Published on

July 12, 2026

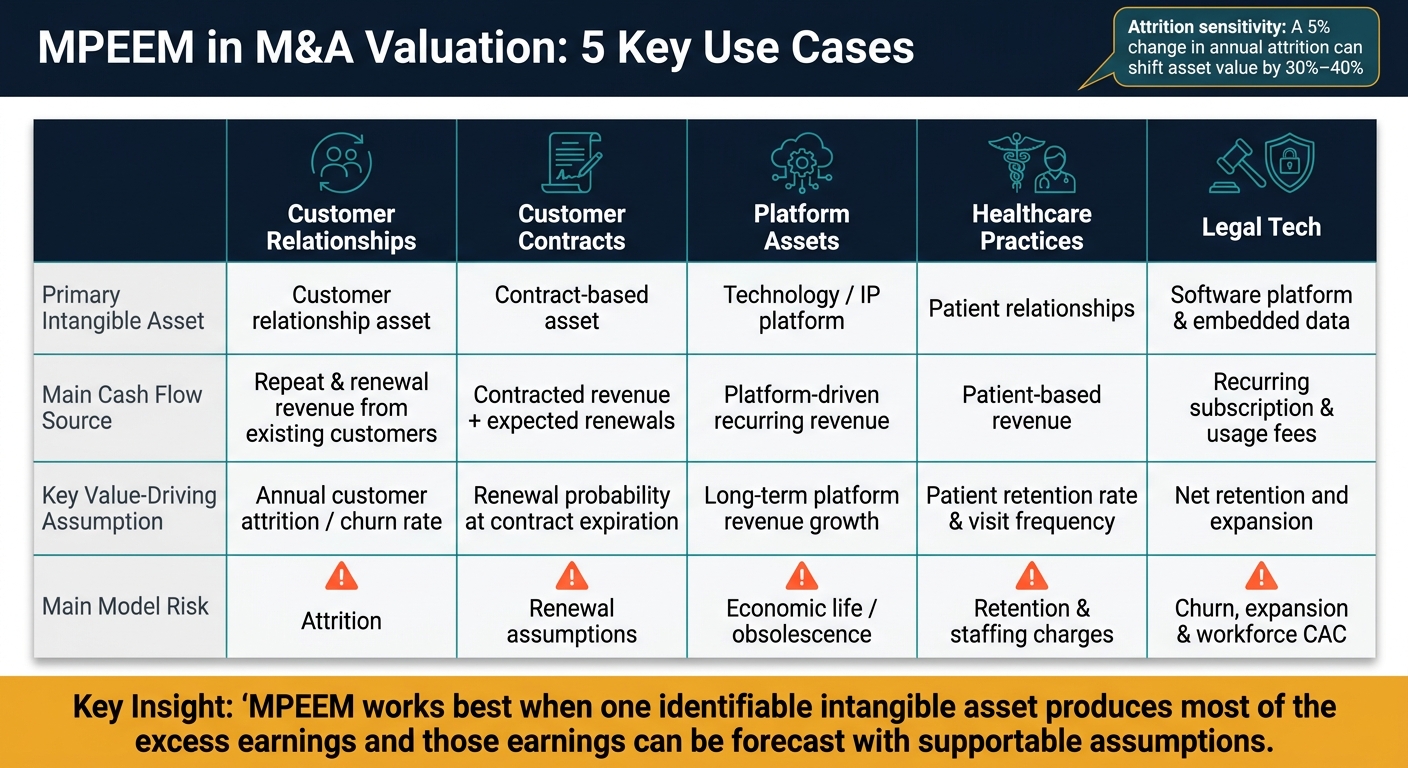

MPEEM is usually the right pick when one intangible asset drives most deal earnings and you can tie those cash flows to that asset. In this piece, I narrow that down to five common M&A cases: customer relationships, customer contracts, platform assets, healthcare practices, and legal tech deals.

Here’s the short version:

The main split is simple:

| Case | Main asset | Main cash flow source | Main model risk |

|---|---|---|---|

| Customer relationships | Existing customer base | Renewals, repeat sales, upsells from current customers | Attrition |

| Customer contracts | In-force contracts | Contracted revenue and supportable renewals | Renewal assumptions |

| Platform assets | Core software or platform | Subscription, usage, or transaction revenue | Economic life |

| Healthcare practices | Patient relationships | Repeat patient visits and care revenue | Retention and staffing charges |

| Legal tech | Platform or recurring client base | Subscription and usage fees | Churn, expansion, workforce CAC |

If I had to sum it up in one line: MPEEM works best when I can isolate one income-producing intangible and defend every major input behind it.

MPEEM works in a pretty narrow set of cases. It makes sense only when one intangible asset drives most of the excess earnings and you can tie cash flows back to that asset with enough detail to defend the model.

If losing the asset would materially cut cash flow, that asset is the main driver.

That shows up in each of the five cases below:

MPEEM needs asset-level data, not just company-level financials.

That means using revenue, retention, renewal, churn, and margin data tied to the asset itself. The goal is simple: the model has to trace future earnings straight back to the intangible being valued.

