Published on

June 24, 2026

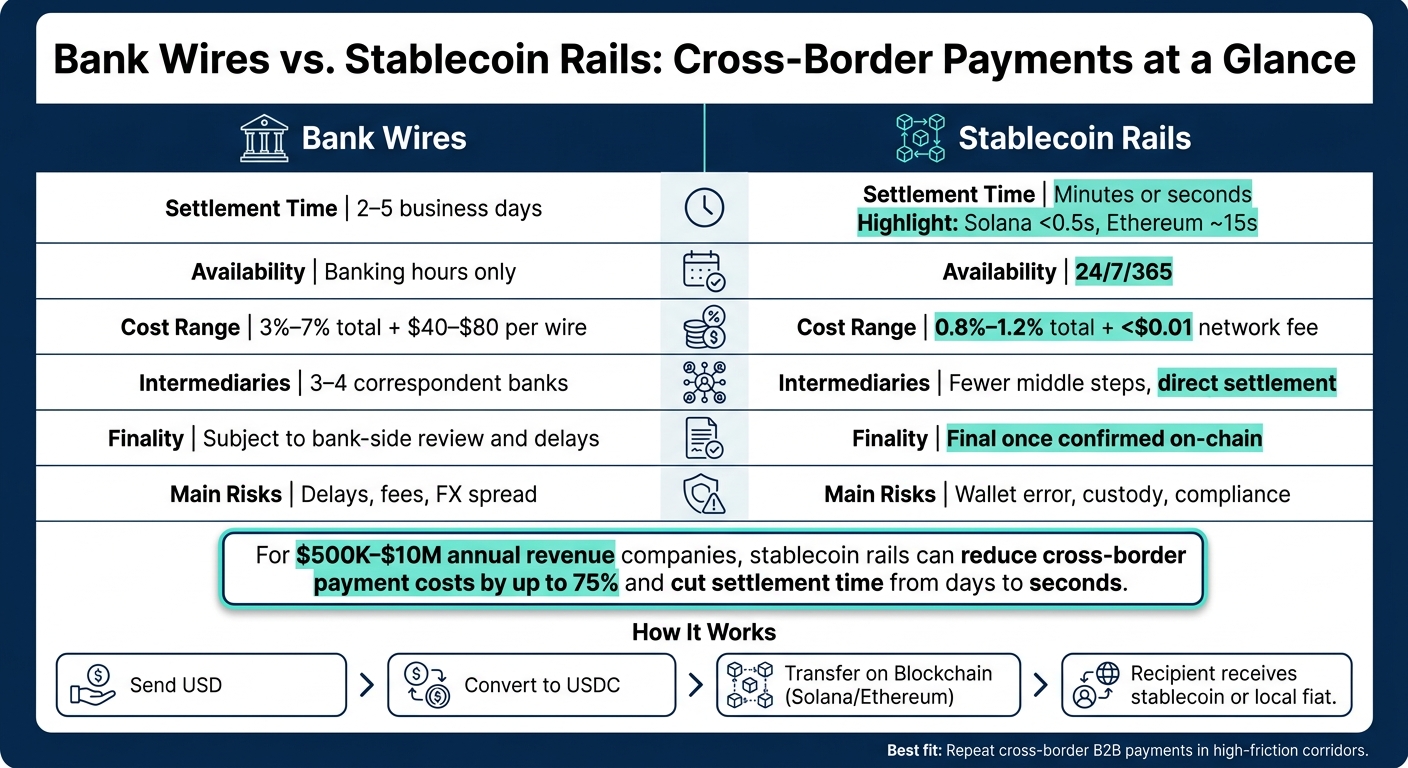

Stablecoins can cut cross-border payment costs from about 3% to 7% to roughly 0.8% to 1.2%, and settlement can move from 2 to 5 business days to minutes. For a U.S. company doing $500,000 to $10 million in annual revenue, that can mean lower payment costs, less cash stuck in transit, and tighter control over supplier payouts and customer collections.

Here’s the short version:

What I’d focus on before using it:

A plain takeaway: stablecoins are not the point; payment efficiency is. If you can set up custody, compliance, reconciliation, and ERP connections the right way, stablecoin rails may give you a lower-cost and faster option for global payments.

| Area | Bank Wires | Stablecoin Rails |

|---|---|---|

| Settlement time | 2 to 5 business days | Minutes or seconds |

| Availability | Banking hours | 24/7/365 |

| Cost range | 3% to 7% total | 0.8% to 1.2% total |

| Intermediaries | 3 to 4 banks common | Fewer middle steps |

| Finality | More bank-side review | Final once confirmed |

| Main risk | Delays, fees, FX spread | Wallet error, custody, compliance |

If I were a fractional CFO leading finance at a mid-market company, I’d treat this as a process decision, not a crypto experiment: start with one corridor, one supplier, small test transfers, and compare the result against your current SWIFT setup.

Bank Wires vs. Stablecoin Rails: Cross-Border Payment Comparison

With the core terms set, the next piece is simple: who moves the money, and who controls each step?

The easiest way to picture a stablecoin cross-border payment is the fiat-in, stablecoin-transfer, fiat-out flow. [11][2]

It works in three stages.

