Published on

February 18, 2026

The cash conversion cycle (CCC) is a critical metric for businesses aiming to grow efficiently. It measures how long cash is tied up in operations before becoming available for reinvestment. A shorter CCC means better liquidity and less reliance on external financing, while a longer CCC can strain cash flow.

Here’s how CCC is calculated and managed:

To improve CCC:

Technology and collaboration are key enablers. Automation tools, AI-driven forecasts, and real-time dashboards streamline CCC management. Cross-department coordination between sales, procurement, and finance ensures smoother operations and better cash flow.

Cash Conversion Cycle Formula and Optimization Strategies

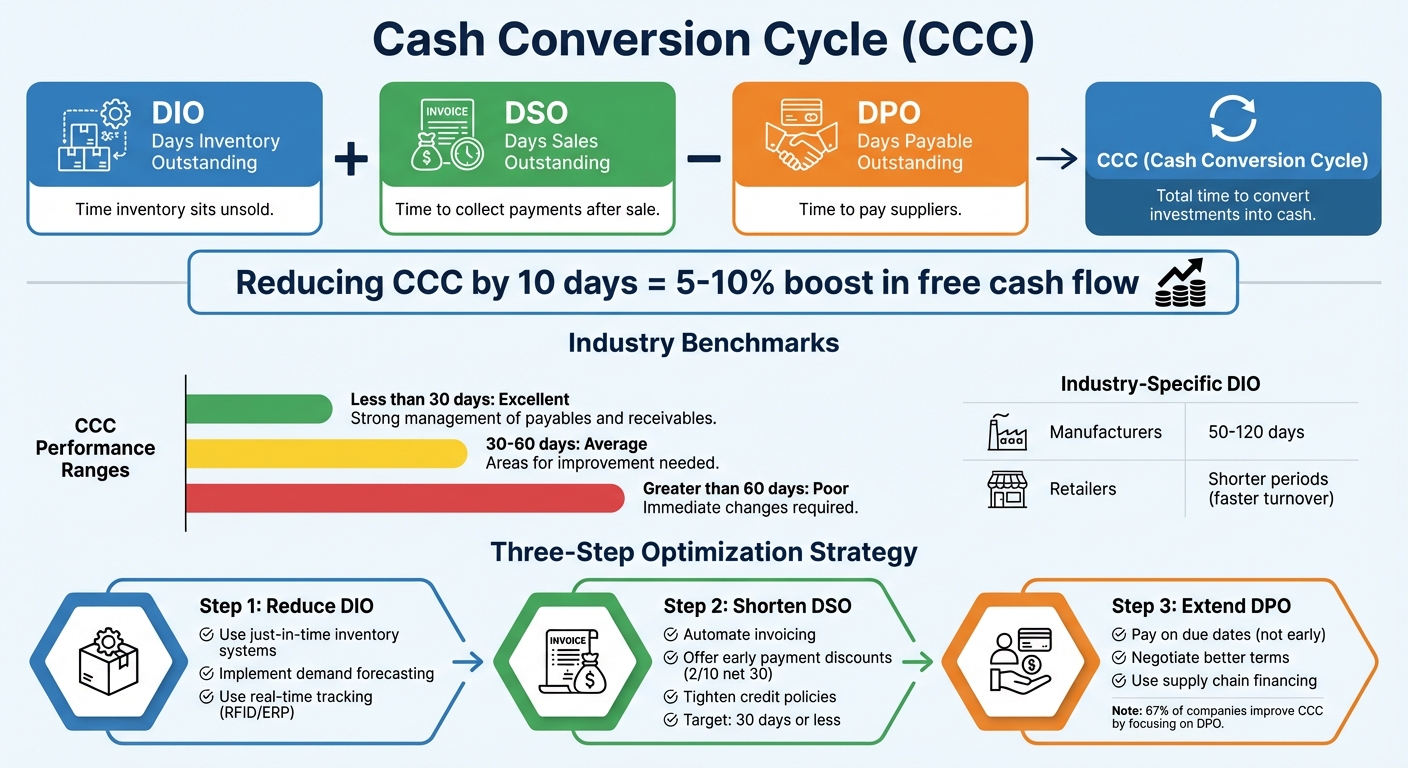

To manage your cash flow effectively, it’s important to break down the Cash Conversion Cycle (CCC) into its three key parts: Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO). Each of these reveals where cash might be tied up in your operations and helps pinpoint areas for improvement.

DIO shows how long your inventory sits on hand before being sold. The longer it remains unsold, the more cash is stuck in products that aren’t earning revenue. A lower DIO means you’re turning inventory into sales faster, which can also reduce storage costs.