If you can't break the data out at the asset level, MPEEM falls apart. In most cases, the forecast horizon runs 5 to 15 years.

You also need to subtract returns for support assets, often called contributory asset charges.

These usually include:

If those charges can't be supported in a clear way, the value becomes unreliable.

The main difference comes down to where the value sits.

Use RFR for licensed IP. Use with-and-without when removing an asset changes the business's value. Use MPEEM when one asset produces the excess earnings and comparable market data is hard to find.

That's why the next five examples center on customer, contract, and platform-driven intangibles.

These are the same conditions that show up in the five cases below.

Customer relationships are one of the most common acquired intangibles in U.S. M&A deals. MPEEM works well here when current customers drive most of the excess earnings, not post-close growth. That’s why customer relationships are often one of the clearest MPEEM use cases.

The forecast should include renewals, repeat purchases, and upsells from customers who were active at closing. It should leave out revenue from customers added after closing. That line matters because it shapes the valuation.

Attrition plays a big role in both useful life and forecast value. A 5% annual attrition rate points to a longer forecast period than a 20% rate, and even a 5% change in yearly attrition can shift asset value by 30%–40%.[11] In practice, analysts usually build attrition from historical cohort data. They may also break it out by customer type or tenure instead of using one blended rate for everyone.[10]

Once attrition sets the life of the asset, CACs show how much of the earnings must be assigned to other assets that help produce those cash flows. Typical required returns are shown below:

| Contributory Asset | Typical Required Return |

|---|---|

| Working capital | 3%–5% |

| Fixed assets | 8%–12% |

| Assembled workforce | 8%–15% |

| Technology / software | 12%–20% |

| Brand / trademarks | 10%–15% |

After those deductions, the remaining amount is the excess earnings tied to the customer relationship. That cash flow is then discounted to present value to estimate the fair value of the customer relationship.

If the cash flows come from signed agreements rather than the customer base in general, the analysis shifts from customer relationships to contracts.

Customer relationships often depend on whether buyers stick around. Customer contracts are different. They depend on signed terms.

Under ASC 805, customer contracts are a separate intangible asset, distinct from broader customer relationships. That means you need a contract-by-contract look at cash flow and useful life. Signed terms, pricing, and renewal rights shape both.

When modeling, include cash flows from in-force contracts and only those renewals supported by evidence. Leave out new business and cross-sell. You also need contract-level data, such as:

Financial statements on their own won’t get you there.[6][1][12] Those inputs are what drive the useful-life estimate.

Useful life should follow the contract itself. Fixed terms, auto-renewals, termination rights, and price escalators all affect how long excess earnings continue. So the analysis should reflect the actual economics of the contract, not assume renewals go on forever.[7][8]

After you project contract cash flows, deduct CACs for working capital, fulfillment assets, delivery technology, and the assembled workforce. And if contract fulfillment costs differ from the rest of the business, don’t rely on blended company margins.[6]

When the asset is the product, the lens changes. At that point, you’re not looking at contract economics first. You’re looking at platform economics. Use MPEEM when the acquired software platform or core code accounts for most of the deal value.

Start by isolating the revenue that comes from the platform itself, such as recurring subscription, usage, or transaction revenue. Leave out nonrecurring implementation or services revenue when it doesn’t belong to the platform economics. Then deduct CACs for the assets that support those cash flows. That usually includes net working capital, net tangible assets like servers and equipment, assembled workforce, and supporting IP like add-on modules or trade names.[2][4][3][13]

For technology assets, the big useful-life issue is economic obsolescence. In plain English, an asset can lose economic value before its legal life runs out because of tech shifts, competition, or broad economic pressure.[14] Some enterprise platforms can support a longer useful life, especially when they have deep integrations and are hard to replace. Others, especially in fast-moving markets, may age out much sooner.[10]

That’s why the technology should be valued over its economic life, not its legal life. It also helps to stress-test the result for churn, obsolescence, and changes in CAC.

The same residual-earnings logic also applies when the business value is embedded in professional practice revenue.

In healthcare acquisitions, MPEEM usually comes down to patient retention. A big part of the deal value often sits in patient relationships, and buyers are mostly paying for repeat patient cash flows.

The starting point is normalized practice cash flow. From there, physician pay is adjusted to market levels, and staff, rent, supplies, and malpractice costs are normalized with benchmark data such as MGMA salary data. In many cases, that process cuts reported EBITDA by a lot before CACs even enter the picture.

Next come CACs for working capital, equipment, clinical staff, and EMR systems. In U.S. physician practices, required returns on fixed assets often land in the 6–10% range, while clinical staff CACs are often estimated at 10–15% of replacement cost.[15][16][17] What’s left after those charges is the excess earnings tied to the patient relationship asset.

