Published on

June 18, 2026

If a merger gets cleared with conduct rules instead of a sell-off, the deal may close, but the limits can last for years and cut into the buyer’s plan. I’d treat behavioral remedies as deal terms, not legal fine print.

Here’s the short version:

A few examples make the point fast. Illumina offered a 12-year supply commitment in the GRAIL deal. Google accepted a 10-year health-data silo in Fitbit. Sprint/T-Mobile included a three-year price freeze. Microsoft’s Activision matter ended with different outcomes across jurisdictions, including a 15-year cloud-rights fix tied to Ubisoft in the UK.

| Remedy type | What it does | Main risk it targets | Common cost to the buyer |

|---|---|---|---|

| Access / supply | Keeps rivals or customers connected to key inputs, APIs, or tech | Foreclosure | Lower margin, service duties, reporting load |

| Pricing / bundling | Limits exclusivity, tying, rebates, or price moves | Leverage from one product into another | Less pricing freedom, weaker cross-sell plan |

| Data firewall | Separates data, teams, or systems | Misuse of sensitive information | Slower integration, IT controls, audit spend |

I’d boil the article down to one point: a behavioral remedy can save a deal, but it can also reshape the deal model for 5, 10, or even 20 years. So before signing, I’d want a clear view of scope, term, enforcement, cost, and who owns compliance inside the business.

Behavioral remedies usually fall into three buckets: access commitments, pricing and contracting limits, and data or firewall controls. Each one lines up with a different antitrust risk: foreclosure, leverage, or data misuse. For growth-stage deals in software, data, and platform markets, these are often the remedies that matter most.

These remedies require the merged company to keep supplying rivals or customers on fair, reasonable, and non-discriminatory (FRAND) terms. Regulators use them when rivals depend on the merged company for an input or interface they can’t do without. The point is simple: stop the merged company from cutting rivals off.

In practice, this can mean opening APIs, giving technical support, or sharing technical specs and interface details so third-party products remain interoperable with the merged company’s platform. Supply duties often also include price caps tied to past averages and minimum volume terms, so the merged entity can’t squeeze downstream rivals by changing price or output. [1]

A clear example came in March 2021. As part of its acquisition of GRAIL, Illumina offered a 12-year supply contract to U.S. oncology customers, guaranteeing access to Illumina’s DNA sequencing technologies with no price increases. The goal was to ease concerns that Illumina could foreclose GRAIL’s rivals from inputs they needed. [2]

This set of remedies goes after sales tactics that could let the merged company carry market power from one line of business into another. That can mean limits on exclusivity, loyalty rebates, tying, and bundling that push customers away from rivals.

In plain English, a company may not be allowed to package a market-leading product with a nearby offering just to win deals. It may also have to end existing exclusivity or supply agreements. In some cases, it can’t negotiate better terms for itself than the terms rivals can get. [1]

The Sprint/T-Mobile merger in July 2019 shows how broad these limits can be. As part of DOJ approval, the parties agreed to a three-year price freeze for consumers, a 5G network deployment commitment, and the divestiture of Boost Mobile to DISH Network. [2] That price freeze put a direct limit on post-closing pricing.

In digital markets, this same concern often moves away from price and toward data access.

In data-driven and platform businesses, the antitrust issue often isn’t control of a physical asset. It’s control of sensitive information. That’s where firewalls and data silos come in. They are built to stop harmful information flows, not just physical access.

These commitments can require separate teams, separate IT systems, and non-disclosure agreements (NDAs) so competitively sensitive information doesn’t move between business units. Regulators often bring in an independent monitoring trustee to audit compliance and report straight to the agency. In some cases, a hold-separate manager runs the ring-fenced unit. [1]

The European Commission approved the Google/Fitbit deal only after Google agreed to keep Fitbit health data in a separate silo for 10 years and barred its use for Google Ads. [2]

The next issue is how to draft, monitor, and enforce these commitments so they survive closing.

The next step is turning access, pricing, and data commitments into terms regulators can actually check.

Divestitures do not always fit integrated businesses or markets driven by product development. In those settings, behavioral remedies can protect competition without forcing the parties to split assets that still matter to the business.

