Published on

July 5, 2026

PE tax risk can cut deal value fast. If a target had remote staff, inventory in other places, contractor activity, or cross-border travel before it filed tax returns, I’d expect buyers to price in back taxes, interest, penalties, and open-year risk.

Here’s the short version:

A few facts shape the whole review. In the U.S., economic nexus often starts at $100,000 in sales or 200 transactions. And if a required return was never filed, the tax year may stay open with no statute cutoff. That can make a small filing miss turn into a much larger deal issue.

What matters most to me is simple: did the company’s records match what its people were doing on the ground? If not, I’d expect buyer questions, slower closing, and pressure on terms.

PE Tax Diligence Process: From Nexus Mapping to Deal Protection

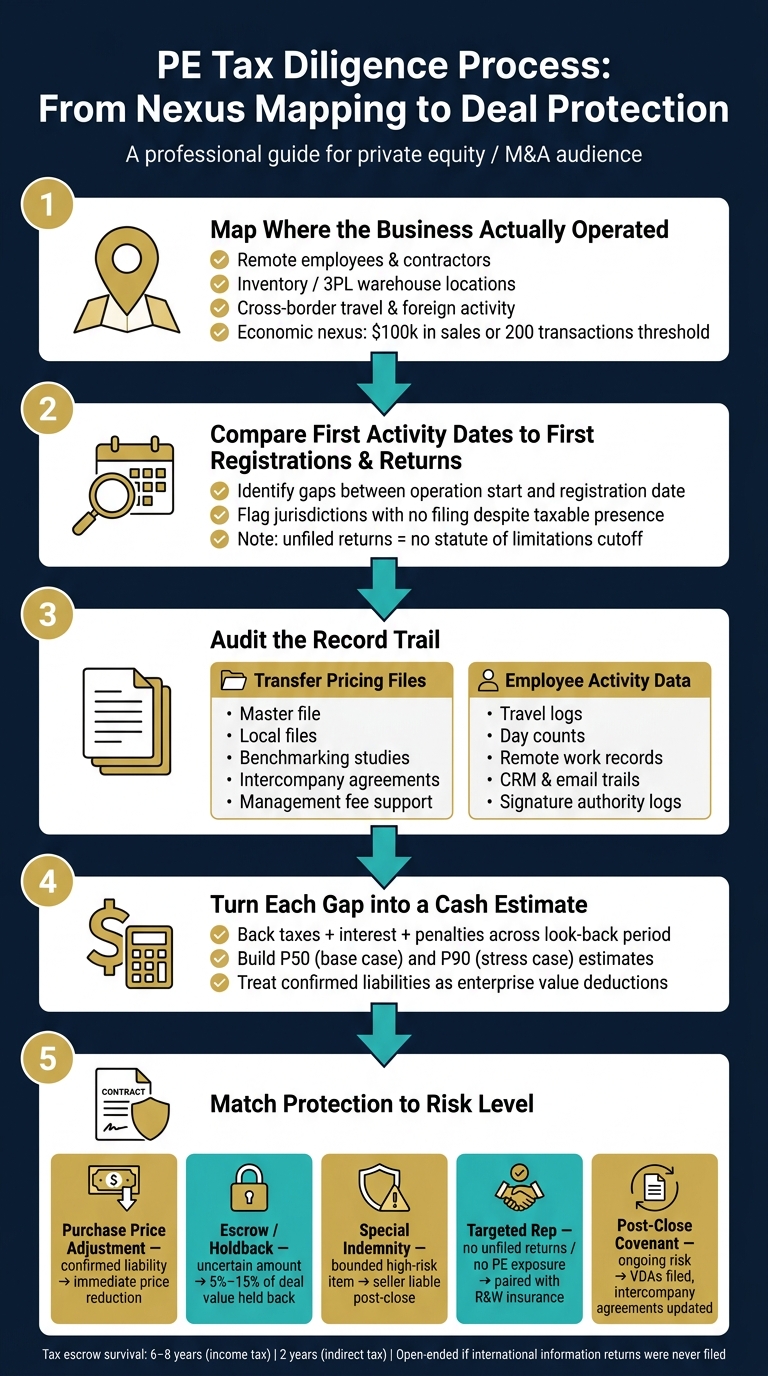

Buyers and sellers rebuild nexus history by putting together a timeline of where the company operated, hired people, stored inventory, and signed contracts. The point is simple: measure unfiled exposure before the deal team locks in price and indemnity terms. That timeline then turns into the buyer's checklist for registrations, returns, and backup records.

