Published on

May 23, 2026

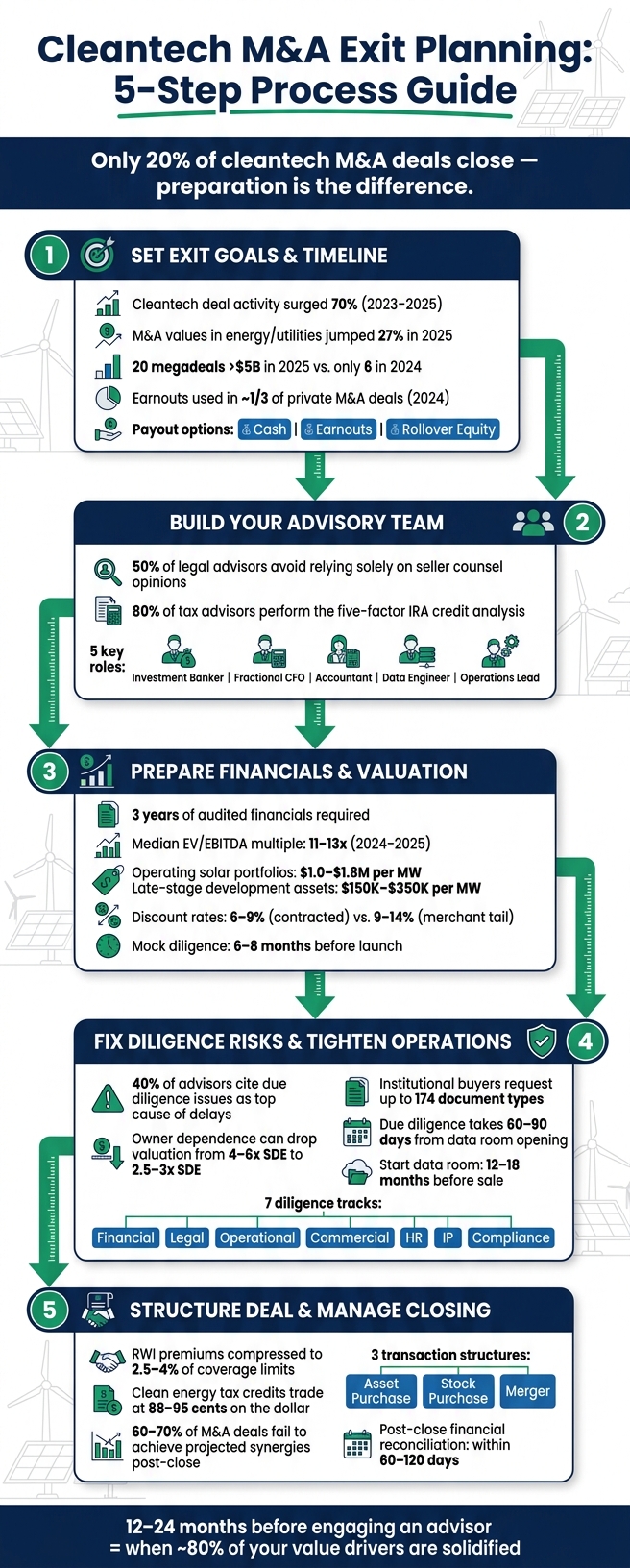

Cleantech M&A exits are complex and require meticulous preparation to maximize value. Here's what you need to know:

The article outlines a step-by-step guide to help founders navigate this process effectively, ensuring readiness across financial, legal, and operational aspects for a successful exit.

Cleantech M&A Exit Planning: 5-Step Process Guide

Before diving into conversations with buyers or bankers, it’s crucial to have clear exit goals. This helps you avoid making decisions that might not align with your long-term interests.

Start by asking yourself two essential questions: How much cash do you need from the sale? and What role, if any, do you want after the sale?

On the financial side, don’t let the headline enterprise value mislead you. In venture-backed deals, liquidation preferences can significantly reduce the actual cash founders receive. To get a clear picture, model the equity waterfall - it’s the only way to know what you’ll walk away with. At the same time, think about your post-sale involvement. Setting these objectives early on can also help you plan for potential tax issues, like Section 280G “parachute payment” taxes, which can add a 20% excise tax if not handled properly [5].

