.

If Europe or APAC is on your roadmap, put ISO 27001 next in line.

Yes. One control set can support both SOC 2 and ISO 27001 because the two frameworks share about 70% of their security requirements.

A unified compliance taxonomy helps fintech firms cover overlap in areas like access controls, encryption, and incident response. The big win is less duplicate work and less repeated evidence collection.

It depends on the framework and the kind of report you need.

SOC 2 Type I usually takes 1 to 3 months.

SOC 2 Type II often takes 9 to 18 months, which includes a 6- to 12-month review period to check how well controls work over time.

ISO 27001 usually takes 6 to 12 months to put in place. If you achieve ISO 27001 first, it can cut the effort for SOC 2 by 30% to 40%.