Published on

July 11, 2026

If cash is tight, supply chain finance changes timing more than profit. I look at it this way: if you buy inventory on Net 30, get paid by retailers in 45 to 60 days, and hold stock for weeks, your cash gets stuck in payables, inventory, or receivables.

Here’s the short answer:

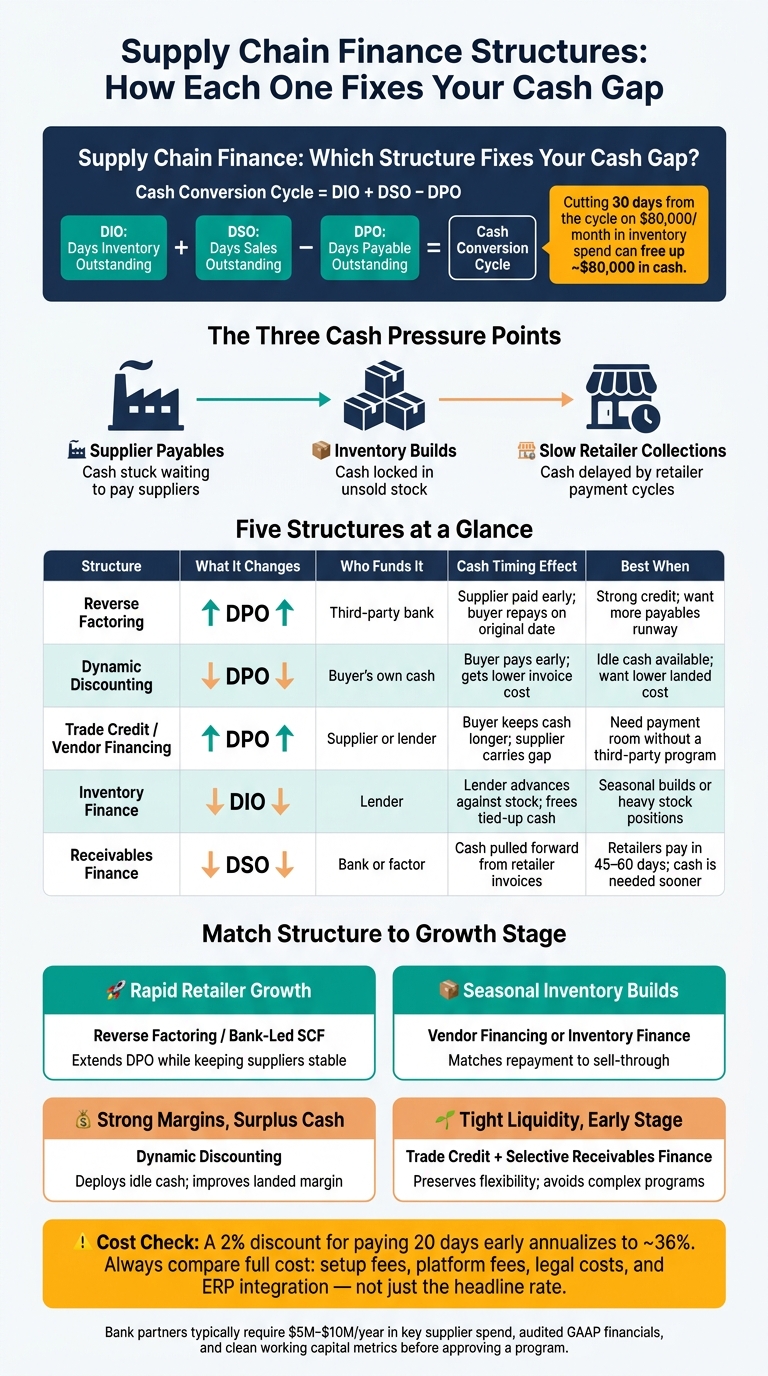

The math is simple: Cash Conversion Cycle = DIO + DSO − DPO. If a brand cuts 30 days from that cycle on $80,000 of monthly inventory spend, it can free up about $80,000 in cash.

