Published on

July 13, 2026

Fraud gets more expensive the longer it stays hidden. In the source article, losses found within 6 months had a median cost of $30,000, while cases that lasted 2–3 years reached $250,000.

If I boil the article down, the message is simple:

This is not just a model problem. It is a workflow problem. A company can have alerting in place and still miss fraud if no one owns the queue, reviews alerts on time, or blocks risky changes before money leaves.

Here’s the short version of what the article covers:

The article also makes one point very clear: static limits stop working as a business grows. A fixed dollar rule that worked at $500,000 in revenue may fail at $10,000,000. That is why relative thresholds, case logging, and regular review matter.

If I were summarizing the full framework in one line, it would be this: connect the data, score the risk, and route each alert to the right person fast.

AI fraud detection only works when transaction data is clean and connected.

The core payment dataset AI needs should include transaction ID, timestamp, amount in USD, payee name, bank details, payment method, invoice/PO links, GL/cost center, and the approval trail.

That approval trail matters more than it may seem at first glance. It can show rushed reviews, odd approvers, and activity outside normal business hours. When you connect that trail to the payment itself, you can tie payment fraud to the people involved and the exact timing of each approval.

Vendor bank-detail changes should sit in their own data stream. Each change needs a timestamp, user, role, reason, supporting evidence, and verification status. With that in place, AI can spot high-risk combinations, like a bank-detail change made right before a large payment or multiple unrelated vendors using the same account number. Those are some of the clearest signs of payment diversion fraud.

Device and login signals add another layer of context. If each payment approval is tied to a device ID, IP address, and authentication method, AI can tell the difference between a routine large wire approved by a fractional CFO from their usual office IP with MFA and that same wire approved at 2:00 a.m. from a new device on a foreign IP. The same idea applies to payroll and vendor records, where small updates can point to a much bigger diversion risk.

Refund data needs the same level of discipline. Every alert depends on linking the refund back to the original order and the policy around it.

At the transaction level, AI needs refund ID, original order ID, amount, reason code, channel, agent, overrides, and settlement timestamp.

Standard reason codes are a big deal here. If agents keep falling back to generic labels like other, the model loses signal. AI can then miss patterns such as one call-center team citing shipping delay on orders where carrier scan data shows on-time delivery, or one agent processing refunds at three times the rate of their peers.

AI can also look at refund behavior across rolling 30- and 90-day windows. That helps it catch patterns that seem normal one by one but look abnormal in the aggregate. A cluster of item not received claims from the same device, or refunds pushed through after a policy window closes without proper escalation, are the kinds of cases rule-based checks often miss.

The table below maps each main data source to the fraud signal it can detect and the team that should act on it. That keeps alert routing clear as the business grows.

| Data Source | Fraud Signal Detected | Control Owner |

|---|---|---|

| ERP / AP system | Duplicate invoices, near-duplicate payments, payments just below approval thresholds, missing PO references | Finance / AP |

| Bank portal logs | Off-hours high-value wires, new beneficiary accounts, payments to recently changed bank details | Treasury |

| Vendor master data | Bank account changes before large payments, recently created vendors, shared account numbers across vendors | Finance / AP |

| Payment processor (ACH, card) | Velocity spikes, split payments near approval limits, unusual payment method shifts | Treasury / Finance |

| Identity platform | New device logins, logins from distant locations in too little time, high-risk login activity tied to payment approvals | IT / Finance |

| Order management / CRM | Refunds exceeding original order value, refunds outside policy windows, high refund rates by customer segment | Operations / Finance |

| Customer service tool | Repeated partial refunds by the same agent, inconsistent reason codes, override flags without escalation | Operations |

| Logistics / carrier data | Non-delivery refunds where scan data confirms delivery, shipping refunds on non-delayed orders | Operations |

For this setup to work, IDs need to match across systems. Vendor IDs, customer IDs, invoice IDs, and bank account tokens should carry the same value whether the record sits in ERP, a banking portal, or a payment processor.

Amount formatting needs the same discipline. Dollar values should be stored as decimals with two fixed places, like $12,450.00, while thousand separators should appear only in the display layer. If that base layer is messy, AI models end up joining mismatched keys and sending alerts that fall apart during review.

With payment and refund data in place, finance teams can use the same approach for payroll and vendor activity.

AI Fraud Detection Methods: Rules vs. Anomaly Detection vs. Supervised Models

The same data-first approach works for payroll and vendor workflows too: pull 6–12 months of history before you switch alerts on. That lookback gives you a baseline, which matters a lot. Payroll and vendor flows are often where diversion and payment tampering show up as a company grows, often requiring the oversight of fractional CFO services.

Payroll fraud detection starts with a few core data sources: payroll run files, employee master records, compensation changes, direct-deposit history, time and attendance logs, and manager approval logs. Put those together, and you can spot pay changes that don’t line up with an employee’s normal pattern.