Useful life depends on a few plain but important things: attrition, succession, and payer mix. Stable primary care practices often show annual attrition of 5%–10%, which can support a 10- to 15-year useful life. More episodic specialty practices, like orthopedics or fertility, often support only a 3- to 8-year useful life.[18][19]

To model that life in a way that matches how the practice actually runs, analysts often fit attrition curves to past EHR, billing, and patient panel data. That helps build a decay profile grounded in the facts. A solo physician’s practice, for example, may have a hard stop if that doctor plans to retire in eight years. A multi-physician group can look different. If patients can shift to another doctor inside the same practice, succession planning may stretch the useful life.[19][20]

Payer mix can shift value too. A practice with heavier Medicaid exposure tends to carry more risk, which pushes present value down.

That same asset-level logic also applies to legal tech acquisitions.

Legal tech follows the same residual-earnings logic when one intangible asset accounts for most of the deal value. In practice, legal tech also fits MPEEM when the value sits mainly in either the software platform or the recurring client base.

The first step is to pin down the primary intangible. In software-led deals, that’s usually the platform technology. In recurring-revenue deals, it’s usually the customer relationships. That call shapes the cash-flow forecast, CACs, and the useful-life estimate.

For platform deals, model only revenue tied to the platform itself, such as:

Leave out implementation and consulting revenue.

For recurring-revenue deals, focus on renewals and expansion by cohort. Do not include new-logo growth.

You also need to deduct CACs for working capital, tangible assets, workforce, and trademarks. That workforce piece matters a lot in legal tech. Many platforms depend heavily on the people behind the product, so if you understate that CAC, you can end up overstating the residual earnings assigned to the primary intangible.[24][25]

Useful life depends on churn, contract structure, product embedding, and obsolescence risk. A SaaS tool that is deeply embedded in a legal team’s workflow may support a longer life. Fast-moving AI tools usually don’t.[21][22][23]

MPEEM in M&A: 5 Key Use Cases Compared

Each of the five M&A settings uses MPEEM in its own way. The table below strips those cases down to the inputs that matter most in valuation. Across all five, the outcome depends on isolating one main intangible asset and the assumption that shapes its excess earnings.

| M&A Setting | Primary Intangible Asset | Main Cash Flow Source | Key Value-Driving Assumption |

|---|---|---|---|

| Customer Lists & Relationships | Customer relationship asset | Repeat and renewal revenue from the existing customer base | Annual customer attrition/churn rate |

| Customer Contracts | Contract-based asset | Contractually committed revenue plus expected renewals | Renewal probability at contract expiration |

| Platform Assets & Core Technology | Technology/IP platform | Platform-driven recurring revenue | Long-term platform revenue growth |

| Healthcare Practices | Patient relationships | Patient-based revenue | Patient retention rate and visit frequency |

| Legal Tech Acquisitions | Software platform and embedded data assets | Recurring subscription and usage fees | Net retention and expansion |

That makes the differences much easier to spot.

The sharpest contrast is between customer contracts and customer relationships. Contracts come with a set term and committed revenue, so most of the weight falls on renewal probability at expiration. Relationships are non-contractual, so the attrition rate does most of the work instead.[5][7]

Platform and legal tech deals both depend on recurring use, but the drivers split from there. Platform deals lean on overall usage growth. Legal tech adds another layer on top: installed-base retention and expansion.

Healthcare is different because physician and clinical-staff CACs can eat up a large share of excess earnings, which means retention and staffing charges both have a big effect.[26][16][27]

MPEEM works in U.S. M&A valuation when one identifiable intangible asset produces most of the excess earnings and those earnings can be forecast with supportable assumptions. It works best when a single asset is doing most of the heavy lifting and the related cash flows can be isolated cleanly.

Across the five cases, the pattern stays the same: one dominant intangible, isolatable cash flows, and assumptions that can be defended. That shared setup is why the method works across very different deal types.

The output depends on clean inputs: supported forecasts, market-based CACs, and a defensible useful life. Phoenix Strategy Group helps growth-stage companies build cleaner financial data and better forecasting discipline for M&A analysis. A well-executed MPEEM is transparent, sensitivity-tested, and consistent with the purchase price allocation. That is what makes the result reliable.

MPEEM is the right choice when you need to value a specific primary intangible asset, such as a customer list or service contract, by isolating the cash flows tied to that asset. It’s a strong fit when customer relationships account for a large share of the intangible value.

This method works best when you have detailed inputs to support the analysis, including revenue forecasts, historical attrition, profit margins, and asset-specific discount rates. If the main source of value comes more from brand or technology, another method may be a better fit.

You need data that helps you isolate cash flows and work out contributory asset charges, including:

You’ll also need enough detail to calculate charges for contributory assets like working capital, fixed assets, workforce, technology, and brand. That’s how you get to the excess earnings tied to customer relationships.

Attrition rate is often the most sensitive MPEEM input in a customer relationship valuation. Even a 5% shift can change value by 30% to 40%.

Other key assumptions matter too, especially Contributory Asset Charges (CACs), asset-specific discount rates, and revenue forecasts. If CACs are set too low or too high, they can skew the result. And if revenue projections are off, or if they include future expansion revenue, the valuation can end up overstated.