Published on

May 26, 2026

The GDPR regulates how personal data of EU residents is handled, especially when transferred outside the European Economic Area (EEA). If you're a U.S.-based company dealing with EU customer data, compliance with GDPR is mandatory, even without a physical EU presence. Violations can lead to fines of up to €20 million or 4% of global revenue.

Key points to know:

To comply, map your data flows, choose the right legal mechanism, and implement safeguards like encryption and data minimization. For financial platforms, ensuring compliance with third-party APIs is particularly important.

According to Chapter V of the GDPR, a cross-border data transfer occurs when personal data from the EU is made accessible to an entity outside the European Economic Area (EEA). For this to happen, three conditions must be met: the organization transferring the data must fall under GDPR's jurisdiction, the data is disclosed or made accessible to a non-EEA entity, and the recipient is located outside the EEA [1].

Interestingly, a physical transfer of files isn’t necessary. For example, if a U.S.-based engineer accesses an EU-hosted database remotely via an API, this still qualifies as a cross-border transfer under GDPR. As Morvantine explains:

"A transfer does not occur if the data never leaves the EEA." [4]

In practical terms, as soon as EU personal data becomes accessible to a party outside the EEA, the rules of Chapter V kick in. This is especially relevant for understanding how these rules apply to U.S.-based financial platforms.

GDPR’s reach extends far beyond the borders of the EU, as outlined in Article 3. A U.S.-based financial platform doesn’t need a physical presence in Europe to fall under GDPR. If the platform provides services - whether free or paid - to individuals in the EU or monitors their behavior, it is subject to GDPR requirements [2].

Consider a U.S. fintech company that onboards EU customers, processes their payments, or tracks their activity. Such actions bring the company under GDPR’s scope, exposing it to potential penalties of up to €20 million or 4% of its global annual revenue [4].

This broad jurisdiction is particularly important when considering how API-driven data flows can trigger GDPR compliance requirements.

APIs play a major role in facilitating cross-border data transfers, often triggering GDPR obligations. For instance, if a financial platform sends EU customer data to a U.S.-based analytics service, payment processor, or fraud detection API, this qualifies as a transfer under Chapter V [1][4].

APIs that handle real-time data syncing, user behavior processing, or onward transfers of data are particularly significant. Even if the initial transfer complies with GDPR, the involvement of sub-processors outside the EEA can pose compliance risks. For example, if your primary U.S. vendor relies on sub-processors not covered by an adequacy decision or Standard Contractual Clauses, your platform could still face violations - even if your direct vendor relationship meets GDPR standards [1][4].

It’s essential to map the entire data flow, from the initial transfer to any subsequent processing, to ensure compliance throughout the data chain. Ignoring these secondary layers can lead to significant regulatory challenges.

GDPR Cross-Border Data Transfer Mechanisms Compared

This section breaks down how to handle cross-border API data transfers while staying on the right side of GDPR regulations.

