Published on

February 27, 2026

When selling a pass-through business - like an LLC, S corp, or partnership - you face unique tax challenges. Without preparation, taxes can consume over 30% of your sale proceeds. Key factors include:

Start planning at least 18-24 months before selling. Timing, structure, and preparation are critical to reducing taxes and keeping more of your earnings. Read on for detailed strategies to navigate this process.

Pass-through entities dodge the double taxation issue that traditional C corporations face. Instead of being taxed at the corporate level - currently a flat 21% - and again when profits are distributed, pass-through entities shift their profits and losses directly to the owners' individual tax returns. While this single-layer taxation simplifies operations, it adds complexity when planning for an exit.

Your basis - the amount you initially invested, adjusted by retained earnings - determines how much of your sale is taxable. If distributions exceed your basis, they’re treated as capital gains. Additionally, some assets, like unrealized receivables (commonly called "hot assets"), may be taxed as ordinary income at top marginal rates, which are expected to revert to 39.6% when current tax provisions expire [7].

"Generally, a partnership doesn't pay tax on its income but passes through any profits or losses to its partners. Partners must include partnership items on their tax returns." - Publication 541, Internal Revenue Service [7]

In partnerships, a reduction in your share of debt during a sale is considered a cash distribution. For example, if your share of partnership debt decreases by $100,000, it’s as though you received $100,000 in cash. If this exceeds your basis, it could trigger a taxable gain. This makes tracking your basis throughout ownership - not just when selling - essential.

Here’s how taxation works during exits for sole proprietorships, partnerships, and S corporations.

Selling a sole proprietorship means selling off individual business assets, such as equipment, inventory, customer lists, and goodwill. Each type of asset is taxed differently. For instance:

On top of this, self-employment tax (around 15.3%) applies to ordinary income from these sales. To reduce your tax burden, structuring the sale to allocate more proceeds to capital assets like goodwill can be beneficial.

Exiting a partnership is more complex. Selling your partnership interest is usually treated as a capital asset sale. However, "hot assets" - such as unrealized receivables and substantially appreciated inventory - are taxed as ordinary income. This means part of your proceeds could be taxed at higher ordinary income rates instead of the lower long-term capital gains rate.

Your partnership basis includes your initial investment plus adjusted liabilities. If your share of partnership liabilities decreases during a sale, the reduction is treated as a cash distribution. If this exceeds your basis, you’ll recognize a capital gain, even if you haven’t received actual cash.

"One of the primary challenges and disadvantages of pass-through taxation is that owners can be taxed on income they haven't actually received." - Craig Fisher, Senior Tax Manager, Aprio [6]

Another wrinkle is the Centralized Partnership Audit Regime (CPAR). Under CPAR, the IRS can collect underpaid taxes from previous years directly from the partnership. If your partnership agreement doesn’t allow these adjustments to be "pushed out" to the original partners from the reviewed year, you could end up paying taxes on income earned by others, including former partners.

For S corporations, exits can involve selling stock for capital gains or selling assets, which results in a mix of ordinary income and capital gains.

Your basis in S corporation stock starts with your initial investment and increases with your share of corporate income. However, unlike partnerships, S corporation basis isn’t affected by corporate debt - only direct shareholder loans can increase it. This limits how much you can take in tax-free distributions compared to partnerships.

The Accumulated Adjustments Account (AAA) tracks the S corporation’s retained earnings. Distributions from the AAA are tax-free up to your basis, but any amount beyond that is treated as a capital gain. Knowing your AAA balance is critical during an exit, as it directly impacts how distributions are taxed. Also, S corporation owners must pay themselves a reasonable salary through formal payroll. If they don’t, the IRS might reclassify exit distributions as wages, making them subject to employment taxes.