These remedies tend to work better when prices and usage can be audited without much guesswork, the sector already has a regulatory framework, the market is fairly predictable, and the parties can cover the cost of an independent monitoring trustee. [5][6]

Vague promises fall apart fast. If a party says it will offer access, on what terms? At what price? For how long? Regulators need hard edges, not soft language.

That means the pricing formula, service levels, and reporting window should be spelled out. Each obligation should connect to a defined competition issue and be written so an auditor can test it.

The table below links common competition risks to concrete commitments, measurable KPIs, and the internal team that would usually own compliance.

| Identified Competitive Risk | Proposed Behavioral Commitment | Compliance KPI | Internal Owner |

|---|---|---|---|

| Foreclosure of Rivals (Vertical) | Mandatory Licensing (FRAND terms) | Number of licenses executed; average time to close license | IP/Licensing lead |

| Higher rival costs | Price caps or MFN (Most Favored Nation) clause | Quarterly pricing audits vs. benchmark | Sales/Finance lead |

| Data Accumulation Advantage | Data silo / information firewall | Audit logs of data access; physical/logical separation | Chief Data Officer / CISO |

| Lock-in | Interoperability / data portability | API uptime; successful data transfer rate | Head of Product / Engineering |

But specificity alone will not carry the day. The remedy also needs an end date. Duration matters, and a sunset clause should be part of the design. Most commitments last five to 10 years. [5][6]

A good example is the Vodafone/Three merger. The UK CMA cleared the deal subject to an £11 billion network investment commitment over eight years and a three-year consumer price cap. [5][6]

Remedy risk shapes both the merger agreement and the valuation model, so it should be priced in early, not tacked on at the end.

In the deal papers, regulatory covenants should set out how far the buyer must go to win approval and the outer limit on the conduct terms it will accept. [1]

On the economics side, behavioral remedies can change the model in a few direct ways:

Still, those costs only mean something if the remedy can be monitored and enforced.

Design is only the starting point. Execution is what regulators watch. Once the deal closes, the company needs one formal owner for remedy compliance.

In most cases, that means a compliance officer or a dedicated committee handling remedy obligations day to day, with legal, finance, operations, sales, and product all involved.[1] And that makes sense. A pricing restriction lands with sales. A data firewall lands with product and IT. A supply commitment lands with operations. If no one owns those handoffs across teams, things slip.

Board oversight matters too. Knowing violations can trigger daily civil penalties and private treble-damage claims.[1] That’s not the kind of risk a company can manage with vague meeting notes or informal check-ins. It needs records that show who was responsible, what was reviewed, and what action was taken.

Regulators don’t take a company’s word for it. They want proof. That’s why they appoint monitoring trustees with broad authority to review books, records, personnel, and facilities during the compliance period, tracking performance across the full remedy term.[1]

During interim periods, regulators may also require an independent hold-separate manager to run a business unit day to day. That manager’s job is tied to the remedy, not the buyer’s business goals.[1]

Companies are also usually required to self-report on a set schedule. That turns internal audit trails, IT access logs, training records, and contract data into evidence. Each remedy needs its own paper trail. A firewall needs access logs. A pricing rule needs discount and contract records. A supply obligation needs fulfillment data. Data separation needs system controls and monitoring.

| Remedy Obligation | Required Data Source | Reporting Frequency | Internal Owner | External Recipient |

|---|---|---|---|---|

| Firewall Compliance | IT access logs, training records | Monthly / Quarterly | Compliance Officer / IT Head | Monitoring Trustee / FTC / DOJ |

| Non-Discrimination | Price lists, discount logs, contract terms | Annually | VP of Sales / Legal | FTC / DOJ / Monitor |

| Supply Commitments | Inventory, order fulfillment logs | Quarterly | Operations / Supply Chain | Monitoring Trustee |

| Interoperability / API Access | API uptime logs, data transfer records | Quarterly | Head of Product / Engineering | Monitoring Trustee / Regulator |

| Hold-Separate Independence | Financial statements, manager meeting minutes | Monthly | Hold-Separate Manager | Monitoring Trustee |

A good example is the Staples/Essendant deal. The FTC required Staples to set up a firewall that restricted access to Essendant's commercially sensitive customer information. Only employees in specific, non-decision-making functions could access that information. In practice, that meant documented IT controls, access logs, and recurring audits to show the firewall was working as required.[4]

Those records aren’t just for regulators. They also become part of the cost base.

