Published on

January 12, 2026

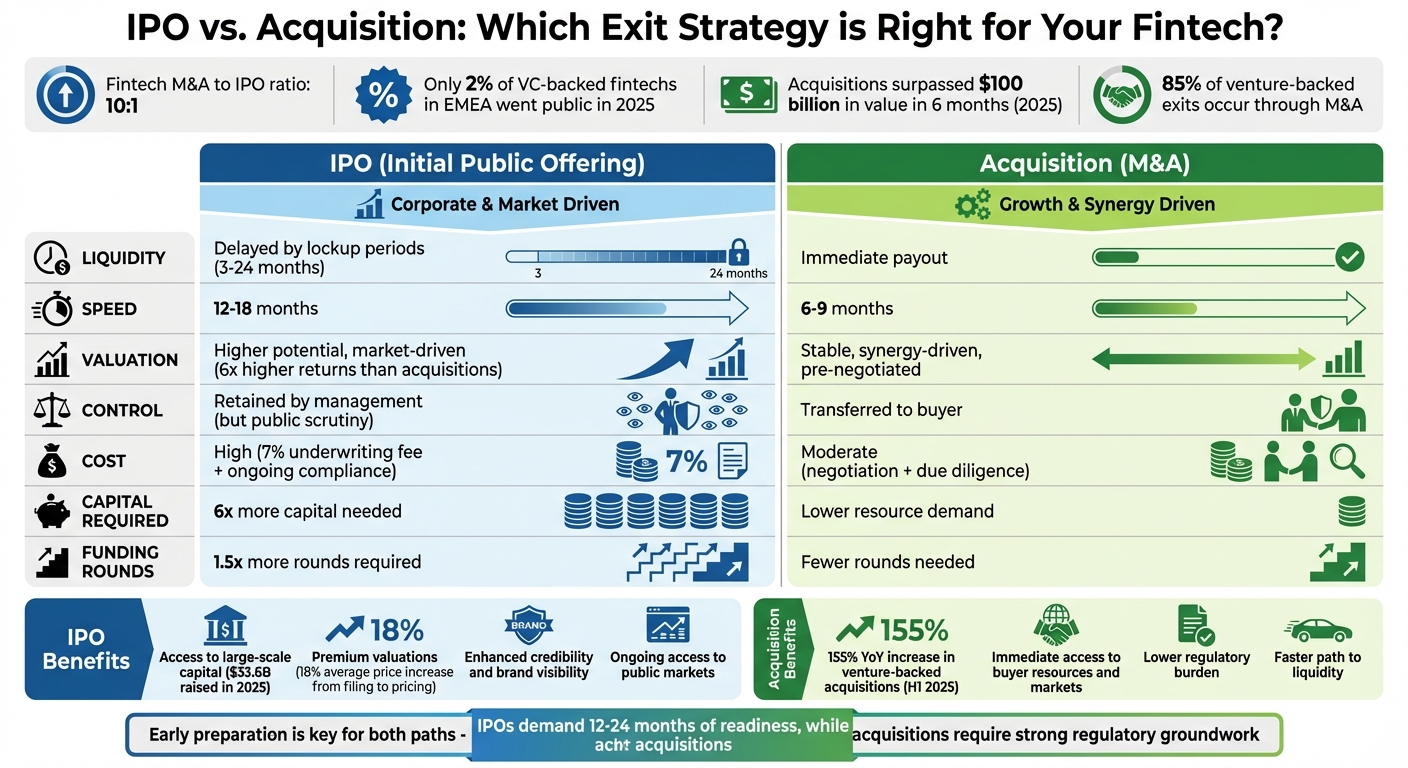

What’s the best way for a fintech to exit - IPO or acquisition? It depends on your goals. IPOs can deliver higher returns but take more time, money, and effort. Acquisitions are faster, more predictable, and dominate the fintech space with a 10:1 ratio compared to IPOs. In 2025, only 2% of VC-backed fintechs in EMEA went public, while acquisitions surpassed $100 billion in value in just six months.