Decide how you want your payout structured. Options include:

Your choice will depend on your financial goals and how much risk you’re comfortable taking. Once you’ve clarified these, align them with current market trends to fine-tune your exit timeline.

Timing your exit matters, and it’s about syncing your readiness with what’s happening in the market. For example, cleantech deal activity surged 70% between 2023 and 2025 [1], while M&A values in energy, utilities, and resources jumped 27% in 2025. Notably, there were 20 megadeals worth over $5 billion that year, compared to just six in 2024 [6].

Right now, operational assets are commanding higher premiums than speculative projects. Buyers are especially interested in deployment-ready platforms like solar-plus-storage hybrids, firm power assets, and projects with secured grid interconnection. Given that interconnection queue wait times in markets like PJM and CAISO can stretch 4–5 years [2], having an approved interconnection position is a major selling point.

Here’s a quick look at how a project’s stage of development impacts its risk profile and valuation focus:

| Development Stage | Risk Level | Primary Valuation Driver |

|---|---|---|

| Greenfield | Highest | Site control, preliminary studies, structuring flexibility [3] |

| Pre-NTP | High | Permit status, interconnection studies, offtake negotiations [3] |

| Notice to Proceed (NTP) | Medium | EPC contracts, supply chain security, construction authorization [3] |

| Commercial Operation (COD) | Lowest | Cash flow stability, production history, O&M optimization [3] |

The upcoming July 4, 2026 deadline under the One Big Beautiful Bill Act (OBBBA) to begin physical construction and qualify for full tax credits [2] has created a sense of urgency. Assets nearing construction readiness are especially appealing, with a flurry of deals expected in the first half of 2026.

"With AI and data centres pushing energy demand to new heights, we're in an exciting era of dynamic dealmaking... 2026 is a prime time for dealmakers to capture value." - Tracy Herrmann, Global Energy, Utilities, and Resources Deals Leader, PwC US [6]

When setting your exit timeline, work backward from the market window rather than focusing only on your internal readiness. Take into account your project’s development stage, interconnection status, and tax credit eligibility to determine the best time to close the deal.

With your exit goals and timeline locked in, the next step is assembling a team that can handle the complexities of a cleantech M&A transaction. These deals require expertise across legal, tax, financial, technical, and regulatory areas - no single adviser can cover it all. Bringing in the right specialists early can mean the difference between a smooth closing and a deal that falls apart.

Your advisers must have specific cleantech expertise, not just general M&A experience. For instance, legal counsel should conduct their own in-depth analysis rather than relying solely on seller-provided legal documents. This is critical, as half of legal advisors in tax credit transactions avoid depending entirely on seller counsel opinions [7]. Similarly, your tax adviser needs to be skilled in specialized evaluations like the "five-factor analysis", which determines whether a project qualifies for IRA tax credits. Around 80% of tax advisors perform this analysis, while others rely only on utility letters [7].

On the financial side, look for advisers who can handle the unique challenges of cleantech assets. They should be able to model power price changes, assess risks like congestion and basis, and evaluate complex revenue structures that mix contracted offtake with merchant exposure [3]. If your asset is at the NTP (Notice to Proceed) or COD (Commercial Operation Date) stage, a technical adviser is essential. They’ll independently verify critical factors like energy yield, SCADA data, and interconnection feasibility [3].

"A systematic, cross-functional risk assessment spanning technical, regulatory, market, and commercial dimensions is required to quantify these exposures before term sheets are signed." - Enverus [3]

To keep everything running smoothly, assign clear roles to your team members. This avoids overlap and ensures every aspect of the deal is covered. Key roles might include:

| Advisory Role | Primary Responsibilities |

|---|---|

| Investment Banker | Valuation, buyer outreach, deal structure, negotiations |

| Fractional CFO | FP&A, forecasting, budgeting, strategic finance |

| Accountant | Weekly close, tax preparation, GAAP compliance, data cleanup |

| Data Engineer | ETL pipelines, data warehousing, analytics dashboards |

| Operations Lead | Team alignment, transition management, post-merger integration |

M&A deals often fail when teams work in silos. To avoid this, establish a single point of accountability - often your fractional CFO or lead M&A adviser. This person ensures that deal execution stays on track and aligns with operational goals week by week. This level of coordination is key to a smooth transition into full M&A support.

