Published on

February 26, 2026

In cross-border mergers and acquisitions (M&A), taxes can significantly impact deal value. Without proper planning, companies may face double taxation - where the same income is taxed in both the home and host countries. Tax treaties, also known as double taxation agreements (DTAs), offer a solution by reducing or eliminating withholding taxes on payments like dividends, interest, and royalties. These treaties can cut rates from 30% to as low as 15%, 5%, or even 0%, depending on the agreement.

Key Takeaways:

Tax Treaty Methods Comparison: Exemption, Credit, and Deduction

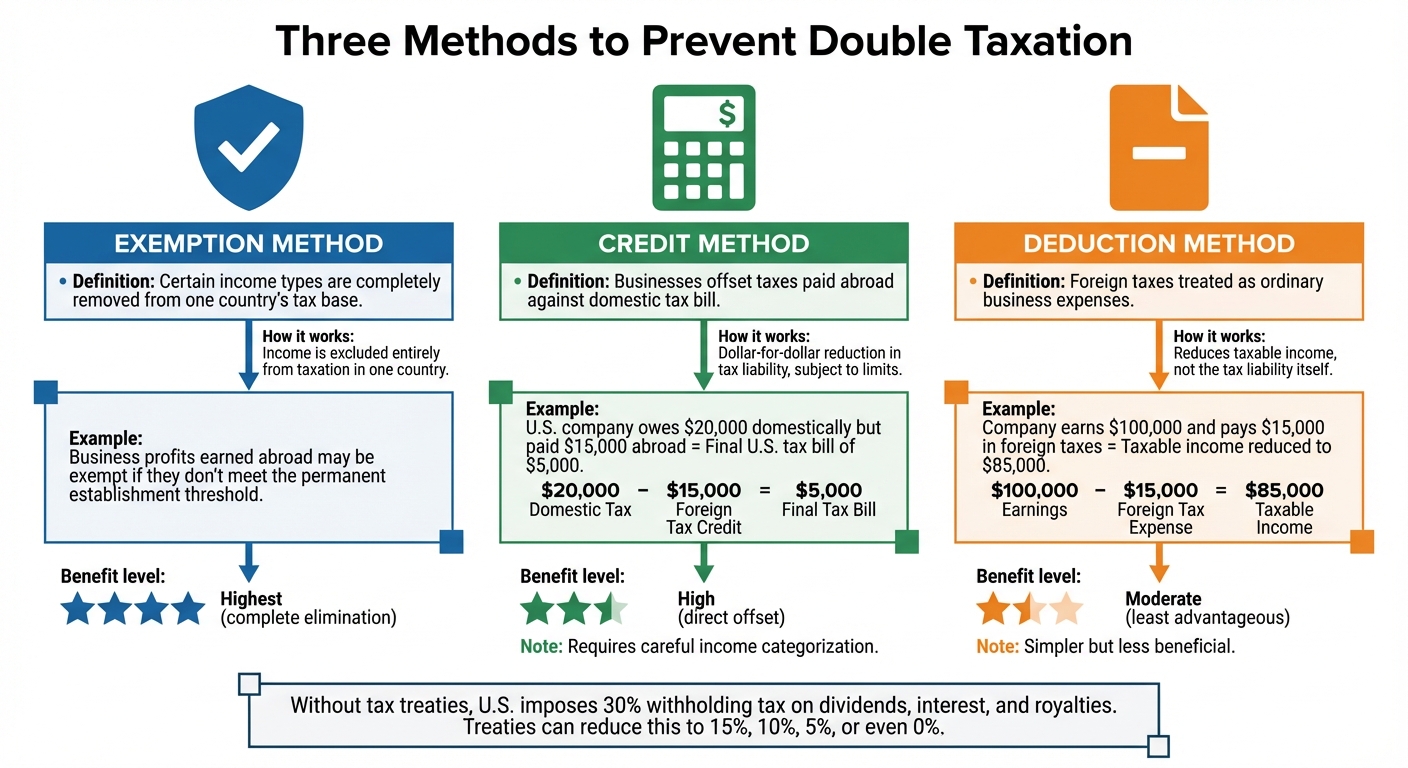

Double tax treaties aim to prevent the same income from being taxed twice by using three main approaches: exemption, credit, and deduction. The exemption method excludes certain income types from being taxed in one of the countries entirely. The credit method lets businesses offset the taxes they’ve already paid abroad against their domestic tax bill, effectively reducing their liability dollar-for-dollar, though it’s subject to limits. The deduction method allows foreign taxes to be treated as business expenses, lowering taxable income instead of directly reducing the tax owed [1].