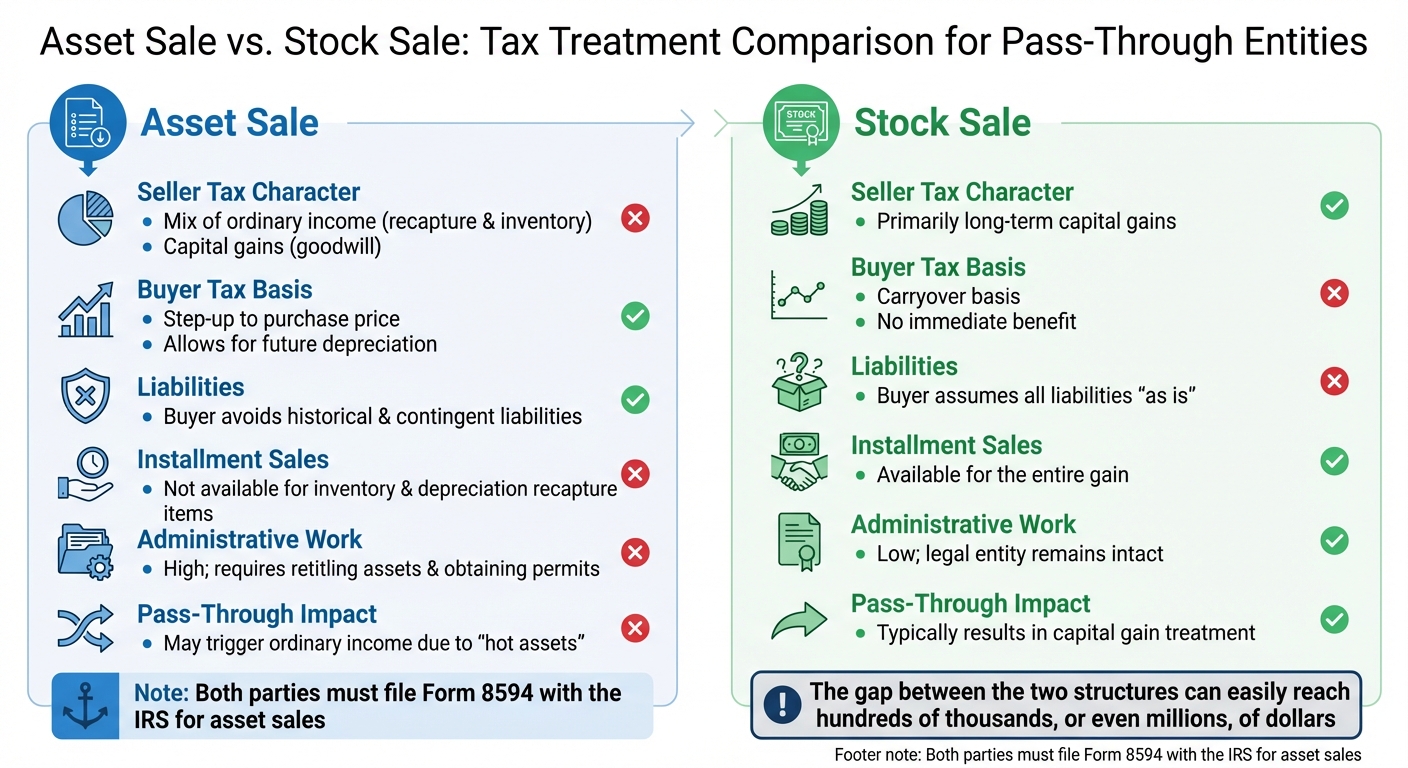

Asset Sale vs Stock Sale Tax Comparison for Pass-Through Entities

When selling a pass-through entity, the structure of the deal - whether it’s an asset sale or a stock sale - leads to different tax outcomes for both the seller and the buyer. This decision directly impacts your tax obligations and plays a critical role in shaping your overall exit strategy. Not only does it affect your immediate tax bill, but it also influences the buyer’s future deductions and the broader financial dynamics of the transaction.

In an asset sale, the buyer purchases specific business assets, such as equipment, inventory, and goodwill, while the legal entity itself remains with the seller. One key advantage for the buyer is the ability to "step up" the tax basis of these assets to align with the purchase price, which allows for more substantial depreciation and amortization deductions in the future. The IRS requires the allocation of the purchase price across predefined asset categories. For the seller, this structure often results in a mix of tax treatments: inventory and depreciation recapture are taxed at ordinary income rates, while goodwill is taxed at long-term capital gains rates [12]. This combination can lead to a higher overall tax burden.