The best alerts don’t rely on a single signal. They look at timing and account relationships at the same time.

Flag issues like:

This is where teams can trip up if they go too broad. A single condition on its own can create noise. It’s usually smarter to combine them. For example, fire an alert only when a large net-pay change and a recent bank-detail edit happen in the same pay cycle, instead of flagging either one by itself. That simple tweak can cut down false positives.

Vendor fraud detection pulls from vendor master records, W-9 and onboarding documentation, ACH change logs, invoice patterns, payment timing, and approval history. From there, score each vendor across onboarding, activity, and change risk.

A common control is to flag bank-detail changes made within seven days of a large scheduled payment. When that happens, require a secondary approval or a callback to a verified vendor contact. That extra step may feel old-school, but it’s often what stops a bad payment from going out.

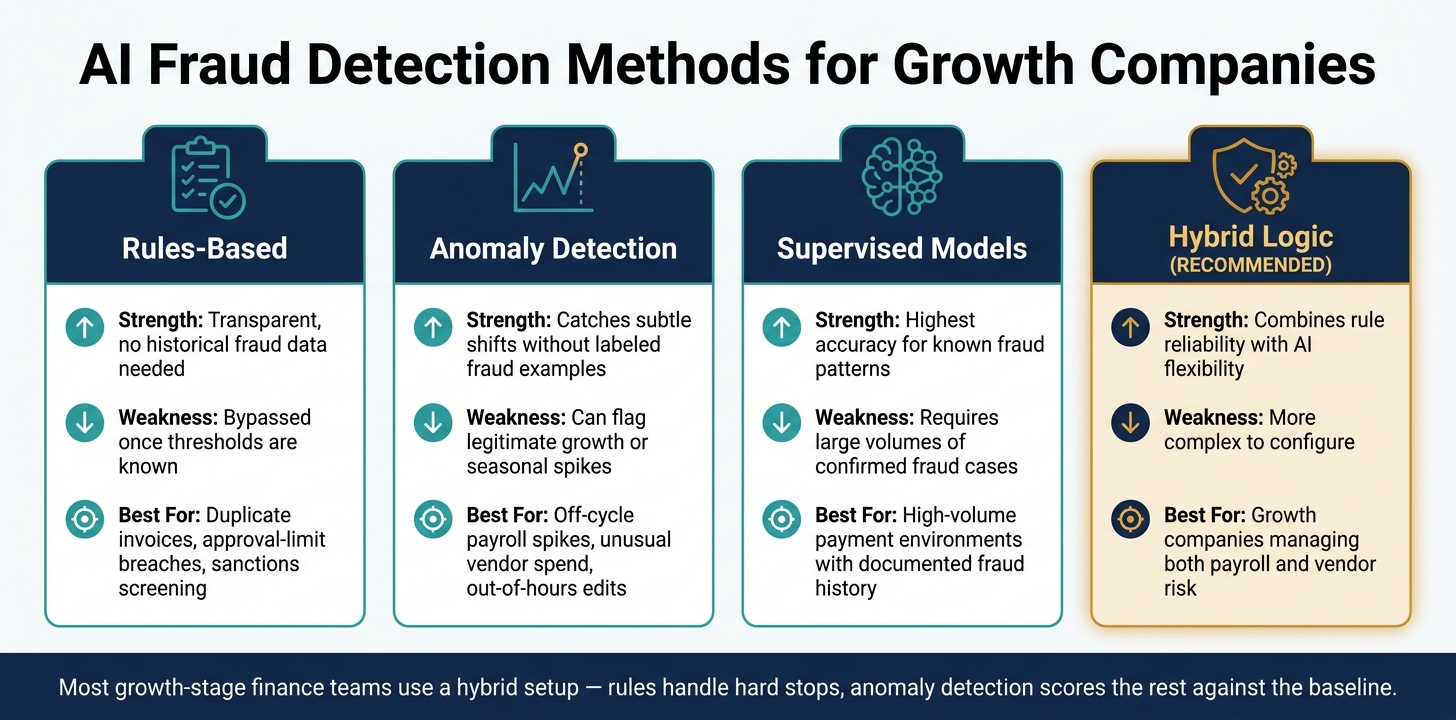

Once you’ve set those alerts, the next call is how to enforce them: with rules, anomaly detection, or a mix of both.

Choose the detection method based on your data quality and how hard the fraud pattern is to spot.

| Method | Strength | Weakness | Best-Fit Use Case |

|---|---|---|---|

| Rules-based | Transparent, no historical fraud data needed | Bypassed once thresholds are known | Duplicate invoices, approval-limit breaches, sanctions screening |

| Anomaly detection | Catches subtle shifts without labeled fraud examples | Can flag legitimate growth or seasonal spikes | Off-cycle payroll spikes, unusual vendor spend, out-of-hours edits |

| Supervised models | Highest accuracy for known fraud patterns | Requires large volumes of confirmed fraud cases | High-volume payment environments with documented fraud history |

| Hybrid logic | Combines rule reliability with AI flexibility | More complex to configure | Growth companies managing both payroll and vendor risk |

Most growth-stage finance teams end up using a hybrid setup. Rules handle hard stops, while anomaly detection scores the rest against the baseline. That helps keep the alert queue under control for the ownership and review process that comes next.

