Published on

July 10, 2026

If you remember one thing, make it this: full ratchet can crush founder ownership, while weighted average usually softens the hit. In a down round, both terms change how preferred shares convert into common shares. But they do not do it the same way.

Here’s the short version:

So when I look at these clauses, I focus on one question: how much ownership moves if the next round is priced lower?

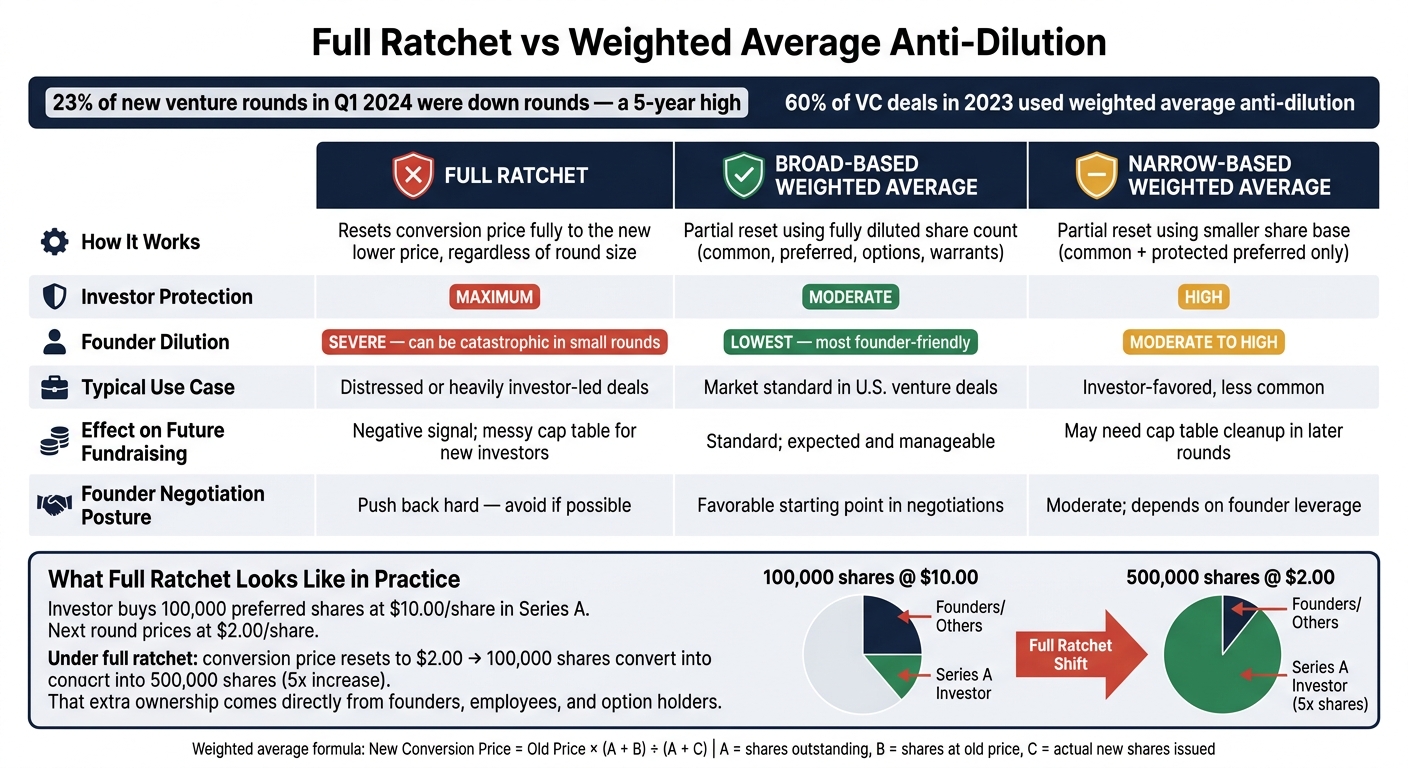

Full Ratchet vs Weighted Average Anti-Dilution: Key Tradeoffs at a Glance

| Term | How it works | Effect on founders | Common use |

|---|---|---|---|

| Full Ratchet | Resets to the new lower price, no matter how small the round is | Harshest dilution | Distressed or investor-led deals |

| Broad-Based Weighted Average | Partial reset using a larger share count | Lightest hit of the three | Common market default |

| Narrow-Based Weighted Average | Partial reset using a smaller share count | More dilution than broad-based | More investor-friendly deals |

A simple example shows the gap fast. If an investor bought at $10.00 per share and the next round prices at $2.00, full ratchet can turn 100,000 shares into 500,000 shares on conversion. That extra ownership comes from founders, employees, and option holders.

Before signing, I’d model:

That turns this from legal wording into plain math. And that’s the part that matters.

Full ratchet is the most aggressive type of anti-dilution protection. It gives investors the most protection because it resets the conversion price to the lowest price paid in a later round, even if the company sells only a small number of shares in that round.

Here’s a simple example. An investor puts in $1,000,000 at $10.00 per share in your Series A and gets 100,000 preferred shares. Later, the company raises a down round at $2.00 per share.

Under full ratchet, that investor’s conversion price resets to $2.00. So on paper, it’s as if they had paid $2.00 per share from the start. Their 100,000 shares now convert into 500,000 shares. That’s a 5x increase in share count.

That extra ownership doesn’t come from thin air. It comes straight out of the ownership held by founders, employees, and option holders. With full ratchet, price is what drives the reset, not round size. That’s why the big thing to watch isn’t just the new price. It’s the formula used to reset the conversion price.

Full ratchet is fairly rare in typical U.S. venture financings. When it shows up, it’s often in distressed situations: a company that’s having trouble raising money, a high-risk bridge round, or a deal where the investor has a lot of leverage and is focused mainly on downside protection.