In a stock sale, the buyer acquires the entire legal entity, including all shares. For the seller, this typically results in long-term capital gains taxation on the entire transaction, which generally comes with a lower tax rate. However, buyers inherit the company’s historical tax basis for its assets and assume all existing and potential liabilities. This limits their ability to claim future tax deductions, making stock sales less appealing from their perspective.

"The gap between the two structures can easily reach hundreds of thousands, or even millions, of dollars, depending on the asset mix, entity form, and state tax exposure."

- Matthew McNally, Managing Partner, Evolved [8]

Because asset sales offer buyers the benefit of a basis step-up, they often prefer this structure. On the other hand, sellers tend to lean toward stock sales to avoid the higher tax burden tied to asset sales. In the case of an asset sale, both parties are required to file Form 8594 with the IRS to report the agreed-upon allocation of the purchase price. This form should ideally be filed at the Letter of Intent stage [10][11]. These structural decisions are pivotal when planning a tax-efficient exit.

| Comparison Aspect | Asset Sale | Stock Sale |

|---|---|---|

| Seller Tax Character | Mix of ordinary income (recapture and inventory) and capital gains (goodwill) [8] | Primarily long-term capital gains [8] |

| Buyer Tax Basis | Step-up to purchase price; allows for future depreciation [8] | Carryover basis; no immediate benefit [8] |

| Liabilities | Buyer avoids historical and contingent liabilities [8] | Buyer assumes all liabilities "as is" [8] |

| Installment Sales | Not available for inventory and depreciation recapture items [9] | Available for the entire gain [9] |

| Administrative Work | High; requires retitling assets and obtaining permits [8] | Low; legal entity remains intact [8] |

| Pass-Through Impact | May trigger ordinary income due to "hot assets" | Typically results in capital gain treatment |

Grasping these distinctions is critical before diving into strategies to minimize taxes as part of your exit plan.

When it comes to selling your business, the tax implications can be daunting. However, with the right strategies, you can significantly reduce the tax burden and retain more of your hard-earned proceeds. The key is to start planning early - ideally 18 to 24 months before your planned exit [4].

For owners of pass-through entities, three strategies stand out: the Qualified Business Income (QBI) deduction, installment sales, and Section 1202 Qualified Small Business Stock (QSBS) exclusions. These tools can help lower taxable income, spread tax liability over time, and even eliminate federal taxes on a large portion of your gains. Let’s dive into how each of these strategies works and how they can fit into your exit plan.

The Section 199A deduction allows eligible pass-through business owners to deduct up to 20% of their qualified business income (QBI), reducing taxable income [15]. Thanks to the One Big Beautiful Bill Act (OBBBA), this deduction is now permanent, providing long-term clarity for tax planning [15].

When selling a business, QBI includes net qualified gains from the sale of assets taxed as ordinary income - like depreciation recapture or inventory gains - but excludes capital gains [16]. This distinction is important for calculating your deduction.

"The permanent QBI deduction under OBBBA provides long-term tax certainty for pass-through business owners."

For high-income earners (above $400,000 for married couples filing jointly in 2026), the deduction is limited to the greater of 50% of W-2 wages or 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property (UBIA) [15]. This opens up planning opportunities. For example:

"Since the QBI deduction for those above the threshold is limited based on W-2 wages, paying higher wages can actually result in greater overall tax savings when the increased QBI deduction exceeds the additional employment taxes incurred."

- Jessica I. Marschall, CPA, Marschall Accounting Services [15]

Starting in 2026, a new minimum QBI deduction of $400 is available for taxpayers with at least $1,000 in aggregate QBI from active businesses [15]. This deduction can be a cornerstone of a well-structured exit plan.

An installment sale under Section 453 allows you to spread out payments from the sale of your business over several years, which can help reduce your annual tax bill. With this method, you report taxable gains as payments are received, potentially keeping you in lower tax brackets and minimizing exposure to the 3.8% Net Investment Income Tax (NIIT) [3].

For example, one business owner restructured their asset sale into a stock sale with a four-year installment plan, saving $600,000 in taxes [3].

