Published on

July 11, 2026

If your fintech is growing, compliance can fail before revenue does. More volume, more states, and more bank-partner scrutiny can turn manual checks into delays, audit issues, and deal risk.

Here’s the short version: I’d build the program around risk assessment, clear control owners, written records, and board review before growth puts pressure on the team. That means covering core areas like AML/BSA, OFAC, KYC/KYB, UDAAP, complaints, privacy, cybersecurity, and bank-partner oversight from the start.

A few facts from the article make the point fast:

If I were summarizing the whole piece in one checklist, it would be this:

The main idea is simple: growth should add configuration, not force a full rebuild of compliance. The article explains how I’d set up that system in a way that holds up under new products, new markets, and more transaction volume.

Once the main risk areas are clear, the next step is to turn them into controls, owners, and evidence.

The risk assessment is what drives controls, ownership, and documentation.

For a growth-stage fintech, a practical setup uses one shared taxonomy across product, customer segment, geography, and channel. It should cover regulatory, operational, fraud, cyber, privacy, vendor, and reputational risk. It also needs to show the U.S. rules that apply and the workflows those rules touch. Use the same scoring factors each time, such as transaction volume, average ticket size, customer risk profile, cross-border elements, cash intensity, and product complexity. That way, the assessment can be updated without rebuilding the whole thing from scratch. [2][1]

The main output is a risk register. Think of it as a working log where each row describes one risk scenario. For example: ACH payments for SMB customers in California through API partners. Each row should show the inherent risk rating, the rules affected, current controls, control owner, residual risk rating, and testing frequency. Update it at least once a year, and again when you launch a new product or enter a new state. Ownership should sit clearly with the CCO or similar lead.

Each product should then be mapped to the rules, workflows, and control owners it sets off. For payments, that usually means BSA/AML, OFAC, and state money transmitter laws tied to KYC onboarding, transaction monitoring, and sanctions screening. For lending, TILA, ECOA, FCRA, and UDAAP connect to credit decisioning, adverse action notices, and servicing. For embedded finance, add bank partner contract requirements, third-party risk management standards, and GLBA data-sharing duties. Start with the areas where inherent risk and regulatory impact are highest. In plain English: if a product is high-volume, consumer-facing, and has tricky terms, it should get controls before a lower-risk pilot.

That register then feeds policies, testing scope, and control ownership.

An effective CMS has five parts: policies and procedures, training, monitoring and testing, issue management, and regulatory change management. [5][7][9] The aim is simple: when a new product or market comes in, it should fit into the setup you already have instead of forcing a full rebuild.

Keep enterprise-wide policies at the center, then layer in product-specific procedures for workflows, thresholds, and escalation paths. If you add a new payment rail or lending product, you should be writing a new procedure, not rewriting the core policy.

High-risk activities and customer segments need more frequent testing. Rule-based monitoring, reconciliations, and exception reports are good places to automate. Manual sampling still has a place, especially in the highest-risk areas where human judgment matters.

Regulatory change management is one of those things teams often push off early, then regret later. Track federal, state, and bank-partner changes, assess the impact, and log each update to policy, training, and controls. [6][8]

Use a risk-and-control matrix, or RCM, to connect each risk to its rule, control, owner, testing frequency, and evidence. When a new product launches, you should be able to add rows to the RCM instead of inventing a new system. [3][4][8]

These CMS elements become the source of truth for ownership, testing, and escalation reporting.

Strong documentation makes bank, investor, and regulatory reviews move a lot faster.

At a minimum, a growth-stage fintech should maintain the following set of documents:

| Document | Purpose |

|---|---|

| Policy and procedure library | Current and prior versions of compliance policies and related procedures, with approval dates and review logs |

| Risk register and RCMs | Risk assessments, risk-and-control matrices, and change logs tied to new products or new rules |

| Control owner / RACI mappings | Shows who is responsible, accountable, consulted, and informed |

| Monitoring and testing results | Test plans, sampling methods, findings, and remediation status |

| Incident logs | Security incidents, operational failures, fraud events, compliance breaches, root-cause analyses, and remediation actions |

| Customer complaints records | Central log with categorization, timeliness metrics, and trend analysis |

| SAR and escalation records | Alert investigations, decisions, SAR filings, and escalation chains where BSA/AML applies |

| Issue and remediation tracker | Open issues, risk ratings, owners, deadlines, remediation plans, and completion status |

Keep policies, risks, controls, tests, and evidence in one role-based system with version control and standard naming. [6][8]

This central record also feeds the operating model and board reporting.

