Published on

February 18, 2026

If you’re negotiating equity clawback provisions, it’s essential to protect your ownership and avoid unnecessary risks. Clawbacks let companies or investors reclaim shares if performance targets aren’t met or misconduct occurs. Poorly structured agreements can lead to disputes, diluted ownership, and loss of control in your company. Here’s a quick breakdown of how to approach these negotiations effectively:

5 Key Steps for Negotiating Equity Clawback Provisions

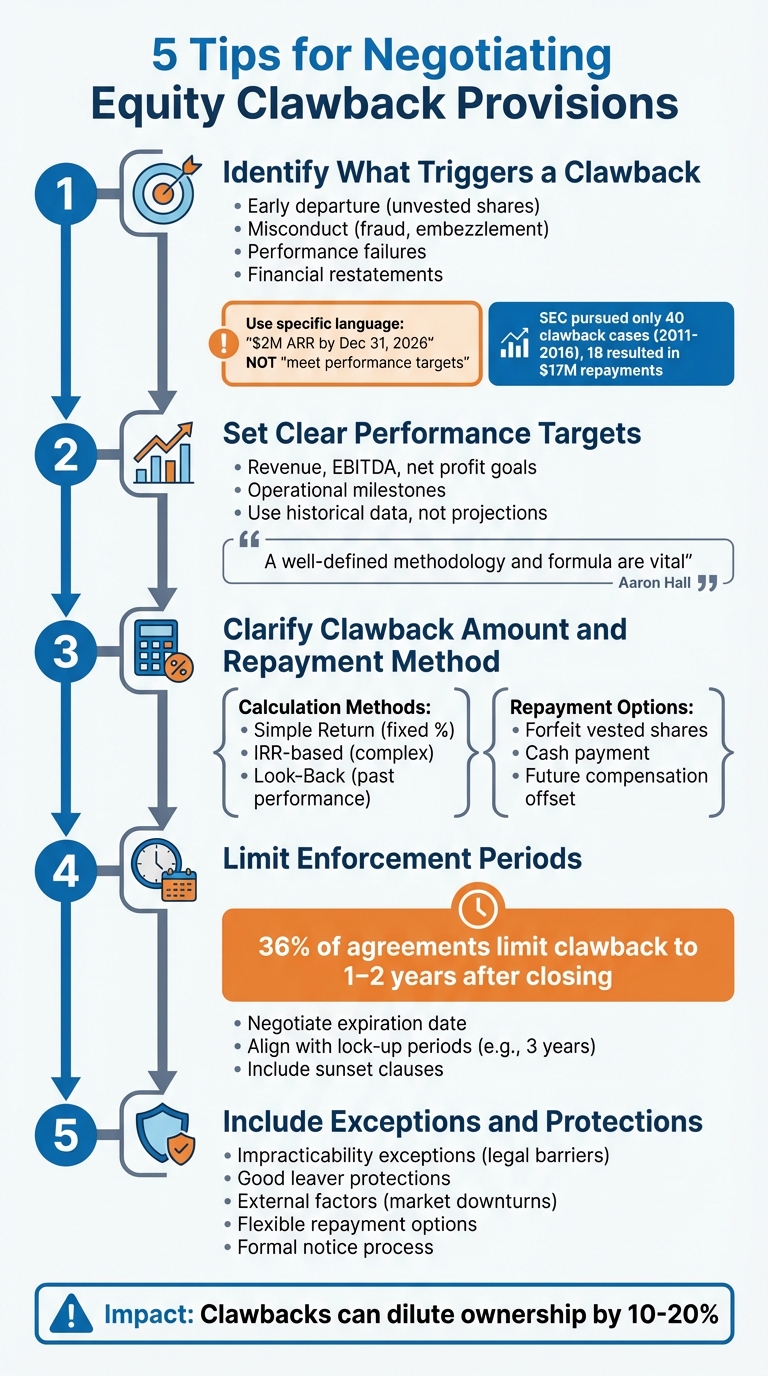

Pinpointing the specific events that can trigger a clawback is crucial. Without clear definitions, you open the door to disputes that can drain your time, money, and equity.

One of the most common triggers is an early departure. For example, leaving a company before fully vesting - often structured on a four-year schedule with a one-year cliff - can result in the repurchase of unvested shares at cost or par value [1]. Other triggers might include misconduct (like fraud, embezzlement, or criminal convictions), breaches of contract (such as violating non-compete clauses or employment terms), failure to meet performance benchmarks (like missing revenue or product milestones), financial restatements (if equity was awarded based on incorrect financial data), and regulatory violations [1]. To avoid future disputes, push for clearly defined, objective benchmarks instead of vague descriptions.