"An installment sale isn't just about deferring taxes - it's about creating a predictable, strategic flow of income while managing exposure."

However, there are some caveats. Depreciation recapture must be recognized as ordinary income in the year of the sale, and installment sales cannot be used for inventory, dealer property, accounts receivable, or publicly traded securities [17]. Additionally, if your total installment obligations exceed $5 million at year-end, the IRS may impose an interest charge on the deferred tax liability under Section 453A [17].

To make the most of this strategy:

By carefully structuring your sale, an installment plan can provide both tax savings and financial flexibility.

Section 1202 offers a significant tax advantage for owners of qualified small business stock (QSBS). If you meet the requirements, you can exclude a large portion of your gain from federal taxes. Under the OBBBA, the QSBS exclusion was increased to $15 million or 10 times your basis, whichever is greater [14]. The "aggregate gross asset" threshold for QSBS eligibility was also raised from $50 million to $75 million [14].

The percentage of your gain you can exclude depends on how long you’ve held the stock:

To qualify for QSBS benefits, your business must be a C corporation with gross assets of $75 million or less at the time the stock is issued. Additionally, at least 80% of the company’s assets must be used in an active trade or business. Certain industries, like professional services, banking, and hospitality, are excluded from QSBS eligibility [14].

If you’ve held QSBS for at least six months but haven’t reached the five-year mark, you can defer the gain by reinvesting in new QSBS within 60 days using a Section 1045 rollover [14]. This allows you to maintain tax benefits while transitioning to a new investment.

For pass-through entities considering a conversion to a C corporation before selling, timing is critical. The five-year holding period starts on the date of issuance, not conversion, so advanced planning is essential. Working with experienced tax advisors can help you navigate these complexities and maximize your benefits.

For personalized advice on incorporating these strategies into your exit plan, reach out to the experts at Phoenix Strategy Group.

Selling a business while operating in multiple states brings a web of tax challenges. Just holding an interest in a pass-through entity can create nexus - a connection obligating you to pay taxes - in every state where the entity operates. This means even passive investors in limited partnerships or LLCs might need to file personal income tax returns in several states, adding complexity to exit planning.

When dividing sale proceeds among states, the rules vary. States use either allocation, which assigns income to a single state (often your home state), or apportionment, which splits it based on factors like sales, property, and payroll. These approaches differ significantly by state. For instance, in Corrigan v. Testa (2016), the Ohio Supreme Court ruled that a nonresident’s capital gain from selling an Ohio LLC interest was taxable only in their home state, as there was no "unitary" business connection. Conversely, Massachusetts took a different stance in VAS Holdings & Investments LLC v. Commissioner of Revenue (2022), applying the "investee apportionment" method and taxing the gain based on where the LLC conducted its business.

"The issue of taxes and regulation - from a state perspective - may often be overlooked in structuring small businesses... entities and their owners may face substantially different tax consequences based on their organizational structure, business operations, types of income, tax elections, and states in which they operate."

- The Tax Adviser [19]

Withholding requirements further complicate matters. Many states mandate withholding taxes from nonresident owners during a sale. Some states also impose taxes directly on the entity itself. For example, California charges LLCs an annual minimum tax of $800, which continues until a certificate of cancellation is filed. In New York, S corporations face a minimum tax ranging from $25 to $4,500, depending on gross receipts [19]. Additionally, over 30 states now offer Pass-Through Entity Tax (PTET) elections, allowing businesses to pay state taxes at the entity level. This can help owners sidestep the federal SALT deduction cap [1].

To avoid lingering tax liabilities and penalties, file certificates of cancellation promptly in all registered states. For example, Texas imposes monthly penalties starting at $100 and climbing to $5,000 for unregistered business activity [19]. Seeking advice from multistate tax experts can help you protect your exit proceeds. For specialized guidance, consider reaching out to Phoenix Strategy Group. These state-level tax hurdles are just one piece of the puzzle, leading into broader considerations like estate and gift tax strategies.

Planning several years in advance - ideally 3 to 5 years - can help business owners lock in favorable valuations and shift future growth out of their taxable estate. This approach can save heirs a considerable amount in taxes.