Behavioral remedies don’t just add compliance expense. They can change how the business runs. Finance leaders should treat that as a core planning issue, not a side note.

Pricing flexibility gets tighter. Non-discrimination and fair-dealing rules can limit the merged company’s ability to charge rivals more for key inputs or access, which can cut into margins on those deals. Firewalls can slow cross-selling and make integrated product development harder because sensitive information can’t move freely across business units.[3]

Then there are the direct cash costs. Monitoring trustees, external auditors, and outside counsel all add recurring spend tied to reporting and oversight. Finance teams should put those items directly into the annual budget, not bury them inside a general legal reserve.

The cleaner approach is to model the full-term effect up front:

Treat remedy costs as operating constraints that stay in the model over time, not as one-time legal fees booked at closing.

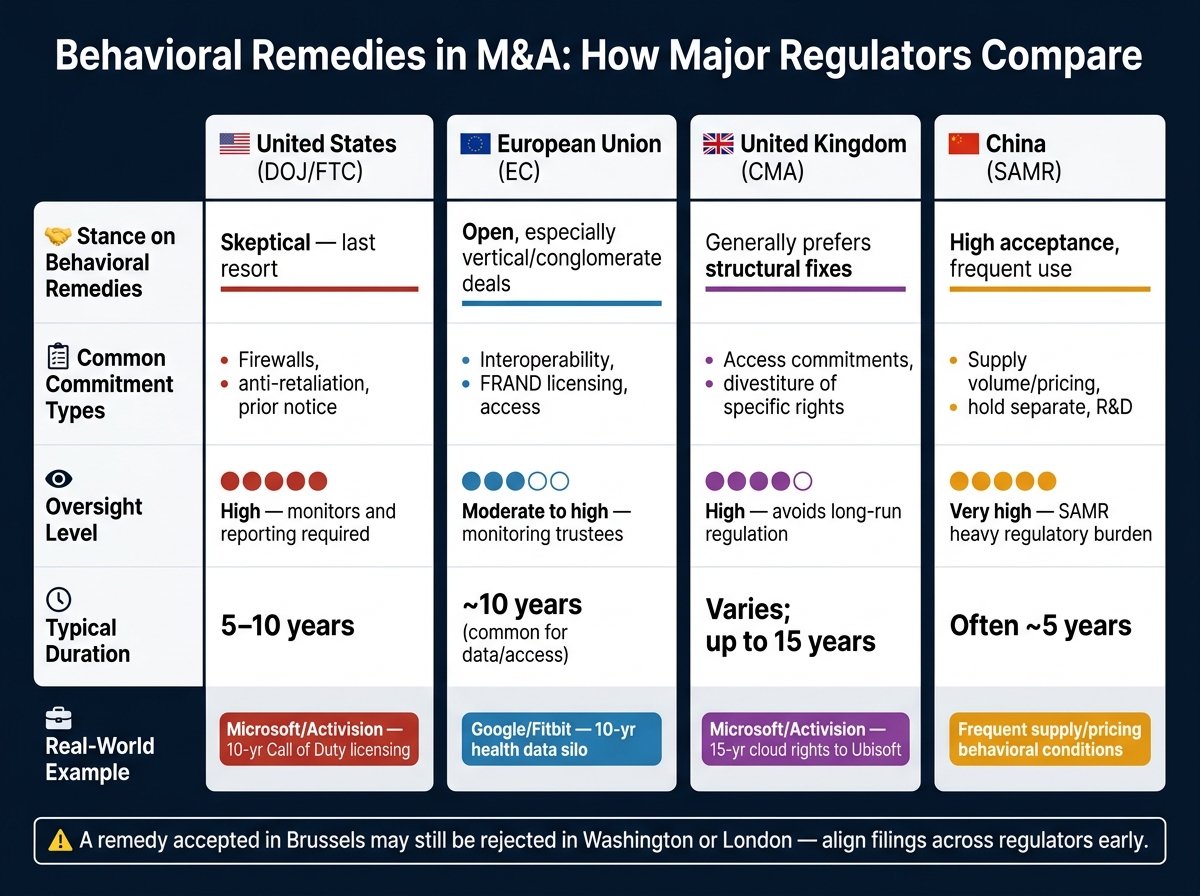

Behavioral Remedies in M&A: Global Regulator Comparison Guide

Enforcement standards change by jurisdiction, and that can reshape both remedy design and overall deal risk. In multi-jurisdiction transactions, that gap matters a lot. The DOJ generally prefers structural remedies because they are cleaner and easier to police. In the U.S., the share of challenged mergers that relied on purely behavioral remedies dropped from 13% in 1999–2003 to 6% in 2017–2021.[2]