The document requests that matter most need to be complete. Buyers usually ask for three years of tax returns and registrations, filing calendars, audit notices, tax memos, transfer pricing files, intercompany agreements, entity charts, revenue by state and country, payroll and contractor records by location, and agent, distributor, and commission agreements.

When sellers pull these materials together before the data room opens, the process tends to move with less friction. Each document should be treated as proof of when tax duties started, not just a record of what got filed. Missing registrations, unfiled returns, or verbal guidance with no written backup often tell a buyer's tax team that the problem may run deeper.

Once the documents are in hand, buyers compare first taxable presence dates. When did the company first earn revenue in a state? When did it hire its first employee there, use a local contractor, or start storing inventory? Those dates are then matched against the first tax registration and the first return filed in that jurisdiction.

The main test is whether the business started operating before it registered or filed its first return. A company may have hired a remote sales rep in one jurisdiction long before registration happened there. That gap is open exposure. Other red flags include records that don't match across legal and tax filings, or cases where the company relied on a verbal conversation with an advisor instead of a written opinion to support its filing position.

Diligence should look at the U.S. and foreign footprint at the same time. For many growth-stage companies, exposure often comes from a mix of issues:

The table below shows the presence types buyers review most often, the proof they test, and the gap they often find:

| Presence Type | What Buyers Test | Common Gap Found |

|---|---|---|

| Remote employees (U.S. states) | Payroll records vs. state tax registrations | Registered late or never registered |

| Inventory / 3PL warehousing | 3PL contracts, shipping records vs. sales tax filings | Nexus triggered but no sales tax return filed |

| Foreign employee travel | Travel logs, day counts vs. treaty thresholds | Day-count threshold tripped across a calendar year or rolling period |

| Contractor / agent activity | Contract templates, signature authority | Local rep binding the company without a local entity [4] |

| Economic nexus (U.S.) | Revenue by state vs. filing thresholds | Sales exceeded threshold with no corresponding filing |

Before accepting the filing position, buyers count days under both calendar-year and rolling-12-month rules. Those records shape which jurisdiction risks end up affecting valuation and indemnity terms.

Filing dates are just the starting point. What matters next is the record trail behind them.

After buyers map the filing timeline, they dig into the documents that support it. In practice, two record sets matter most: transfer pricing files and employee activity data. Those records help show whether the tax position lines up with what the business was actually doing.

If a PE is found, the next issue is simple: how much profit should sit there? That answer usually comes from the transfer pricing file set.

Buyers look at the master file, local files, benchmarking studies, and signed intercompany agreements - such as service agreements, IP licenses, and cost-sharing arrangements. They are not just checking boxes. They are using these records to see whether the structure matches the facts on the ground.

The main test is straightforward: does the paperwork match reality? Persistent losses with no clear business reason, management fees with no support, and agreements signed after the fact all stand out as warning signs.

Buyers also test whether the entity booking the profit is the one doing the work that drives that profit. If income sits in an entity with no employees and no record of actual activity, that points to a substance problem.

The table below shows the transfer pricing records buyers review most often, what each one is meant to show, and where things tend to break down:

| Record Type | What Buyers Test | Common Gap Found |

|---|---|---|

| Intercompany agreements | Legal basis for profit allocation; check for retroactive signatures | Agreements signed after the fact or never executed |

| TP local files | Country-specific arm's length justification | Missing or outdated benchmarking studies |

| Functional analysis | Whether the entity has the people and assets to justify its profit share | Profit sitting in shell entities with no substance |

| P&L-to-intercompany reconciliation | Whether actual financial flows match the documented TP policy | Undocumented intercompany charges or inconsistent booking |

| Management fee support | Evidence of actual services performed | Fees charged with no underlying service documentation |

When these records are incomplete, buyers usually have to estimate how much profit allocation lines up with substance. That uncertainty often gets priced into the deal.

Once profit attribution is under review, attention shifts to where people were actually working.

Physical presence is the second major proof point. Travel logs and expense reports help test whether day-count thresholds were crossed. Remote work records matter too, because steady work from a home office can create PE risk. Buyers use these records to confirm where work happened, not to revisit the threshold rules already mapped in the nexus timeline.