For instance, instead of using broad terms like "failure to meet performance targets", specify something measurable, such as "failure to achieve $2,000,000 in annual recurring revenue by December 31, 2026" [1]. Similarly, avoid ambiguous terms like "unethical behavior" when defining misconduct. Use precise language, such as "conviction of a felony" or "proven embezzlement."

Many agreements also differentiate between “Good Leavers” and “Bad Leavers.” Good Leavers - those who leave due to death, disability, or unfair dismissal - typically keep their vested shares and might even receive fair market value for unvested ones. On the other hand, Bad Leavers - those who resign voluntarily or are terminated for cause - often lose their unvested shares and may need to sell vested shares at the lower of cost or fair market value [5].

Between 2011 and 2016, the SEC pursued just 40 clawback cases against top executives, with only 18 resulting in repayments totaling $17,000,000 [5]. While these cases represent a small percentage of deals, the impact of enforced clawbacks can be significant, often diluting ownership by 10% to 20% [1]. To protect your interests, negotiate triggers that are specific, measurable, and fair from the outset. This clarity not only reduces ambiguity but also sets the stage for fair performance targets in subsequent negotiations.

Once you've identified the triggers for clawbacks, the next step is to establish specific and measurable performance benchmarks. Vague or ambiguous targets can lead to disputes and potentially unfair enforcement. Clear benchmarks not only help define clawback amounts but also streamline enforcement timelines during future negotiations.

Some commonly used metrics include revenue targets, EBITDA, and net profit goals. Operational milestones, like rolling out a new product feature or securing a regulatory license, also work well as concrete targets. Avoid general statements like "achieve profitability"; instead, set precise financial goals tied to specific deadlines.

"A well-defined methodology and formula are vital to facilitate accurate and fair determinations." – Aaron Hall [1]

When setting these targets, rely on historical performance data rather than overly optimistic projections. For example, if past revenue growth has been modest, it wouldn’t make sense to set an aggressive target without a clear plan for market expansion or additional funding. Also, consider external factors that could impact performance but shouldn’t automatically trigger clawbacks. Building in a reasonable buffer for minor variances ensures clawbacks only apply when there’s a significant shortfall in performance.

Transparency is key. Establish clear reporting protocols from the start. Decide on the accounting standards to be followed (e.g., GAAP), the frequency of performance reporting, and who will verify the data. Including audit rights in your agreement adds an extra layer of fairness, ensuring metrics are measured consistently and disputes over accounting practices are minimized.

Once you’ve set the triggers and performance targets, the next step is to define how much equity will be recovered and how the repayment process will work. Vague terms can lead to financial difficulties and unnecessary equity loss, so clarity is critical.

Start by outlining the calculation method. Some commonly used formulas include:

Each approach carries unique implications. For instance, while Simple Return is easier to calculate, IRR-based formulas offer a more nuanced view of financial performance. Be specific about which formula will be used and how it will be calculated to avoid confusion or disputes later on [1].

Next, address the repayment method. Will repayment involve forfeiting vested shares, returning already exercised stock, or making a cash payment equivalent to the value of the shares? Each option comes with distinct tax and liquidity implications. The SEC has noted that clawbacks don’t necessarily require recovery from the original equity grant, as assets are considered "fungible" [6]. Companies can also offset clawbacks against future bonuses, cancel unvested awards, or withhold deferred compensation. Opting for future compensation offsets rather than immediate cash repayment can ease the financial burden, especially during market downturns.

"The executive officer may not have the funds available or wish to sell existing stock holdings to pay back the amount due - each of which could create unpleasant economic or tax hardships." – Steve Seelig, Senior Director, WTW [6]

Clear repayment terms can help avoid unnecessary conflict. Include a clause requiring the board to notify you and discuss the proposed recovery method before finalizing it. This allows you to negotiate a repayment plan that aligns with your financial situation. Additionally, consider tax implications upfront - repaying the gross value of previously taxed equity can lead to significant losses if you’re unable to recover taxes already paid [6].

Leaving clawback provisions open-ended can create uncertainty, as they could theoretically remain in effect forever. To avoid this, it’s important to negotiate a specific expiration date for clawback rights, often referred to as a statute of repose. This ensures clarity about when your equity is fully secured and prevents investors from reclaiming shares long after the deal is finalized.