Supply Chain Finance Structures: How Each One Fixes Your Cash Gap

| Option | What it changes | Best when |

|---|---|---|

| Reverse factoring | DPO | I want more time to pay without squeezing suppliers |

| Dynamic discounting | DPO goes down | I have extra cash and want lower invoice cost |

| Trade credit / vendor financing | DPO | I need more room before payment is due |

| Inventory finance | Inventory funding | I need cash tied up in stock |

| Receivables finance | DSO goes down | Retailers pay too slowly |

My takeaway: the right setup depends on where cash is getting stuck. If the problem is supplier payments, I focus on DPO. If the problem is slow retailer collections, I focus on DSO. If too much money sits in stock, I look at inventory funding. The rest of the article walks through those choices in plain English.

The next step is figuring out which setup lines up with your cash gap. For consumer brands, the squeeze usually shows up in one of three places: supplier payables, inventory builds, or slow retailer collections.

| Structure | Starts With | Who Funds It | Cash Timing | Cost / Tradeoff | Best-Fit Use Case |

|---|---|---|---|---|---|

| Reverse Factoring | Buyer | Third-party bank or financier | Supplier gets paid early; buyer repays on the original due date or an agreed extension | Financing spread tied to the buyer's credit profile | Brands with strong credit that want to preserve cash |

| Dynamic Discounting | Buyer | Buyer's own cash | Supplier gets paid early; buyer pays sooner | Early-payment discount in exchange for faster cash outflow | Brands with idle cash seeking a lower net invoice cost |

| Vendor Financing | Supplier or lender | Supplier or lender | Supplier or lender extends payment terms; buyer preserves cash, supplier or lender carries the gap | Supplier-financed terms can lead to higher prices | Extending payables without a third-party program |

| Trade Credit | Supplier | Supplier | Buyer pays on agreed net terms | No explicit fee; payment due on standard terms | Everyday inventory purchases and production runs |

| Inventory Finance | Buyer | Lender | Lender advances against stock; frees cash tied in inventory | Interest on the advance; collateral required | Seasonal inventory builds and large stock positions |

| Receivables Finance | Buyer | Bank or factor | Lender advances against approved invoices; pulls cash forward from retailer payments | Discount or fee on the advance amount | Brands waiting on slow retailer payment cycles |

At a simple level, the choice comes down to this: do you want to preserve payables, fund inventory, or pull receivables forward?

Reverse factoring raises DPO. Your brand sets up a facility with a bank or fintech lender. Once you approve a supplier invoice, the financier pays the supplier early at a rate based on your credit profile.

You then repay on the original due date or on an agreed extension. That means more runway for your cash, while suppliers get paid sooner. It's a classic win-if-structured-well setup for brands with solid credit.

Dynamic discounting lowers DPO. You pay earlier in exchange for a lower net invoice cost.

The tradeoff is pretty straightforward: you use your own cash sooner. So this works best when idle cash would do more for you through supplier discounts than sitting in the bank.

Standard trade credit stretches DPO without third-party funding. A supplier ships goods and gives you net 30 or net 60 to pay, which raises DPO modestly within agreed terms.

Vendor financing takes that a step further. In that setup, a supplier or lender carries longer terms on your behalf, so your business keeps cash longer while they carry the gap. Of course, that cost doesn't just disappear. Over time, it can show up in higher prices.

Inventory finance supports DIO by turning stock into working cash before it sells. That's often useful during seasonal inventory builds or when stock positions get heavy.

Receivables finance lowers DSO by advancing funds against retailer invoices, instead of making you wait through a 45- or 60-day payment cycle.

Once the structure is picked, the next move is setting supplier groups, discount terms, and approval rules.

Once you’ve picked the structure, the next step is simple: decide who gets early payment, what it costs, and what approval rules apply.