Dependent agent risk is a bit less obvious, but it can be just as serious. Buyers check CRM records, email trails, and signature authority logs to see whether anyone negotiated contracts or pushed them forward on the company's behalf. Titles like "Regional Sales Lead" or "Strategic Account Director" can point to agency risk, which is why buyers look past the title and into what that person actually did.

On record quality: real-time travel logs and project documentation carry far more weight than after-the-fact reconstruction [5].

When those contemporaneous records are missing, buyers tend to price the exposure with a cautious hand.

Once diligence shows where the exposure sits, buyers have to put a dollar figure on it and decide who carries the risk in the purchase agreement. At that point, the findings stop being a tax memo and start affecting price, terms, and closing mechanics.

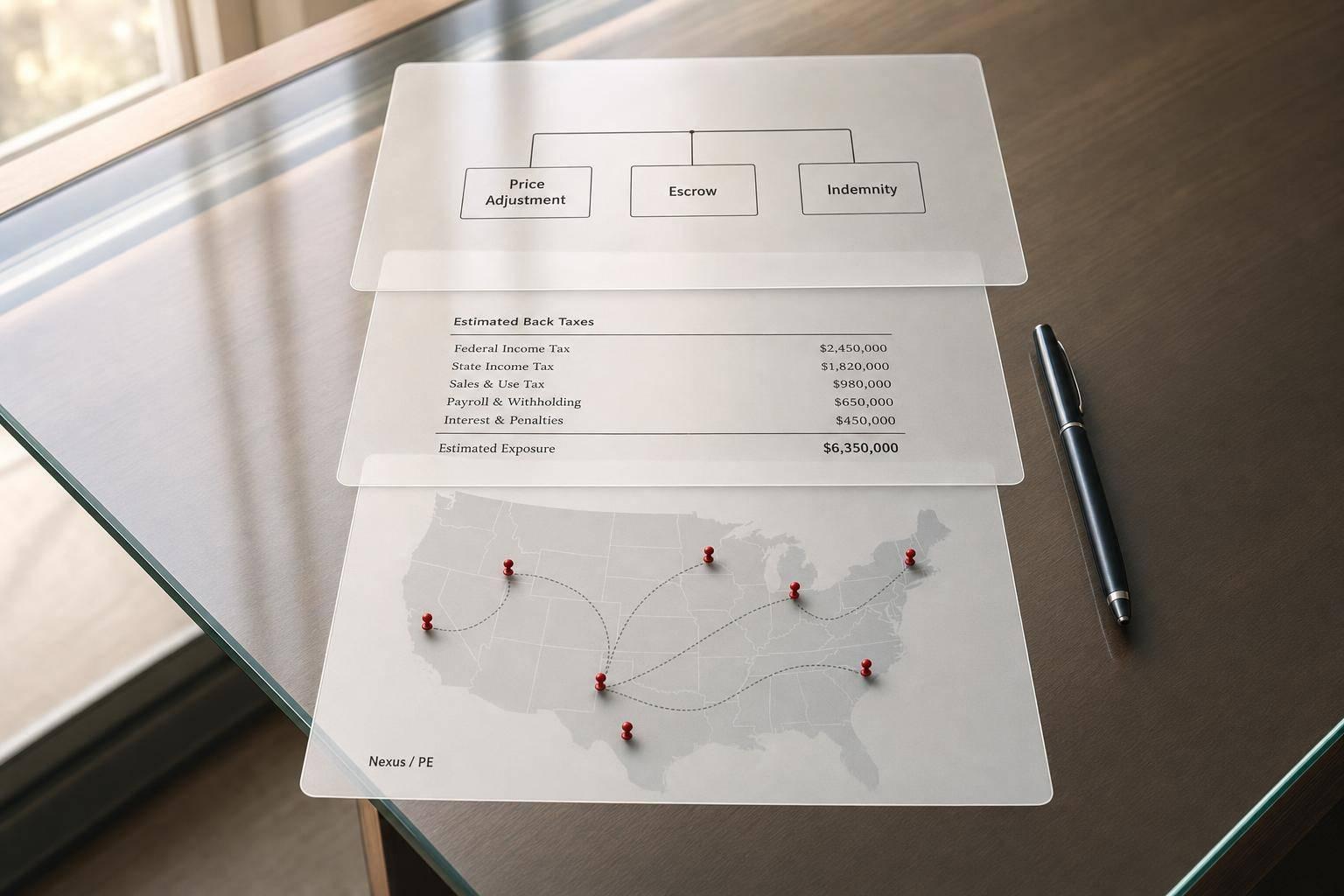

The starting point is usually the reconstructed filing gap. Buyers use it to estimate back taxes, penalties, and interest across the full look-back period. Many deal teams build both P50 and P90 cash estimates, then use that range in the negotiation.