When combined with clearly defined triggers and repayment methods, a fixed timeframe strengthens transparency. In fact, 36% of secondary market agreements limit clawback liability to just one or two years after closing [8].

"The most common limitation would be to agree that the seller is only liable for recalls of distributions within a certain time period, typically one to two years after closing."

For added consistency, you might align clawback periods with related contractual terms, such as a three-year lock-up period [7]. Another option is to negotiate sunset clauses, which explicitly state when the company’s right to reclaim shares will expire [1].

Steer clear of undated clawback agreements, as they can lead to legal uncertainty and may even be viewed as unfair by the courts [4]. Setting clear time limits not only safeguards your legal position but also fosters the stability needed for long-term partnerships. Up next, learn how to negotiate exceptions and protections to further secure your equity.

Even the strictest clawback provisions can feel unfair when external factors are ignored. That’s why it’s crucial to negotiate exceptions and safe harbor clauses to shield yourself from unjust claims.

Start by requesting impracticability exceptions. These come into play when legal barriers - like ERISA regulations or local labor laws - or excessive recovery costs make clawbacks unreasonable. You can also tailor "good leaver" protections to address specific situations, such as adjustments for events like death, disability, or wrongful termination. Additionally, ensure that external factors like economic downturns or regulatory shifts aren’t treated as defaults that automatically trigger clawbacks [1][3][6]. Once these exceptions are in place, shift your focus to crafting flexible repayment terms.

Flexible repayment options can make a big difference. Instead of requiring an immediate return of cash or stock, explore alternatives like offsetting future bonuses, dividends, or unvested awards. The Securities and Exchange Commission (SEC) supports this approach, stating:

"The rules do not prevent an issuer from securing recovery through means that are appropriate based on the particular facts and circumstances of each executive officer that owes a recoverable amount"

- SEC [6]

To further protect yourself, formalize a process for reviewing clawback actions before they’re enforced.

Establish a formal notice process that gives you the opportunity to review recovery calculations and propose alternative repayment methods. As WTW advises:

"policies create a forum for executive officers and the board to discuss the recoupment action being proposed... This process would be less adversarial"

- WTW [6]

For added fairness, consider involving an independent third party to verify clawback calculations. This level of oversight is often managed by fractional CFO services to ensure objective financial reporting. Finally, include language that allows the board’s compensation committee to use discretion, ensuring each case is reviewed individually rather than triggering automatic clawbacks [6].

Equity clawback provisions can have a direct and significant effect on your ownership and control of your company. For instance, if a clawback reclaims 20% of your equity, your ownership stake drops by the same amount, potentially altering board dynamics and shifting voting power[1]. To protect your interests, it’s essential to establish clear triggers, realistic performance benchmarks, and fair repayment terms. This approach helps safeguard both your equity and the overall balance of control within your company.

Striking the right balance between investor protections and founder safeguards is key. Clear and well-defined terms prevent misunderstandings that could lead to disputes, damage reputations, or even result in costly litigation[2]. By setting specific triggers, achievable performance targets, fair valuation methods, and reasonable timeframes, you create a framework that protects both parties and reduces the risk of conflict.

Because of the complex nature of clawback provisions, it’s wise to consult experienced advisors during negotiations. The nuances of calculation methods, board dynamics, and legal considerations often require expert guidance. Working with advisors like Phoenix Strategy Group can provide the strategic support you need. Their expertise in fractional CFO services and M&A advisory can help you reduce dilution risks while maintaining strong, collaborative relationships with your investors.

To identify unclear clawback language, keep an eye out for phrases like "as soon as possible," "reasonable efforts," or "at the discretion of the company." These terms often fail to specify exact triggers, deadlines, or criteria, which can make enforcement tricky. Instead, provisions should explicitly outline triggering events, set clear timeframes, and detail calculation methods. Consulting with legal counsel is a smart move to ensure the terms are both precise and enforceable.

The most balanced clawback performance targets focus on metrics that represent a company’s long-term success and align everyone’s interests. Popular choices include financial indicators like revenue, EBITDA, or net income, as these are quantifiable and directly tied to the company’s performance. Tools like high-water marks and hurdle rates are also useful - they ensure clawbacks are triggered only in cases of true underperformance, steering clear of penalizing short-term fluctuations.

To reduce the tax burden of a clawback, it's a good idea to work with a tax professional who can assess your unique circumstances. They might suggest strategies like adjusting the timing of when you recognize gains or losses or structuring the clawback in a way that minimizes taxable events. Since tax rules can differ depending on the type of clawback and your location, expert advice is crucial.