Phoenix Strategy Group is designed to address the silo problem directly. Their approach combines M&A advisory with hands-on operational support, covering everything from investment banking and fractional CFO services to bookkeeping cleanup and data engineering. By keeping all these services under one roof, they ensure consistency across financial cleanup, buyer narratives, and due diligence.

Their track record speaks volumes: over 100 M&A transactions, 5+ IPOs, and $200 million raised for clients in just the last 12 months [4]. For cleantech founders, this integrated approach offers both deal execution and financial credibility. As David Darmstandler, Co-CEO of DataPath, shared:

"As our fractional CFO, they accomplished more in six months than our last two full-time CFOs combined." [4]

Once your advisory team is set, the spotlight shifts to your financials. Buyers will dive into your numbers, and this is where deals can either come together or fall apart. Disorganized records, unexplained cash issues, or overly optimistic projections can erode buyer trust in no time. This step connects your past performance with future projections and valuation metrics, both of which buyers will scrutinize closely.

Buyers typically expect three years of audited financial statements, and they’ll compare every line item with your internal management accounts. Any discrepancies between what you’ve reported externally and internally will immediately raise concerns. Beyond the basics, you’ll need to adjust earnings to exclude one-time items like unusual marketing costs or extraordinary gains, so buyers can focus on your recurring performance.

Two common diligence hurdles are related-party transactions and unexplained cash balances. Be sure to document all promoter-related and related-party expenses, and reconcile every bank account fully. Buyers and their advisers often view unexplained cash balances as deal-breakers.

"M&A readiness is the ability of your financials to support extended diligence, informed negotiations, and realistic integration planning." - Sachin Gokhale [8]

Solid historical financials provide the foundation for credible forecasts and bolster your valuation story.

Once your past performance is clear, buyers will shift their focus to your future projections. These forecasts should be grounded in realistic operational assumptions. For cleantech assets with Power Purchase Agreements (PPAs), it’s helpful to split your model into two sections:

Use the P50 energy production estimate as your baseline revenue figure and include P75 and P90 scenarios to show downside sensitivity. Don’t forget to account for technical degradation - solar panels, for instance, lose about 0.4–0.7% efficiency annually [9]. Present sensitivity tables upfront to show that your forecasts are disciplined and realistic, which can help reduce prolonged negotiations.

"In sell-side processes for renewable portfolios, the single most common source of bid dispersion is the treatment of the merchant tail." - Energy IB [9]

With clear financials and well-structured forecasts, you’re ready to tackle valuation. The goal is to align your valuation multiples with current market dynamics. For example, the median EV/EBITDA multiple for operational renewable energy companies was around 11–13x in 2024–2025 [9]. Factors like contract quality, the creditworthiness of the offtaker, and asset maturity will influence where your deal fits within this range.

For context, operating solar portfolios with long-term PPAs often sell for $1.0–$1.8 million per MW, while late-stage development assets (secured PPA, NTP-ready) typically range from $150,000–$350,000 per MW [9].

To build buyer confidence and minimize the risk of price reductions during final negotiations, back up your valuation with a QoE report, tax memo, litigation register, and IP schedule. Running a mock diligence exercise 6–8 months before launching your sale process can help you identify and fix any gaps ahead of time.

Once your financials and valuation story are solid, it’s time to focus on eliminating surprises during due diligence. Nearly 40% of advisors highlight due diligence issues as a leading cause of transaction delays [7]. The good news? Most of these challenges can be addressed if tackled early.

Cleantech deals come with their own set of legal hurdles. One major area of concern is tax credit eligibility. If your project claims Investment Tax Credits (ITC) or Production Tax Credits (PTC), buyers will dig deep into the "placed-in-service" date. This isn’t just about having a utility Permit-to-Operate letter - it’s about meeting a rigorous five-factor analysis. Make sure all credits are properly registered with the IRS, and have Transfer Election Statements and pre-filing registration IDs ready before entering the market [11].

Another critical area is compliance with FEOC (Foreign Entity of Concern) regulations, especially for deals targeting a 2026 exit. Buyers will scrutinize your equipment sourcing and manufacturing chain to ensure no prohibited foreign entities, as defined under the Inflation Reduction Act, are involved [11].