For manufacturers, DIO tends to be longer - anywhere from 50 to 120 days - due to complex production processes. Retailers, on the other hand, usually move inventory more quickly, resulting in shorter DIO periods [4].

Once inventory is sold, the next challenge is collecting payment, which is where DSO comes into play.

DSO measures how long it takes to receive payment after making a sale. A longer DSO means cash is tied up for extended periods, which can slow down your ability to reinvest in the business. By reducing DSO, you can speed up cash inflows and keep operations running smoothly.

As J.P. Morgan explains:

"A shorter CCC reduces a company's external financing needs and frees cash for strategic investments" [1].

However, growth can complicate this balance. For example, during expansion, offering more flexible credit terms to attract new customers might lengthen DSO, creating a gap between delivering goods and receiving payment.

The other side of the equation involves managing how long you take to pay your suppliers, which is measured by DPO.

DPO tracks the time your company takes to settle supplier invoices. A higher DPO allows you to hold onto cash longer, using trade credit to your advantage. Studies indicate that 67% of companies improve their CCC by focusing on extending DPO [5].

But there’s a fine line. Extending DPO too much can harm supplier relationships. As the Association for Financial Professionals warns:

"While it is good for the company's own working capital position to delay payment as long as possible, it should consider the impact of delaying payment on its own supply chain" [6].

Overextending payment terms could lead to strained relationships, reduced credit terms, or even supply disruptions. Striking the right balance across all three metrics - DIO, DSO, and DPO - is critical. Research shows that reducing the overall CCC by just 10 days can result in a 5–10% boost in free cash flow [2]. This highlights how careful adjustments can significantly impact your financial health and growth potential. For many businesses, navigating these complexities requires the strategic oversight of fractional CFO services.

Improving your Cash Conversion Cycle (CCC) means focusing on its three main components: inventory, receivables, and payables. The goal isn’t to push every number to the extreme but to strike a balance that supports growth without straining your business relationships.

To free up cash tied in inventory, the first step is to align stock levels with demand. Adopting a just-in-time (JIT) inventory system can help you order goods only when needed, cutting down on storage costs and minimizing unsold stock. Combine JIT with demand forecasting tools to ensure you're ordering the right amount at the right time.

Using real-time tracking systems, like RFID tags or ERP software, gives you visibility into which items are selling quickly and which are sitting idle. Regularly reviewing your inventory turnover ratios can highlight slow-moving products. From there, you can take action - whether that’s offering discounts or liquidating outdated stock. Another option is negotiating smaller, more frequent deliveries with suppliers instead of bulk shipments. This approach keeps your DIO low without risking stockouts that might hurt customer satisfaction.

The trick is not to cut inventory so much that you can’t fulfill orders. The goal is to maintain a lean stock while still meeting customer needs. This balance ensures you have enough liquidity to support growth without compromising service.

Once your inventory is optimized, the next step is to speed up your cash collections.

Getting paid faster starts with making payments easier for your customers. Automate invoicing so bills are sent out as soon as goods or services are delivered. This gets the payment process moving right away. You can also offer early payment discounts - like 2% off for payments within 10 days - to encourage quicker settlements while maintaining customer goodwill.

Another effective approach is to use customer payment portals. These platforms let your clients view invoices and pay through their preferred methods, such as ACH or credit cards, at their convenience. Tighten credit policies upfront by thoroughly screening customers before offering them credit. This reduces the risk of late payments and minimizes the need for aggressive collections later on.

As J.P. Morgan wisely puts it:

"The aim isn't simply to delay all payments and accelerate all collections, but rather to manage cash flow in alignment with your business values and customer/supplier expectations" [7].

Additionally, streamline how you apply payments to invoices. A standard DSO target is 30 days or less [7], and reaching this benchmark can significantly improve cash flow, giving you more resources to reinvest in growth.

With collections optimized, it’s time to focus on managing supplier payments.

To improve your cash flow, schedule payments so they’re made on the due date - never earlier. Paying invoices before they’re due unnecessarily ties up funds. Automating your accounts payable process ensures payments are scheduled precisely when they’re due.

Consider negotiating dynamic discounting agreements with suppliers. This lets suppliers access early payments through a third party if needed, while you maintain or even extend your payment terms. However, only accept early payment discounts if the savings outweigh your borrowing costs. Otherwise, it’s better to hold onto your cash.