Other major regulators do not always see it the same way. The European Commission is more willing to accept behavioral commitments, especially in vertical or conglomerate deals. Those often include access, interoperability, and licensing terms. China's SAMR also uses behavioral remedies often, in many cases to shield domestic downstream competitors. The UK's CMA sits closer to the U.S. position and usually prefers structural fixes, though it has accepted long-term conduct commitments in certain matters.

Microsoft's Activision Blizzard deal is a clear example of how far regulators can split. Microsoft signed 10-year licensing agreements for Call of Duty with Nintendo and Nvidia, and the UK CMA later cleared the deal only after Microsoft agreed to divest cloud streaming rights to Ubisoft for 15 years.[2] You can see the split most clearly in how each regulator handles access, duration, and oversight.

Use the matrix below to compare remedy risk before committing to a filing plan.

| Jurisdiction | Stance on Behavioral Remedies | Common Commitment Types | Oversight | Typical Duration |

|---|---|---|---|---|

| United States (DOJ/FTC) | Skeptical; usually a last resort | Firewalls, anti-retaliation, prior notice | High; usually requires monitors and reporting | 5–10 years[3] |

| European Union (EC) | More open in vertical/conglomerate deals | Interoperability, FRAND licensing, access | Moderate to high; uses monitoring trustees | 10 years is common for data and access commitments[2] |

| United Kingdom (CMA) | Generally prefers structural fixes | Access commitments, divestiture of specific rights | High; avoids long-run regulation where possible | Varies; can be long-term, such as 15 years[2] |

| China (SAMR) | High acceptance; frequent use | Supply volume/pricing, hold separate, R&D | Very high; SAMR bears a heavy regulatory burden | Often 5 years[4] |

For multi-jurisdiction deals, remedy offers should be lined up across regulators early. A behavioral commitment that works in Brussels can still be turned down in Washington or London, leaving the transaction stuck with hold-separate obligations and added cost.[2]

Remedy risk should be built into the deal model from day one, not after the letter of intent is signed. A pricing restriction or a long-term supply commitment can change the economics of a transaction in ways a standard synergy model may not catch.

Model each likely regulatory outcome in the deal case. What does a firewall cost to run each year? How much does a non-discrimination commitment squeeze margins? How much does data separation slow product integration? Founders and investors should pressure-test these remedy scenarios against valuation and integration plans before signing.

That is where specialized transaction support can help. Phoenix Strategy Group works with growth-stage companies to model remedy costs, set up reporting workflows, and review exit impact.

Behavioral remedies can get a deal across the finish line, but they also bring long-term operating limits. The hard part is not just getting the remedy accepted. It is pricing the constraint, assigning who owns it, and making that call before signing.

Structural remedies usually mean divestitures: selling assets or whole business units to keep the market competitive. Once that sale is done, agencies often have little left to oversee.

Behavioral remedies allow the merger to move forward, but with rules attached. Those rules can include licensing technology, giving rivals access, or staying away from certain pricing moves. Unlike structural remedies, they need regular agency oversight, which makes them harder to carry out.

Behavioral remedies usually come into play when divestiture or other structural relief isn't available, or just doesn't go far enough to fix the anticompetitive harm.

That tends to happen in vertical deals and foreclosure-type cases. Sometimes there's no suitable buyer. In other cases, there isn't a clean asset package that can be sold off. And sometimes agencies decide that conduct rules can fix the problem on their own - and that those rules can be monitored and enforced in a practical way.

Buyers should price long-term behavioral remedy risk with one simple point in mind: if the remedy falls apart, the transaction parties bear the cost, not consumers.

That matters more than it may seem at first glance. These remedies often call for years of agency oversight, and that can turn into a steady drag on the deal. The parties may face added administrative costs, compliance duties, enforcement risk, and limits on profit maximization during the monitoring period.