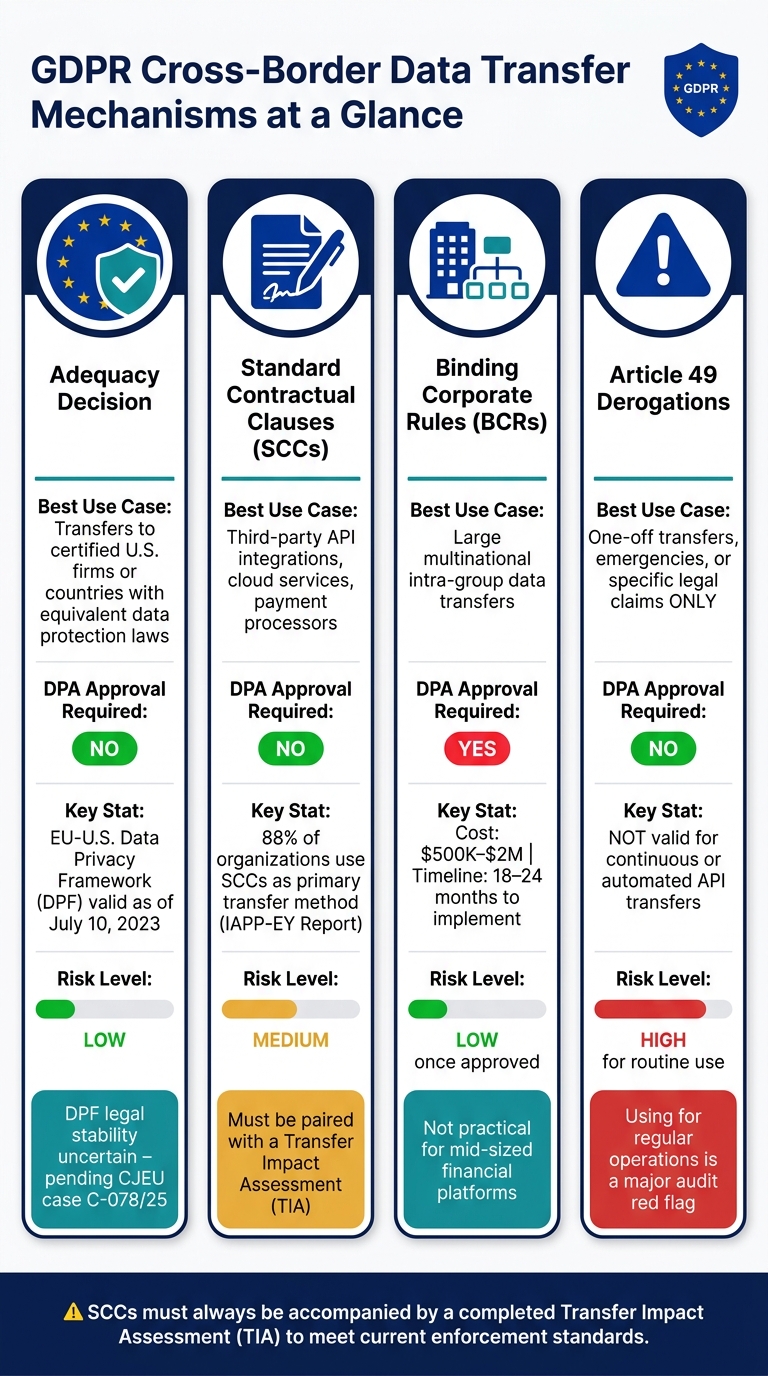

Once you’ve confirmed that your API data flows fall under GDPR, the next step is choosing a legal mechanism for the transfer. GDPR offers four main options:

| Mechanism | Best Use Case | DPA Approval Required? |

|---|---|---|

| Adequacy Decision | Transfers to certified U.S. firms or "safe" countries | No |

| SCCs | Third-party API integrations, cloud services, payment processors | No |

| BCRs | Large multinational intra-group data transfers | Yes |

| Article 49 Derogations | One-off transfers, emergencies, or specific legal claims | No |

The 2021 SCCs use a modular structure to fit different types of data relationships. For example:

SCCs require detailed documentation, including:

In light of the Schrems II ruling, you’ll also need to conduct a Transfer Impact Assessment (TIA). This evaluates whether U.S. surveillance laws, like FISA 702, could undermine SCC protections for your data flow [3][4]. If risks are identified, you’ll need supplementary measures. For example, Customer-Managed Encryption Keys (CMEK) can ensure decryption keys stay in the EEA, preventing U.S. authorities from accessing intelligible data under FISA 702 [4].

The Meta case from May 2023 highlights the risks of insufficient safeguards. Meta faced a €1.2 billion fine due to TIA shortcomings [4].

"The prudent legal strategy is to treat the DPF as a convenience mechanism... while maintaining robust SCC and TIA infrastructure as the permanent baseline." - Morvantine [4]

The 2021 SCCs also offer a docking clause, which allows new parties (e.g., additional API sub-processors or subsidiaries) to join without renegotiating the entire agreement [11][6].

Article 49 derogations are meant for rare, edge-case scenarios, such as:

These derogations are not designed for regular, automated API calls, such as those used for transaction processing or fraud detection. Continuous transfers automatically disqualify them from Article 49 coverage [5][2].

"The derogations in Art. 49 of the GDPR must be interpreted narrowly and... they must not be used for regular data transfers involving a large number of persons." - BfDI [10]

"It should be taken into account that no protection for the transferred data is guaranteed in the case of data transfers based on Art. 49 GDPR." - BfDI [10]

For financial platforms, relying on Article 49 for core operations is a major red flag during audits. The solution? Replace the derogation with SCCs, complete the necessary TIA, and document the change. Reserve Article 49 solely for the rare, exceptional cases it was intended to address.