Start with the goal. Maybe you want to extend payables runway. Maybe you want to help suppliers that are short on cash. Or maybe you’re trying to make a term change work better on both sides. That choice shapes the whole program.

Then group suppliers based on two things:

Early payment tends to matter most for small, strategic suppliers that don’t have strong bank access. Vendors with plenty of cash usually don’t get as much from early payment.

There’s also a catch here. Longer terms can push suppliers to ask for higher prices, which can wipe out the working-capital gain.

That’s why segmentation matters. It should guide which suppliers get early-payment offers and what terms each group receives.

Set unit pricing first. Then handle payment terms or early-payment discounts as a separate discussion.

That separation matters. If pricing and terms get mixed together, the cash gain can disappear into a higher unit cost. You want the benefit to show up in DPO, not in the price of the goods.

When you review terms, compare the supplier’s effective financing cost, not just your own borrowing rate. And be careful about pushing terms past Net 60. Costs for suppliers tend to climb fast after that point.

Use one approval workflow so only approved invoices enter the program. That gives you a more predictable setup and cuts down on surprise cash outflows.

Once terms are in place, the program needs to show up in weekly cash forecasts.

Build early-payment outflows into the forecast before the cash leaves the bank account. Then track unit prices before and after term changes. That helps you see whether the cash gain is holding up or getting eaten away by price increases.

Good forecasting shows what’s actually happening: whether the program is freeing up cash, or just moving payment timing around.

For growth-stage consumer goods brands, bank-funded SCF mostly helps you keep DPO in place while giving suppliers a way to get paid early. That matters because it can stretch your payables runway without putting suppliers in a cash squeeze.

Banks underwrite the buyer, not the supplier. So before a program goes live, your finance setup needs to be solid. At a minimum, bank partners usually want audited or reviewed GAAP financials, reconciled balance sheets, clean working capital metrics, a steady procure-to-pay process, and clean vendor files with legal names, EINs, payment instructions, and key supplier spend of about $5 million to $10 million per year. Brands with strong FP&A, forecasting, and bookkeeping tend to move through this process with less friction.

Once the structure makes sense, look at the full cost, not just the quoted rate. That headline number is only the first layer. For example, a 2% discount for paying 20 days early annualizes to about 36%. On paper, that can look simple. In practice, the effective cost may be much higher than it first appears.

Then add the rest: setup fees, platform fees, legal costs, and ERP integration expenses. For smaller programs, those fixed costs can push up the effective cost of capital by a lot.

The table below compares the three main structures across the areas that usually matter most to growth-stage brands:

| Dimension | Bank-Funded SCF | Internally Funded Early Payment | Vendor Financing / Trade Credit |

|---|---|---|---|

| Access to Capital | Adds outside liquidity; extends payables without draining cash. Limited by credit approval and volume minimums. | Uses current cash; no new facilities needed. Constrained by internal liquidity. | Available before full bankability; supplier-funded. Limited by each supplier's risk appetite. |

| Flexibility | Helps during inventory spikes. Program parameters can be slow to change. | Terms and discounts can change fast. Flexibility drops when internal cash tightens. | Negotiated supplier by supplier. Fragmented terms make cash planning harder. |

| Complexity | Centralized at scale. Higher legal, technical, and onboarding complexity. | Lower outside complexity. Still needs process changes and monitoring. | Low systems complexity; mostly contractual. Managing many custom arrangements gets harder over time. |

| Supplier Impact | Offers early payment; improves supplier cash flow predictability. Some suppliers may push back on added admin. | Discounts can be tailored; can help relationships. Suppliers may lose early payment if cash swings. | Suppliers are directly involved; may trade better terms for volume. Stretching too far can pressure supplier liquidity. |

| Likely Cost Profile | Often competitive versus unsecured borrowing; tied to the buyer's credit profile. Fees may still run above internal funding cost. | Discount economics stay with the brand; often cheaper when cash is available. Opportunity cost comes into play if that cash could earn more elsewhere. | Explicit costs may be low or buried in pricing. The economic cost often shows up in higher unit prices or weaker terms. |

A bank-funded program that costs a bit more on paper can still be the better move if it protects internal cash during a major retailer launch or a seasonal inventory build. In those moments, tying up cash in supplier discounts can mean passing on growth investments with a better return.

