Published on

July 5, 2026

Venture debt can extend runway by 6 to 12 months without new dilution, but it can also create a cash problem if your milestone slips. That’s the whole deal in one line.

If I were reviewing this topic fast, I’d focus on six things:

Here’s the short version: venture debt tends to work when you have one dated milestone, enough cash buffer, often managed by fractional CFO services, and a clean path to the next round. It tends to hurt when timelines are binary, repayment starts before value-creation hits, or covenants leave too little room.

| Area | What to watch |

|---|---|

| Best use case | Bridge to a near-term clinical, regulatory, or commercial milestone |

| Main upside | More cash with less dilution up front |

| Main risk | Fixed repayment even if the milestone is delayed |

| Bank-style lenders | Lower rates, lower warrant load, tighter covenants |

| Specialty lenders | Higher rates, more warrants, more milestone-based terms |

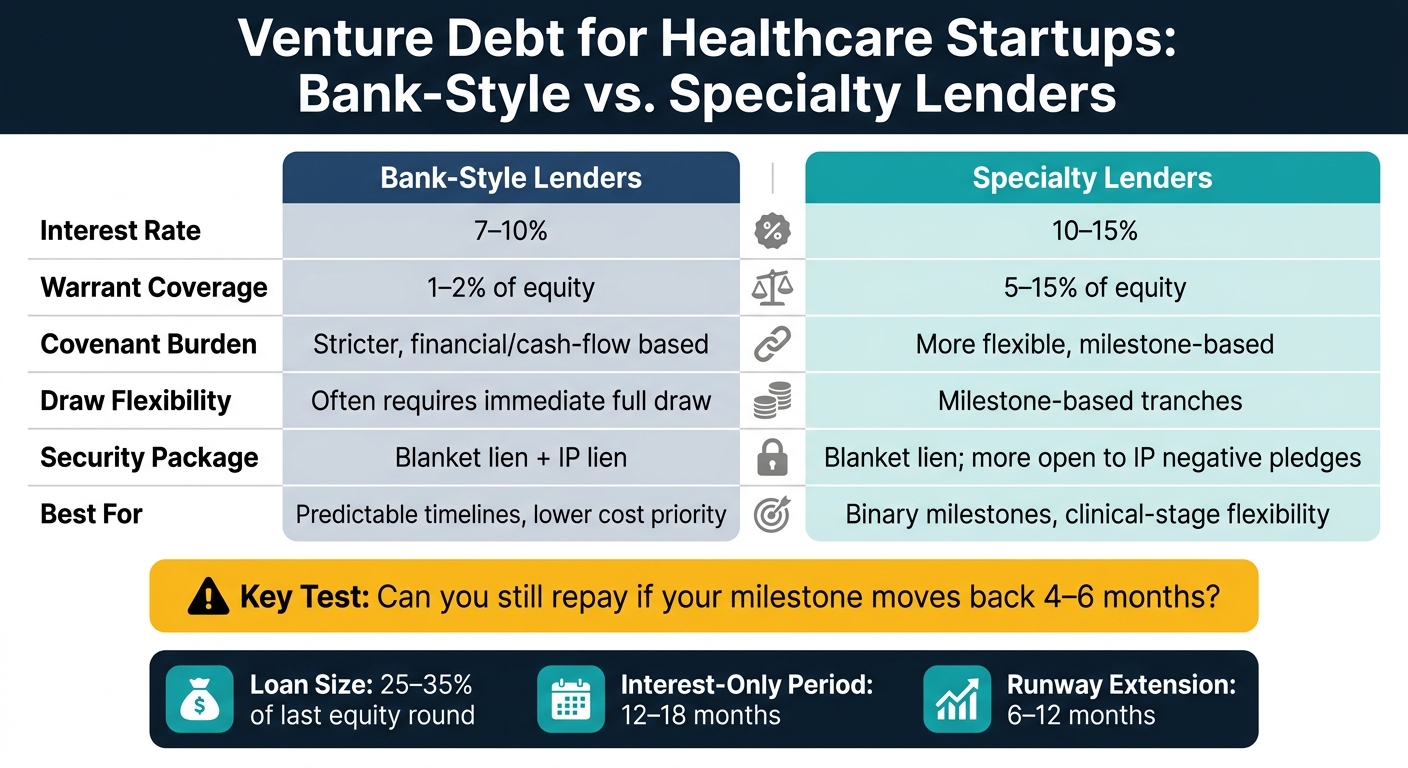

| Key test | Can you still pay if the milestone moves back 4 to 6 months? |

I’d read the article with one question in mind: does the debt buy time, or does it add pressure?

Venture Debt for Healthcare Startups: Bank vs. Specialty Lenders at a Glance

Venture debt facilities are usually sized at 25%–35% of your most recent equity round [3]. So if you just closed a $20 million Series B, a facility in the $5 million to $7 million range is common.