Creating a solid data map is essential for identifying and safeguarding every API-based data transfer. Begin by developing a Record of Processing Activities (ROPA) to document each API data transfer. This should include the legal entity sending the data, the receiving entity and its location, the types of data being transferred (e.g., transaction IDs, IBANs, behavioral metadata), the frequency of transfers, and the legal framework in use - such as SCCs, the DPF, or BCRs [3].

Make sure to account for onward transfers as well. For instance, a payment processor based in the U.S. may route data to sub-processors in countries like India or Singapore. These additional data flows fall under your compliance responsibilities as well [12][13].

As previously discussed in GDPR obligations for API data flows, maintaining detailed logs is critical for handling breach notifications. Track every API call with details like user attribution, timestamps, endpoints, HTTP methods, and status codes. This level of detail ensures you can conduct thorough investigations and meet the 72-hour notification deadline in case of a breach [7].

Once your data map is complete, the next step is to carefully evaluate third-party API partners.

After mapping your data flows, it's time to ensure that each third-party API you work with meets compliance standards. Before integrating any third-party API that processes EU personal data, verify the following:

For vendors based in the U.S., check their certification status on dataprivacyframework.gov before relying on adequacy. However, given the ongoing legal challenges to the DPF (e.g., Case C-078/25, La Quadrature du Net, with a decision expected in late 2026 or early 2027), it’s wise to implement Module 2 SCCs as a backup plan. As Morvantine highlights:

"The DPF should be used as a primary transfer mechanism where available, but no organization that cannot operationally tolerate a sudden adequacy invalidation should rely on the DPF alone without an active fallback mechanism." [4]

Additionally, require vendors to maintain a public sub-processor list and provide updates via email or RSS notifications. This allows you to exercise your GDPR-mandated right to object when changes occur [14]. For financial data with higher risks, insist on encryption keys that are managed exclusively within the EU. If the vendor holds the decryption keys, they could be compelled by U.S. laws to release plaintext data [4].

One of the most effective ways to reduce the risks of cross-border data transfers is by sending less data in the first place. Configure API endpoints to return only the data fields that are absolutely necessary. As APIScout explains:

"An API endpoint that returns a full user profile when only the email address is needed violates the data minimization principle." [7]

For analytics and AI training, use hashed user IDs in processing pipelines and store the identity mapping in a separate, tightly secured database. This ensures that even if the analytics dataset is exposed, it cannot be directly linked to individuals without the mapping key [15]. For highly sensitive data like national IDs or account numbers, consider using envelope encryption at the application layer. This provides an additional layer of protection, even if the underlying database is compromised [15].

Don’t forget that data minimization also applies to backups. Align your backup deletion policies with your erasure commitments, or maintain a deletion log that can be applied if a backup is restored [15]. By limiting data exposure and incorporating pseudonymization techniques, you strengthen your overall GDPR compliance efforts.

One of the most frequent mistakes organizations make is treating Standard Contractual Clauses (SCCs) as mere paperwork and skipping the required Transfer Impact Assessment (TIA). This is especially risky for API-driven data transfers, where the fast-paced, continuous flow of information leaves little room for error. Dr. Thiébaut Devergranne, Founder of Legiscope, highlights this issue:

"A controller using SCCs without these supporting elements [TIA and supplementary measures] is subject to the same enforcement risks as having no valid transfer mechanism." [8]

Another common misstep is choosing the wrong SCC module. For instance, using a Controller-to-Processor module when a Controller-to-Controller relationship is in place renders the safeguard invalid. Additionally, some organizations are still relying on outdated SCC templates, even though the deadline to migrate to the updated 2021 modular SCCs expired on December 27, 2022 [8][16].

Transparency with sub-processors is another ongoing challenge. Many organizations fail to fully map their sub-processor chain in Annex III or rely on vague security descriptions in Annex II, both of which undermine compliance efforts.

These issues are further complicated by rulings like Schrems II, which have added new hurdles for data transfers to the U.S.

The Schrems II decision has fundamentally changed the landscape of U.S.-EU data transfers. By invalidating the Privacy Shield, it raised the bar for what constitutes "adequate protection" under GDPR. U.S. laws, such as FISA Section 702, allow government access to data regardless of where it’s stored, creating a direct conflict with GDPR’s requirements [9].

The U.S. CLOUD Act further complicates matters by enabling U.S.-based API providers to disclose data stored in the EU. For financial platforms relying on U.S.-hosted APIs, SCCs alone don’t cut it. Technical measures, such as using EU-managed encryption keys through tools like Google CMEK or AWS KMS (with keys stored within the European Economic Area), are essential to keep data secure - even if accessed under a U.S. warrant [4].

