Published on

May 23, 2026

When you sell a business, taxes can significantly reduce your proceeds. But with the right planning, you can minimize, defer, or even eliminate some of these taxes. Here are seven strategies to help you keep more of your earnings:

Key takeaway: Early planning is essential. Strategies like QSBS exclusions and trust planning require years of preparation. Starting now can save you millions during a business exit.

Capital Gains Tax Rates by Business Structure & Sale Type

When you sell a business, the IRS taxes the profit you make - the difference between your original investment (basis) and the sale price. The tax rate you face depends largely on how long you’ve held the asset. If you’ve owned it for over a year, it’s considered a long-term gain and is taxed at lower rates: 0%, 15%, or 20%. However, if you’ve held it for less than a year, it’s treated as short-term and taxed as ordinary income, which can go as high as 37% federally [2].

For high-income earners, there’s an extra layer of taxation. The Net Investment Income Tax (NIIT) adds an additional 3.8% to capital gains, bringing the potential top federal rate to 23.8%. However, active business owners are often exempt from the NIIT on proceeds from a sale. These basic rules form the foundation for understanding more advanced tax strategies.

"Taxation on realization creates what is called a 'lock-in' effect. When the tax rate on capital gains is constant with respect to the holding period, investors are financially rewarded for deferring the sale of the asset for as long as possible." - Grace Enda and William G. Gale, Brookings Institution [2]

The structure of the deal - whether it’s a stock sale or an asset sale - also plays a big role in determining the tax outcome. In a stock sale, the buyer acquires ownership interests directly, and the seller usually pays long-term capital gains tax on the entire profit. In an asset sale, the purchase price is divided among various assets like equipment, goodwill, and real estate. Each of these asset classes is taxed differently, and some, like equipment, may trigger depreciation recapture, which is taxed as ordinary income [1][4].

Here’s a breakdown of how federal taxes apply to different business types in an asset sale:

| Entity Type | Corporate-Level Tax | Owner-Level Tax | Approx. Effective Federal Rate |

|---|---|---|---|

| C Corporation | Yes (21%) | Yes (up to 23.8%) | 38–40% |

| S Corporation | No (unless built-in gains apply) | Yes (capital gains rates) | ~23.8% |

| Partnership / LLC | No | Yes (capital gains rates) | ~23.8% |

| C-Corp (Stock Sale) | No | Yes (capital gains rates) | ~23.8% |

For C corporations, an asset sale can result in a combined federal tax rate of 38–40%. This happens because the profits are taxed twice: first at the corporate level (21%) and then again when distributed to shareholders. In contrast, pass-through entities like S corporations, partnerships, and LLCs avoid this double taxation, as gains flow directly to the owners’ personal tax returns [3][5].

Understanding these distinctions is crucial when planning for the best tax outcomes. These fundamentals set the stage for more tailored capital gains strategies in the next section.

An installment sale offers a way to spread out your tax liability by collecting payments over several years instead of receiving the full sale price at closing. This approach allows you to recognize taxable income only as payments are received, rather than being taxed on the entire gain upfront. According to IRC Section 453, as long as at least one payment is made after the year the sale closes, the transaction qualifies for installment treatment [6].

The tax is calculated using the gross profit ratio, which divides the gain by the total contract price. This ratio determines the taxable portion of each payment. By spreading the income over time, you can manage your annual taxable income, potentially keeping it within lower capital gains tax brackets. This method may also help you avoid the 3.8% Net Investment Income Tax (NIIT), which applies to income over $200,000 for single filers or $250,000 for married couples filing jointly [6][7].

For example, a $5 million sale with a $500,000 basis restructured as an installment sale could increase after-tax proceeds by approximately $210,000 compared to an all-cash sale [7].

"The culprit isn't typically the sale price; it's the devastating impact of immediate tax obligations and payment security concerns that can slash actual proceeds by 40% or more." - Ken Fick, CPA and MBA [7]

However, there are some key considerations to keep in mind. Depreciation recapture is taxed as ordinary income in the year of the sale, regardless of when payments are received. This means you'll need enough liquidity to cover this tax liability upfront [6]. Additionally, while the principal payments are eligible for capital gains treatment, the interest portion of each installment is taxed as ordinary income.