In plain English, it tends to appear when the investor holds the stronger hand and founder-friendly terms are not the main priority.

Full ratchet can get expensive fast, and the effects can stack up. As the protected investor’s share count grows, founders and employees take the hit.

A few things often happen:

So the risk shift is pretty stark. Full ratchet pushes almost all down-round pain onto common holders. It protects or even increases investor ownership, cuts into founder and employee equity, and can make future rounds messier.

Weighted average goes after the same anti-dilution goal, but it softens the reset by taking round size into account.

Unlike full ratchet, weighted average adjusts the conversion price only part of the way, based on how large the down round is. The formula is: New Conversion Price = Old Conversion Price × (A + B) ÷ (A + C). Here, A is the total shares outstanding before the new round, B is the number of shares that would have been issued at the old price, and C is the actual number of shares issued in the new round.

Put simply: the larger the down round, the larger the reset. But the hit is still lighter than under full ratchet. That usually means less dilution for founders and employees.

The key difference between broad-based and narrow-based weighted average is what counts toward A in the formula.

Broad-based uses the fully diluted share count. That usually includes:

Narrow-based uses a smaller share pool, often just common stock plus the specific preferred series getting the protection.

That one choice changes the math in a big way. Broad-based leads to a smaller reset. Narrow-based leads to a larger one. And that, in turn, changes how much ownership moves in a down round.

Compared with full ratchet, weighted average is a softer approach. It tracks the size of the down round instead of forcing a full reset to the new lower price.

So if the down round is small, the conversion-price change is usually modest. If the round is larger, the reset gets bigger too, but it still tends to be less harsh than full ratchet.

Weighted average showed up in 60% of venture capital deals in 2023 and is the market standard in most U.S. venture deals [2]. Investors still get downside protection, but founders avoid the kind of severe dilution that full ratchet can cause.

| Feature | Broad-Based Weighted Average | Narrow-Based Weighted Average |

|---|---|---|

| Denominator (A) | Fully diluted (Common, Preferred, Options, Warrants) | Common + protected Preferred only |

| Investor Protection | Moderate | High |

| Founder Dilution | Lower; more equity preserved | Higher; more equity transferred |

| Market Prevalence | Industry standard | Less common; more investor-led deals |

| Negotiation Posture | Founder-friendly starting point | Investor-friendly |

In many deals, broad-based is the more founder-friendly place to start in negotiations.

The main difference comes down to how much dilution each formula pushes onto the cap table when a down round happens.

Full ratchet can sharply increase investor ownership even after a small down round. Weighted average works differently. It scales the adjustment based on the size of the round, so the dilution is usually smaller and more in line with what actually happened. That’s why the formula matters just as much as the anti-dilution label at the top of the term sheet.

Down rounds can also lead to option pool top-ups or pre-money pool increases, and founders usually eat that dilution. For example, a $40 million pre-money valuation with a 15% pool increase leaves only about $34 million for existing holders [3].

That math often turns on a few terms that founders can still push on.

Three terms matter most:

The table below shows how these three structures differ in leverage, dilution, and deal pressure.

| Feature | Full Ratchet | Broad-Based Weighted Average | Narrow-Based Weighted Average |

|---|---|---|---|

| How it works | Resets prior preferred shares to the new lower price, no matter how small the round is | Uses a formula with all outstanding shares to calculate a partial reset | Uses the same formula, but with a smaller share base, often preferred shares only |

| Investor Protection | Maximum | Moderate | High |

| Founder Dilution Severity | Severe; can be catastrophic in small rounds | Lowest; most founder-friendly outcome | Moderate to high; more punishing than broad-based |

| Typical Use Case | Distressed or heavily one-sided deals | Market standard | Less common; investor-favored deals |

| Effect on Future Fundraising | Negative signal; can make the cap table hard for new investors | Standard; expected and manageable | May need cleanup in later rounds |

| Founder Leverage | Founders need to push back hard | Low; the usual default in the market | Moderate; depends on founder leverage |

Anti-dilution terms can change post-round ownership in a big way, especially in a down round. By Series B, founders have already given up a meaningful share of ownership [1]. And if you agree to terms before you model them, dilution can climb even more. The key issue is simple: how much does each formula change ownership in a worst-case round?

Use the same assumptions for both formulas so you can see the dilution gap side by side. At a minimum, model these four cases:

In Q1 2024, 23% of all new venture rounds were down rounds - the highest rate in more than five years [1]. That’s not edge-case stuff. It’s worth modeling the downside before you sign.

Once you can compare each case side by side, the negotiation gets a lot more concrete. It stops being a guess and turns into a math problem. Full ratchet gives investors the most protection. Weighted average usually leaves founders with more ownership.

Phoenix Strategy Group can help build dilution models and cap table scenarios before you close.

Founders should usually push back on full ratchet. It can be highly dilutive, and it ignores two big factors: how large the down round is and how many shares the company issues.

If an investor puts it on the table, try to negotiate guardrails like:

That way, you’re not stuck with a term that can hit the cap table much harder than the round itself might suggest.

Carve-outs are exclusions that stop certain share issuances from triggering anti-dilution price adjustments. In plain English, they keep routine moves, like employee stock options or shares tied to a strategic partnership, from setting off investor protections by accident.

They can also cover bridge rounds or other tactical cash infusions, so anti-dilution provisions apply only to major equity events. That gives founders more room to operate and helps protect their ownership stake.

Not always. A weighted average approach is often more balanced and usually less punishing for founders than full ratchet. But the result comes down to the exact formula used.

A broad-based weighted average is usually more founder-friendly because it counts all outstanding equity. A narrow-based version counts fewer shares, which can lead to a bigger price reset and more founder dilution.