While the EU-U.S. Data Privacy Framework (DPF) aims to address these issues, its stability is far from guaranteed. For example, the Privacy and Civil Liberties Oversight Board (PCLOB), a critical part of the EU Commission’s adequacy decision, lost its quorum on January 27, 2025, after three members were dismissed [9][3]. Additionally, the pending La Quadrature du Net case before the Court of Justice of the European Union (CJEU) could potentially invalidate the DPF, creating further uncertainty for businesses.

Failing to address these compliance issues can lead to hefty fines. Financial platforms using third-party APIs are particularly vulnerable if they neglect essential GDPR processes. Since 2023, regulators have issued fines exceeding €2 billion for data transfer violations [9]. This enforcement trend underscores that no organization is exempt from scrutiny.

| Company | Fine | Date | Violation |

|---|---|---|---|

| Meta Platforms Ireland | €1.2 billion | May 2023 | SCCs used without adequate supplementary measures for FISA Section 702 exposure |

| TikTok | €530 million | May 2025 | Failure to verify SCC effectiveness and sub-processor transparency |

| Uber | €290 million | July 2024 | Transferred driver data to the U.S. for 27 months without a valid transfer mechanism |

| WhatsApp Ireland | €225 million | September 2021 | Transparency failures in data transfers to its U.S. parent |

Data based on regulatory actions and announcements [9].

It’s not just large tech companies that face these penalties. Regulatory bodies are expanding their focus to mid-sized businesses in sectors like financial services, healthcare, and HR - industries where sensitive personal data frequently flows through third-party APIs. Companies relying on U.S.-based analytics tools, payment processors, or cloud infrastructure without properly documented TIAs and SCCs are equally at risk, even if their scale is smaller.

Navigating cross-border GDPR compliance requires ongoing attention to legal, technical, and documentation requirements. Standard Contractual Clauses (SCCs) remain the go-to legal mechanism, but they must be paired with a completed Transfer Impact Assessment (TIA) to meet enforcement expectations [4].

For data transfers to the U.S., the Data Privacy Framework (DPF) should be your primary mechanism, with Module 2 SCCs as a fallback option. However, due to the DPF's uncertain legal standing, any organization that cannot handle a sudden invalidation of adequacy should avoid relying solely on it [4].

Legal compliance is just one piece of the puzzle. Strong technical measures are equally important. For instance, using EU-based encryption keys - such as Bring Your Own Key (BYOK) setups within the European Economic Area (EEA) - is becoming increasingly necessary for protecting sensitive financial data, especially under U.S. surveillance laws like FISA Section 702. Regularly updated data mapping and consistent TIA reviews can further reduce regulatory risks.

Regulators are no longer focusing exclusively on major tech companies. Mid-sized financial platforms that depend on U.S.-based analytics tools, payment processors, or cloud services are now facing greater scrutiny, especially if their TIA documentation is incomplete [4].

Given the complexity of these requirements, expert advisory support can be a game-changer. Phoenix Strategy Group (phoenixstrategy.group) partners with growing financial companies to ensure their data engineering and strategic infrastructure are designed to handle cross-border compliance challenges, including API risks and evolving regulations.

Yes, accessing EU personal data remotely from the U.S. is considered a data transfer under GDPR. According to the European Data Protection Board, this includes activities like granting access rights, approving remote access requests, or even displaying data for support purposes. If you're looking for help navigating compliance, Phoenix Strategy Group provides strategic advisory and data engineering services designed specifically for the operational and technical needs of growth-stage companies.

If the U.S. recipient has an active and relevant self-certification under the EU-U.S. Data Privacy Framework (DPF), this should be your primary mechanism for data transfers. However, given the possibility of legal challenges to the DPF, it’s wise to keep Standard Contractual Clauses (SCCs) as a backup option.

In cases where the recipient isn’t DPF-certified, their certification doesn’t cover the specific data being transferred, or if the DPF is invalidated, rely on SCCs as your standalone transfer mechanism. This ensures compliance and continuity in cross-border data handling.

When conducting a Transfer Impact Assessment (TIA) for API-based data flows, the focus should be on ensuring that the destination country’s legal framework enables the data importer to fulfill contractual obligations while upholding GDPR-level data protection. Here are the key areas to consider:

If the evaluation reveals that the risks to data protection remain high, it is essential to suspend the data transfers until adequate safeguards can be established.