This strategy works best for pass-through entities like S corporations, LLCs, and partnerships. C corporations, however, face double taxation on asset sales, which can significantly reduce the benefits of deferring taxes [7]. It's also important to note that installment sales generally cannot be applied to inventory, dealer dispositions, or publicly traded securities [6].

To reduce the risk of buyer default, consider securing payments with tools like a promissory note, a standby letter of credit, or a structured sale involving a financial intermediary. You'll also need to track and report each payment annually using IRS Form 6252 [6].

When paired with other tax planning strategies, installment sales can be a powerful way to enhance your overall exit plan.

Investing capital gains into a Qualified Opportunity Fund (QOF) can both defer and potentially reduce taxes. A QOF is a corporation or partnership specifically set up to invest in Qualified Opportunity Zones (QOZs) - economically distressed areas identified and certified by the federal government. Across the U.S., there are 8,764 certified QOZs spanning all 50 states, Washington, D.C., and five U.S. territories [9].

To take advantage of this program, you must reinvest eligible capital gains into a QOF within 180 days of realizing the gain [8]. These investments must be in the form of equity - debt instruments are not eligible. Qualifying gains can come from the sale of assets like business stock, real estate, Section 1231 property, or partnership interests. However, gains from transactions involving related parties are excluded [8][12].

The tax benefits are structured in three parts:

"The opportunity zone program is designed to offer a three-part tax incentive for investors who reinvest capital gains into Qualified Opportunity Funds (QOFs)." - Thomas Wall, Partner, Anchor1031 [12]

Recent regulatory updates have added even more incentives. The Opportunity Zone program became permanent with the signing of the One Big Beautiful Bill Act on July 4, 2025. Under the updated rules, known as OZ 2.0, the fixed expiration date has been replaced with a rolling five-year deferral period for investments made after December 31, 2026 [10][11]. Additionally, a new category called Qualified Rural Opportunity Funds (QROFs) offers enhanced benefits, including a 30% basis step-up after five years, compared to the standard 10% for traditional QOFs. For example, if you defer $1,000,000 in gains:

There are a few practical considerations to keep in mind. Depreciation recapture cannot be deferred through Opportunity Zone investments [12], and state tax rules may differ. For instance, California does not align with federal QOZ regulations, meaning state taxes could still be due upon exit. Additionally, compliance is key: you must file Form 8996 to self-certify your QOF and Form 8997 annually to report your holdings. Failure to meet these requirements could trigger an inclusion event, ending your tax deferral early [8][9].

To make the most of Opportunity Zone investments as part of your tax strategy, consider seeking expert advice. Phoenix Strategy Group specializes in helping investors navigate these opportunities effectively.

If your business holds substantial real estate assets, a Section 1031 like-kind exchange can help you defer taxes on capital gains, depreciation recapture, and the Net Investment Income Tax (NIIT) [13]. Without a strategy like this, taxes could take a hefty bite - 30% or more - out of your proceeds [13].

Here’s how it works: To qualify, you need to hire a Qualified Intermediary (QI) before the sale closes. The QI acts as a neutral third party, holding the proceeds so you never directly handle the funds. If you take control of the money, the exchange is immediately disqualified.

"A 1031 exchange is not a loophole you can 'fix later' at closing. The 1031 exchange rules require planning before the sale contract is signed." - Rustin Diehl, JD, LLM (Tax), Allegis Law [13]

Once the sale of your property is finalized, the clock starts ticking on two key deadlines: 45 days to identify replacement properties and 180 days to close the purchase. These timelines are set in stone - no extensions allowed. Here’s a quick overview of the process:

| Milestone | Deadline | Action Required |

|---|---|---|

| Day 0 | Closing date | Proceeds go directly to the QI |

| Day 45 | Identification deadline | Submit a written list of replacement properties to the QI |

| Day 180 | Exchange deadline | Close on the replacement property |

| Tax filing | With your return | Report the exchange using IRS Form 8824 |

For example, in 2024, a client sold a Chandler, Arizona duplex purchased in 2014 for $185,000 and sold it for $520,000. The $335,000 gain included $42,000 in depreciation recapture. By using a 1031 exchange to reinvest in a Mesa commercial strip center, the client deferred about $85,000 in taxes, keeping that money working in the new property [15].