Here’s a quick breakdown:

Quick Comparison:

Feature

IPO

Acquisition

Delayed by lockup periods

Immediate

12–18 months

6–9 months

Higher potential

Stable, synergy-driven

Retained but public scrutiny

Transferred to buyer

High

Moderate

Whether you prioritize long-term independence or fast liquidity, early preparation is key. IPOs demand financial readiness and scalability, while acquisitions require strong regulatory and operational groundwork. Both paths can lead to success - choose what aligns with your fintech’s stage and goals.

An Initial Public Offering (IPO) marks the moment when a private fintech company steps into the public arena, offering shares to the general public for the first time on a stock exchange. This move provides founders and early investors with a partial exit while still holding onto a substantial share of ownership. At the same time, it opens the door to public capital markets [4]. By going public, a fintech transforms into a publicly traded entity, typically listed on major exchanges like NASDAQ or NYSE. This shift not only establishes liquidity but also assigns a public valuation to the company.

For fintech firms, an IPO is more than just a fundraising event. It’s a milestone that boosts brand credibility and creates a new form of "currency" - publicly traded stock - that can be leveraged for future acquisitions [4][10]. The process, however, is no quick sprint. It usually spans one to two years, involving key steps like selecting an investment bank, filing registration documents with the SEC, conducting investor roadshows lasting several weeks, and finally, pricing and listing [9][10]. While demanding, this transition can lead to both financial and operational benefits.

The most obvious perk of an IPO? Access to large-scale capital without giving up control. Public investors, especially in strong markets, often pay premium valuations for companies with high growth potential. By contrast, acquirers tend to discount financial projections during due diligence [4]. For perspective, 13 IPOs in September 2025 alone raised over $8 billion, making it the busiest month for new listings since late 2021. In total, traditional IPOs brought in $33.6 billion in 2025, marking the strongest year since 2021 [14].

But the advantages don’t stop at raising funds. The IPO process itself pushes companies to improve their operations. It demands better data systems, integrated technology, and tighter internal controls, which help eliminate reliance on manual, error-prone processes [13]. The market rewards such preparation: enterprise tech IPOs since 2019 have seen their prices climb an average of 18% from initial estimates to final pricing, reflecting investor enthusiasm for well-prepared businesses [4]. Additionally, once public, companies gain ongoing access to capital markets for future funding rounds without sacrificing control, making acquisitions easier to finance.

"2026's IPO window is open - but selective. A shutdown-driven backlog and easing rates are bringing supply, yet investors are paying a premium for scaled, cash-generative stories with clear profitability paths - especially in AI infrastructure, software, and specialty risk." - Mike Bellin, IPO Services Leader, PwC US

While the benefits are clear, the IPO journey also comes with its fair share of hurdles.

Going public isn’t cheap - or easy. One of the biggest challenges is assembling a team of experienced public market professionals. Fintech companies need to hire a CFO with SEC expertise, along with controllers and internal audit teams. Finding talent with both fintech and public market knowledge can be tough [13]. On top of that, the underwriting fee alone typically takes 7% of the proceeds, and companies must budget for ongoing legal, accounting, and marketing expenses that don’t directly contribute to their core business [9][11].

Then there’s the heavy regulatory burden. Companies must file a Form S-1 registration statement with the SEC, which usually provides initial feedback within 27 calendar days. Financial statements can also become "stale" if they’re more than 134 days old, potentially delaying the process [12]. Post-IPO, compliance doesn’t get any easier. Newly public companies must adhere to Sarbanes-Oxley Section 404 certification requirements by their second annual report, though investors often expect these controls to be in place even before listing [13].

The market environment in 2026 adds another layer of complexity. With a backlog of over 800 unicorns entering the year, investors are increasingly selective. They’re favoring companies with proven, cash-generative models over those focused solely on rapid growth [14]. The median time to IPO for companies valued at $500 million or more reached over 11 years in 2025, underlining how long it can take for fintechs to achieve the maturity needed for a successful public debut [14]. Adding to the challenge, lock-up agreements typically restrict insiders from selling shares for 3 to 24 months after the IPO, delaying full liquidity [11].

