Published on

July 10, 2026

If I were a U.S. manufacturer picking a new market today, I would not start with the headline tax rate. I would start with import VAT/GST timing, refund delays, product classification, and invoice rules because those are often what squeeze cash flow management and cut margin.

Here’s the short version:

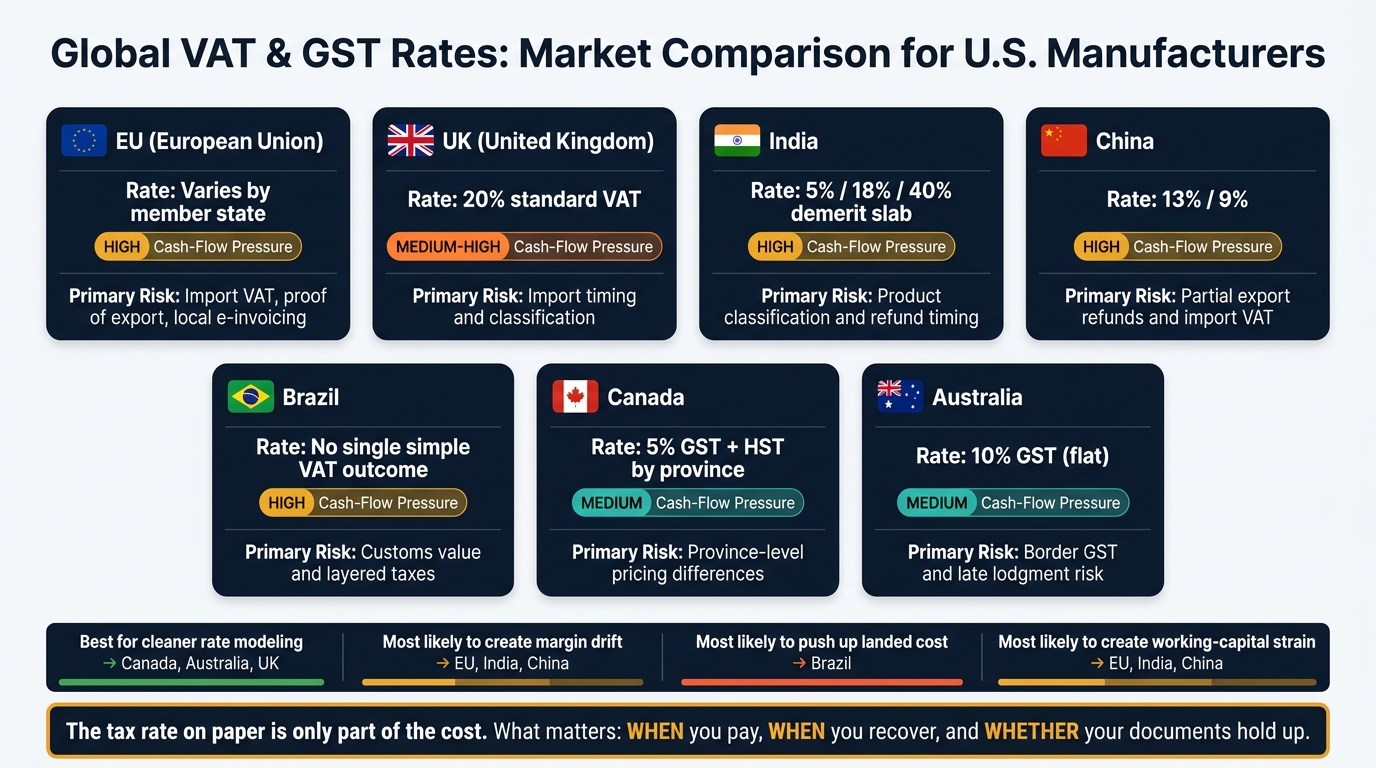

If I had to reduce the whole article to one idea, it would be this: the tax rate on paper is only part of the cost. What matters just as much is when I pay, when I recover, and whether my documents hold up.

