Published on

June 26, 2026

If you transfer shares to a CRT before a sale is locked in, the trust can sell without an immediate capital gains tax at the trust level. That can keep more money invested after closing, but you trade that for less upfront liquidity, annual payouts instead of full access to cash, and an irrevocable gift to charity.

Here’s the short version:

A quick way I’d frame it: a CRT is not a way to avoid tax. It’s a way to change when tax shows up, how cash comes back to you, and where the remainder goes.

| Issue | Direct Sale | CRT Sale |

|---|---|---|

| Tax at closing | Capital gains tax due right away | No immediate capital gains tax at trust level |

| Cash access | After-tax proceeds available at once | Paid out over time |

| Reinvestment amount | Net after tax | Gross sale proceeds inside trust |

| Charity | Optional separate gift | Required remainder gift |

| Timing risk | Low | High if transfer is too late |

If I were reviewing this before a founder exit, I’d focus on four things first: timing, payout design, deduction limits, and whether giving up principal fits the plan.

CRT vs. Direct Sale: Founder Exit Tax Strategy Comparison

A Charitable Remainder Trust (CRT) is an irrevocable split-interest trust under IRC § 664. It pays income to a noncharitable beneficiary for a set term or for life, and then the remainder goes to charity[5][8]. For founders, that setup changes three big things: how sale proceeds are handled, when taxes are paid, and what cash flow looks like after the exit.

To qualify, a CRT must pay 5% to 50% of the trust’s value each year. The charitable remainder also needs a present value of at least 10% of the initial contribution[5][8].

Founders usually compare two main options.

A Charitable Remainder Unitrust (CRUT) pays a fixed percentage of the trust’s assets, revalued each year. If the trust grows, the dollar payout can grow too. A Charitable Remainder Annuity Trust (CRAT) pays a fixed dollar amount set when the trust is created, and that amount does not change.

| Feature | CRUT | CRAT |

|---|---|---|

| Payout | Fixed % of annual asset value | Fixed dollar amount set at creation |

| Payment stability | Variable; moves with portfolio | Constant; predictable year-to-year |

| Inflation protection | High; payments grow if assets appreciate | None; fixed payments lose purchasing power |

| Additional contributions | Permitted after the trust is established | Not allowed after creation |

| Risk of depletion | Low; payments scale down if trust shrinks | Higher; fixed payments can deplete the trust |

| Founder fit | Best for long-term growth and flexibility | Best for a specific, guaranteed income stream |

That choice matters more than it may seem at first glance. A higher-growth founder may lean toward a CRUT because the payout can move with the portfolio. Someone who wants a set income amount each year may prefer a CRAT. The tradeoff is simple: more payment certainty on one side, more flexibility on the other.

Payout design also affects the charitable deduction. For private company stock, a Flip CRUT can begin as a net income trust and switch after the sale[5][6].

The founder contributes the assets. The income beneficiary gets the payments. The charity receives what is left at the end. The trustee runs the trust and handles administration[4][5].

If the trust holds illiquid assets, such as private company stock, an independent appraiser should value those assets[6]. That step matters because the numbers used at funding can shape both compliance and tax results.

Payout terms can shift the whole math of the plan. Higher payout rates mean more annual cash flow, but they also reduce the charitable deduction and increase the risk that the trust runs down too far. Longer terms can mean more total income over time, but they also make weak investment performance more painful.

That’s why small changes here can have a big effect later. A founder isn’t just picking a percentage. They’re setting the balance between income now, tax timing, and what eventually goes to charity.

With the structure in place, the next issue is how funding and sale timing shape the tax result.

A CRT is tax-exempt under IRC § 664(c). That means it can sell contributed shares without paying capital gains tax at the trust level. But the tax doesn't just vanish. It's deferred and then picked up as distributions go out to the beneficiary [5][1].

With a CRT, timing can make or break the tax result.

The shares need to go into the trust before any binding sale obligation exists. A nonbinding LOI can still work, but only if there is real closing risk left. If the deal is basically done, the IRS can treat the gain as the founder's under the anticipatory assignment of income doctrine [6][2].

Ferguson v. Commissioner is the case people point to here. It shows the risk in plain terms: once a sale becomes a practical certainty, the IRS can tax the gain to the contributor [6][5].

The founder may also get an income tax deduction based on the actuarial present value of the charitable remainder interest [5][9]. That value is calculated using the IRS § 7520 rate, which was 4.6% as of March 2026 [3]. If the asset is appreciated capital-gain property, the deduction is usually capped at 30% of adjusted gross income, with a 5-year carryforward [5][10].

