Published on

June 26, 2026

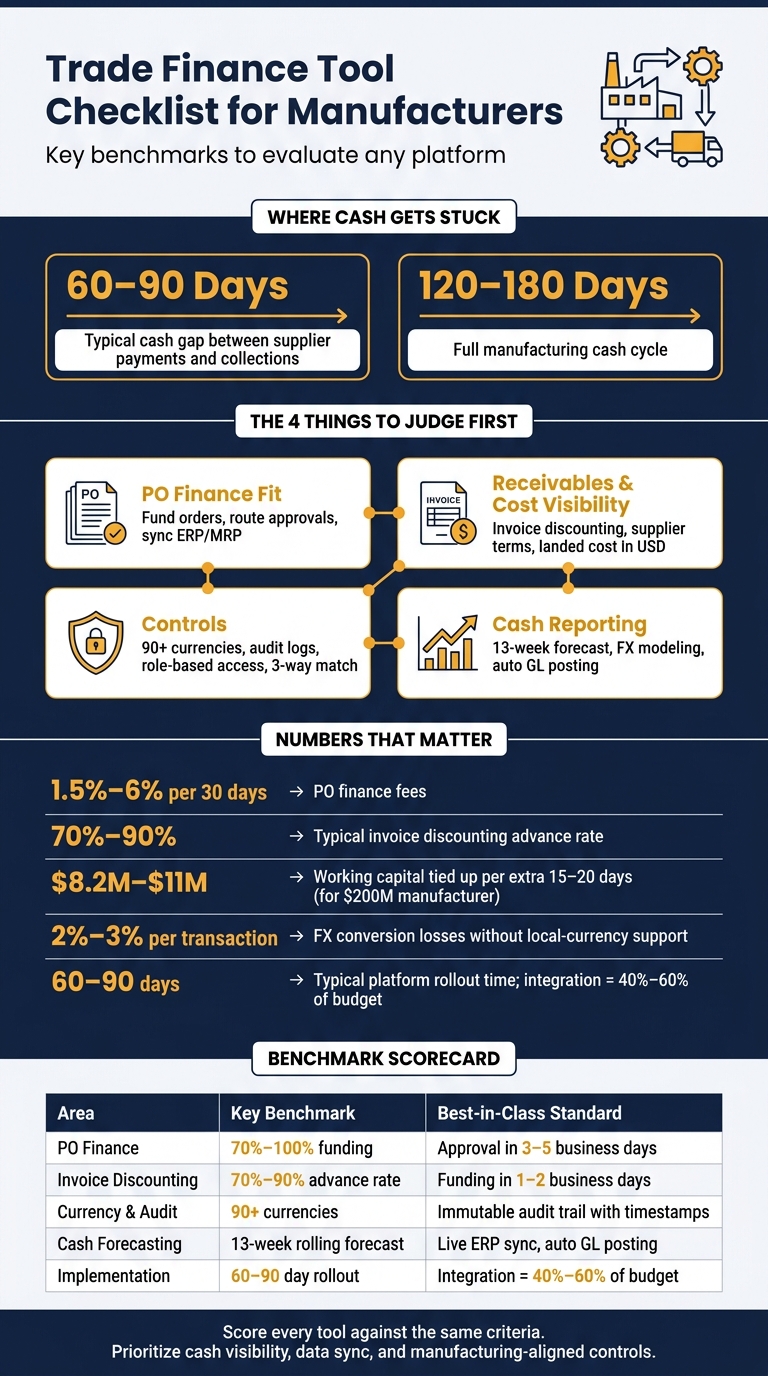

If I were picking a trade finance tool, I’d start with one question: where is cash getting stuck? For most manufacturers, the answer sits somewhere between supplier payments, inventory, and customer collections - and that gap can run 60 to 90 days, while the full cycle can stretch to 120 to 180 days.

Here’s the short version: I’d judge any tool on four things first:

A few numbers matter right away:

The main takeaway: I wouldn’t pick a platform based on transaction processing alone. I’d put more weight on cash visibility, data sync, and controls that match how manufacturing timing works.