While IPOs can open doors to substantial capital, acquisitions offer a quicker and more predictable way for fintech companies to transition. An acquisition happens when a larger company - often a bank, financial institution, or tech giant - buys out a fintech, either entirely or by purchasing a controlling stake. Unlike IPOs, which involve selling shares to the public, acquisitions are private deals negotiated directly between the buyer and the fintech. These transactions typically include steps like screening, valuation, due diligence, deal structuring, and post-merger integration.

Acquisitions usually wrap up within nine months [3]. However, they come with their own set of challenges, particularly regulatory ones. Buyers must navigate federal and state licensing requirements, handle change-of-control filings, and engage with regulators early to streamline approval processes.

The deal terms often include mechanisms like earnouts, escrows, and indemnities to address valuation differences. Banks tend to focus on a fintech's profitability and immediate financial impact, while founders often emphasize long-term growth and revenue potential [15].

Why do so many fintech companies choose acquisition as their exit strategy? One of the main reasons is speed and predictability. Acquisitions offer immediate liquidity for shareholders through direct purchase agreements, bypassing the market fluctuations and investor sentiment risks that can derail IPOs [3]. In the first half of 2025, acquisitions of venture-backed companies surged past $100 billion, marking a 155% year-over-year increase [6].

Another advantage is the lower resource demand. IPOs require nearly six times more capital and about 1.5 times as many funding rounds compared to acquisitions [1]. Acquisitions also spare founders the intense public reporting and regulatory scrutiny that come with going public. With over 85% of venture-backed exits occurring through mergers and acquisitions (M&A) [3], this route is the dominant choice for many fintechs.

Beyond the financial benefits, acquisitions can accelerate growth and scale. Joining forces with a larger entity often means immediate access to new markets, established customer bases, and advanced technology. For instance, in 2021, Fifth Third Bank acquired Provide, a fintech focused on healthcare professionals like dentists and veterinarians, to expand its lending and card services [15]. Similarly, in 2016, Capital One acquired Paribus, integrating its price-tracking technology to introduce a "Price Protection" feature on its credit cards, boosting customer retention and attracting retail partners [15].

"Strategic M&A will likely be the main exit route for European startups, followed by sponsor-led M&A."

For fintechs struggling with cash flow or facing stagnant growth in tough funding climates, an acquisition can provide a much-needed lifeline [3].

Despite its perks, going through an acquisition isn’t without its hurdles. One of the biggest downsides is the loss of control. Founders often relinquish decision-making power and may find it challenging to adapt to the acquirer's corporate environment. These cultural mismatches are a common reason why integrations fail.

Valuation is another sticking point. Buyers tend to discount future projections, often leading to lower offers [1]. For example, banks - despite their size - accounted for less than 1% of all fintech acquisitions between 2013 and 2023. Even among those deals, only 13% of bank-fintech acquisitions in the last decade exceeded $300 million in announced deal sizes [15].

Talent retention is another critical issue. Deals can lose value if key employees or founders leave after hitting earnout milestones, typically around the two-year mark [15]. In fact, roughly 90% of M&A transactions fail in the long run due to poor execution and post-deal strategy issues [15]. Common integration challenges include merging incompatible tech systems, ensuring compliance with data residency laws, managing third-party vendor dependencies, and addressing cybersecurity and privacy concerns (e.g., CCPA, GDPR). Intellectual property disputes and AI governance issues can also derail deals.

To avoid such pitfalls, fintechs should start early on regulatory, privacy, and cybersecurity preparations. Strengthening the leadership team with experienced CFOs or legal advisors and securing clear intellectual property rights can also help prevent delays and complications during the acquisition process.

When it comes to fintech exit strategies, IPOs and acquisitions differ significantly in terms of timing, control, and risk. IPOs tend to generate returns nearly six times higher than acquisitions but require much greater capital - six times more, to be exact - and involve 1.5 times more financing rounds. Meanwhile, over 85% of venture-backed exits happen through mergers and acquisitions (M&A). In fintech, the numbers lean even more heavily toward M&A, with a striking 10-to-1 ratio of acquisitions to IPOs. For context, only 2% of EMEA fintech firms exit via IPOs [1][3][7].