Global VAT & GST Rates: Market Comparison for U.S. Manufacturers

| Market | Main rate point | Main risk for manufacturers | Cash-flow pressure |

|---|---|---|---|

| EU | Varies by member state | Import VAT, proof of export, local e-invoicing | High |

| UK | 20% standard VAT | Import timing and classification | Medium-High |

| India | 5% / 18% / 40% | Product classification and refund timing | High |

| China | 13% / 9% | Partial export refunds and import VAT | High |

| Brazil | No single simple VAT outcome | Customs value and layered taxes | High |

| Canada | 5% GST + HST by province | Province-level pricing differences | Medium |

| Australia | 10% GST | Border GST and late lodgment risk | Medium |

A simple way to read this comparison:

So if I were building a market-entry model, I would test rate, refund lag, import tax timing, invoice rules, and channel structure before I trusted any margin forecast.

The EU is a good example of why headline VAT rates don't tell the whole story. For U.S. manufacturers, the harder part is usually local setup, paperwork, and the exact moment goods cross the border. That's what makes the EU one of the toughest VAT systems to deal with.

Most manufactured goods are taxed at the local standard VAT rate. Lower rates and limited zero-rating apply to some basic items, while exports are generally zero-rated. Rates also shift under new directives, so pricing models need to be checked on a regular basis.

At the border, two things matter most: proof that the goods were exported and the timing of the import. Those details can change the actual tax cost more than the stated rate itself.

EU exports to the U.S. are zero-rated, but proof of export is required. If that proof is missing, the tax position can fall apart fast.

Imports now face VAT at entry, and the small-parcel rules changed on July 1, 2026. The €150 customs duty exemption was abolished, a temporary fixed customs duty of €3 per declaration line now applies to parcels under €150, and import VAT may be reported through IOSS for eligible parcels [2].

Import VAT creates a working-capital gap at the point of entry. Managing these complex cash flow challenges often requires the expertise of fractional CFO services to maintain liquidity. That means cash goes out before it can be recovered, which can squeeze margins even when the sale looks fine on paper.

Things get messier with mixed contracts. If a deal includes goods, installation, and service, each part may need its own tax treatment. That can turn a pricing issue into a day-to-day admin problem, especially when invoicing and reporting rules change from one country to another.

ViDA is pushing standardized e-invoicing and digital reporting across the EU, while countries such as Denmark already use local digital invoice standards [1]. In plain terms, one invoice process usually isn't enough.

U.S. manufacturers need ERP systems that can manage country-specific invoicing and reporting rules across member states. If the system can't handle those local differences, errors tend to show up in billing, filings, or both.

Compared with the EU, the UK has fewer VAT rate tiers. That sounds simpler on paper. In practice, manufacturers still run into classification issues, border friction, and refund-timing risk.

Most manufactured goods fall under the 20% standard rate. The 5% reduced rate applies only in a narrow set of cases [3].

UK exports are generally zero-rated, while imports are subject to VAT at the border. If declarations are filed late, that can trigger scrutiny and weaken relief claims [1].

That border timing has a direct effect on cash flow.

The pressure shows up when VAT has to be paid before sales cash arrives. In that case, margin can look fine on paper while cash gets squeezed in the bank account. Model VAT based on payment and refund timing, not just accrual timing, because import VAT can tie up cash and compress free cash flow [4]. Sales channel choice matters too, especially when you're comparing direct sales with distributor models.

Cross-border invoices need the correct VAT number, tax point date, and goods or services description [1].

India stands out because the tax result depends a lot on how the product is classified, not just the top-line GST rate. On September 22, 2025, India changed its GST setup, moving from the old four-tier structure to 5% and 18%, plus a 40% demerit slab[5].

Most manufactured goods sit in either the 5% or 18% slab. Electric vehicles are taxed at 5%, while products such as LED lamps, printing ink, and power-driven pumps fall under 18%[6]. The 40% demerit slab applies to tobacco, cigarettes, and similar sin goods[5].