Fintech Compliance Operating Models: Centralized vs. Federated vs. Transaction Monitoring Architectures

Once you have a risk register and control matrix, the next step is simple: decide who owns each control, who checks it, and what happens when something goes wrong. This is the execution layer. It turns the risk register and control matrix into day-to-day work.

Use a light three-lines-of-defense model so every control has an owner, a reviewer, and a clear escalation path.

The first line - product, operations, and customer support - handles daily control execution. These teams run KYC procedures, work sanctions alerts, manage fraud queues, and follow documented escalation steps. The second line - the CCO and AML/BSA Officer - sets policy, interprets U.S. rules such as BSA/AML, OFAC, Reg E, and UDAAP, and independently checks whether first-line controls are working.[18][14] The third line - internal audit or an external firm - tests both the first and second lines from time to time and reports findings straight to the board or audit committee. If there is no internal audit team, bring in an external firm once or twice a year.[18][13]

Each role should have written ownership that regulators and bank partners can review:

| Role | Core Responsibilities |

|---|---|

| CCO | Owns the CMS; sets policies; has direct access to the CEO and board; coordinates across product, engineering, ops, and finance |

| AML/BSA Officer | Runs the AML program; sets CDD/EDD standards; manages SAR filings and OFAC screening; reports directly to the board on AML matters[10] |

| Operations leads | Execute KYC workflows, sanctions and fraud alert processing, complaints management, and customer communications |

| Product managers | Build compliance into product requirements documents, including disclosures, consent flows, and jurisdiction-specific settings, before development starts |

| Engineering/data teams | Put technical controls in place - KYC integrations, sanctions screening, access controls, audit logs - under change control with compliance sign-off |

| Finance | Reconcile transaction data, track fraud loss ratios, estimate exposure during escalations, and support compliance budgeting |

The CCO should have direct access to the CEO and board. That independence lets compliance surface concerns without commercial pressure getting in the way.[18]

Once ownership is clear, set the minimum control group each team must run.

The controls that usually break first at scale are the ones still being handled by hand. More volume can swamp oversight fast.

At onboarding, require CIP collection, identity verification, OFAC screening, and fraud checks. Apply CDD/EDD to higher-risk customers. Risk-based CDD and EDD should apply to higher-risk segments - crypto-related businesses, money service businesses, and foreign politically exposed persons - with added documentation and approval steps built into the workflow, not treated as one-off exceptions.[15][19][22]

For ongoing activity, use transaction monitoring for structuring, velocity, and high-risk geographies. Screen payments on a continuous basis, and manage cases with standard templates and SAR rules. Fraud management should add velocity limits, multi-factor authentication for high-risk actions, and manual review queues for suspected account takeover events. Complaints handling needs one intake point, issue-type categorization, root cause tracking, and written resolution timelines that meet Reg E requirements for consumer accounts.

When you think about automation, start with the controls that are high-volume and rule-bound: sanctions screening, basic KYC verification, and transaction threshold alerts. Case management automation - audit trails, routing, investigation templates - is also an early, high-impact investment because it helps operations and audit readiness at the same time.[12][17][22]

Access controls and vendor oversight complete the baseline. Least-privilege access, segregation of duties, and audit logs that show who changed what and when are basic requirements. If vendors handle KYC, transaction monitoring, or card processing, you need documented due diligence, SOC report reviews, and contractual SLAs for data protection. Even when work is outsourced, regulators still hold the fintech responsible.

Those controls should be set up in a way that can grow with the business, without forcing a full rewrite of the operating model.

