Published on

July 12, 2026

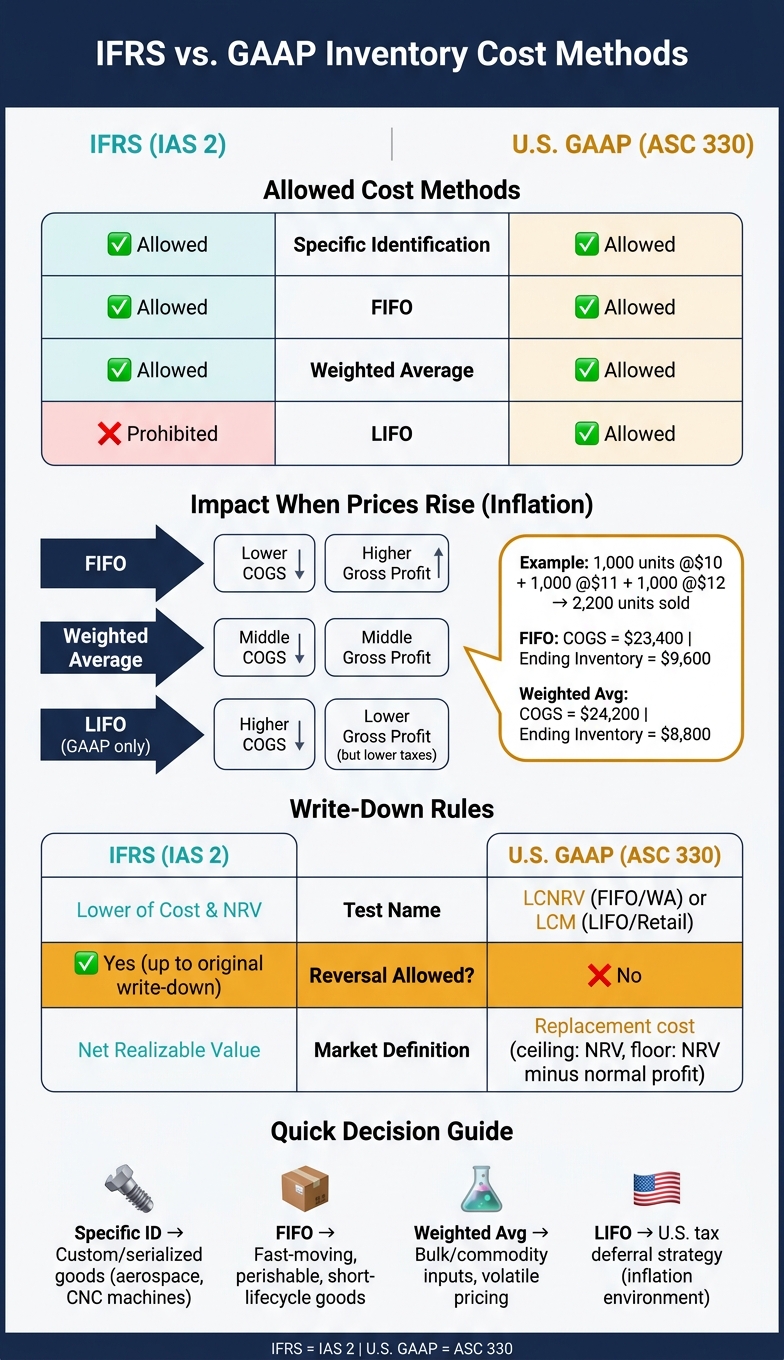

Your inventory method changes COGS, gross margin, taxes, and write-downs. If costs are rising, FIFO usually shows lower COGS and higher profit, LIFO usually shows higher COGS and lower profit, and weighted average sits in between.

Here’s the short version:

A fast example shows why this matters. If a company buys 1,000 units at $10, 1,000 at $11, and 1,000 at $12, then sells 2,200 units, FIFO COGS is $23,400 and ending inventory is $9,600. In that same setup, weighted average gives $24,200 of COGS and $8,800 of ending inventory.