Trade Finance Tool Checklist: Key Benchmarks for Manufacturers

| Area | What I’d check first | Key benchmark |

|---|---|---|

| PO finance | Funding %, approval flow, ERP/MRP sync, 3-way match | 70%–100% funding; 3–10 business days approval |

| Invoice discounting | Eligibility rules, borrowing base, collections control | 70%–90% advance; funding in 1–2 business days |

| Supplier terms & landed cost | Net term modeling, tariff/duty/freight breakout | Per-unit landed cost in USD |

| Currency & audit | Local-currency pay, FX rate logs, immutable audit trail | 90+ currencies; full event timestamps |

| Cash flow & FP&A | 13-week forecast, scenarios, GL posting | Forecast updates from live ERP data |

If I were using this checklist, I’d score each tool against the same points and rule out anything that can’t connect funding, controls, and forecasting in one workflow.

Use this checklist to see whether a tool can handle PO finance from intake through repayment. The focus here is simple: intake, approvals, funding terms, and system sync.

Start with PO intake. The tool should support digital upload, API, and EDI, with direct ERP connectivity so your team doesn't have to re-enter data by hand. When a platform connects straight to ERPs like NetSuite, Epicor, or Microsoft Dynamics 365, production data and financing data stay in step [6][9].

Approval routing matters just as much. You want multi-level conditional approval paths tied to dollar thresholds, so large funded orders don't sit in limbo waiting on one person. After approval, the next need is real-time status tracking from supplier payment to shipment release, plus milestone alerts that line up with U.S. business hours even if the supplier is overseas [6][3].

The main checkpoints to track are:

There's also a very practical issue here: about 50% of PO lines change after they're issued [6]. If a tool only records the first version of the PO and misses later changes, your exposure data can be off by the time the goods ship.

On the funding side, get clear on what the platform will advance and what that advance will cost. Most PO finance setups pay 100% of the supplier's invoice straight to the supplier, often by wire or Letter of Credit. But some providers only advance 70% to 90%, which means you have to fund the rest yourself [10][3]. Fees usually fall between 1.5% and 6% per 30 days, with lower pricing on larger deals [3].

Repayment comes from customer payment, so the financing cost has to fit inside your gross margin. A common rule of thumb is 20% to 25% gross margin for PO financing to make sense from a cost standpoint [10][3].

System sync is another area where details matter. A one-way pull can leave finance and production looking at different records. Ask for bidirectional API sync with your ERP or MRP system, not just a one-way data export.

Use this table to score tools on the same criteria before you build a shortlist:

| Evaluation Criteria | Minimum Requirement | Best-in-Class Standard |

|---|---|---|

| Typical Minimum PO Size | $25,000–$50,000 [3] | No minimum (specialty providers) [3] |

| Typical Funding Percentage | 70%–90% of supplier invoice amount [3] | 100% of supplier invoice amount [10][3] |

| Accepted Document Inputs | PDF upload [6] | API, EDI, OCR-parsed PDF, and email parsing [6] |

| Approval Time | 5–10 business days [3] | 3–5 business days [3] |

| ERP/MRP Integration Depth | CSV/manual export [6] | Native bidirectional API (SAP, NetSuite, MS Dynamics, Epicor, Infor) [6] |

| 3-Way Matching | 2-way (PO to invoice) [8][10] | 3-way (PO, goods receipt, and invoice) [6][8] |

| Required Gross Margin | 20%–25% minimum [10][3] | Varies by deal |

Once PO finance checks out, move to invoice discounting and supplier-term controls to test the rest of the working-capital cycle.

Margin pressure in manufacturing doesn't come from just one place. It shows up in receivables, payment terms, freight, duties, and tariffs. If a tool handles only financing or only cost tracking, your team still ends up stitching things together by hand. What you want is one connected view of receivables financing and supply-chain cost drivers.

Start with the receivables engine. You need a real-time eligibility engine, not a basic approval workflow. The platform should pull in ledger data as it changes, apply exclusion rules for overdue, concentrated, or disputed invoices, and recalculate the borrowing base as credits, returns, and other adjustments come in [11]. It should also track invoice status from digital submission through net-proceeds calculation [11].

Advance rates for invoice discounting usually fall between 70% and 90% of eligible receivables [11][12]. Check that the tool supports multi-currency invoices, USD reporting, and a clear view of net proceeds. It should also support confidential invoice discounting, where you keep control of collections and customers are not told about the financing arrangement [11].