Be aware of the "same taxpayer" rule, which means the entity selling the original property must also be the one acquiring the replacement property. If you need to restructure - say, converting from a partnership to an LLC - you must do so before starting the exchange. To defer all taxes, the replacement property must be of equal or greater value, and any debt on the old property must be replaced. Any shortfall, known as "boot", becomes taxable immediately [14].

"A properly structured 1031 exchange lets you defer capital gains and depreciation recapture, preserving capital to reinvest in higher-value properties." - Rustin Diehl, JD, LLM (Tax) [13]

For advice on how a Section 1031 exchange could fit into your broader exit strategy, reach out to the experts at Phoenix Strategy Group. This approach works well alongside other strategies to help you optimize your business exit.

If you were a founder or an early investor in a domestic C corporation and have been planning for an exit, Section 1202 of the tax code could offer you a significant tax benefit. This provision allows eligible shareholders to exclude up to 100% of their capital gains from taxation. That means these gains are not subject to the 3.8% Net Investment Income Tax (NIIT) or the Alternative Minimum Tax (AMT) when selling Qualified Small Business Stock (QSBS) [20].

"Section 1202 invites founders, early employees, and investors to take risks, build value, and retain more of their gains." - Joe Forish, CFA, CFP [18]

However, this exclusion isn’t automatic - it comes with specific requirements tied to the stock’s issuance date and the duration it’s held.

The exclusion amount depends on when the stock was issued and how long it has been held. For stock issued on or before July 4, 2025, shareholders can exclude up to 100% of gains if the stock is held for over five years. This exclusion is capped at either $10 million per issuer or 10 times your investment basis, with the company’s total assets limited to $50 million.

For stock issued after July 4, 2025, the One Big Beautiful Bill Act (OBBBA) increased the per-issuer exclusion cap to $15 million (adjusted for inflation starting in 2027) and raised the asset threshold to $75 million [20]. A tiered holding period applies under the updated rules:

| Holding Period (Stock Issued After July 4, 2025) | Gain Exclusion | Effective Federal Tax Rate (Including NIIT) |

|---|---|---|

| 3 Years | 50% | 15.9% |

| 4 Years | 75% | 7.95% |

| 5+ Years | 100% | 0% |

To qualify, the stock must be issued directly by a domestic C corporation. Importantly, S-corporations, LLCs, and partnerships are not eligible to issue QSBS. Furthermore, the company must use at least 80% of its assets in a qualified trade or business. This excludes industries like law, health, accounting, and financial services [18].

Another critical factor is that the exit must be structured as a stock sale rather than an asset sale. Since approximately 70% of small business exits are structured as asset sales, achieving QSBS eligibility often requires early negotiations with potential buyers [21]. Startup attorney Joe Wallin highlights the importance of making the right entity choice from the beginning:

"Choosing the wrong entity at formation is the most expensive avoidable error in startup law. On a $20 million exit, a founder who formed as an S corp instead of a C corp could owe over $3 million in federal capital gains tax." [19]

To maximize the benefits of QSBS, consider filing a Section 83(b) election on nonvested stock to start the holding period immediately. Another strategy is gifting shares to non-grantor trusts or family members to spread the per-issuer exclusion caps across multiple recipients [16][17].

While Section 1202 provides a powerful federal tax benefit, it’s worth noting that some states, such as California, Pennsylvania, and New Jersey, do not conform to this provision. As a result, state-level capital gains taxes may still apply.

QSBS is just one of several tools available to help optimize your tax strategy during an exit. Early planning and careful structuring can make a significant difference in the financial outcome.

Timing plays a huge role in minimizing taxes during an exit. When you close a deal can make or break your tax strategy. A single day can shift millions in tax liability from one year to the next, offering a chance to defer payments and keep your money working longer. This strategy ties closely with managing income and deductions for the best tax results.

Take this example: closing on January 1 instead of December 31 can push your tax bill out by an entire year. You’re not paying less, but you’re holding onto your capital for longer - a financial advantage you don’t want to overlook.

"Exit tax outcomes are determined years before the deal not during negotiations." - Tim Freese, CPA [22]

But timing isn’t just about the closing date. There’s even more value in planning how you handle income and deductions before the sale. For instance, deferred compensation is taxed as ordinary income in the year of the sale. By restructuring those balances at least 18 months before the sale, you can avoid stacking them on top of your capital gains - potentially keeping yourself out of a higher tax bracket [5]. Similarly, accelerating deductions, like prepaying expenses or making charitable contributions, in a high-income year can help reduce your exposure to the 3.8% Net Investment Income Tax (NIIT).