The federal lifetime estate and gift tax exemption is set at $13.99 million per individual for 2025 and is projected to increase to $15 million in 2026. However, any gifts exceeding the $19,000 annual exclusion require filing IRS Form 709 along with detailed documentation. To prepare for IRS scrutiny, it’s crucial to obtain qualified appraisals and maintain at least five years of financial records [25].

"The prudent business owner will employ estate planning techniques to ensure that the future appreciation of the business accrues outside his or her estate, while also minimizing the income taxes due from the owner upon any sale."

These foundational steps pave the way for using advanced tools like GRATs and FLPs to transfer future appreciation in a tax-efficient manner.

A GRAT is a strategic way to transfer business interests to family members while retaining fixed annuity payments for a set term. If your business grows faster than the IRS "hurdle rate" (the Section 7520 rate), any excess appreciation passes to your beneficiaries without triggering gift taxes [21][23].

A popular approach is the "zeroed-out" GRAT, where the annuity payments are structured to make the remainder interest nearly worthless for tax purposes. This allows you to transfer significant wealth without tapping into your lifetime gift tax exemption [20][23][24]. Since GRATs are grantor trusts, you remain responsible for the trust's income taxes, effectively making an additional tax-free gift to your heirs [21][23].

However, GRATs carry a key risk: if you pass away during the trust's term, its assets revert to your taxable estate, negating the tax benefits. To address this, many advisors recommend creating a series of short-term "rolling GRATs" lasting 2 to 4 years instead of one long-term trust [23][24]. Tax savings can also be amplified by contributing discounted FLP interests into a GRAT [20][24].

An FLP provides a way to retain control of your business as the General Partner while gifting Limited Partner (LP) interests to family members. One of the main advantages of this structure is the ability to apply valuation discounts. Since LP interests typically lack voting rights and are not easily sold, their taxable value can be reduced by 20% to 40% [23][24].

"LP interests often carry lower valuations for estate and gift tax purposes due to: Lack of Control Discount... [and] Lack of Marketability Discount."

- CPA Exams Mastery [24]

For example, applying a 30% discount to a $5,000,000 gift reduces its taxable value to $3,500,000. At a 40% tax rate, this could save $600,000 in taxes. To defend these discounts, it’s essential to establish a legitimate business purpose for the FLP - such as asset protection or centralized management - and to avoid mixing personal and partnership funds [24].

| Discount Type | Description | Typical Impact on Value |

|---|---|---|

| Lack of Control | Reflects that a minority owner cannot make key decisions. | 10–25% |

| Lack of Marketability | Reflects the difficulty of selling interests in a private business. | 20–35% |

| Combined Discount | The total reduction applied to the pro-rata value of the interest. | 20–40% |

Getting the timing right and staying on top of compliance are key to reducing tax liabilities when exiting a business. A rushed sale can lead to hefty tax bills - sometimes costing you hundreds of thousands of dollars. Careful planning can help prevent taxes from eating away as much as 30% (or more) of your sale proceeds [3][28]. On the other hand, poor timing or incomplete records could derail the entire deal.

"The difference between proactive and reactive tax planning can have a material impact on your net proceeds. The time to start planning your exit's tax strategy isn't when you receive an offer: it's now."

- Matthew Sapowith, Founder, Sapowith Tax Advisory [28]

Start planning your exit 18–24 months ahead of time. This allows you to restructure your business entity, meet holding period requirements, and prepare clean financial records [4]. If your exit strategy involves more complex moves - like Section 1202 QSBS planning or converting your entity structure - you’ll need a longer runway of 3 to 5 years [26][30].

Buyers typically want to review at least three years of tax returns, profit and loss statements, and balance sheets during the due diligence process [27]. If your records are disorganized or don’t match your tax filings, you could face delays, lower offers, or even deal cancellations. Reconciling your financial statements with your tax returns ahead of time can help you catch and fix any discrepancies before a buyer’s audit does [27].

One important step is to separate personal expenses from business expenses as early as possible. Things like vehicle costs, family meals, or home office deductions that won’t transfer to the new owner should be clearly documented and removed from your business financials [27][30].

"Business owners should operate as though the company is always 'for sale'. Opportunities often arise unexpectedly and financials that aren't sale-ready can delay or derail a deal."