With receivables controls in place, the next step is simple: see whether the tool can model supplier terms and show what they do to cash.

Receivables are only part of the picture. The same tool should show how supplier terms and landed cost shape margin.

Model the cash effect of supplier terms inside the platform. Tie terms to each order and test shifts like Net 30 to Net 60. For a $200 million manufacturer, an extra 15 to 20 days in the cash cycle can tie up $8.2 million to $11 million in working capital [5]. That kind of math should live in the system, not in a spreadsheet someone forgot to update.

Landed cost visibility matters just as much. The platform should break out product cost, freight, insurance, customs duties, tariffs, brokerage fees, inland transportation, and handling on a per-unit basis in USD. It also needs support for imperial units such as pounds and cubic feet. U.S. tariffs on certain goods reached as high as 145% by early 2025 [2]. And tariffs don't just hit margin on paper. They also create a financing cost, since duties are paid at import, often 60 to 90 days before the customer pays. Pricing analysis needs to include that financing cost, not just the tariff rate [2].

| Evaluation Criteria | Pass/Fail Standard |

|---|---|

| Invoice Eligibility | Real-time eligibility engine that applies exclusion rules for overdue, concentrated, or disputed invoices [11] |

| Borrowing Base | Real-time recalculation that accounts for credits, returns, and other adjustments [11] |

| Invoice Status Tracking | Tracking from digital submission through final net proceeds [11] |

| Invoice Types | Domestic, export, progress billing, partial shipments, and short shipments [5] |

| Advance Rate | 70% to 90% of eligible receivables [11][12] |

| Funding Speed | Funds available within 1 to 2 business days of shipment [12] |

| Collections Control | Borrower retains ledger control and collections, often confidentially [11] |

| Multi-Currency Support | Multi-currency invoices with USD reporting and FX loop closure [12] |

| Supplier Terms Modeling | Scenario analysis for terms such as Net 30 versus Net 60 [1][5] |

| Landed Cost Components | Product cost, freight, insurance, customs duties, tariffs, brokerage fees, inland transportation, and handling per unit [2] |

| Physical Metrics | Support for imperial units such as pounds and cubic feet in landed cost calculations |

Next, test whether the platform can enforce currency controls, audit trails, permissions, and document linkage.

After you’ve confirmed funding and landed-cost visibility, the next step is simple: make sure the platform can control cross-border payments and keep a defensible audit trail. For global trade finance, that means tight currency controls, clear records, and access rules that don’t leave room for guesswork.

Global manufacturers can’t afford FX losses. Forced conversions at retail rates can eat up 2% to 3% per transaction [13]. The platform should let you hold and pay in local currencies while still rolling up reporting in USD [13].

Each FX conversion should show the exact rate used, with a timestamp in a standard format such as MM/DD/YYYY HH:MM [6]. That rate should tie back to an interbank benchmark, not a marked-up retail rate, and the platform should support scenario analysis for exchange-rate swings [13][7].

Some platforms also offer hedging or fixed-rate payment terms. That can help protect margins in the gap between supplier payment and customer remittance [13][7].

Once currency handling checks out, the next test is traceability. Can every transaction be tracked, approved, and reviewed without gaps?

An audit trail only matters if it’s immutable. No user, including administrators, can change the log [6]. Every upload, edit, approval, and document release should be recorded with a named user and timestamp [6][4].

It also helps to keep everything in one place. Use a single transaction record that connects all messages, amendments, and documents, with version history kept in that same record [4].

Permissions matter just as much. Finance, operations, and compliance teams—often managed with the help of fractional CFO services—should each have defined access levels [6][4]. Before payment goes out, require automated three-way matching. Each amendment should also link back to the original PO, shipment record, and invoice.