Beyond tax and sourcing concerns, take a hard look at any sustainability claims your company has made. Whether these appear on your website, in marketing materials, or even in older documents, they need to be verifiable. As Jones Day points out:

"Public targets/claims can operate as 'soft liabilities' (future capex, operational changes, supplier data collection, assurance costs) the buyer inherits on post-close." [10]

Overstating or failing to back up environmental claims can expose you to legal risks after the deal closes.

After legal risks are addressed, shift your attention to reducing reliance on the owner. Buyers aren’t just purchasing your current revenue; they’re buying the confidence that this revenue will continue without you. If the business leans too heavily on your personal relationships or daily involvement, it could hurt your valuation. In fact, studies show that high owner dependence can pull valuation multiples down from 4–6x SDE to as low as 2.5–3x SDE [12].

This process takes time, so start early. Ideally, you should have at least one management layer - like a General Manager or COO - handling the day-to-day operations with minimal input from you. Aim to implement this structure 12–18 months before a sale. Additionally, document all recurring processes to ensure the business can run independently. A practical test? Step away for 30 days and monitor the results. If the business holds steady, you’ve demonstrated operational independence [12].

"A buyer is not acquiring your past. They are acquiring your future cash flows. If those cash flows depend on your continued presence, the buyer is underwriting your personal involvement, not the business. And people are not bankable." - Mike Ye, M&A Advisor [12]

Once operational risks are under control, focus on organizing your documentation. A well-prepared data room not only speeds up due diligence but also shows professionalism. On the flip side, a messy data room can slow things down and even give buyers a reason to renegotiate the price.

"A disorganized data room does not just slow the process. It gives buyers a reason to reprice." - Samuel Levitz, InvestorReadyCapital [13]

Structure your data room around standard diligence categories like Financial, Legal, Operational, Commercial, HR, IP, and Compliance. Use consistent file naming conventions (e.g., Financial_EBITDA_Bridge_2026-Q1) and assign responsibility for each category to a key team member, such as the CFO, COO, or General Counsel. If any documents are missing, include a brief explanation. As Samuel Levitz advises:

"Silence on a gap is worse than a brief explanation. Unexplained gaps often translate to a lower price or a larger indemnification clause." [13]

Start building the data room 12–18 months before a potential sale. Institutional buyers often request up to 174 different document types [13], and the due diligence process typically takes 60–90 days from data room opening to deal closure.

Here’s a breakdown of core diligence tracks and essential documents:

| Track | Key Documents |

|---|---|

| Financial | Audited statements (3–5 years), EBITDA bridge, AR/AP aging, tax returns, cap table |

| Legal/Gov | Articles of incorporation, board minutes, material contracts, litigation files |

| Operational | Org chart, IT stack documentation, facility leases, supplier contracts |

| Commercial | Top 10 customer contracts, churn data, sales pipeline, pricing history |

| HR/Team | Employee roster, executive agreements, equity incentive plans, benefit summaries |

| IP | Patent/trademark registrations, IP assignments, software licenses |

| Compliance | Business licenses, environmental records, data privacy docs |

Taking these steps will help you prepare for due diligence and set the stage for a smoother transaction process later on.

Once your data room is polished and diligence risks have been addressed, it’s time to focus on structuring the deal and managing the closing process.

The terms in your LOI and purchase agreement can significantly affect the financial outcomes of your deal. For example, earnouts are frequently used in cleantech deals to bridge disagreements on future growth projections. These performance-based milestones, often tied to EBITDA or revenue, allow both parties to reach a compromise without abandoning negotiations.

Pay close attention to representations and warranties. In mid-market deals, Representation and Warranty Insurance (RWI) has largely replaced traditional seller indemnification. By 2026, RWI premiums have compressed to 2.5%–4% of coverage limits, while retentions have dropped to 0.5%–1% of enterprise value [5]. This trend enables sellers to exit with minimal escrow requirements.

Cleantech transactions often involve unique considerations. If your deal includes Investment Tax Credits (ITC) or Production Tax Credits (PTC), carefully review the Tax Credit Transfer Agreement (TCTA). Clean energy credits currently trade at 88 to 95 cents on the dollar, depending on the technology and sponsor strength [11]. Additionally, identify any change-of-control triggers in key contracts, such as power purchase agreements (PPAs), interconnection agreements, or equipment leases. Overlooking a consent requirement could cause delays or even derail the deal.

"The structure of your deal determines who pays what in taxes, which liabilities follow you home, and whether your key contracts survive." - Alex Lubyansky, M&A Attorney [14]

Once you've clarified the key terms, you’ll need to decide on the transaction structure that best suits your goals.