Even a well-planned program can hit rough patches. The most common trouble spots are supplier onboarding resistance, invoice disputes, and payment terms that get stretched too far.

Smaller suppliers, in particular, may look at early payment programs and think, what's the catch? If enrollment feels confusing or the financial upside isn't clear, participation can stall. The fix is pretty simple:

Invoice disputes are easier to miss, but they can do real damage. If approvals move slowly or invoices get flagged too often, early payment doesn't happen on time. And when approvals are late, suppliers notice fast. That weakens trust. Tight procure-to-pay controls and clear approval SLAs are what keep the program working day to day.

There’s also a line brands can cross with payment terms. Pushing terms to Net 60, Net 90, or longer without a working early payment option can quietly put pressure on supplier cash flow. That can lead to supplier pushback, stock-outs, and slower participation in the program.

The right setup depends on where the pressure sits: payables, receivables, or inventory.

From there, the next question is which structure fits your growth stage and cash gap.

Once cost and risk are clear, the next step is fit. You want the structure that lines up with the problem you have right now. Put simply: match each structure to the cash gap it fixes. Each one changes DPO, DSO, or inventory funding in its own way.

When order volume climbs fast, supplier stability matters more than pushing payment terms even further. In this case, bank-led SCF is often the better move. It can extend DPO while helping suppliers stay steady and keeping the relationship on solid ground.[2][1][6]

Big pre-season inventory buys put pressure on DIO in a different way. If cash is tight, vendor financing or inventory finance can help carry that load. If liquidity is less of a problem and margin is the bigger goal, dynamic discounting may make more sense - but only if the discount lifts landed margin.[3][5][8]

When cash is tight and unit economics are still being proven, flexibility matters more than scale. Start with trade credit. Then layer in selective receivables finance for the slowest-paying accounts. Save early payment for suppliers whose disruption would bring production to a halt.[2][4][7]

A rolling 13-week cash forecast should act as the guardrail here. The mix you choose should improve DPO, DSO, or inventory funding without causing a new cash squeeze. If a structure improves the cash conversion cycle, keep it. If it only moves the pressure from one week to another, change it.

Use the matrix below to match the main cash constraint to the right structure.

| Growth Condition | Primary Structure | Why It Fits |

|---|---|---|

| Rapid retailer growth, stretched payables | Reverse factoring / bank-led SCF | Extends DPO while keeping suppliers stable |

| Large seasonal inventory builds | Vendor financing or inventory finance | Matches repayment to sell-through |

| Strong margins, surplus cash | Dynamic discounting | Improves landed margin; deploys idle cash |

| Tight liquidity, early stage | Trade credit + selective receivables finance | Preserves flexibility; avoids complex programs |

Start with your liquidity and day-to-day priorities.

If you have surplus cash and want more profit from it, dynamic discounting lets you earn a return by paying suppliers early.

If you want simplicity and predictability, traditional early payment programs are easier to run.

If cash is tight and you need longer payment terms without putting pressure on supplier relationships, reverse factoring is the best fit.

Beyond the headline interest rate, supply chain finance often comes with extra fees for early payment. In many cases, suppliers pay around 10% to 20% of the invoice value.

That can add up fast.

There’s also the admin side to think about. If the process is clunky, companies can end up with more moving parts in their accounts receivable workflow, which means more complexity and more time spent managing it.

A growth-stage brand often turns to bank-backed supply chain finance when it needs longer payment terms without putting pressure on supplier relationships.

This can free up cash for growth or debt paydown, help the business handle inventory spikes or scale-up periods, and give suppliers the option to get paid early. In some cases, it can stretch payment terms to 120–180 days while helping the company keep day-to-day operations steady.