"Most owners optimize EBITDA. Few optimize after-tax proceeds." - Tim Freese, CPA [22]

Here’s a quick breakdown of timing decisions that can have the biggest impact during your exit planning:

| Planning Phase | Critical Timing Actions |

|---|---|

| 3 Years Before Exit | Normalize owner compensation; evaluate QSBS eligibility; clean up financial reporting |

| 18–24 Months Before | Restructure deferred compensation; minimize working capital; halt unnecessary reinvestment |

| 1 Year Before Exit | Harvest investment losses; explore charitable planning; stress-test multi-state tax exposure |

| At Deal Closing | Align purchase price allocation; confirm installment sale structure; finalize earnout treatment |

Earnout agreements add another layer of complexity to income timing. Without a cap on payments, "open transaction" treatment might let you recover your basis before recognizing gains [5]. Like other timing strategies, structuring earnouts requires early and careful planning. It’s also a good idea to have a CPA model tax outcomes for both stock and asset sale scenarios before you sign any LOI [22].

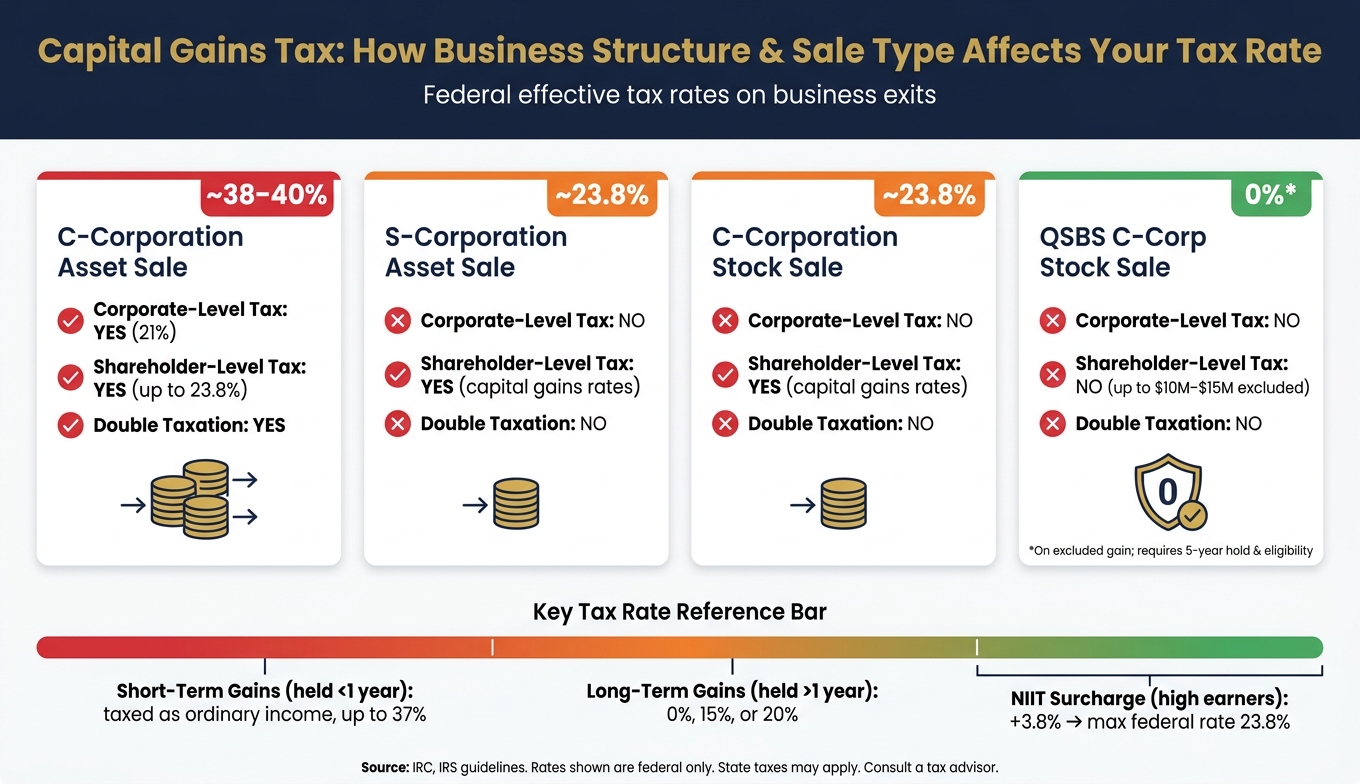

The way your business is structured and how a deal is framed can have a massive impact on the taxes you pay during an exit. For high-value transactions, the difference between a C-corp asset sale and a QSBS (Qualified Small Business Stock) stock sale could mean millions of dollars in after-tax proceeds [5]. That’s why structuring your exit with tax outcomes in mind is so important.

The main issue lies in how taxes are layered. In a C-corp asset sale, the IRS takes its share twice - once at the corporate level and again when dividends are distributed to shareholders. This double taxation leads to significantly higher overall rates. On the other hand, a stock sale or a pass-through structure, such as an S-corp, LLC, or partnership, typically results in a single layer of taxation, which is around 23.8% [5].

Here’s a quick look at how tax impacts vary by structure and sale type:

| Structure | Asset Sale (Federal) | Stock Sale (Federal) |

|---|---|---|

| C-Corporation | ~38–40% (double tax) | ~23.8% |

| S-Corporation | ~23.8% (flow-through) | ~23.8% |

| Partnership/LLC | ~23.8% (flow-through) | ~23.8% |

| QSBS C-Corp | N/A | 0% on first $10M gain |

If the buyer opts for a Section 338(h)(10) election, it could significantly increase your tax liability. In such cases, you should negotiate a price premium to compensate for the added tax burden. These negotiated "gross-ups" are often between 5% and 10% of the purchase price [5].

For C-corp owners considering a switch to an S-corp to avoid double taxation, it’s essential to plan for the five-year built-in gains (BIG) recognition period. Any appreciated assets sold during this period will still face corporate-level taxes [5]. Decisions made when forming your entity can have long-term tax consequences, potentially costing millions if not carefully planned.