This matters most at the border. That’s where export refunds and import taxes can shape cash flow in a big way.

Exports are zero-rated. Manufacturers can ship under a Letter of Undertaking (LUT) and recover input tax credit, or they can pay IGST and claim a refund later[1]. Imports face Basic Customs Duty plus IGST, with IGST calculated on the customs value plus duty, which can slow down input credit recovery[1].

One point needs close attention: the inverted duty structure. That happens when GST on inputs is higher than GST on the finished product. India’s GST Council has revised the refund formula for this issue, which matters most for manufacturers in sectors such as electronics, solar energy, and textiles[6].

The 2025 simplification removes some guesswork, but product classification still has a direct effect on margin. If a product is placed in the wrong slab - say 5% instead of 18%, or the other way around - the pricing error can be serious.

The gap between slabs also affects channel strategy. A distributor model and a local-assembly model can lead to different credit timing and refund exposure. So even if the headline tax rate looks simple, the math underneath can shift. Manufacturers still need to monitor CBIC circulars for product-specific rulings[1].

Once the classification changes the rate, it changes the invoice too.

India’s compliance burden depends heavily on getting classification right. For manufacturers, this is not just a tax-planning issue. It’s also an invoicing issue, especially for packaged goods covered by the Legal Metrology Act, 2009[6].

China’s VAT setup looks simple at first glance. But once you factor in export refunds and import taxes, the math gets a lot tighter. In early 2025, China replaced its provisional VAT rules with a formal VAT law. Even so, refund timing and import VAT still play a big part in landed cost and cash flow.

China uses a two-tier VAT system:

China does not refund the full VAT charged on exports. Instead, the refund is 11% for goods taxed at 13% and 8% for goods taxed at 9%, minus a 2% service fee [7].

That gap matters. On a ¥10,000 sale taxed at 13%, the refund comes to ¥1,078, not the full ¥1,300 [7].

Imports bring another cost layer. At the border, most imported manufactured goods face 13% import VAT on top of customs duties. And when extra tariffs kick in, landed cost can jump fast. Some U.S. goods have faced rates as high as 125% [7].

This is where profitability can get squeezed. Since the export refund rate is lower than the VAT paid, exporters need to build that refund shortfall into pricing. They also need to plan for slower cash recovery.

China’s instant refund system, introduced in April 2025, can help cash flow for eligible entities. But many refunds still move through bank transfer, and those can take 7 to 14 business days [7].

That timing can change how a seller thinks about channel mix. It can affect whether direct sales make more sense than working through local distributors [1]. It also means invoice accuracy isn’t just an admin issue. It has a direct effect on cash.

China requires official VAT invoices, or fapiao, for compliance and refund eligibility [7]. China is also moving toward digital invoicing, so businesses need systems that line up with the latest fapiao rules [7].

Brazil is a landed-cost market, not a simple rate-only market.

Brazil’s indirect tax load is shaped less by one VAT/GST-style rate and more by customs valuation plus several import charges. For imports, customs valuation usually starts with the customs transaction value. It can also include sale-linked additions like assists, royalties, and license fees[8]. That affects both import timing and channel pricing.

When the customs base goes up, the taxable amount rises across multiple import charges. In plain English, landed cost climbs before the goods even reach the customer.

A higher customs value can squeeze margin unless you reset pricing.

The commercial invoice, customs declaration, and any sale-linked costs need to line up with the declared customs value[8].

Canada is simpler than a lot of VAT markets. But don't let that fool you. Province-level tax differences still shape pricing, cash flow, and invoicing.

Canada applies a 5% federal GST. In HST provinces, businesses charge one combined rate, and that rate changes by province. For example, Nova Scotia's HST is 14% effective April 1, 2025 [1].

That matters most when you're setting prices and issuing invoices. A single national quote can lead to different net results depending on the province. So tax systems need to track provincial rates in real time.