"Fintech is defined by a disproportionate number of large M&A transactions compared to IPOs (on the order of 10-1)."

Timing is another major factor. IPOs generally take 12 to 18 months to complete [1], while acquisitions wrap up much faster, typically within 6 to 9 months [1][5]. Liquidity is also a key point of contrast: acquisitions provide immediate payouts at the time of closing, while IPOs come with lockup periods ranging from 3 to 24 months, delaying when insiders can sell their shares [1][17].

Here’s a quick breakdown of the key differences:

Feature

IPO

Acquisition

Delayed by lockup periods

Immediate (cash, stock, or combination)

Longer (12–18 months)

Faster (6–9 months)

Higher potential; influenced by public market demand

Synergetic; pre-negotiated and stable

Retained by management but subject to public scrutiny

Transferred to acquirer

Market volatility, regulatory hurdles (e.g., SOX), high disclosure costs

Integration issues, potential cultural clashes, risk of undervaluation

High (underwriting, legal, ongoing compliance)

Moderate (negotiation, due diligence, legal)

Valuations for IPOs and acquisitions are shaped by different forces. IPO valuations are driven by public market sentiment, with innovative fintech companies often commanding premium pricing. For example, in strong market conditions, IPO prices can climb an average of 18% from the initial filing range to the final pricing [4]. On the other hand, acquisition valuations are rooted in strategic synergies and direct negotiations. To put this into perspective, since 2018, the average acquisition price for large fintech M&A transactions (over $50 million) has been about $403 million [7]. Meanwhile, large publicly listed fintech firms boast an average market cap of $5.1 billion - or $2.5 billion when excluding outliers like Coinbase and Nubank [7].

Getting your fintech ready for an IPO or acquisition requires more than just good timing - it demands financial and operational readiness. To maximize your exit's value, focus on three core areas: People, Processes, and Systems [18]. This means having experienced leadership, standardized KPIs, efficient financial close processes, and scalable ERP platforms. Here's a telling stat: 78% of public companies had a seasoned CFO in place for at least a year before their IPO, and 83% had implemented ERP systems like NetSuite, Oracle, or SAP at least 12 months prior to filing [18].

When it comes to impressing investors, speed matters. Companies aiming for an IPO often close their books in under 10 days, compared to the industry average of 15 days [18]. A faster close cycle signals operational efficiency, which investors love. But it’s not just about speed - you’ll also need audited financial statements, clear EBITDA adjustments, revenue trend analyses, and well-organized tax documents to sail through due diligence [6].

However, challenges abound. Nearly half of CFOs (48%) report difficulties with data integration, and over a third (34%) struggle with audit preparation [6]. Addressing these issues early is critical.

Internal controls are another area that requires attention long before the IPO process begins. Companies should aim to formalize SOX compliance and internal controls at least 1 to 2 years before filing. This helps avoid the embarrassment of disclosing material weaknesses - something 65% of companies still face at IPO time, often due to gaps in financial reporting or outdated technology [18]. For acquisitions, the diligence process kicks off even earlier. Start tackling regulatory, privacy, and cybersecurity concerns at the NDA stage to avoid deal-breaking surprises later [8].

Operational scalability is equally important. Investors want to see that your business can grow without costs spiraling out of control. Standardizing procedures, automating finance functions, and tracking key metrics like Annual Recurring Revenue (ARR) and Remaining Performance Obligations (RPO) are essential [18]. If your fintech relies on AI or algorithmic models, you’ll also need to document model governance to meet compliance requirements like fair lending and anti-discrimination standards [8]. These steps not only prepare your company for an exit but also lay the groundwork for successful strategic partnerships.

Once your internal systems are in top shape, bringing in expert advisors can take your exit strategy to the next level.

"Sell-side readiness can be time-consuming and complex, and working with a deal advisory team can help you effectively manage the sale process and navigate the numerous M&A considerations that always arise."