Beyond structuring deals to defer taxes, proactive estate planning can significantly lower your capital gains tax burden. Many business owners wait until deal terms are finalized to begin tax planning, which often results in missed opportunities. The most impactful estate planning strategies require action before signing a Letter of Intent (LOI). At this stage, your business can be valued at a lower rate for gift tax purposes, preserving more value and complementing other exit planning efforts.

Here’s the basic concept: transferring ownership interests before your business is formally valued allows those interests to be gifted at a lower valuation. This valuation is typically based on current earnings rather than the premium a buyer might pay at the time of sale. Tools like Family Limited Partnerships (FLPs) make this even more advantageous. FLPs enable you to gift non-voting shares at a discount because of their reduced marketability and lack of control, lowering the taxable value of the gift [25][26].

For high-growth businesses, Intentionally Defective Grantor Trusts (IDGTs) are a powerful option. With an IDGT, you sell business interests to the trust in exchange for a promissory note, effectively removing future appreciation from your taxable estate. As the grantor, you remain responsible for the trust's income taxes, which allows for a tax-free transfer of wealth to your heirs [25]. If you hold Qualified Small Business Stock (QSBS), gifting shares to multiple family members or non-grantor trusts can multiply the $10 million federal capital gains exclusion per recipient [26].

ING trusts, which are established in states with no income tax (like Ohio or Tennessee), can help reduce state tax liabilities. These trusts act as separate taxpaying entities. For instance, in a 2025 Baird Trust case study, a founder named Adam had stock with a $2 million basis and a $42 million sale value. By setting up an ING trust in a no-tax state before the sale, Adam avoided his home state's 10% income tax on a $40 million gain - saving $4 million outright [24].

"Pre-sale estate planning allows you to turn a one-time liquidity event into a multigenerational wealth transfer strategy." - Mariner Wealth Advisors [23]

Another option, the Charitable Remainder Trust (CRT), offers multiple benefits: it defers capital gains taxes, provides an income stream, and grants a charitable deduction [23]. With the federal gift tax exemption set at $15 million per person in 2026, founders have a valuable opportunity to move appreciated assets out of their estate before finalizing a deal [23][25]. To fully leverage these strategies, it’s best to start planning 3–5 years ahead of your exit. This timeline allows you to maximize holding periods, secure valuation discounts, and take full advantage of these techniques [26].