Exports are generally zero-rated. That means registered businesses can usually still recover input tax through ITCs.

Imports work differently. GST/HST is charged at the border. In practice, import GST gets paid first and recovered later, which can tie up cash.

Province-by-province rate differences can squeeze margins and create friction with channel partners when companies use one national price across Canada.

Invoices need to match each transaction to the correct provincial rate. The main challenge is keeping track of the right province-level rate, plus any sector-specific exemption that changes tax treatment and ITC recovery.

Australia’s GST system is fairly simple on paper: one standard rate, no lower-rate bands, and a small group of GST-free or input-taxed supplies. For U.S. manufacturers, the main headache usually isn’t working out the rate. It’s handling compliance and managing cash flow.

Australia applies a flat 10% GST to most goods and services. Some supplies are GST-free or input-taxed, but there aren’t any reduced rates.

For manufacturers, what happens at the border often matters more than the headline rate. Exports are GST-free. Imported goods can trigger GST at the border, and registered businesses may recover that amount later through input tax credits. If remittance is late, director penalties can apply.

That border setup tends to affect cash timing more than pricing logic. Even with a flat 10% rate, late GST payments and slow recovery can increase the actual cost of capital.

Australia requires GST-compliant tax invoices and on-time lodgment. Late filing can trigger Director Penalty Notices and personal liability [9]. In practice, invoice accuracy and lodgment timing are part of margin control, not just a compliance task.

These tax systems shape margin, cash flow, and compliance cost. For a U.S. manufacturer, the differences can show up fast in pricing, invoicing, and landed-cost planning.

| Market | Key Pros | Key Cons | Margin Risk |

|---|---|---|---|

| EU | Reduced-rate eligibility can support pricing flexibility for certain goods; exports are zero-rated when documentation is sound | EU rate changes and digital reporting keep planning in flux | Shifting reduced-rate eligibility rules can create pricing uncertainty |

| UK | One national VAT regime is easier to model than layered local taxes | Late import declarations and tariff classifications can trigger penalties [1] | Import timing and classification errors can disrupt landed-cost planning |

| India | Lower GST rates on certain goods can improve competitiveness | Product classification can push goods into a higher GST slab | Misclassification can erode margin and distort invoices |

| China | Export refunds support outbound pricing | Refund timing and rule changes add compliance friction | Refund lag can tighten cash flow and affect channel choice |

| Brazil | State-level tax differences force market-by-market pricing | Layered taxes and state variation make pricing and filing harder | Layered taxes and state variation can cascade into higher landed cost |

| Canada | Federal GST is standardized, but provincial HST still changes pricing by market | Province-by-province rate changes complicate national quoting and invoicing | Regional rate changes can disrupt national pricing consistency |

| Australia | Flat 10% GST simplifies pricing; exports are GST-free | Border GST and lodgment rules create cash-flow and filing risk | Import GST and late filing can tie up cash and trigger penalties |

The big split is pretty simple: some markets use cleaner GST systems, while others create margin pressure through classification rules, refund timing, or state-by-state variation.

Canada stands out here as one of the easier GST setups in this group. The federal framework is standardized, which helps. That said, manufacturers still have to price around provincial HST differences instead of leaning on one national average.

Australia is similar in that its flat 10% GST makes pricing easier to map out. But “simple” doesn’t mean hands-off. Border GST and lodgment timing still need close attention, especially if cash flow is tight.

Rate design matters most when it changes the tax on the product itself, not just the headline rate in the market. That’s where the EU, India, and China can get tricky.

In the EU, reduced rates can help with pricing, but the rules don’t always sit still. Member states including Greece and Romania have been warned for non-compliance with VAT directives, which adds uncertainty around reduced-rate eligibility [1]. For a manufacturer, that can turn pricing into a moving target.

India has a similar issue, but it shows up through GST slabs and classification. The CBIC has issued specific clarifications for items like ready-to-eat popcorn, pepper, and raisins to determine the correct GST treatment [1]. That’s not just a paperwork issue. If a product lands in the wrong category at scale, margin can slip little by little until the damage is hard to ignore.