Private company stock adds one more step. It needs a qualified independent appraisal completed within the IRS timing window. In Estate of Hoensheid, the Tax Court threw out a $3.2 million deduction because the donor used a financial advisor instead of a qualified appraiser [6].

Once the trust is funded, the trustee needs to handle the sale on their own.

The basic flow is simple: the founder transfers shares to the trust, the trustee sells them, and the trust reinvests the full sale proceeds. On paper and in practice, the trustee, not the founder, is the seller of record.

For illiquid private stock, a Flip CRUT is often the better fit. It can work as a net-income trust while the stock is still illiquid, then switch to a standard percentage payout after the sale closes [5][6].

After the sale, the next piece is the tax treatment of the trust payouts.

CRT distributions follow tier ordering rules. In many cases, early distributions are taxed as capital gains first. The system uses a worst-in, first-out (WIFO) rule under IRC § 664(b) [3][5].

| Tier | Income Type | Tax Treatment |

|---|---|---|

| 1 | Ordinary income (interest, nonqualified dividends) | Taxed as ordinary income |

| 2 | Capital gains from the business sale | Taxed as capital gain income |

| 3 | Tax-exempt income (for example, municipal bond interest) | Tax-free to the beneficiary |

| 4 | Return of corpus | Tax-free |

The trustee has a few core jobs after funding:

Once the trust and tax rules are clear, the next step is simple: run the numbers. The point is to compare after-tax proceeds and cash flow using the same assumptions on both sides.

Start with the basics. You need the sale price, your cost basis, your combined federal and state capital gains tax rate, trust setup and admin costs, your payout rate, the trust term or life expectancy, expected portfolio returns, and the IRS § 7520 rate.