When combined with earlier tax strategies, these estate planning approaches can help you craft a highly efficient and effective exit plan.

Relying on a single approach rarely delivers the best results. Instead, combining strategies can significantly improve tax efficiency. Take this example: a founder who qualifies for the Section 1202 QSBS exclusion could avoid federal taxes on the first $10 million of gain (or up to $15 million under the One Big Beautiful Budget Act [27]). Then, by using an installment sale, they could defer taxes on the remaining proceeds, spreading payments over several years. This approach helps keep annual income below the threshold that triggers the 3.8% Net Investment Income Tax [22]. In a $20 million transaction with $15 million of gain, this combination of strategies can increase after-tax proceeds by more than $3.5 million compared to a traditional C-corp asset sale [5]. Together, these tactics create a well-rounded exit plan.

The table below highlights how the choice of entity structure alone can significantly affect the effective tax rate, even before layering additional strategies:

| Entity Structure | Corporate-Level Tax | Shareholder-Level Tax | Illustrative Effective Rate |

|---|---|---|---|

| C-corp asset sale | Yes (21%) | Yes (23.8%) | ~38–40% combined |

| S-corp asset sale | No | Yes (capital gains) | ~23.8% federal |

| C-corp stock sale | No | Yes (capital gains) | ~23.8% federal |

| QSBS stock sale | No | No (up to $10M–$15M) | 0% on excluded gain |

Source: [5]

Timing is everything when combining these strategies. For example, the QSBS exclusion requires a five-year holding period, and recognizing built-in gains during entity conversions has its own timing considerations. Additionally, trust and estate planning often need to begin well before a deal closes. To maximize benefits, it’s essential to review QSBS eligibility and entity structure early. For installment sales and state residency planning, aim to finalize details 6–12 months before closing. These timing factors, layered with other tax strategies, can help secure the best possible outcome.

As Tim Freese, CPA, aptly explains:

"Exit tax outcomes are determined years before the deal - not during negotiations." [22]

Selling a business is a major milestone, but capital gains taxes can take a big bite out of your proceeds. The seven strategies covered in this article - installment sales, Opportunity Zones, 1031 exchanges, QSBS exclusions, deal timing, entity structure, and estate planning - offer practical ways to help you keep more of what you've earned.

The key to all these approaches? Time. As Goldman Sachs wisely notes:

"The tax implications of selling a business should be considered at all stages of the transaction." [3]

Some strategies, like QSBS exclusions or trust planning, require years of preparation, making early action critical. Starting sooner rather than later expands your options and puts you in a stronger position to optimize your tax outcome.

Consider this: on a $20 million deal, a well-structured exit plan could save you over $3.5 million in after-tax proceeds [5]. That’s a powerful reminder of how preparation, the right deal structure, and expert advice can make a huge financial difference.

For personalized guidance, reach out to Phoenix Strategy Group. Their M&A advisory and fractional CFO services can help you evaluate your structure, model potential deal scenarios, and create a custom exit strategy tailored to your goals.

The most effective ways to save on taxes during an exit involve planning ahead and fine-tuning the structure of your business entity. For example, converting to a C-corporation can help you qualify for Qualified Small Business Stock (QSBS) benefits, while options like installment sales or stock sales can lower your tax burden. These strategies often need to be mapped out years before the exit to fully leverage tax advantages and stay within legal guidelines.

When deciding between a stock sale and an asset sale, it’s all about aligning with your tax and strategic objectives. For sellers, a stock sale tends to be more favorable because it typically qualifies for capital gains treatment, which can mean lower taxes. Plus, it avoids the issue of double taxation.

On the other hand, buyers usually lean toward asset sales. Why? They get depreciation benefits, which can be a big financial advantage. However, this approach might result in higher taxes for the seller.

To navigate these differences effectively, early planning is key. Negotiating terms - like agreeing on a higher sale price - can help bridge the gap between buyer and seller preferences.

To get the most out of QSBS and trusts - and to stay on the right side of compliance - start planning at least 18 to 24 months before you plan to exit your business. Starting early gives you the time needed to handle structuring and documentation properly, which are key to making the most of your tax strategies.