Published on

July 1, 2026

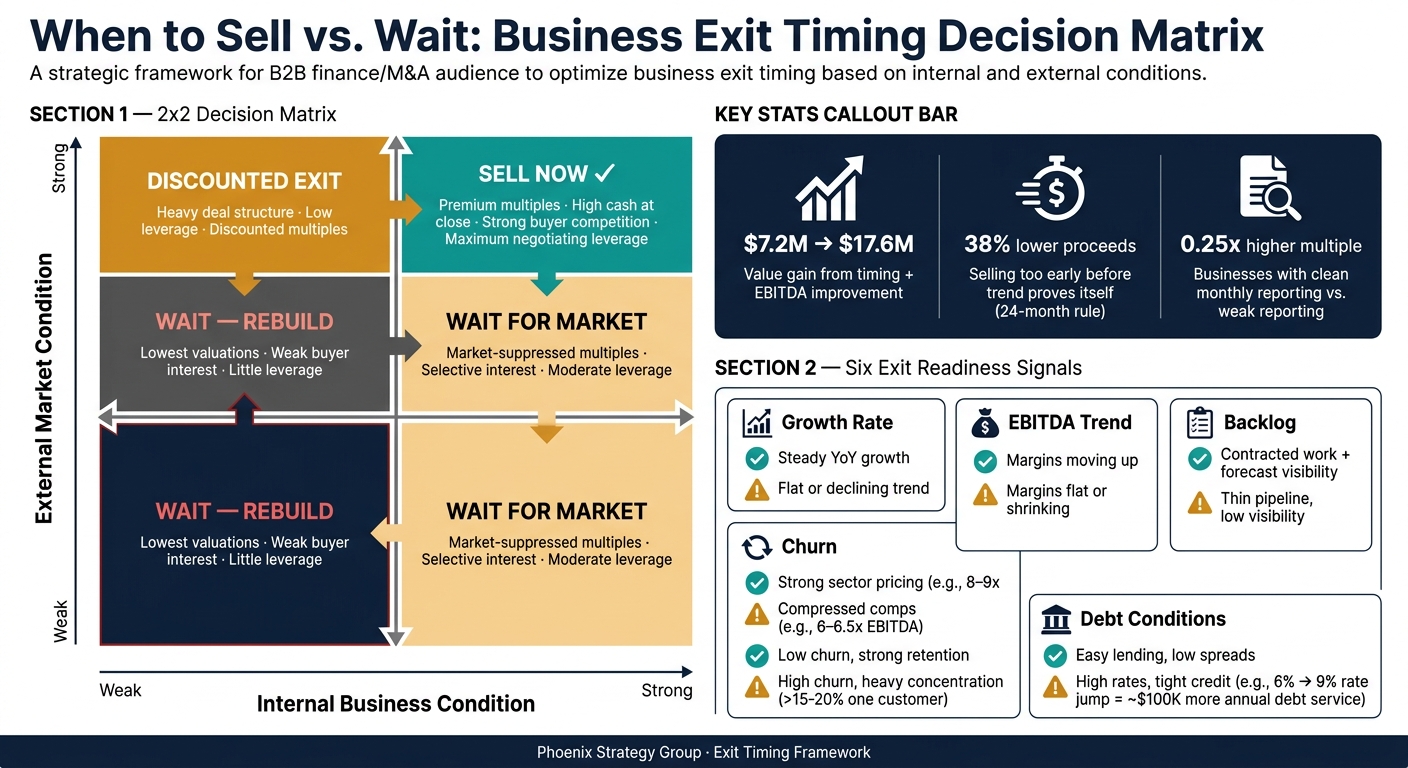

Exit timing can change your sale price by millions. In the example from the article, a business moved from $7.2 million in value to $17.6 million just by improving EBITDA and selling in a better market window.

If I were deciding whether to sell, I’d keep it simple:

The article comes down to six checks:

A buyer is not just paying for what the company did last year. A buyer is paying for what they think the company will do after closing. That is why timing affects not only price, but also terms.

| Signal | What I’d want to see | What it usually means |

|---|---|---|

| Growth rate | Steady year-over-year growth | More buyer comfort |

| EBITDA trend | Margins moving up | Better pricing power |

| Backlog | Contracted work and forecast visibility | Less buyer doubt |

| Churn | Low churn, solid retention | More confidence in future revenue |

| Market multiples | Strong sector pricing | More bid pressure |

| Debt conditions | Easier lending, lower spreads | Buyers can pay more |

Bottom line: the best time to sell is when business performance, market demand, and founder readiness line up at the same time. If even one of those is off, deal terms can get worse fast.

That’s the lens I’d use for the rest of the article: Is the window open now, or is there more money in waiting 12 to 36 months?