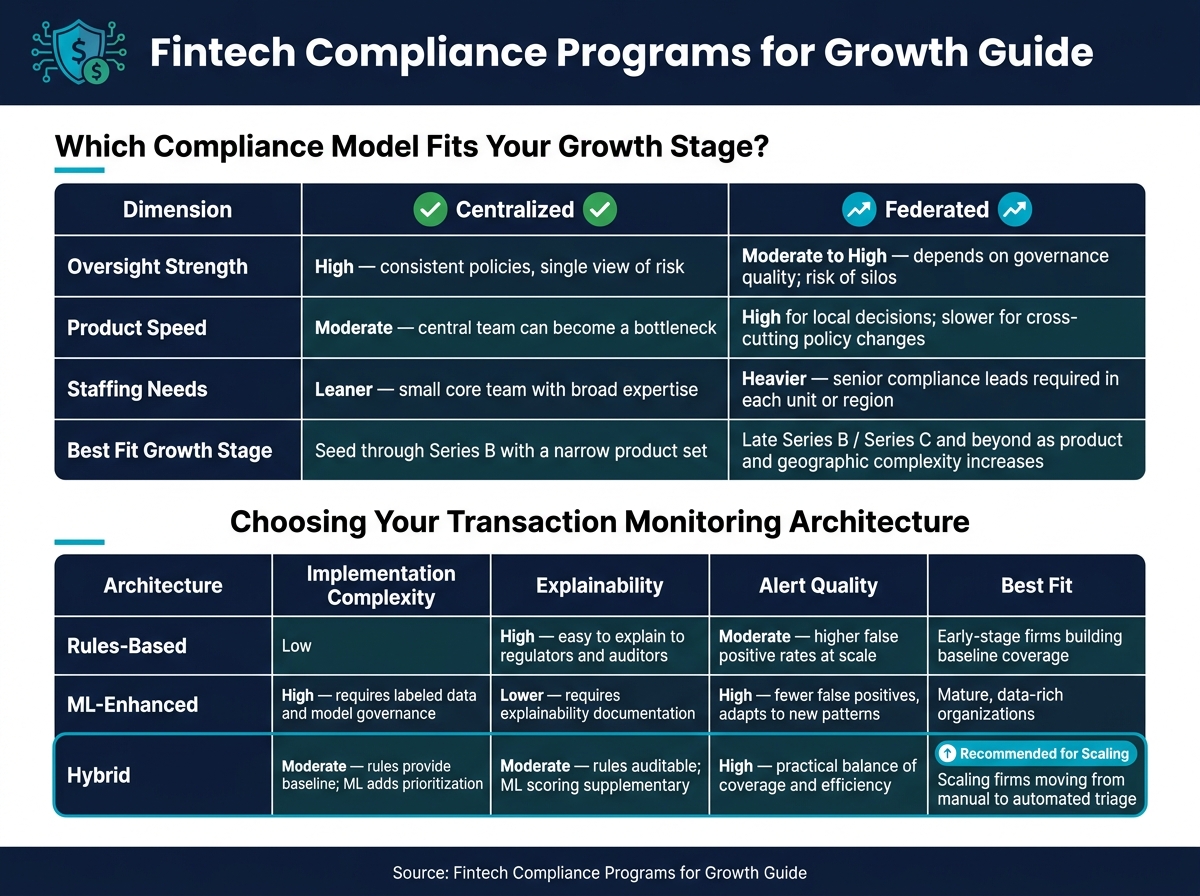

Start with a centralized model. Move to a federated one when product lines, geographies, or bank-partner demands make local ownership necessary. A small team under the CCO can usually cover all products and geographies when the product set is narrow. That model starts to strain when the company runs multiple business lines with different risk profiles - say, consumer lending alongside B2B payments - or expands into states with materially different licensing rules.[11][16][20]

At that stage, a federated model places compliance leads closer to each product line or region, while a central function keeps control of standards, policy ownership, and board reporting. There’s a trade-off here. Federated models can move faster at the local level, but they also need more senior compliance staff and tight governance so policy doesn’t get interpreted five different ways.

| Dimension | Centralized | Federated |

|---|---|---|

| Oversight strength | High - consistent policies, single view of risk | Moderate to high - depends on governance quality; risk of silos |

| Product speed | Moderate - central team can become a bottleneck | High for local decisions; slower for cross-cutting policy changes |

| Staffing needs | Leaner - small core team with broad expertise | Heavier - senior compliance leads required in each unit or region |

| Fit by growth stage | Seed through Series B with a narrow product set | Late Series B / Series C and beyond as product and geographic complexity increases |