These treaties also establish residency tie-breakers, which determine which country has the primary right to tax. This is typically based on factors like where a business is incorporated or managed. By doing so, they ensure that two countries don’t claim full taxation rights on the same income [1]. Additionally, these agreements help lower withholding taxes on cross-border payments, simplifying international transactions.

"Tax treaties can be seen as one leg in a three-legged stool supporting informed corporate tax structuring, with the other stools being applicable domestic codes (such as IRS regulations) and tax-related domestic court rulings." - Marcia DeForest, Director, US Corporate Tax Services, Vistra [2]

Under the exemption method, specific types of income are completely removed from one country’s tax base. For instance, treaty provisions may exempt business profits earned abroad if they don’t meet the threshold for a permanent establishment [1].

The credit method provides a direct offset for taxes paid abroad. For example, if a U.S. company owes $20,000 in domestic taxes but has already paid $15,000 in foreign taxes, the credit reduces the U.S. tax bill to $5,000. However, this method requires careful categorization of income [1].

The deduction method, while simpler, is less advantageous. It treats foreign taxes as ordinary business expenses, reducing taxable income rather than the tax liability itself. For example, if a company earns $100,000 and pays $15,000 in foreign taxes, the deduction lowers their taxable income to $85,000. Using these methods, treaties help reduce the financial burden of cross-border operations.

Without a treaty, the U.S. imposes a 30% withholding tax on dividends, interest, and royalties paid to foreign entities [1][2]. Tax treaties significantly cut these rates - often to 15%, 10%, 5%, or even 0%, depending on the type of income and the specific agreement [2][4].

"In general, interest and royalties derived and beneficially owned by a resident of a Contracting State are taxable only in that State." - Luxembourg-U.S. Tax Treaty [2]

To benefit from these reduced rates, businesses must secure a certificate of tax residency from their country’s tax authority and submit proper documentation, such as Form W-8BEN or W-8BEN-E for U.S. transactions [1][4]. They also need to meet Limitation on Benefits (LOB) rules, which prevent treaty shopping - where residents of third countries try to exploit treaty benefits indirectly [2][4].

Beyond lowering withholding taxes, treaties offer additional benefits like participation exemptions and tax deferral opportunities. Participation exemptions are especially useful in parent-subsidiary setups. Countries like Luxembourg and the Netherlands provide these exemptions, allowing parent companies to exclude certain dividends and capital gains from taxation if they hold a qualifying stake in a subsidiary [2].

Tax deferrals complement these exemptions by delaying income recognition. For example, companies can retain profits within foreign subsidiaries rather than repatriating them immediately, enabling reinvestment abroad at lower tax rates. This strategy optimizes the long-term tax profile of multinational operations. Engaging expert Fractional CFO services can help navigate these complex international tax structures.

Treaties also define permanent establishment (PE) rules, which can help businesses defer taxes. Profits are only taxed in a foreign country if a company has a PE there, such as an office or factory. By avoiding the PE threshold - like using independent sales agents without contract-signing authority - companies can operate in foreign markets without triggering local income taxes [1].

The United States has over 60 income tax treaties with various global trading partners, offering a way to reduce tax costs on cross-border transactions. Without these treaties, U.S. law enforces a 30% withholding tax on dividends, interest, and royalties paid to foreign entities. However, with the right treaty strategy, these rates can often be significantly lowered - sometimes even eliminated - making mergers and acquisitions (M&A) more appealing[1][2].

That said, tapping into these benefits isn't automatic. U.S. tax treaties include strict anti-abuse measures to prevent "treaty shopping", where companies from non-treaty countries attempt to claim benefits they aren't entitled to. Two key provisions to combat this are the Limitation on Benefits (LOB) clauses and the Principal Purpose Test (PPT). Successfully navigating these rules is crucial for structuring cross-border deals.

The U.S. has established strong tax treaties with several major M&A hubs, including Canada, the United Kingdom, the Netherlands, Luxembourg, Germany, Ireland, Switzerland, and Mexico[5]. For instance, treaties with the UK, the Netherlands, and Mexico allow for a 0% withholding tax rate on intercompany dividends between parent and subsidiary companies, provided certain conditions are met.

When planning a deal, companies should carefully evaluate which treaty networks offer the best balance of low withholding rates and manageable compliance requirements. The choice of jurisdiction can significantly influence after-tax returns. Once a preferred treaty network is identified, businesses must ensure they comply with provisions limiting treaty benefits.

LOB clauses are designed to ensure that only entities with a genuine connection to the treaty country can access reduced tax rates. Companies must typically satisfy one of several tests, including:

"The LOB article is premised upon the view that a resident of a Contracting State must have some further connection to that country in order to benefit from that Contracting State's income tax treaty with the United States."