Buyers don't pay for the past. They pay for the cash flow they expect after the deal closes. That's why momentum shapes both valuation and deal terms.

When revenue is climbing and EBITDA margins are getting better, buyers can forecast future cash flows with more confidence. And that usually shows up in two places: higher EV/EBITDA multiples and more cash at close. If performance is flat or slipping, buyers tend to protect themselves. They shift more of the deal value out of the upfront payment and into earnouts, seller notes, and tighter indemnity terms.

In early 2026, a regional outpatient diagnostics group with clean financials and strong growth momentum drew four competing offers between 8x and 9x EBITDA, which led to a $36 million exit with a minimal earnout and just 10% equity rollover [2]. The flip side is just as telling. A similar business that waited and entered a cooler private equity market got a top offer closer to 6.5x EBITDA, with 30% of the value tied to multi-year earnouts [2].

Clean accrual-based financials covering the last 24 to 36 months, along with third-party QoE support, can cut down on buyer pushback [4][8].

Here's the pattern in plain English [5][2]:

| Performance Trend | Valuation Multiple | Deal Structure | Buyer Behavior |

|---|---|---|---|

| Accelerating Growth | Premium (e.g., 8.5x EBITDA) | High cash at close; minimal earnouts | Competitive tension; aggressive bidding |

| Flat Performance | Market | Balanced cash and earnouts | Focus on stability and retention |

| Declining Performance | Discounted (e.g., 6.0x EBITDA) | Large earnouts (30%+); seller notes | Heavier diligence; more re-trading |

Even strong operating momentum can lose ground if the market or credit backdrop shifts.

Once your performance is clear, market mood starts to matter. A lot.

Buyer count and bid intensity move with sector sentiment. In a hot market, the same business can see a 1.0x to 2.0x swing in EBITDA multiples [5][2]. More buyers usually means more tension in the process. Fewer buyers gives them room to slow things down, dig harder in diligence, and push for better terms as the finish line gets closer.

Public comps matter here too. When those multiples fall, private buyers usually widen the gap between what they could pay and what they're willing to offer. If public company multiples in your sector compress, private buyers often reset risk and trim offers within one to two quarters [7]. Tracking those comps before you launch can save you from walking into the market with the wrong price in mind.

Debt capacity puts a cap on what many buyers can pay.

Most private equity buyers fund 50% to 70% of a purchase price with debt [5]. When interest costs go up, more of the company's cash flow gets pulled into debt service. That leaves less room to support a higher price. For example, if the interest rate on a $5 million acquisition jumps from 6% to 9%, annual debt service rises by about $100,000 [5]. That can pull down valuation and trim the pool of buyers who can still make the deal work [5].

After the Fed's rate cuts in late 2025, credit markets eased heading into 2026. That gave private equity buyers more leverage capacity and more room to stretch on price [2]. Founders who watch credit spreads - the extra yield lenders charge over government debt - can often spot early whether deal terms are likely to lean aggressive or conservative before a buyer ever shows up [7].

Once market conditions look workable, the next step is simpler and harder at the same time: figure out if the business is actually ready.

Before you hire a banker or send out a teaser, take a hard look at the company as it stands today. Use current results across multiple quarters, not one nice-looking period. Buyers want to see consistency over time. If the numbers only shine on their own, the story usually falls apart in diligence. These metrics are the internal side of timing. They show whether you’ll have leverage when a buyer comes to the table.

Buyers care far less about one strong quarter than they do about growth they can believe will keep going. That means they look at year-over-year trends, how spread out revenue is across customers, and how much growth comes from existing accounts expanding over time.

Sell too early, and buyers may treat that momentum like a blip instead of a pattern. Businesses growing EBITDA at 15% or more per year that sold in the first year of that acceleration received median proceeds 38% lower than those that waited 24 months to let the trend prove itself [3]. That’s the tension. Go out too soon, and momentum gets discounted. Wait too long, and a flattening curve can hurt you just as much. If growth has plainly leveled off by the time you launch, buyers will often assume the peak is behind you.

And growth on its own isn’t enough. It has to show up in earnings and in how much visibility you have into what comes next.

Buyers spend a lot of time on normalized EBITDA. They strip out one-time items and owner-specific expenses because they want the earnings base they believe will stick after the deal closes.

A rising EBITDA trend usually points to a business that’s getting better as it scales. A flat or slipping trend can set off alarms, even when revenue is climbing. From a buyer’s point of view, that gap can mean the growth is costing too much or may not last.

Backlog and forecast visibility matter just as much. A contracted backlog, paired with known conversion rates, gives buyers a cleaner view of future cash flow. Without that, they have to price in more uncertainty. In many cases, tighter forecasting can matter more than faster growth because buyers put a premium on certainty [1].