Advisory support can streamline even the most complex preparations. For example, Phoenix Strategy Group specializes in helping growth-stage fintechs gear up for exits. They offer services like cash flow forecasting, KPI development, revenue engine analysis, and unit economics evaluation - all of which are crucial for exit readiness. With venture-backed acquisitions rising 155% year-over-year in early 2025 [6], having the right financial infrastructure and advisory support can make the difference between achieving a premium valuation or leaving money on the table.

Advisors also help with practical, hands-on steps. These include conducting mock audit committee meetings, running investor calls, and preparing earnings releases for at least two quarters before filing [18]. They’re instrumental in transaction tax structuring, valuation projections, and organizing your data room for a smooth due diligence process [6]. As your accounting team grows - often exceeding 10 members for IPO-ready startups [18] - advisory partners ensure you’re building the right capabilities at the right time.

Deciding between an IPO and an acquisition often hinges on your company's growth stage, liquidity requirements, and the broader market environment. For an IPO, you'll need consistent revenue patterns and reliable earnings forecasts [2]. If your fintech isn't quite there yet, pursuing an acquisition may be the more practical route.

Control is another major factor. IPOs generally allow your management team to maintain control over strategic decisions, while acquisitions usually come with a shift in control [1].

Market conditions in 2026 are showing signs of improvement but remain selective. In 2024, 225 U.S. companies went public - a 46% jump from the previous year [2]. However, investors are prioritizing companies that are "scaled and cash-generative" with clear paths to profitability, rather than those still burning through cash [14]. On the other hand, acquisitions are thriving. Venture-backed M&A deals surpassed $100 billion in the first half of 2025, marking a 155% year-over-year increase [6]. With over $2.5 trillion in global "dry powder" available for acquisitions [5], M&A continues to dominate, accounting for more than 85% of venture-backed exits [3].

"2026's IPO window is open - but selective. A shutdown-driven backlog and easing rates are bringing supply, yet investors are paying a premium for scaled, cash-generative stories with clear profitability paths."

These dynamics highlight the importance of aligning your exit strategy with both your fintech's internal readiness and the external market landscape.

The ideal exit strategy depends on your fintech's stage of development and the prevailing market conditions. If you're aiming for long-term independence, enhanced global visibility, and the ability to leverage public shares for future acquisitions, an IPO could be your best option [1]. However, if immediate liquidity, access to a larger company's resources, or strategic synergies are more pressing, an acquisition might be the better choice [3].

Preparation is key. Start operating as if you're a public company at least 12 to 24 months before a planned IPO [10]. A dual-track approach - preparing for both an IPO and a potential acquisition - can keep your options open as market conditions shift [14]. Partnering with expert advisors, like Phoenix Strategy Group, can also make a significant difference. Their services, including cash flow forecasting, KPI development, and M&A support, help position your fintech for maximum returns in any exit scenario.

When fintech companies face the decision between pursuing an IPO or opting for an acquisition, they need to carefully consider various factors like financial objectives, regulatory obligations, and their long-term vision. An IPO can unlock access to public capital, often leading to higher valuations and providing resources for future expansion. However, going public isn’t cheap - it demands significant upfront investment, multiple funding rounds, and strict adherence to regulations such as Sarbanes-Oxley. Timing is also crucial; strong equity markets can enhance IPO outcomes, while weaker markets might lead to reduced valuations.

In contrast, acquisitions typically offer a quicker and more predictable payout with fewer regulatory complexities. That said, acquisitions might not command the same valuation premiums as public markets, and they often come with challenges like integrating operations and aligning company cultures post-deal. Founders should also reflect on their personal aspirations - whether they’re looking for a clean exit or want to remain involved in the company’s trajectory.

Since every fintech has unique circumstances, a tailored analysis is essential. Collaborating with a specialist advisor like Phoenix Strategy Group, which provides expertise in M&A, financial planning, and exit strategies, can help craft a path that aligns with your company’s stage of growth and long-term goals.

In 2026, the fintech IPO landscape is showing signs of a slow but steady recovery, thanks to a more predictable regulatory environment and cautious yet supportive capital markets. However, activity still hasn’t returned to the highs of previous years. For many fintech companies, acquisitions are becoming a more realistic and appealing exit route, driven by strong buyer interest and well-funded fintech firms eager to make strategic purchases.