The shift usually happens for one of three reasons:

For transaction monitoring, the architecture choice tends to follow a similar path:

| Architecture | Implementation Complexity | Explainability | Alert Quality | Best Fit |

|---|---|---|---|---|

| Rules-based | Low - deterministic thresholds and scenarios | High - easy to explain to regulators and auditors | Moderate - higher false positive rates at scale | Early-stage firms building baseline coverage |

| ML-enhanced | High - requires labeled data, model governance, and technical expertise | Lower - requires explainability documentation for regulators | High - fewer false positives, adapts to new patterns | Mature, data-rich organizations |

| Hybrid | Moderate - rules provide baseline; ML adds prioritization layer | Moderate - rules remain auditable; ML scoring is supplementary | High - practical balance of coverage and efficiency | Scaling firms moving from manual alert review to automated triage |

The hybrid approach is often the most practical option for scaling firms.[21][17] Rules cover the regulatory baseline and help keep auditors comfortable. ML scoring then sits on top and helps teams decide which alerts analysts should review first, cutting down the manual workload without replacing the rule set.

Match the model to your current level of complexity, then review it again as product lines and geographies expand.

Scaling compliance means adding configuration, not rebuilding the program as products, markets, and volume grow. Once controls and ownership are set, the next move is making sure they hold up with each launch.

For growth-stage fintechs, a three-tier model is usually the most practical setup. Tier 1 covers low-risk, domestic consumer accounts with limited product functionality. Tier 2 is the default for most customers: full identity verification, beneficial ownership for business accounts, and standard transaction monitoring. Tier 3 is for higher-risk profiles - politically exposed persons, complex corporate structures, high-risk industries, or ties to jurisdictions with known AML deficiencies - and adds source-of-funds checks, adverse media screening, tighter monitoring rules, and more frequent reviews, often every 6–12 months.[25][27]

The way this scales is pretty simple: put the tiers into policy and build templated workflows around each one. That keeps each new launch from turning into a one-off project. For example, a consumer-wallet fintech moving into SMB accounts can reuse Tier 2 logic, then layer on beneficial ownership, business registry checks, and business-pattern monitoring. A cross-functional launch committee can review a short control memo that maps the product to a tier, notes any added risk, and records go-live sign-off. That gives bank partners or regulators a clean audit trail.[3]

Of course, tiers on paper aren't enough. You also need metrics that show when risk is climbing or when controls are starting to slow growth.

A compliance program that can't measure itself won't scale well. The core dashboard should cover the full customer lifecycle and show both risk and efficiency in one place.

| Metric Category | Key KPIs | Why It Matters |

|---|---|---|

| Onboarding | Approval rates, manual review volume, abandonment rates | Drops in approvals or spikes in referrals can point to rules that are too conservative. |

| AML/BSA | Alert volumes, false-positive rates, SAR filing rates | False-positive trends help tune rules and staffing. |

| Operations | Case aging by bucket (0–2 days, 3–7 days, 8+ days), backlog volume | Backlogs can create reporting risk. |

| Consumer Protection | Complaint volume by category, resolution timelines | Spikes in one category can point to product or training gaps. |

| Governance | Training completion rates, audit/partner findings, policy exceptions | Shows repeat control weaknesses and internal readiness. |

Recurring issues should feed into one register so repeat failures across new products or markets show up in one place.[3][26]

Escalation triggers should be set ahead of time. A 20% spike in suspicious activity alerts, any regulatory inquiry or Matters Requiring Attention (MRA) from a bank partner, or a breach of internal risk appetite limits should automatically route to Compliance leadership and, when needed, the board.[3] Management should also tie risk appetite thresholds to automatic actions - for example, pausing a rollout if metrics cross preset limits - so issues in new-market activity sit side by side with legacy operations.[3][24][28]

These same metrics should shape staffing plans, vendor spend, and rollout timing. If alert volume jumps, the answer shouldn't be guesswork.