Generating alerts is only half the job. The other half is making sure someone looks at them, takes action, and records the outcome without turning the queue into a mess. Once AI starts flagging risk, the control process decides what happens next: does the alert stop a bad transaction, or does it become background noise?

The same signals used for detection should also decide who steps in.

Each alert type needs a named owner and a backup reviewer. Payment-routing and bank-account-change alerts usually belong with Treasury or AP. Payroll change and off-cycle payment alerts usually go to HR and Payroll. Large customer refunds or write-offs usually sit with Revenue Operations or AR, with oversight from the Controller. [8][9][11]

Critical alerts - like a high-risk vendor bank-detail edit or an off-cycle payroll payment to a new account - should be routed within 1–2 business hours and placed on a temporary hold until cleared. High alerts should move within 24 hours. Medium- or low-priority alerts can move within 2–3 business days. If the possible loss is more than $50,000, or if repeat control failures point to a bigger problem, escalate to finance leadership or legal/compliance. [5][8][13]

Maker-checker matters here. The person who requested the change can't be the one who approves the alert. That split should be enforced inside the ERP, HRIS, or AP workflow, not left as a policy sitting in a binder. Every alert outcome also needs to be logged with a case ID, summary, decision, financial impact, and timestamp. [8][9][10]

Static thresholds stop working fast when volume grows. A fixed dollar cutoff might make sense for a smaller team, then fall apart once transactions start piling up. That's why relative thresholds work better in many cases.

For example, you can flag vendor invoices that go above 150% of that vendor's usual monthly average. Or flag payroll changes that push net pay more than 30% above the prior period. [6][7]

Not every alert type should be tuned the same way. For wires and bank changes, lean toward higher recall. For high-frequency, low-dollar refunds, lean toward higher precision. Make threshold changes in small steps - about 3–5 points at a time - and give each change at least one week before deciding whether it helped. If a rule produces fewer than 1 confirmed issue per 100 alerts, it needs to be redesigned or suppressed. [3][4][6][7]

Detection falls apart when the data can't be trusted. If too many people can edit vendor records, payroll files, or bank portal settings, the alerting layer is already on shaky ground.

Use role-based access controls so only designated roles can make changes to vendor master records, payroll files, and bank portals. If someone wants to override a high-risk alert, require second-level sign-off and a written log entry. [12][13][15]

Run a formal review at least quarterly. Backtest current rules against 12–24 months of historical transactions to see how many known loss events the rules would have caught and how many false positives they would have created. Track a short set of operating metrics:

Also log every threshold change, why it was made, and finance leadership sign-off before release. [14]

The takeaway is straightforward: connect the data, layer the models, and send alerts to people who can move fast.

As a company grows, the risk grows with it. More transactions, more vendors, more payroll changes - those extra moving parts give fraud more room to hide. And when it sits there too long, the cost goes up.

This framework comes down to three parts: connect the data, layer the detection methods, and route alerts to clear owners. Payments, refunds, payroll, and vendor activity should work like one system, not four separate streams. Fraud often shows up in the spaces between them.

The detection stack matters too. Rules catch known red flags. Anomaly detection spots outliers. Supervised models match known fraud patterns. But detection by itself isn’t enough. It only helps when the alert lands with the right owner at the right time.

That’s where ownership and SLAs come in. Every alert needs a named owner, a response window, and a maker-checker path that keeps requesters separate from approvers. Without that setup, even a well-tuned model turns into a dashboard people glance at and ignore.

Static thresholds also break down as volume shifts. Dynamic, relative thresholds - paired with regular backtesting and case-driven tuning - help keep controls calibrated as transaction volume grows.[1][16][2]

Start with four core systems: your ERP or accounting software, bank accounts, CRM, and payroll or HRIS platforms. Those systems hold the main data you need to track cash, revenue, and headcount.

Begin with read-only API access. That gives you room to check AI-suggested mappings, verify the data is clean, and make sure everything lines up before you add more advanced automation or write-back features.

Use rules for repetitive, standardized, high-volume work like basic accounts payable and accounts receivable workflows.

Choose rules when you need absolute consistency, clear logic, and direct policy execution. Use AI for more complex patterns, cutting false positives, and spotting anomalies or unstructured data that static rules can miss.

Fraud thresholds need regular updates so models keep working as threats shift. AI can watch activity in real time, but finance teams should still review risk models every quarter.

It also helps to check performance metrics monthly to catch problems early. Then, run annual system audits to make broader adjustments as the business grows.