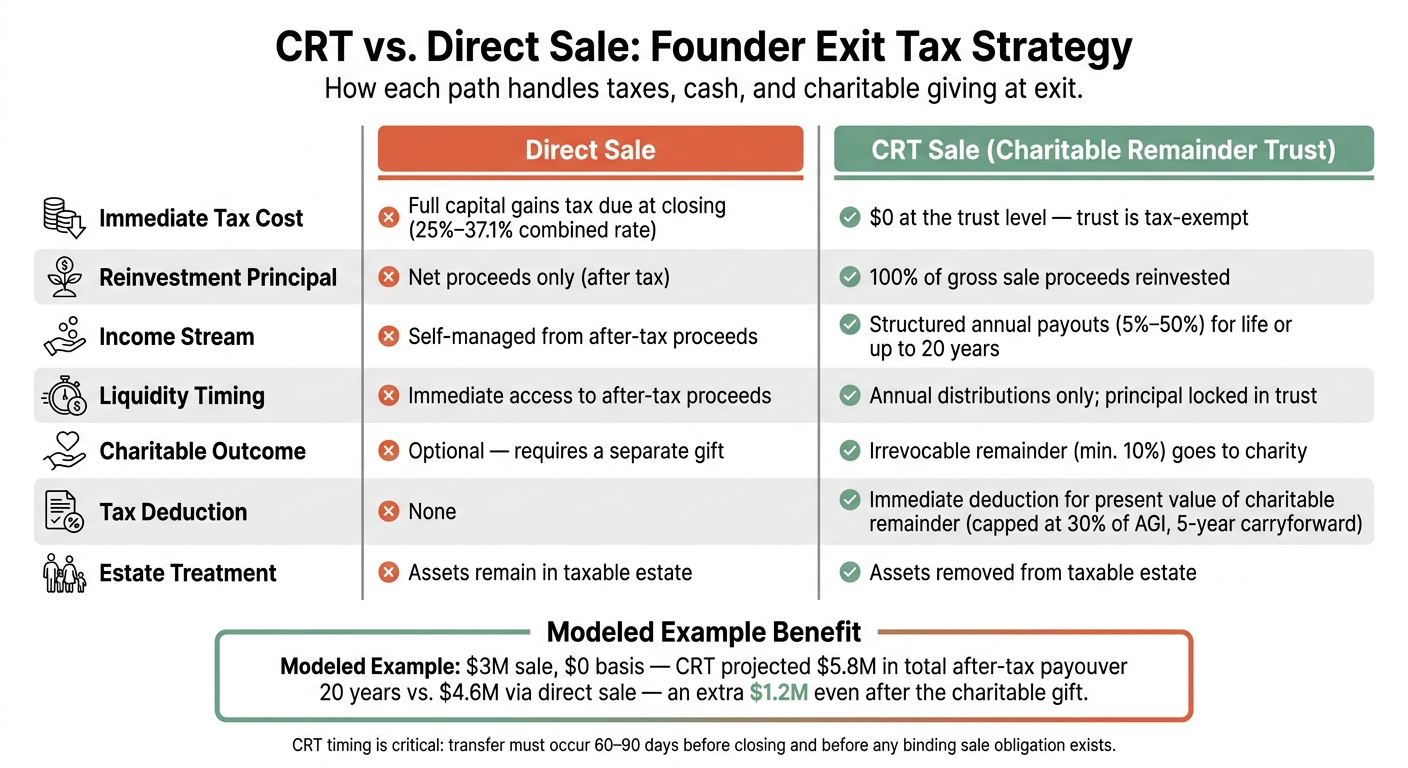

| Feature | Direct Sale | CRT Sale |

|---|---|---|

| Immediate tax cost | Full capital gains tax due at closing | $0 at the trust level; the trust is tax-exempt [5] |

| Reinvestment principal | Net proceeds only after tax | 100% of gross sale proceeds reinvested [5] |

| Income stream | Self-managed from net proceeds | Structured annual payouts of 5% to 50% for life or up to 20 years [5][3] |

| Charitable outcome | None, unless you make a separate gift | Irrevocable remainder of at least 10% to charity [5][3] |

| Tax deduction | None | Immediate deduction for the present value of the charitable remainder [5] |

| Liquidity timing | Immediate access to after-tax proceeds | Annual distributions only; principal stays in the trust [5][3] |

| Estate treatment | Assets remain in your taxable estate | Assets are removed from your taxable estate [4] |

A simple model shows how those trade-offs can play out over time. In a modeled $3,000,000 secondary sale with a $0 basis, a founder using a 20-year NIMCRUT received an immediate $300,000 tax deduction and deferred $1,080,000 in taxes that otherwise would have been due at closing. Over 20 years, the CRT projected $5,800,000 in total after-tax payouts, compared with $4,600,000 in a standard taxable account - an extra $1,200,000 even after the charitable gift [7].

That’s the part founders need to pressure-test. A result like that can look great on paper, but it only means something when you run it against your own hold period, tax rate, and cash needs.

A CRT is not the right fit for every exit. Direct sale can win when immediate liquidity, inheritance goals, or UBIT risk matter more than tax deferral.

The model has to use the same assumptions on both sides. If the inputs shift, the comparison stops being useful.

At a minimum, the model should reflect:

In practice, that means modeling CRT proceeds against direct-sale net proceeds with the same payout, return, tax, and cost assumptions. No moving the goalposts.

The model only works if the founder’s liquidity, tax, and estate goals line up with the trust structure.

After you run the numbers, the next step is simpler to say than to do: figure out whether the CRT fits the asset, the deal timeline, and the founder's goals.

A CRT often works best for founders who hold low-basis assets, have a real charitable goal, and can live with less cash up front in exchange for income paid over time. In plain English, this is usually a fit when staged income matters more than immediate liquidity.

That said, fit isn't just about the math. Execution matters too, especially the timing of the transfer and the type of asset going into the trust.

Timing can make or break the plan. The trust needs to be funded before any binding sale exists. If not, the gain may still be taxed to the founder. In Estate of Hoensheid v. Commissioner (T.C. Memo. 2023-34), the Tax Court disallowed the charitable deduction after the sale was already a practical certainty [6].

Two other trouble spots come up again and again:

A CRT is a trade. You defer taxes and set up income over time, but you give up control through an irrevocable charitable commitment and accept less immediate liquidity. The decision usually turns on four things: asset appreciation, charitable intent, income needs, and deal timing [4][5].

If the asset qualifies, the timing is clean, and the charitable goal is real, a CRT is worth modeling before closing.

No. A Charitable Remainder Trust is not the right fit for every founder exit.

It tends to make the most sense for owners with highly appreciated equity who want steady long-term income instead of a lump-sum payout and who also have genuine charitable intent.

There’s a catch, of course: part of the assets must eventually go to charity. So this isn’t just a tax move or a deal trick. Founders should work with an advisory team to model the tax, legal, and valuation outcomes before making a decision.

Set up your Charitable Remainder Trust and move your business equity into it before you sign any binding sale papers, such as a letter of intent or term sheet.

That timing matters. If you wait too long, the IRS may apply the assignment of income doctrine and treat the sale proceeds as your income, which means you could owe tax in your own name.

Once a letter of intent is signed, the legal review gets tighter. So it’s smart to coordinate early with your M&A counsel.

You also give up the residual value of any assets you move into the CRT. When the trust term ends, or when you pass away, those assets must go to the charity you named, not to your heirs.

And because a CRT is irrevocable, you no longer own those assets directly. That’s the trade-off. Many founders deal with it through a wealth-replacement plan, often using life insurance.