Standardizing payment terms across your business is another way to avoid inconsistencies and maximize trade credit benefits. But don’t push payment terms so far that you strain supplier relationships. Work transparently with key suppliers to establish schedules that work for both sides. Maintaining trust with your suppliers ensures stability in your supply chain, even as your business grows.

Technology can be a game-changer when it comes to managing your cash conversion cycle (CCC). While process improvements lay the groundwork, modern tools take efficiency to the next level by automating tasks and offering real-time insights.

Relying on manual spreadsheets or disconnected systems often leads to errors and delays. Tracking inventory, payments, and invoices across fragmented platforms simply can’t keep up with the needs of a growing business. That’s where advanced technology steps in to simplify and streamline the process.

Automation builds on manual optimizations, tightening your CCC even further. For example, automated receivables software can instantly send invoices as soon as goods are shipped. It also provides online portals that make it easier for customers to pay quickly using ACH or credit cards [9][5]. On the payables side, automation ensures that payments are made according to your pre-set schedules. This approach not only optimizes cash flow but also maintains healthy supplier relationships.

ERP systems enhance inventory management by automating reorder triggers and reducing idle stock [10][11]. This minimizes the amount of cash tied up in inventory and cuts down on the risk of losses from outdated or unsellable stock.

AI-powered tools take cash flow forecasting to a level that manual methods simply can’t match. These systems analyze data from ERP platforms, bank transactions, and even broader economic trends to deliver highly accurate predictions [13]. Companies that adopt AI forecasting report improvements in accuracy ranging from 20% to 30% [13].

AI also helps by performing automated variance analysis - comparing forecasts to actual outcomes and identifying the reasons for any discrepancies. Whether it’s delayed customer payments or unexpected changes in buying behavior, these insights allow you to tackle potential problems with Days Sales Outstanding (DSO) before they escalate [13]. AI can even simulate thousands of "what-if" scenarios, helping you prepare for challenges like market shifts, new product launches, or supply chain disruptions [14][15]. With these predictive insights, you can monitor every aspect of your CCC in real time.

Dashboards are another powerful tool for CCC management, offering a consolidated view of key metrics like Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payable Outstanding (DPO). Unlike spreadsheets, which can quickly become outdated, real-time dashboards ensure decisions are based on the latest data [2][3].

For example, Kyriba users report a consistent 6-day improvement in their CCC by using automated liquidity solutions [11]. These platforms integrate directly with ERP systems and bank accounts, creating a single, reliable source for cash visibility [8]. Dashboards can also include automated alerts, flagging issues like customers nearing their credit limits or overdue invoices [16]. This allows your team to address potential cash flow problems proactively.

Tracking trends over time is just as important as monitoring individual metrics. A shrinking CCC quarter over quarter can indicate improving efficiency and financial health [8].

| CCC Performance Range | Interpretation & Action |

|---|---|

| Less than 30 days | Excellent; suggests strong management of payables and receivables [3]. |

| 30 – 60 days | Average; indicates areas for improvement in managing inventory and capital [3]. |

| Greater than 60 days | Poor; immediate changes to working capital strategies are needed [3]. |

For growing companies, leveraging these tools - possibly with guidance from experts like Phoenix Strategy Group - can help maintain financial agility while scaling operations. With the right technology in place, you’ll be better equipped to adapt to challenges and seize new opportunities.

To truly optimize the cash conversion cycle (CCC), technology alone isn't enough. Without effective collaboration across departments like procurement, sales, and finance, inefficiencies can persist, leading to missed opportunities to free up capital and improve cash flow. When these teams work in silos, it can result in misaligned payment terms, inconsistent credit policies, and unnecessary bottlenecks.

In industries where capital requirements are high, the gap in Days Payable Outstanding (DPO) between top performers and median performers can range from 25 to 40 days [18]. That gap represents a massive amount of capital that could be redirected to fuel growth. Here’s how better alignment between departments can unlock that potential.

Procurement and finance teams need to move beyond their traditional roles of processing purchase orders and invoices. By integrating procurement data with finance master data through Budget-to-Pay (B2P) systems, these teams can track every purchase request against budget lines, helping to identify necessary expenditures versus wasteful spending [17].

A key step in this process is spend segmentation. Suppliers can be grouped into three tiers:

Each tier requires a tailored payment strategy. For instance, strategic suppliers can benefit from supply chain finance programs, allowing them to receive early payments at a lower cost of funds. Meanwhile, transactional suppliers might be assigned longer standard payment terms.

To ensure fairness and avoid favoritism, procurement should create supplier matrices that are validated by operations, quality, and finance teams. Any changes to standard payment terms should require CFO approval through a term-exception registry [18].