- Bradford Hall, MGO CPA LLP [4]

In the year leading up to your exit, consider reducing the working capital held in the business. Buyers typically don’t pay extra for surplus cash or inventory, so pulling out excess capital ahead of time can increase your net proceeds without affecting the purchase price [4].

Once your financials are in order, you can focus on timing your exit to maximize tax benefits.

The timing of your closing date can significantly impact your tax bill. For example, a manufacturing business owner in the Midwest saved $600,000 by restructuring their sale as a stock sale with a four-year installment plan and delaying the closing to January. This reduced their tax bill from $1.9 million to $1.3 million [3].

Relocating to a tax-friendly state before the sale can also help you avoid state capital gains taxes, which can range from 5% to 13% of your total bill [3][29]. If you anticipate federal tax rates increasing in the next year, closing your deal in December can help lock in the current rates.

"Timing gives you power. Power to negotiate, power to protect value and power to decide what legacy you want to leave - not just what you walk away with."

- Tiffany Kuntemeier, Partner, Wipfli Advisory LLC [26]

To further optimize your exit, consider including a "tax-efficient exit" clause in your Letter of Intent [30]. Work with your advisors to model the after-tax proceeds of an asset sale versus a stock sale before finalizing the deal [26][29].

For tailored advice on creating a tax-efficient exit strategy, you can consult with Phoenix Strategy Group, where experts can help you craft a plan that fits your unique situation.

Start planning your exit at least 18–24 months in advance. This timeline gives you room to fine-tune your business structure, increase EBITDA, and trim down excess working capital [4][5]. If you're considering more intricate strategies, like Section 1202 or entity conversions, you’ll need even more time to ensure everything is set up properly. Early preparation helps you make smarter decisions when it comes to structuring your deal.

When it comes to deal structure, the details matter. Buyers often lean toward asset sales because they come with depreciation benefits, but sellers usually prefer stock sales to take advantage of capital gains treatment. A Section 338(h)(10) election can help bridge this gap [4][5]. Keep in mind that "hot assets" - things like unrealized receivables and highly appreciated inventory (valued at more than 120% of their basis) - can trigger ordinary income tax rates instead of capital gains, which could impact your bottom line [31].

Tax strategies can make a big difference in your exit outcome. For example, the QBI deduction has lowered top federal tax rates from 37% to 29.6% [2]. Another option is Section 1202, which can exclude up to $10 million (or $15 million for stock acquired after July 4, 2025) in gains if you've held the stock for five years [4]. Additionally, installment sales offer a way to defer taxes over time.

"A knowledgeable CPA can help you identify red flags, clean up reporting, and implement strategies that improve the business's financial profile so you're prepared to act when the timing is right."

- MGO CPA LLP [4]

Navigating exit planning can be tricky, so it’s wise to team up with CPAs, financial advisors, and legal experts. They can help you tackle challenges like the Centralized Partnership Audit Regime and phantom income issues. For tailored, tax-efficient strategies, you can consult Phoenix Strategy Group.

The decision to go with an asset sale or a stock sale hinges on factors like tax impact, liability concerns, and the goals of both the buyer and seller. In an asset sale, buyers can pick and choose specific assets while steering clear of most liabilities. On the other hand, a stock sale transfers ownership of the entire entity, including all its assets and liabilities. Sellers often lean toward stock sales because of potential tax benefits, whereas buyers usually prefer asset sales to reduce their exposure to liabilities.

When we talk about “hot assets,” we’re referring to specific items like inventory or unrealized receivables that can trigger ordinary income during a partnership or business transaction. Unlike capital gains, which often enjoy lower tax rates, ordinary income is taxed at a higher rate. Because of this, knowing how these assets are handled is key to managing your tax obligations effectively and staying compliant with tax laws.

Yes, you can potentially use Qualified Small Business Stock (QSBS) to lower the taxes on your exit. Under current tax rules, the sale of QSBS may allow for substantial exclusions on capital gains. This includes provisions updated by the OBBBA Act passed in 2025. To find out if your stock qualifies for these tax advantages, it’s best to consult with a tax professional who can guide you through the specifics.