The next test is pretty blunt: can your customer base and your reporting hold up under scrutiny?

Buyer concern tends to climb when one customer makes up more than 15% to 20% of revenue [1]. That kind of concentration can put pressure on valuation because too much of the story depends on one relationship. Every 10-point reduction in a top customer's revenue share can improve multiple support [3].

Retention metrics help fill in the rest of the picture:

When churn is high and concentration is heavy, buyer confidence drops. And when confidence drops, pricing power usually goes with it.

Financial readiness is the part many founders underrate. Businesses with steady monthly close processes and clean EBITDA reconciliations transact at multiples 0.25x higher on average than those with weak reporting [3]. In plain English, buyers pay more when the numbers are easy to trust.

That usually means having a few basics locked down:

Use these metrics to judge whether the sale window is open now, or whether the business needs a bit more time before you go out to market.

When to Sell vs. Wait: Business Exit Timing Decision Matrix

Once you've looked at your internal metrics, the next call is pretty simple on paper: sell now, or spend the next 12 to 36 months building more value first? That call shouldn't come down to instinct. It should come down to where the business stands today and what buyers can underwrite with confidence.

The matrix below helps sort your company into a sell-now or wait bucket.

The best sale windows usually show up when two things happen at the same time: your business is in good shape, and the market is open to deals. Of course, those two things don't always move together.

| Condition | Decision Outcome |

|---|---|

| Strong Internal / Strong External | Premium multiples; favorable terms; strong buyer interest; high negotiating leverage |

| Strong Internal / Weak External | Market-suppressed multiples; selective interest; moderate leverage |

| Weak Internal / Strong External | Discounted multiples; heavy structure; low leverage |

| Weak Internal / Weak External | Lowest valuations; weak interest; little leverage |

Use the matrix to figure out which problem to solve first: internal performance or external market conditions.

A common mistake is waiting for a "perfect" moment that only becomes clear in hindsight. That kind of delay can bring limited upside and serious downside [6]. For example, delaying a sale by one year to chase 20% growth can lift the fourth-year earnout target by 107% [6]. After close, that target can be much harder to hit. So the longer you wait, the more likely it is that the price target moves up while your leverage moves down.

Selling under pressure can be just as damaging. If burnout or cash strain forces the process, most negotiating leverage is gone before talks even begin. And going to market before the financials are clean creates retrade risk. If buyers find reporting gaps during diligence, they'll lower the offer.

If the matrix says wait, use that 12- to 36-month window to remove buyer risk, not just add revenue. That's the part many founders miss.

Use earnings quality, transferability, and growth visibility as the go/no-go test.

Exit timing is a data call. It comes down to one thing: do your internal and external signals line up right now?

The best sale windows come from alignment, not perfection. When business health, market conditions, and owner readiness line up, you can negotiate from a position of strength. When they don’t, you’re on weaker ground no matter how solid the company feels from the inside.

The core metrics are pretty simple. Focus on the same signals buyers will underwrite, not a long list that pulls attention away from the sale decision. Growth rate, EBITDA trend, backlog and revenue visibility, churn, market multiples, and debt market conditions each tell one part of the story. Track them every month, not just when you’re thinking about a sale. That habit is often the difference between founders who walk into a process with leverage and those who end up scrambling to explain gaps during diligence.

Phoenix Strategy Group helps growth-stage companies put the right reporting, FP&A, and M&A readiness in place for a credible exit. Readiness matters just as much as timing. Track the signals now, before leverage shifts.

Your sell window opens when three things line up: business readiness, market conditions, and your personal goals.

That usually means the business is performing well, your records are ready for diligence, and you have enough runway to run a sale process without being pushed into a corner.

It also helps to look outside the company. Check buyer demand, financing availability, and valuation multiples in your sector. The best time to sell is when those factors make a deal more attractive than continuing to operate as a private company.

Business readiness matters most. Market timing can add to the price, but it’s hard to predict and outside your control.

When conditions line up - like lower interest rates and strong buyer competition - valuations can climb. That said, you can’t build your whole plan around the market behaving the way you want.

What you can control is the business itself. A prepared company with clean financials, stable EBITDA, less founder dependency, and operations that can scale tends to do better in a sale process.

The strongest outcome usually comes when that internal readiness meets a good market window.

Wait only when the likely upside is bigger than the risk.

You’ll usually get the best price when earnings quality is strong, growth is easier to see, and the business can transfer cleanly to a new owner. That mix tends to pull in more buyers, and more buyers often means better offers.

If you’re about 18 to 36 months away from a major EBITDA threshold, waiting may make sense when the risk-adjusted outcome could add at least 30% to your proceeds. If the expected gain is below 20%, let your personal goals guide the call. Start formal exit prep 18 to 24 months before closing.