When the exposure can be measured, it is often treated like a liability and deducted from enterprise value [3][4]. In smaller deals, or in founder-led sales, even a fairly modest PE issue can move the economics in a noticeable way.

The protection package usually matches the level and shape of the risk.

| Protection Option | When It Applies | Impact on Seller |

|---|---|---|

| Purchase Price Adjustment | Quantifiable, confirmed historical liability | Immediate reduction in cash received at close |

| Escrow / Holdback | Known risk with uncertain final amount; typically 5%–15% of deal value | Seller receives funds only after the survival period |

| Special Indemnity | Specific, bounded risk in a high-risk jurisdiction | Seller remains legally liable post-close for that item |

| Targeted Representation | No unfiled returns, PE exposure, or residency misstatements | Provides a claim basis and is often paired with R&W insurance |

| Post-Close Covenant | Ongoing risk requiring process changes | Buyer and seller cooperate on filings or VDAs after closing |

Survival periods depend on the tax involved. Tax escrows tied to income tax liabilities often run 6 to 8 years, while indirect tax issues, like sales tax, often have a 2-year survival window [4]. And there’s a catch: if the company never filed a required international information return, the statute may remain open with no end date. That usually pushes buyers toward special indemnities or escrows instead of relying on standard reps [1][2].

There’s also a big deal-structure point here. In a share deal, the buyer steps into the target’s full PE history, including problems that started before the acquisition. Asset deals usually give the buyer more cover because past liabilities tend to stay with the seller. Still, successor liability rules in some places can reach the buyer even in an asset purchase [2][4].

Closing doesn’t make the issue disappear. In many deals, the purchase agreement includes a post-close covenant that requires the seller or the combined business to fix the problem in the jurisdictions flagged during diligence.

Common steps include:

VDAs matter because they can limit the look-back period and waive penalties, turning an open-ended problem into a cost the parties can actually measure [2]. Teams also tend to clean up operating practices after closing, especially where employee movement or remote work helped create the exposure in the first place.

PE tax exposure usually doesn't sit in one obvious spot. It builds over time through remote work, intercompany charges, and missed filings across different jurisdictions. That's why the fix isn't a last-minute tax memo. It's a disciplined diligence review.

Start by mapping the footprint. Then test filings against actual business activity, review transfer pricing and travel records, and turn each gap into a dollar figure. Once you quantify the issue, the conversation shifts to price, escrow, or indemnity.

Even a small compliance gap can turn into a much bigger enterprise-value issue at closing if no one deals with it early. The goal is to walk into buyer review with a defensible package already in place.

Phoenix Strategy Group helps growth-stage companies organize payroll, travel, intercompany, and tax data into a defensible diligence package before buyers review it. A clean, quantified PE file helps protect price and reduce closing risk.

PE tax exposure starts when a company’s activities create a taxable presence in a jurisdiction where it has not been filing returns.

Common triggers include:

It’s easy to miss how this happens. A team sets up shop abroad, inventory sits in a local warehouse, or a distributor starts signing deals on the company’s behalf. On paper, those moves may seem routine. For tax purposes, they can create PE exposure fast.

The most important records are the ones that back up your past tax filing positions and your nexus or permanent establishment (PE) stance.

What matters most? Keep proof from the same time period that shows where people, inventory, and day-to-day business activity were located. That kind of record can make a big difference if a tax authority takes a closer look.

That usually includes:

In M&A, PE and tax nexus risks are often treated much like debt-like liabilities because they can cut into the target’s value. If due diligence turns up unfiled returns, audit exposure, or business activity that creates foreign tax obligations, buyers may push for a lower purchase price.

They may also ask for escrow holdbacks, special indemnities, or a different deal structure to push post-closing risk back to the seller.