– Michael J. Miller, Partner, Roberts & Holland[7]

Before finalizing a deal, companies should conduct a thorough LOB analysis. Simply being a resident of a treaty country doesn’t guarantee benefits - verify which specific test your structure meets and document key operational decisions made within the treaty jurisdiction. Beyond meeting these objective criteria, companies must also address the more subjective Principal Purpose Test.

Unlike LOB clauses, the PPT focuses on the intent behind a transaction. This provision denies treaty benefits if one of the main purposes of the arrangement is tax avoidance. Over 100 countries have incorporated the PPT into their treaties through the OECD's Multilateral Instrument (MLI)[8].

Even if a company meets all LOB requirements, the IRS can deny benefits under the PPT if tax avoidance is deemed a primary motive. To pass PPT scrutiny, companies must demonstrate genuine business activity. For example, holding companies should have local employees, active management, and conduct board meetings within the jurisdiction. Additionally, companies should maintain clear documentation explaining the business rationale for their chosen structure.

On September 19, 2025, the IRS issued guidance (Memorandum AM2025-002) clarifying that treaty relief for Branch Profits Tax (BPT) may apply to reverse foreign hybrids, provided LOB requirements are satisfied[3]. To avoid issues under the PPT, businesses should also consider potential exit taxes and withholding tax implications early in the M&A planning process. This ensures the structure remains financially sound while meeting compliance standards. A well-rounded approach is critical to navigating these complex treaty rules effectively.

Cross-border M&A deals, even with a carefully planned tax treaty strategy, come with risks that can undermine expected savings. Common challenges include transfer pricing disputes, permanent establishment triggers, and compliance failures. These issues can lead to double taxation, penalties, or expensive audits. Addressing these risks early in the planning phase is crucial. Engaging fractional CFO services can provide the specialized financial oversight needed to navigate these complexities.

Transfer pricing, which involves transactions between related entities, is heavily scrutinized in cross-border M&A. For example, when a U.S. company acquires a foreign entity or sets up intercompany financing, tax authorities will examine whether the pricing reflects arm's-length market rates. If authorities suspect profit shifting through artificial pricing, they can adjust the terms, often resulting in double taxation.

Tax treaties offer a solution through the Mutual Agreement Procedure (MAP), where competent authorities from both countries negotiate to resolve disputes. In 2019, the U.S. competent authority closed 142 transfer pricing MAP cases, with approximately 81% resulting in agreements that eliminated double taxation[9]. However, timing is critical - delaying a MAP request can trigger "hot interest", which adds an extra 2% interest on large corporate underpayments[9]. To avoid this, businesses should initiate MAP requests early in the audit process.

For long-term stability, companies can secure bilateral Advance Pricing Agreements (APAs), which set approved transfer pricing methods for five years or more. The OECD BEPS Action 14 recommends resolving new MAP cases within an average of two years[9]. Additionally, filing a protective claim for a refund alongside a MAP request can safeguard rights under domestic law if negotiations stall.

The next step is to evaluate risks tied to creating a taxable presence.

Another major risk in cross-border M&A is permanent establishment (PE). A PE occurs when a company’s activities in a foreign country establish a taxable presence, leading to local income tax and payroll obligations. PE risks often surface during legal entity rationalization or when centralizing functions but retaining key personnel in multiple locations. Triggers for PE include maintaining a fixed place of business, such as an office or warehouse, construction projects lasting over 12 months, or employing agents authorized to negotiate or execute contracts on the company’s behalf.

"By properly interpreting the treaty and adhering to certain activities, a company can avoid creating a PE in the foreign country and potentially avoid foreign taxation on the income earned in the foreign country."

– PBMares[1]

To minimize PE risks, companies should conduct a pre-deal PE analysis to identify potential triggers. One effective tactic is hiring independent sales agents in foreign markets, ensuring they do not have the authority to finalize contracts. This strategy reduces exposure to foreign income and payroll taxes while allowing market access. Additionally, companies should closely monitor the duration and scope of construction or installation projects to stay within treaty limits.

Beyond transfer pricing and PE concerns, compliance with reporting standards is essential. To access treaty benefits, companies must meet strict documentation and reporting requirements. This includes obtaining a certificate of tax residency from their domestic tax authority and submitting forms like IRS Forms W-8BEN-E or W-8IMY to the foreign tax authority. These forms demonstrate treaty eligibility and enable reduced withholding rates on dividends, interest, and royalties.

Companies must also meet substance requirements, which involve maintaining active business operations, local employees, and management in the treaty jurisdiction. Filing a treaty notification or protective filing can preserve rights if a MAP request cannot be submitted immediately. These filings should be updated annually until a formal request is made.