| Feature | Pass/Fail Standard |

|---|---|

| Currency Coverage | Support for 90+ currencies; ability to hold and pay in local currency while reporting in USD [13] |

| FX Rate Source | Real-time interbank rates, not marked-up retail rates [13] |

| FX Timestamp Format | FX events recorded in a standard format such as MM/DD/YYYY HH:MM [6] |

| FX Scenario Analysis | Rate-swing modeling between supplier payment and customer remittance dates [13][7] |

| Audit Log Immutability | Logs cannot be altered by any user, including administrators [6] |

| Audit Log Detail | Captures specific user, action type, and timestamp for every event [6][4] |

| Document Threading | All amendments, messages, and documents linked to a single transaction record [4] |

| Three-Way Matching | Automated verification of PO, goods receipt, and supplier invoice before payment [6] |

| Role-Based Permissions | Separate access levels for finance, operations, and compliance teams [6][4] |

| Compliance Checks | Built-in KYC/AML and sanctions screening during supplier onboarding [1] |

Once funding, cost visibility, and controls are set up, the next test is simple: can the platform turn trade activity into cash forecasts you can use?

Start with cash visibility, not access to funding. If a PO-funding tool can't produce a dependable 13-week forecast, it's just processing transactions.

The platform should tie together current receivables, expected payment timing, and upcoming supplier payments in a rolling 13-week cash forecast with confidence intervals [5]. That forecast should refresh on its own as new transactions come in, not sit around waiting for someone to export and update a spreadsheet.

It also needs to drill down by customer, supplier, product line, and geography so you can see exactly where a liquidity gap is starting to show up [5]. Add scenario modeling for shipment delays, term changes, and FX swings [1][2][15], and now the tool starts helping with actual decision-making. Predictive collections and cash forecasting can improve forecast accuracy by 15% to 20% [5].

Live integration is what makes a tool usable day to day.

Forecast quality comes from live system data, not periodic exports.

Live ERP data is better than manual uploads because it keeps financing, ledger, and forecast data in sync. Ask for native API connectivity to your ERP so financing activity posts straight to the general ledger and reconciles with bank statements without manual work [1][5]. Automated GL posting can cut month-end close time by 1 to 3 days [5]. If you run more than one ERP because of acquisitions or subsidiary setups, the platform should support middleware or an iPaaS layer to pull data together across entities [5].

Use these criteria to compare tools side by side.

| Evaluation Category | Pass/Fail Criterion |

|---|---|

| PO Finance Fit | PO finance available for your deal size; fees between 1.5% and 6% per transaction [3] |

| Invoice Discounting & Receivables Controls | Automated three-way matching confirmed [5][6] |

| Supplier Terms & Landed Cost | Supplier term modeling and full landed-cost breakout including tariffs and financing fees [2] |

| Multi-Currency & Audit Trails | Local-currency settlement supported; complete digital audit trail on every transaction and approval workflow [1][6] |

| Cash Flow Reporting | 13-week rolling forecast with drill-down by customer, supplier, product line, and geography; scenario modeling included [5][15] |

| Live ERP/FP&A Integration | Native API to ERP; automated GL posting; no manual reformatting before data enters forecasting models [1][5] |

| Implementation Timeline | Specialized platforms typically deploy in 60 to 90 days; integration costs can account for 40% to 60% of total project budget [14][15] |

Pick the tool that helps your team run the day-to-day work while giving finance a clean view of cash from PO through collection. Score each option against the same criteria, and put more weight on cash visibility and integration than on plain transaction processing.

Start by finding where working capital gets stuck with your Cash Conversion Cycle:

Days Inventory Outstanding + Days Sales Outstanding - Days Payable Outstanding

This gives you a clear view of where cash is sitting too long.

If payables are the problem, reverse factoring can help extend supplier terms. If you’re sitting on extra cash, dynamic discounting can put idle capital to work. And if there’s a funding gap, purchase order financing can cover new orders, while inventory financing turns stock into a managed liability.

Before rollout, put native ERP integration at the top of the list. API-based connections let you sync invoices in real time, match purchase orders automatically, and automate early payments without leaning on manual file exports.

You’ll also want to confirm integration with banking systems, KYC/AML workflows, and credit bureau connectivity. And check whether the API architecture can handle your transaction volume, so you can help avoid surprise overage costs as activity grows.

Manufacturers should put multi-currency treasury tools and tight compliance controls at the top of the list.

That matters because FX risk drops when teams can use automated hedging, track FX positions in real time, and pay suppliers in their local currency while the manufacturer settles in USD.

Audit and payment risk also go down when the system keeps automated audit trails, stores documented decision records, uses letters of credit, and runs validation checks for sanctions and discrepancies before funds are disbursed.