One Fortune 200 manufacturer adopted this collaborative approach, unlocking $30 million in cash flow by offering supply chain finance to strategic suppliers. They also saved an additional $15 million through dynamic discounting for smaller vendors. By providing flexible options rather than imposing blanket term extensions, they achieved a 63% supplier adoption rate [12].

Even small operational tweaks can make a big difference. For example, setting the invoice date as the goods-receipt date plus one day and consolidating payment runs to fixed days each month can reduce delays and avoid the need for difficult supplier negotiations [18].

Just as procurement and finance must work together, sales and finance need to collaborate to speed up cash collection. Sales teams often focus on closing deals, but without proper coordination, they may offer overly generous payment terms that create extended receivables and strain working capital.

To address this, billing should begin immediately after a deal is finalized, avoiding unnecessary delays between service delivery and invoice issuance [19]. Simplifying invoice layouts to include only essential information can also prevent confusion and speed up payment processing [5][19].

Finance can support sales by sharing customer payment histories. This allows sales teams to offer tiered credit terms, rewarding reliable payers with better terms or faster delivery while requiring deposits from customers with inconsistent payment patterns [5]. Automated accounts receivable tools can help maintain consistent follow-ups, ensuring positive customer relationships while keeping payments on track [5]. Since the chances of recovering overdue receivables decrease over time, finance should monitor unpaid bills closely and alert sales for timely intervention [19].

"Every dollar held inside receivables is a hostage; every dollar paid out early to suppliers is a gift." - Umbrex [18]

For companies in growth stages, working with advisors like Phoenix Strategy Group can help establish processes that keep procurement, sales, and finance aligned as the business scales.

Optimizing your cash conversion cycle (CCC) isn’t just about crunching numbers - it’s about unlocking the cash flow needed to grow your business. By adopting strategies like just-in-time inventory management to lower Days Inventory Outstanding (DIO), offering incentives like a 2/10 net 30 discount to speed up Days Sales Outstanding (DSO), and negotiating better terms with suppliers to extend Days Payable Outstanding (DPO), you can create a more efficient liquidity engine. A shorter CCC means less dependence on external financing and more room for self-sustained growth. In fact, the J.P. Morgan Working Capital Index 2020 revealed that 53% of companies that reduced their CCC achieved 67% of their gains through improvements in DPO alone [20].

Technology takes these efforts to the next level. Automated invoicing, AI-driven cash flow predictions, and real-time dashboards help identify and address bottlenecks. However, the real magic happens when procurement, sales, and finance teams work together - segmenting suppliers, aligning payment terms with customer collections, and sharing data to streamline operations.

Businesses that combine these approaches have managed to cut their CCC by over 20 days in just one quarter [21]. For companies in growth stages, this can mean having extra working capital to invest in hiring, infrastructure, or expansion - without relying on costly credit lines or external funding.

As your business scales, managing cash flow becomes more challenging. Partnering with advisors like Phoenix Strategy Group can help you establish systems to maintain a healthy CCC, even during periods of rapid growth, fundraising, or preparing for an exit. Keep tracking your metrics, compare your performance to industry benchmarks, and fine-tune your strategies as you grow.

A "good" cash conversion cycle (CCC) can look very different depending on your industry. For instance, in sectors like retail and manufacturing, businesses often target a range of 30 to 60 days. On the other hand, service-based industries typically have shorter cycles since they deal with little to no inventory.

If you're looking to improve your CCC, start by comparing your numbers to the typical benchmarks in your field. From there, focus on practical steps like better inventory management, negotiating more favorable payment terms with suppliers, and speeding up receivables. In general, a shorter CCC reflects stronger cash flow management and a more efficient operation.

The best starting point - whether it's DIO (Days Inventory Outstanding), DSO (Days Sales Outstanding), or DPO (Days Payable Outstanding) - hinges on your immediate cash flow needs. Focus on the area creating the most pressure on your cash:

The key is to prioritize adjustments that bring the quickest improvement to your cash flow.

To stretch your Days Payable Outstanding (DPO) without straining relationships with suppliers, it’s all about strategy and balance. Start by categorizing your suppliers into tiers - strategic, leverage, and transactional. This segmentation helps you customize your negotiation tactics based on each supplier’s role and importance to your business.

Approach these discussions with an emphasis on shared benefits, open communication, and maintaining trust. For instance, you can explore options like supply chain finance programs or dynamic discounting. These tools allow you to extend payment terms while giving suppliers the chance to receive early payments if they need quicker cash flow. It’s a win-win: you improve your cash flow, and they maintain financial flexibility.