One critical mistake to avoid is settling disputes with foreign tax authorities without consulting the U.S. Advance Pricing & Mutual Agreement Program (APMA). Such settlements can block MAP access if they hinder the U.S. authority’s ability to negotiate. Additionally, taxpayers involved in IRS Appeals must address or separate transfer pricing issues within 60 days of the opening conference to retain MAP eligibility. With more than 3,000 bilateral tax treaties in effect worldwide[2], staying compliant is vital to securing treaty benefits and avoiding costly disputes.

Maximizing the benefits of tax treaties in cross-border M&A deals requires careful planning and attention to detail at every stage. With numerous treaties available to navigate, this checklist outlines the essential steps - from initial analysis to post-merger compliance.

"Tax treaties can be seen as one leg in a three-legged stool supporting informed corporate tax structuring, with the other stools being applicable domestic codes... and tax-related domestic court rulings." – Marcia DeForest, Director, US Corporate Tax Services [2]

Once these analyses are complete, move forward with structuring the deal to maximize treaty advantages.

With due diligence as the foundation, structure the transaction to make full use of treaty benefits:

These steps help minimize double taxation and enhance the overall tax efficiency of the deal.

After the deal is structured, maintaining compliance with treaty requirements is key to preserving tax benefits:

"Sponsors and advisors should continue to ensure that structures are carefully reviewed in light of the relevant treaty terms, and that documentation is kept up to date to support any treaty claims." – Caldwell [3]

Cross-border M&A transactions present exciting growth opportunities, but the tax challenges they bring can significantly reduce deal value if not properly managed. With over 3,000 bilateral tax treaties in place worldwide[2], there’s a considerable chance to lower or even eliminate the standard 30% withholding tax on dividends, interest, and royalties. The trick lies in skillfully navigating treaty provisions - whether it’s dealing with Limitation on Benefits (LOB) clauses or Principal Purpose Tests (PPT).

To make the most of these treaties, expertise is critical at every stage of the transaction. During pre-deal due diligence, it’s essential to confirm tax residency, evaluate LOB qualifications, and ensure beneficial ownership requirements are met. When structuring the deal, utilizing intermediary jurisdictions or hybrid entity provisions can help achieve optimal withholding rates and defer taxes. Post-merger, ongoing compliance becomes vital, from maintaining proper treaty documentation and monitoring ownership changes to coordinating with state-level tax rules that may not align with federal treaty protections.

"Understanding and effectively utilizing tax treaties can significantly reduce tax liabilities, avoid double taxation, and ensure compliance with international tax regulations for cross-border companies." - Lynn M. Eller, Partner, International Tax Team Leader, PBMares[1]

This perspective highlights the importance of professional advisory support in navigating the tax intricacies of cross-border M&A. With over 70% of dealmakers identifying rising tax risks as a growing threat to M&A success, the stakes couldn’t be higher[11].

For companies grappling with LOB requirements, PPT compliance, and permanent establishment risks, Phoenix Strategy Group offers specialized M&A advisory services tailored to every stage of treaty optimization. Their services range from pre-deal tax analysis and transaction structuring to managing post-merger compliance. By combining deep expertise with advanced financial modeling, they help maximize deal value while minimizing tax exposure.

Whether you’re exploring a cross-border acquisition or preparing for an international exit, having seasoned advisors on your side ensures you can leverage treaty benefits effectively while steering clear of anti-abuse measures and permanent establishment risks. A well-executed deal starts with the right team.

To figure out which tax treaty applies to your transaction, start by examining the agreements between the U.S. and the other country involved. Pay close attention to the treaty's effective dates, residency rules, and key provisions. Tools like the IRS treaty list and technical explanations can provide detailed insights into the treaty’s specifics. Taking the time to research thoroughly will help you understand how the treaty may affect your deal.

To qualify for reduced withholding rates, you need to ensure several key steps are followed. First, confirm that a valid tax treaty exists between your country and the United States. Next, verify that you meet the residency and eligibility requirements outlined in the treaty. Additionally, you’ll need to provide all necessary documentation - this often includes Form 8833 in the U.S.

Carefully review the specific provisions of the treaty and applicable rules to ensure compliance. Properly completing and submitting the required forms, along with adhering to the guidelines, is crucial for successfully reducing withholding rates.

A deal structure might comply with legal standards but still fail the LOB (Limitation on Benefits) or PPT (Principal Purpose Test) due to factors like unexpected permanent establishment risks, tax compliance hurdles, or conflicts with tax treaty provisions. These missteps can result in unforeseen tax obligations or compliance breaches, even when the structure is technically lawful.