IFRS vs. GAAP Inventory Cost Methods: Side-by-Side Comparison

| Method | IFRS | U.S. GAAP | Best fit | When prices rise | Write-down rule |

|---|---|---|---|---|---|

| Specific identification | Allowed | Allowed | Serialized or job-specific items | Uses actual unit cost | IFRS: lower of cost and NRV; GAAP: lower-of-cost rule depends on framework use |

| FIFO | Allowed | Allowed | Fast-moving, interchangeable items | Lower COGS, higher ending inventory | IFRS: lower of cost and NRV; GAAP: LCNRV |

| Weighted average | Allowed | Allowed | Bulk or commodity-like items | Middle ground | IFRS: lower of cost and NRV; GAAP: LCNRV |

| LIFO | Not allowed | Allowed | Some U.S. companies seeking tax deferral | Higher COGS, lower ending inventory | GAAP: LCM |

| Lower-of-cost test | Required | Required | All inventory at period-end | Can cut profit if inventory value drops | IFRS: NRV-based; GAAP: LCNRV or LCM |

If I had to boil the article down to one point, it’s this: pick the method that matches your inventory type, your system, and your reporting rules—or consult fractional CFO services for expert guidance - then apply the write-down test the right way.

Before a finance team picks an inventory costing method, it needs to get three things straight: whether items are interchangeable, how the inventory system records movements, and how much input costs swing over time. Those trade-offs shape which method makes sense for the inventory base.

The first cut is simple: are the inventory items interchangeable or not?

Interchangeable items are functionally identical and usually aren’t tracked as one-by-one units. Think standard steel coils, bulk chemicals, or standardized components. When items fall into this group, FIFO, weighted average, and, under U.S. GAAP, LIFO can all be used because the units are treated as equivalent for costing.

Non-interchangeable items work differently. These are unique, high-value, or project-specific units with their own identifiers, such as serial numbers, lot numbers, or job numbers. Good examples include custom machinery, aerospace components, or one-off engineered systems. Under both IFRS and U.S. GAAP, these items generally require specific identification, which means actual costs are traced directly into COGS when the item is sold.[6][1][14]

That’s the first big dividing line between specific identification and pooled-cost methods. If a company misclassifies serialized items, COGS can get distorted and audit risk goes up. So this call has to be right from the start. It’s the line between specific identification and methods like FIFO and weighted average.

The way the system records inventory movement matters too.

In a periodic system, inventory costs are not updated all the way through the period. Instead, the company counts inventory at period-end and calculates COGS as beginning inventory + purchases − ending inventory. The cost flow method is then applied at the end of the period.[10]

A perpetual system does the job in real time. Each receipt, production posting, and shipment updates inventory and COGS as it happens. Under FIFO, every outbound transaction pulls from the oldest cost layers first. Under moving weighted average, the unit cost is recalculated with each new purchase receipt. Most modern ERP systems use perpetual tracking, which gives finance teams more timely COGS data.[7][13]

This difference matters because periodic and perpetual tracking can change how cost layers are consumed. Under U.S. GAAP, the two systems can produce different COGS and ending inventory figures, since purchase timing affects which layers are used up. Finance teams should be clear on which system they run and apply the method the same way every time. The system shapes how costs move into COGS.

When input costs are rising, the gap between FIFO, weighted average, and LIFO becomes much easier to see.

Under FIFO, older and lower-cost layers flow into COGS first. That usually leads to lower COGS and higher reported margins. Under LIFO, which is allowed only under U.S. GAAP, the newest and highest-cost layers are expensed first. That pushes COGS up and reported income down, but it can also lower taxable income. Weighted average blends available costs together and usually lands somewhere in the middle.[8][4]

Obsolescence is a different problem. Slow-moving SKUs may need a write-down even if their historical cost still looks fine. Weighted average can make this harder to spot because problem items may get buried inside a pooled cost rate, which can delay loss recognition.[9][12]

Those effects stand out more clearly in the method-by-method comparison that follows. These trade-offs drive which method fits the inventory base.

For non-interchangeable inventory, specific identification is the cleanest method. It tracks the actual cost of each individual unit. When that unit is sold, its recorded cost moves into COGS. There’s no averaging here - each unit keeps its own actual cost.

IFRS requires specific identification for non-interchangeable or project-specific inventory. U.S. GAAP also allows it, especially for serialized or custom-built goods like specialized CNC machines, medical devices, or aerospace components.[5][16][18]

That level of precision changes both COGS and ending inventory. Since actual unit costs move straight into COGS, this method can lead to higher COGS and lower ending inventory than FIFO or weighted average. It also gives you a clearer view of project margins, though it can make earnings swing more from period to period.[15][19][20]

Specific identification still follows lower-of-cost rules. Under IFRS, companies write inventory down to NRV and reverse the write-down if the value recovers. Under U.S. GAAP, companies write inventory down under LCM and, in most cases, do not reverse the loss.[16][17][21]

First-in, first-out (FIFO) assumes the oldest units in inventory are sold first, so the newest units stay in ending inventory. In manufacturing, that often lines up with how goods move in the plant or warehouse. For finance teams, the big issue is simple: FIFO can shift margin, inventory value, and write-down risk all at once.