China adds another wrinkle: export refunds. Those refunds can support outbound pricing, which sounds good on paper. The catch is timing. If refunds are delayed or rules change, cash can get stuck in the system longer than expected, and that can affect channel decisions.

Compliance gets heavier when rates, refunds, and invoice rules shift by product or by region. Brazil is the clearest case. Layered indirect taxes and state-level variation make filing and pricing harder to standardize across the country.

India also needs close watching because CBIC classification updates can change the tax treatment for specific goods [1]. For manufacturers moving into either market, compliance infrastructure shouldn’t be treated as a side cost. It needs to be part of the market-entry financial model from day one.

Once you compare rates market by market, the next step is to turn those differences into forecast inputs. For most teams, that means modeling six things: the statutory VAT/GST rate, any reduced or zero-rated treatment for the product category, import tax timing and refund lag, invoice format rules, and channel-specific tax recovery assumptions.

That last point matters more than it may seem at first glance. Channel choice changes tax recovery timing. Selling through a distributor versus selling direct can change how tax is recovered and when the cash comes back.

These inputs shape margin, cash timing, and invoice treatment. Import VAT can remain unrecovered for weeks or months. And in markets with strict proof-of-export and refund rules, the effective cost of selling can end up higher than the statutory rate.

Channel mix can make that even more pronounced. A direct sales model gives you more control over invoice design and tax recovery records. A distributor model can make local compliance easier, but it can also leave you with less visibility into whether zero-rating or reduced-rate eligibility is being applied the right way at the transaction level.

Phoenix Strategy Group works with growth-stage manufacturers to model VAT/GST rates, refund timing, landed cost, and channel impact directly into FP&A and cash flow forecasts before market entry.

The main takeaway isn't just the rate. It's how each tax system shapes pricing, cash flow, channel mix, and invoicing.

| Market | Primary Decision Lens for U.S. Manufacturers |

|---|---|

| EU | Model SKU-level reduced rates, zero-rating, and country-specific invoicing |

| UK | Watch import declaration timing, classification, and invoice details |

| India | Map GST by product category and classify correctly |

| China | Model export refund lag, import VAT, and fapiao rules |

| Brazil | Build landed cost from customs value and layered import taxes |

| Canada | Price by province-level HST, not a national average |

| Australia | Account for border GST and lodgment timing |

The statutory rate is rarely the number that creates the biggest problem. More often, it's the refund lag, the documentation gap, or a tricky classification issue that catches manufacturers off guard. Model those first.

There’s no one market that’s always the easiest to model for VAT or GST. Tax complexity swings a lot from country to country, and the rules can change fast.

That’s the core challenge. A setup that works for Germany may not fit Singapore, and Brazil can be a different beast altogether. Each market has its own tax logic, filing rules, and edge cases.

Because tax laws vary across places like Germany, Singapore, and Brazil, businesses need a standardized approach and continuous monitoring to model them well across jurisdictions.

Import VAT and delayed refunds can put real pressure on cash flow. That’s especially true during big moments like asset purchases or supply chain integration, when working capital is already stretched.

If a business pays VAT at import and doesn’t get it back on time, the result is a liquidity gap. In plain English, cash goes out and stays tied up longer than expected. That can make assets look more expensive than they are on paper and create friction across day-to-day operations.

A few basics can help lower that risk: proper classification, timely VAT registration, and a smooth recovery process. When those pieces are in place, businesses are in a better position to avoid cash getting stuck at the border.

Product classification matters because it decides the VAT, GST, or customs duty rate applied to your goods. Use the wrong HS or HTS code, and you may pay too much or too little tax. Either way, you're taking on financial and legal risk.

Those taxes also feed straight into landed cost. So if a product is misclassified, your COGS can climb fast. And if you can’t pass that extra cost on to customers, your gross margin gets squeezed right away.