Pricing can add up fast, so it pays to map it out line by line. The base interest rate usually lands between 8% and 15%, and it’s often set as SOFR plus 600–800 basis points [2][3]. On top of that, many lenders charge:

That balloon fee can sneak up on teams that focus only on the monthly payment. Model it from day one.

Most facilities also come with 12–18 months of interest-only payments before amortization starts [3][2]. After that, repayment usually shifts into amortization over the remaining 24–36 months of the loan term [3]. On paper, that may look fine. In practice, it only works if the payment schedule lines up with your clinical, regulatory, or fundraising milestones.

A lot of healthcare venture debt is set up in milestone-based tranches. You get the first draw at closing, and later draws are tied to clinical, regulatory, or financing milestones [3]. That sounds simple enough, but there’s a catch: if a milestone slips, you can lose access to the next tranche.

Lenders also usually ask for a first-priority lien on all company assets through a UCC-1 filing. For IP, many use a negative pledge instead of taking the IP directly, which blocks new secured borrowing unless the lender says yes [2][1]. That can make future royalty financing or other secured debt much harder unless you negotiate a carve-out or refinance the facility [2].

Reporting is part of the package too. Expect monthly or quarterly financial reporting, insurance upkeep, and compliance certificates that confirm you’re meeting material agreement terms [2]. Many debt funds also want you to keep cash on hand equal to at least 35% of the total facility [2]. That kind of minimum can shape how much of the loan is usable in day-to-day planning.

The choice between a bank and a specialty lender usually comes down to a plain tradeoff: lower-cost capital vs. more milestone flexibility. It also changes the covenant load, the draw setup, and how much equity you hand over through warrants.

| Feature | Bank-Style Venture Debt | Specialty Lenders |

|---|---|---|

| Interest Rate | 7–10% [3] | 10–15% [3] |

| Warrant Coverage | 1–2% of equity [3] | 5–15% of equity [3] |

| Covenant Burden | Stricter (financial/cash-flow based) [3] | More flexible (milestone-based) [3] |

| Draw Flexibility | Often requires immediate full draw [3] | Milestone-based tranches [3] |

| Security Package | Blanket lien + IP lien [3] | Blanket lien; more open to IP negative pledges [2] |

The next step is checking how covenants and warrants change the true cost of the loan.

After you compare lender types, the next step is the covenant package. The interest rate is only one part of the bill.

Many facilities require a minimum cash balance. As of Q1 2026, about 45% of debt funds required cash on hand equal to at least 35% of the facility, up from 15% to 20% in earlier cycles [2]. Lenders also often set burn-rate caps and revenue minimums [2].

In healthcare, two default triggers need close attention.

The first is the Material Adverse Change (MAC) clause. It gives a lender the right to call a default if it thinks your financial condition or business outlook has materially worsened, even if you haven't missed a payment [2]. The second is the investor-abandonment clause. If current VC backers sit out the next round, the lender can treat that as a default [2].

Those clauses are tough because they're subjective. You can't plug them neatly into a spreadsheet and move on. That's why they deserve hard negotiation before anything gets signed.

A covenant breach can also trigger an automatic interest-rate step-up of 200 to 300 basis points and may accelerate the full outstanding balance [2]. For a healthcare startup waiting on a Phase 2 trial or an FDA filing, that kind of clause can turn a short delay into a cash crunch fast.

Once the covenants are clear, the next issue is equity. Put simply: what does the lender get for taking the risk?

Warrants are the lender's equity kicker. They give the lender the right to buy shares at a fixed price, usually the price from your most recent equity round. For specialty healthcare lenders, warrant coverage usually falls between 10% and 20% of total loan value [3], and in healthcare that often lands at about 0.5% to 1.5% of total equity [2]. For bank-style lenders, coverage is much lower, usually 1% to 2% of equity, but the tradeoff is less flexibility [3].

Then there are the extra fees:

Warrants can look minor at the start. They don't stay minor if the company's valuation climbs before exercise.

The Geron Corporation deal in November 2024 is a good example of how this can play out. To close a $125 million royalty deal with Royalty Pharma, Geron had to fully repay $86.5 million in existing venture debt because the existing lenders' first-priority lien and IP negative pledge were structurally incompatible with what the royalty buyer required [2].

The table below shows how covenant load and warrant dilution can shift based on lender type and deal setup. Neither path is always better. The right answer depends on your stage, your cash balance, and how much room you need to operate.

| Feature | Light Structure (Bank-Style) | Heavy Structure (Specialty/BDC) |

|---|---|---|

| Warrant Coverage | 1%–2% of equity [3] | 5%–15% of equity [3] |

| Covenant Structure | Stricter; often requires cash deposits [3] | More flexible; milestone-aligned [3] |

If covenants leave too little cash on the balance sheet, the loan can shrink runway instead of extending it.