IFRS and U.S. GAAP both allow FIFO for interchangeable inventory, while IFRS does not allow LIFO.[22][25][27][29] So FIFO is easy to use from a rules standpoint. But when input costs move, its effect on margin can change fast.

For manufacturers, FIFO changes reported margin and ending inventory at the same time. When prices go up, FIFO pushes older, lower costs into COGS first.[23][24][4] That lowers COGS and leaves newer, higher-cost units in ending inventory. The result is higher gross profit and higher ending inventory.

Example: 1,000 units at $10, 1,000 at $11, and 1,000 at $12, with 2,200 units sold, gives FIFO COGS of $23,400 and ending inventory of $9,600. Weighted average would give $24,200 and $8,800.[28][4]

That gap matters. FIFO can make margins look stronger during inflation, but it also leaves more value sitting on the balance sheet.

FIFO does not change the lower-of-cost test for ending inventory. Under IFRS, inventory is measured at the lower of FIFO cost and net realizable value (LCNRV). If NRV falls below cost, the manufacturer writes inventory down and records the loss. IFRS also allows that write-down to be reversed in a later period if NRV recovers, up to the original cost.[9][26][27]

Under U.S. GAAP, FIFO inventory uses LCM, and reversals are not allowed. Once inventory is written down, that lower carrying value becomes the new cost basis.[9][27]

This is where FIFO can sting a bit. In inflationary periods, FIFO often leaves a higher ending inventory balance on the books. If selling prices later fall or demand weakens, that higher balance can mean a larger write-down. Weighted average smooths those costs instead of keeping distinct cost layers.

Unlike FIFO, weighted average cost rolls all purchase prices into one per-unit cost. The result is smoother COGS and ending inventory across all units on hand.

That’s why many manufacturers use it when input costs swing up and down. Instead of leaving those changes in separate cost layers, the method spreads them into one blended rate.

Both IFRS and U.S. GAAP allow this method. Inventory still has to pass the lower-of-cost test: LCNRV under IFRS and LCM under U.S. GAAP.

Next up is LIFO, which is allowed under U.S. GAAP only.

LIFO is a U.S. GAAP-only method that sends the newest costs into COGS first.

Put simply, LIFO assumes the most recent inventory costs move to COGS before older costs do. U.S. GAAP allows LIFO, while IFRS does not. For manufacturers dealing with rising input costs, that can change reported margin and taxable income in a big way.

When prices are rising, LIFO increases COGS and lowers ending inventory. It changes the cost flow assumption, but the inventory still needs its own lower-of-cost test.

Under U.S. GAAP, LIFO inventory is tested under LCM.

Before inventory goes on the balance sheet, it also has to pass a lower-of-cost test. The exact rule depends on the reporting framework and, under U.S. GAAP, the cost method being used.

Under IFRS (IAS 2), inventory is reported at the lower of cost and net realizable value (NRV). NRV is the estimated selling price in the ordinary course of business, minus estimated costs of completion and the costs needed to make the sale.[22][16]

If NRV drops below cost because inventory is obsolete, damaged, slow-moving, or hit by falling prices, the company writes inventory down and records the loss in earnings.[31][32][33][2][37]

IFRS does allow reversals.[5][16][36] So if NRV later goes back up, the earlier write-down can be reversed in part or in full. But there's a limit: the reversal can't exceed the original write-down amount. That reversal lowers current-period COGS or may be presented as other income, which can make earnings swing from period to period.[5][36]

U.S. GAAP uses different tests depending on the cost method.[2][30]

| Cost Method | Test Applied | Reversal Allowed? |

|---|---|---|

| FIFO or weighted average | LCNRV (lower of cost and net realizable value) | No |

| LIFO and the retail inventory method | LCM (lower of cost or market) | No |

Under LCM, market means replacement cost, with a ceiling of NRV and a floor of NRV less normal profit.[30][26] Under LCNRV, cost is compared directly with NRV, much like IFRS.[2] The big difference is what happens later: U.S. GAAP does not allow reversals, so the written-down amount becomes the new cost basis.[2][36]

That gap is the main point in the IFRS vs. GAAP comparison that follows.