When choosing between an IPO and an acquisition, fintech companies need to consider several key factors, including market conditions, their growth trajectory, and the readiness required to navigate public markets. Acquisitions often offer faster access to liquidity and involve less risk, whereas IPOs can open doors to long-term growth and increased market visibility.

Preparing for an IPO or acquisition takes meticulous planning and a solid groundwork. It all begins with getting your financials in top shape. This means maintaining accurate bookkeeping, having audited financial statements, and building a reliable financial planning and analysis (FP&A) model that can withstand stress tests. For IPOs, compliance with regulations like SOX and ensuring a clean capital structure are non-negotiable for passing due diligence.

Equally crucial is crafting a compelling strategic narrative that highlights your company’s vision and having a clear roadmap to profitability. Showcasing strong growth metrics, bringing together an experienced management team, and organizing a well-structured data room are also key steps. Partnering with seasoned advisors early in the process can make the journey smoother and set your fintech up for a successful exit.

{"@context":"https://schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"What should fintech companies consider when deciding between an IPO and an acquisition?","acceptedAnswer":{"@type":"Answer","text":"<p>When fintech companies face the decision between pursuing an IPO or opting for an acquisition, they need to carefully consider various factors like financial objectives, regulatory obligations, and their long-term vision. An IPO can unlock access to public capital, often leading to higher valuations and providing resources for future expansion. However, going public isn’t cheap - it demands significant upfront investment, multiple funding rounds, and strict adherence to regulations such as Sarbanes-Oxley. Timing is also crucial; strong equity markets can enhance IPO outcomes, while weaker markets might lead to reduced valuations.</p> <p>In contrast, acquisitions typically offer a quicker and more predictable payout with fewer regulatory complexities. That said, acquisitions might not command the same valuation premiums as public markets, and they often come with challenges like integrating operations and aligning company cultures post-deal. Founders should also reflect on their personal aspirations - whether they’re looking for a clean exit or want to remain involved in the company’s trajectory.</p> <p>Since every fintech has unique circumstances, a tailored analysis is essential. Collaborating with a specialist advisor like <strong>Phoenix Strategy Group</strong>, which provides expertise in M&A, financial planning, and exit strategies, can help craft a path that aligns with your company’s stage of growth and long-term goals.</p>"}},{"@type":"Question","name":"How might the market conditions in 2026 influence the decision between an IPO and an acquisition for fintech companies?","acceptedAnswer":{"@type":"Answer","text":"<p>In 2026, the fintech IPO landscape is showing signs of a slow but steady recovery, thanks to a more predictable regulatory environment and cautious yet supportive capital markets. However, activity still hasn’t returned to the highs of previous years. For many fintech companies, acquisitions are becoming a more realistic and appealing exit route, driven by strong buyer interest and well-funded fintech firms eager to make strategic purchases.</p> <p>When choosing between an IPO and an acquisition, fintech companies need to consider several key factors, including market conditions, their growth trajectory, and the readiness required to navigate public markets. Acquisitions often offer faster access to liquidity and involve less risk, whereas IPOs can open doors to long-term growth and increased market visibility.</p>"}},{"@type":"Question","name":"What steps should a fintech take to prepare for a successful IPO or acquisition?","acceptedAnswer":{"@type":"Answer","text":"<p>Preparing for an IPO or acquisition takes meticulous planning and a solid groundwork. It all begins with getting your financials in top shape. This means maintaining <strong>accurate bookkeeping</strong>, having <strong>audited financial statements</strong>, and building a reliable <strong>financial planning and analysis (FP&A) model</strong> that can withstand stress tests. For IPOs, compliance with regulations like SOX and ensuring a clean capital structure are non-negotiable for passing due diligence.</p> <p>Equally crucial is crafting a compelling <strong>strategic narrative</strong> that highlights your company’s vision and having a clear roadmap to profitability. Showcasing strong growth metrics, bringing together an experienced management team, and organizing a well-structured data room are also key steps. Partnering with seasoned advisors early in the process can make the journey smoother and set your fintech up for a successful exit.</p>"}}]}