Once covenants and warrants are clear, the next question is simple: does the debt buy time, or does it just add pressure?

Venture debt usually adds 6 to 12 months of runway [6][3]. But that range only works when draw timing, burn, and repayment match the company’s plan. If the repayment clock starts before your next milestone, the math can fall apart fast.

The safest way to look at debt is as a bridge to one specific, dated milestone. Not as extra padding. Not as a general cash reserve.

That distinction matters. More debt doesn’t always mean more room to operate. Some lenders require minimum cash-on-hand headroom of 35% of the total facility [2]. In plain English, that means part of the capital sits there as protection for the lender instead of being used by the business. So the stated facility size can look bigger than the amount you can put to work.

If principal repayment begins before the milestone is hit, the loan can do the opposite of what you wanted. Instead of extending runway, it starts eating into it.

Healthcare timelines slip all the time. Patient enrollment can move slower than planned. Payer contracts can take another quarter. FDA review cycles can drag longer than expected. That’s why founders should pressure-test the model before signing anything.

A good starting point is to model a 4- to 6-month delay in the key milestone - the "Milestone Delta" [4]. Then ask the hard question: can the company still cover debt service and covenant minimums, or does that delay push it into a down round?

That’s the heart of the risk. Debt can buy time, but it also makes a miss more costly.

Acorda’s Chapter 11 is a warning sign here: secured debt gets paid first, but that priority still does not stop a distressed outcome [2].

A three-case model can show whether the loan gives the company breathing room or just sets up another raise under stress.

| Metric | No Debt | Moderate Debt | Aggressive Debt |

|---|---|---|---|

| Runway Extension | 0 months | 6–9 months [3] | 12+ months [3] |

| Monthly Obligations | Operating costs only | Interest-only payments before principal begins [1][2] | Higher once principal repayment begins [1][2] |

| Covenant Risk | None | Lower, but still requires cash headroom [2] | Higher if performance slips [2] |

| Dilution Risk | Higher if a new round is needed sooner | Lower if the company reaches the next milestone [4][3] | Critical if milestones slip and refinancing becomes difficult [4][2] |

Aggressive debt can work when growth is predictable and margins are strong [5]. As Diwakar Sinha, Founder, Polaris Healthcare Partners, put it:

"Debt is fuel, but it's also weight. It accelerates growth, and amplifies strain." - Diwakar Sinha, Founder, Polaris Healthcare Partners [5]

That line gets to the point. If the business is already stretched, piling on more debt can speed up the strain instead of fixing it.

After you’ve looked at structure, covenants, and runway, the last question is pretty simple: does this debt buy time, or does it add pressure?

You have to judge venture debt as a full package: pricing, covenants, liens, warrants, and repayment timing. A low rate can still be a bad deal if it boxes you in when you need to raise again. Management keeps control, but covenants still shape what the company can and can’t do. That’s why the structure needs to be tested under stress, not just in the base-case model [2].

The final review should test the loan against a missed-milestone case, not just the plan you hope happens. Before signing, check these six items:

The right deal is the one that can hold up through a delayed trial, slower enrollment, or a pushed-out raise. If the structure creates lien conflict, thin headroom, or subjective default risk, it’s not extending runway. It’s borrowing strain.

If you need help stress-testing the numbers, build the model before you sign. Phoenix Strategy Group can help model covenant headroom, repayment capacity, and dilution tradeoffs.

Venture debt fits healthcare startups that have already raised institutional equity and need extra capital to extend runway, reach key clinical or commercial milestones, or bridge funding rounds without giving up more equity than they need to.

It tends to work best when growth is fairly predictable and the leadership team can manage repayment. For healthcare companies, that can be a big deal. Long development cycles and regulatory hurdles can stretch timelines fast, and venture debt can help cover that gap without adding too much financial pressure.

Model cash flow with rolling forecasts across scenarios like delayed regulatory approvals, reimbursement changes, and missed milestones. This gives you a clearer view of how the business might hold up when things don’t go to plan.

Track DSCR and aim for at least 1.5x. That target helps keep a cushion above the more common 1.25x minimum.

Also model the end of the interest-only period. That’s the point when principal and interest payments kick in and monthly burn goes up.

Stress-test covenant compliance too. And check how sensitive the model is to floating-rate moves tied to SOFR or Prime.

Beyond the interest rate, pay close attention to the terms that shape risk and flexibility.

That includes warrants, which can dilute your ownership later, and covenants such as minimum cash balance rules or burn-rate limits that can box you in when cash gets tight. You should also check for any first-priority lien on company assets, including intellectual property. That kind of claim can matter a lot if things go sideways.

It also helps to review the interest-only period. A longer one can ease near-term cash pressure and give you more runway.

Then there are material adverse change clauses. These can give lenders a lot of room to act based on their own judgment, so they deserve a close read.