When cost is higher than the required floor, the entry hits both inventory and margin. Here's why: COGS = Beginning Inventory + Purchases − Ending Inventory. So a write-down lowers ending inventory on the balance sheet and increases COGS by the same amount, which squeezes gross margin in the period the loss is recorded.[31][34] Under U.S. GAAP, that effect stays in place. Under IFRS, it may be reversed if NRV recovers, up to the original write-down amount.[2][5][16][36]

A write-down is not the same as a write-off. A write-down reduces the carrying amount of inventory that still has some recoverable value. A write-off removes inventory that has no recoverable value at all, such as destroyed or expired goods.[32][35][37]

The next section shows how IFRS and U.S. GAAP diverge in practice.

Use this comparison to spot the differences that matter in U.S. manufacturing. The big one is LIFO: U.S. GAAP allows it, but IFRS does not.[1][3][39] IFRS uses lower of cost and NRV. U.S. GAAP splits the rule: LCNRV for FIFO and weighted average, and LCM for LIFO and the retail inventory method. That gap hits hardest when a manufacturer reports under both systems or handles inventory across borders.

| Method or Rule | IFRS Status | GAAP Status | Typical Use Case | Inflation Impact on Earnings | Write-Down Rule |

|---|---|---|---|---|---|

| Specific identification | Allowed under IAS 2 | Allowed under ASC 330 | Custom machinery, aerospace components, made-to-order goods | Tracks actual item flow and minimizes distortion | Lower of cost and NRV under both frameworks |

| FIFO | Allowed | Allowed | Perishables, chemicals, and fast-moving consumer goods | Usually higher earnings and higher ending inventory in inflationary periods | Lower of cost and NRV under both frameworks |

| Weighted average cost | Allowed | Allowed | Bulk materials, liquids, and commodity-like inputs | Usually a moderate effect; smooths inflation impacts | Lower of cost and NRV under both frameworks |

| LIFO | Prohibited | Allowed | Some U.S. manufacturers seeking tax benefits in inflationary environments | Usually lower earnings and lower ending inventory in inflationary periods | Lower of cost or market (LCM) under GAAP |

| Lower-of-cost test (overlay) | Required | Required | Obsolete, damaged, or slow-moving inventory at period-end | Reduces earnings when a write-down is recorded | IFRS: lower of cost and NRV; GAAP: lower of cost and NRV for FIFO/weighted average, lower of cost or market (LCM) for LIFO and the retail inventory method |

For U.S. manufacturers, the issue isn't just the rule itself. It's the extra reporting work that comes with it. If your company uses LIFO for its U.S. books, you'll need a separate conversion layer or a parallel inventory process to produce IFRS-compliant financials.[27][40]

That reconciliation can change earnings and covenant metrics like EBITDA, current ratio, and inventory turnover. In plain terms, this isn't only an accounting policy call. It can shape your inventory method, reporting controls, and tax posture.

Once you’ve compared the rules, the next step is picking the method that matches your inventory, your systems, and your reporting needs. There’s no one-size-fits-all answer here. The best place to start is with your product mix, then work outward to daily operations and outside reporting demands.

Your inventory type should shape the first decision:

A lot of manufacturers don’t stick to just one approach across everything. It’s common to use specific identification for custom, high-value jobs, while using weighted average or FIFO for bulk commodity inputs that feed into those same jobs.

And if your product mix doesn’t make the answer obvious, your ERP system often will.

Pick the method your ERP can handle without manual patches or spreadsheet-heavy workarounds. Before you lock anything in, make sure the system can run the method in a controlled, audit-ready way.

LIFO is usually the hardest to manage from a systems angle. It means keeping cost layers by pool, dealing with liquidations, and supporting GAAP disclosures.[41][11][44] If your ERP can’t maintain LIFO layers cleanly, don’t use LIFO. It’s that simple. When the system can’t support the method well, the day-to-day risk and audit exposure usually beat any tax upside on paper.

Once system support checks out, the last screen is outside reporting.

LIFO can reduce taxable income during inflation, but it also makes comparison harder and adds friction to cross-border reporting.[22][38][43][45]

Lenders and investors often lean toward FIFO or weighted average because those methods are easier to compare across reporting bases. In some cases, loan agreements even require covenant calculations on a non-LIFO basis so the numbers are normalized. If your company may pursue a foreign listing, overseas growth, or a cross-border deal, starting with FIFO or weighted average can save a lot of cost and hassle later.