Choosing the right transaction structure is critical, as it impacts taxes, liabilities, and operational considerations. Here’s a breakdown of the three main options:

| Factor | Asset Purchase | Stock Purchase | Merger |

|---|---|---|---|

| What transfers | Selected assets and assumed liabilities | Entire entity (all assets/liabilities) | Everything by operation of law |

| Tax basis | Stepped-up to fair market value | Carryover (seller's old basis) | Depends on structure |

| Liability exposure | Limited to assumed liabilities | All liabilities (known and unknown) | All liabilities (surviving entity) |

| Contract transfer | Requires individual assignment/consent | Usually automatic (check change-of-control) | Automatic by operation of law |

| Best for | Distressed assets, cherry-picking | Clean companies, contract-heavy firms | Large deals, public companies |

Tax treatment options also play a role. For instance, Section 338(h)(10) elections allow for a stepped-up basis, and Section 1202 exclusions can be beneficial for C-corp sellers [15]. Carefully weigh these factors to determine the structure that aligns with your financial and operational priorities.

Closing the deal is just the beginning of a successful transition. Poor integration planning is a major reason why 60%–70% of M&A transactions fail to achieve projected synergies [5].

"Post-closing integration remains the largest destroyer of deal value, with 60 to 70 percent of transactions failing to deliver projected synergies." - Michael Kimball, Esq. [5]

To avoid this, address any ESG data gaps early. Buyers will inherit your emissions reporting obligations, so audit your GHG data collection processes before closing. Ensure the purchase agreement includes rights to collect Scope 3 data from your suppliers [10]. Establishing a clear integration roadmap that prioritizes preserving the "green value proposition" can help retain key personnel and maintain deal value [16].

For carve-out deals, a Transition Services Agreement (TSA) can help ensure continued access to shared sustainability systems and emissions tracking during the handoff. If operating assets are involved, plan for a final financial reconciliation within 60–120 days post-closing to reconcile actual production revenue and costs with the estimates used at the effective date [17]. These steps build on earlier efforts to organize your financial and operational processes, setting the stage for a smoother integration.

Successfully navigating a cleantech M&A exit demands thorough and early preparation. The reality is stark: mid-market deal completion rates hover below 60% [18], and even among closed deals, 60%–70% fail to achieve projected synergies [5]. These figures highlight just how crucial disciplined groundwork is. The difference between a high-value exit and a disappointing one often boils down to how far ahead you start planning.

The 12 to 24 months before engaging an advisor are particularly critical, as this is when around 80% of your value drivers become solidified [18]. Founders who take the time to refine their financials, reduce dependency on themselves as owners, diversify their customer base, and address legal issues tend to secure better multiples than those who rush into the process unprepared.

"Buyers are acquiring the business, not the founder - and the exit preparation period is when you prove that." - Daniel Bae, Founder, Lyndon Advisory [18]

Cleantech businesses face unique challenges, such as interconnection delays, permitting hurdles, and meeting ESG standards. Tackling these issues early, as outlined in this guide, is essential. Bringing together the right team of experts - M&A counsel, tax advisors, and financial specialists like Phoenix Strategy Group - ensures these obstacles are addressed head-on, setting the stage for a smoother and more successful exit.

To set yourself up for a successful cleantech M&A exit, start planning 12 to 24 months before bringing in an advisor or kicking off a formal sell-side process. Early preparation is crucial to fine-tune key value drivers like audited financials, consistent revenue and EBITDA growth, and legal readiness. By addressing these areas ahead of time, you'll position your business to take advantage of favorable market conditions when they align with your growth stage.

When setting up a cleantech data room for buyers, it's crucial to include the right documents. Typically, these include:

Keeping these documents well-organized and up to date is critical to ensure a smooth and efficient M&A process. Buyers will expect clarity and thoroughness in every category.

Tax credits and power purchase agreements (PPAs) play a key role in increasing the valuation of cleantech deals by providing stable cash flows and long-term financial advantages. Tax credits, such as the Investment Tax Credit (ITC) and Production Tax Credit (PTC), enhance the financial appeal of projects by improving their economic feasibility. Meanwhile, long-term PPAs linked to operating assets add further value by delivering predictable and steady revenue streams over time.