Transaction volume drives alert volume. Alert volume drives staffing needs and vendor spend. That's why the key links are transaction-level data feeds into monitoring systems and forward-looking volume forecasts that let compliance model how many alerts, cases, and staff hours a new product or market is likely to create before launch. Review compliance KPIs each month alongside revenue and transaction forecasts, then roll that output into quarterly board materials.[3][23]

These reports become the core inputs for board review and escalation.

Scalable compliance starts with governance, not software. Tools matter, but board review is what turns dashboards and metrics into actual decisions.

For a growth-stage fintech, a good rhythm is monthly management reporting and quarterly board or committee reviews, with ad hoc escalation for high-severity issues. Board materials should stay high-level and focused on decisions. That usually means:

The board doesn’t need day-to-day operating detail. Management should own that. The board’s job is to answer three simple questions: Does the program work? Is it staffed and funded for growth? Do unresolved issues need action? That keeps the board focused on risk without getting buried in operations.

Some matters shouldn’t sit around until the next scheduled meeting. Suspected BSA/AML control failures, sanctions screening breakdowns, data privacy or cybersecurity incidents with regulatory impact, repeat audit or testing failures, consumer complaints, bank-partner concerns, missed regulatory filing deadlines, or an overdue high-risk remediation item should go to the board fast. If something needs a budget change, policy exception, or executive call, escalate it right away.

The split between oversight and execution is what keeps a compliance program independent and effective. If the board tries to run the program itself, it loses distance. If it stays too hands-off, early control problems can slip by.

| Area | Board Responsibility | Management Responsibility |

|---|---|---|

| Policy approval | Approves the compliance framework and key policies | Drafts, updates, and trains employees on policies |

| Risk appetite | Sets and reviews risk appetite at least annually | Aligns controls, staffing, and monitoring to approved limits |

| Issue escalation | Receives high-severity issues promptly and challenges management on gaps | Self-identifies issues and escalates them per defined thresholds |

| Staffing and budget | Ensures the compliance function has adequate independence and resources | Manages headcount, vendor spend, and capacity planning |

| Control design | Reviews whether the control framework is appropriate for the business | Designs and operates controls, procedures, monitoring, and testing |

| Testing follow-up | Reviews testing results and remediation status | Runs QA and independent testing and closes findings on time |

| Partner communications | Reviews major partner issues and oversight outcomes | Manages day-to-day partner monitoring, audit responses, and communications |

| Growth alignment | Requires capacity assessments before approving major expansion | Presents staffing, tooling, and control-coverage plans before launch |

Once roles and review timing are set, the next step is simple in theory and hard in practice: keep growth tied to capacity.

The main thread across this guide is straightforward. Build the governance structure before volume backs you into a corner. Start with a risk assessment that covers products, customers, geographies, and channels. Put a documented compliance management system in place with clear owners and written policies. Automate high-volume controls before manual review turns into a choke point. Set up reporting that reaches leadership on a fixed schedule, not only when something goes wrong.

The companies in the best position to avoid enforcement actions treat compliance as a standing governance issue. It sits on risk assessment, control ownership, and testing, then goes up to the board for review and gets funded before the pressure hits. Founders should tie every expansion plan to staffing, controls, and testing. If that capacity isn’t there, growth will outpace the program.

Fintech firms should put formal compliance in place as early as they can. Doing that helps cut risk, avoid penalties, and build trust with investors and regulators.

This matters even more for growth-stage companies. When a company scales without a clear framework, it can end up with data gaps and compliance problems that are far harder - and more expensive - to fix later, especially before funding, a new market launch, or an audit.

Start with controls tied to high-volume data and critical risk areas. Put automated data collection in place for transaction monitoring and customer details. Then use risk analytics for real-time threshold tracking and suspicious activity flagging.

Next, add automated workflow approvals, reconciliation checks, secure API gateways, and system-generated audit trails. These controls help support accurate reporting, protect working capital, and keep your team audit-ready as volume grows.

Review compliance on a tiered schedule, with monthly internal reviews, quarterly assessments, and annual external validations under board oversight.

The board should also be ready to call for interim reviews when major changes happen, such as new product launches, market expansions, or major regulatory updates.