Use the matrix below to narrow the options fast.

| Decision Factor | Lean Toward Specific ID | Lean Toward FIFO | Lean Toward Weighted Average | Consider LIFO |

|---|---|---|---|---|

| Product type | Custom, serialized | Short-life-cycle | Commodity, bulk | Inflation-exposed, high-volume |

| ERP support | Lot/serial tracking | Layer tracking | Automated average costing | Complex layer and pool management |

| Tax priority | Low relevance | Higher taxes in inflation | Higher taxes in inflation | Tax deferral in inflation |

| IFRS compatibility | Compatible | Compatible | Compatible | Not compatible |

| Lender/investor preference | High transparency | Balance sheet recency | Stable margins | Requires reconciliation |

After you pick a cost method, the biggest trouble usually comes from how that method is used day to day. Most inventory valuation mistakes trace back to three problems: inconsistent policy, old cost data, and write-down rules applied the wrong way.

Don’t use different costing methods for similar items across locations or product lines unless you have a documented rule for it. If lot tracking is weak too, things can go sideways fast.

When transaction records are incomplete - missing receipts, late postings, or adjustments no one documented - cycle count variances get much harder to explain. And once that happens, write-down decisions start to rest on guesswork instead of facts.

A few basic controls help a lot:

The next problem is valuation discipline. Standard costs need to be reviewed on a fixed schedule. If that review slips, your inventory values can drift away from what the items actually cost.

It also helps to tie cost updates to engineering change control. That way, when a bill of materials changes, re-costing happens automatically instead of getting missed in the shuffle.

For slow-moving stock, flag SKUs with 180–360 days of inactivity for an obsolescence review. That gives the team a clear signal to check whether carrying values still make sense.

This is one of the most common compliance errors: mixing terms from different reporting frameworks. Don’t do that across entities.

Under U.S. GAAP, inventory is generally measured using LCNRV for FIFO and weighted average. LCM applies only to LIFO and the retail inventory method. Under IFRS, the rule is NRV, and reversals are allowed.

Under IAS 2, a write-down can be reversed up to the original write-down amount if the reasons for it no longer exist, but the carrying value can never exceed original cost.[46] Under U.S. GAAP, reversals are not permitted.[47]

The fix is pretty simple: publish separate policy memos for each reporting framework and train each entity on the framework it uses.

These rules shape how inventory flows through COGS, the balance sheet, and write-down testing. And that has a direct effect on gross margin, taxes, and covenant compliance. Put simply: the costing method and the testing rules work together to set COGS, inventory value, and reported earnings.

The best choice is the one that fits how inventory actually moves, follows the reporting rules, and gives management numbers they can use. A commodity processor doesn’t operate like a serial-tracked job shop, so they shouldn’t default to the same method.

After you line up the method with inventory flow, the next step is practical: can your reporting base handle it without a mess? For U.S. manufacturers, LIFO can help during inflation, but it also creates cross-border issues and may call for reserve adjustments under IFRS reporting.

It also helps to stay disciplined here:

For growth-stage manufacturers getting ready to scale, finance a raise, or prepare for exit, method choice turns into a business issue, not just an accounting one. Phoenix Strategy Group can model method effects, quantify tax impact, and support inventory policies that hold up under investor and lender review.

The best inventory method comes down to how your business runs and what your reporting needs look like.

FIFO is often a good fit for consumer goods brands in food, beverage, and personal care. Why? It lines up with how stock usually moves in those categories, and it’s accepted under both GAAP and IFRS.

If keeping track of individual cost layers gets messy across a large number of SKUs, weighted average cost can be a practical, compliant choice.

LIFO, on the other hand, is usually limited to U.S.-only businesses because IFRS does not allow it.

FIFO and weighted average can change reported gross margin and profit.

When costs are going up, FIFO usually leads to lower COGS and higher profit because it assumes the oldest inventory gets sold first. That means the items flowing into cost of goods sold often come from earlier, lower-cost purchases.

Weighted average works differently. It uses the average cost of all units available for sale, which smooths out price swings. As a result, profit under weighted average is often less volatile than under FIFO.

You need to write inventory down when it becomes obsolete, damaged, unsellable, or when its market value drops below its recorded cost. This keeps ending inventory from being overstated and stops profit figures from getting warped.

Under U.S. GAAP, inventory is measured at the lower of cost or net realizable value. Regular cycle counts and physical audits help spot these problems early and cut the risk of financial misstatements.