First, your company funds a corporate account in U.S. dollars, and a payment provider converts that fiat into a stablecoin such as USDC. [11][4]

Second, that stablecoin moves across a blockchain network like Solana or Ethereum to the recipient’s wallet, without correspondent banks in the middle. [11][1]

Third, the recipient can either keep the stablecoin or convert it into local currency and cash out through local rails. [11][13]

That’s the basic path. Money goes in as dollars, travels as a stablecoin, and comes out in the currency the recipient needs.

The timing is where things start to look very different from a wire. Settlement finality can happen in seconds - under 0.5 seconds on Solana and about 15 seconds on Ethereum - while old-school cross-border payments usually take 3–5 days. [11][2] And because blockchain settlement runs 24/7, payments don’t have to wait for banking hours, cutoff windows, or the next business day. [4]

On the company side, there’s still a lot of operational work. AP teams verify wallet addresses against an approved allow-list and approve payments through multisig. AR teams monitor finality and decide when to convert incoming receipts into local currency. [12][4][13] In other words, the rails may be new, but the need for tight controls is not.

Cost is another big difference. On high-throughput chains like Solana or Base, network fees are often less than $0.01 per transaction. A standard wire, by contrast, can cost $40–$80. [12][11]

The next issue isn’t just how the payment moves. It’s who owns what.

No single party controls the full flow. Each participant handles one part of the payment chain, and those lines need to be clear so treasury, AP, and AR teams can assign ownership and build the right checks around it.

That matters because stablecoin payments are coordinated, not centrally controlled.

| Participant | Role | Operational Responsibility | Key Control Point |

|---|---|---|---|

| Stablecoin Issuer | Asset Creator | Maintains reserve backing and redemption access | Monthly reserve attestations and audits |

| Payment Processor | Orchestrator | API integration, on/off-ramp handling, chain routing | KYB/AML screening and KYC |

| Blockchain Network | Settlement Layer | Records and finalizes transactions 24/7 | Chain selection and finality monitoring |

| Wallet / Custodian | Asset Security | Controls access and signing permissions | Multi-signature and role-based access |

| Company Treasury | Controller | Manages liquidity, selects assets, sets policy | Approval matrix and buffer limits |

| Recipient (Beneficiary) | Beneficiary | Receives funds; manages local currency conversion | Wallet security and FX timing |

One practical effect of this setup is that stablecoin rails can reduce pre-funded nostro balances and free up working capital. [4][7]

That speed comes with a tradeoff: risk management and control design shift more directly to treasury, AP, AR, and custody teams.

Stablecoin rails put more control - and more risk - on treasury, AP, and compliance. For companies scaling these operations, fractional CFO services can provide the necessary oversight. That changes the job. With a bank wire, there’s often a bit more room for recovery if something goes wrong. On-chain, settlement is final. Once funds move, they move. So approvals, screening, and custody rules need to be in place before anyone hits send.

The biggest operational risk is simple and brutal: sending funds to the wrong wallet. Blockchain transactions are irreversible, so a bad address can mean a permanent loss. The basic playbook is straightforward: use mandatory address whitelisting, require multisig approvals, and send a small test transfer to any new destination before sending the full amount. [1]

Credit risk matters too. A stablecoin is only as strong as its reserves and its redemption terms. For business payments, that usually means sticking with regulated, fiat-backed stablecoins that publish monthly reserve attestations and steering clear of algorithmic tokens. [3][10]

Then there’s wallet and custody risk. If private keys are stolen - or a non-regulated custodian fails - funds may be gone for good, with no regulator stepping in to make things right. That’s why many firms lean on regulated, insured custodians to lower that exposure. [1]

Compliance can’t stop at onboarding. AML and sanctions checks need to run on every transfer, in real time, at the transaction level. And Travel Rule requirements add another layer: sender and recipient details need to travel with the payment. [1][10]

Chain choice also affects risk. Different blockchains come with different tradeoffs on security, speed, and cost. A congested network can slow settlement or push gas fees higher than expected. [1][10]

| Risk Category | Business Impact | Control Approach |

|---|---|---|

| Issuer/Reserve Risk | Loss of principal if the issuer fails or the stablecoin de-pegs | Use regulated, fiat-backed tokens with monthly attestations |

| Operational Error | Permanent loss of funds sent to the wrong address | Address whitelisting, test transfers, and multisig approvals |

| Compliance/AML | Regulatory fines or frozen accounts | Real-time transaction-level screening and sanctions checks |

| Custody/Private Key Risk | Theft or permanent loss of funds | Regulated, insured custodians with SOC 2 Type II certification |

| Liquidity/Slippage | Higher-than-expected conversion costs | Providers with internal OTC desks and deep liquidity access |

| Regulatory Uncertainty | Frozen assets or sudden loss of service | Use issuers compliant with the GENIUS Act or MiCA |

Those controls lead straight into the next issue: every on-chain movement still needs to tie back cleanly to the general ledger.

Every on-chain transfer needs a matching internal record, whether that’s an invoice, a payout, or a treasury move. In the U.S., accounting treatment is still unsettled. Stablecoins may be classified as cash equivalents or intangible assets, depending on the jurisdiction and the reserve structure behind the token. Until there’s final guidance, document your classification logic clearly. [3][15]

At the transaction level, each transfer should link the on-chain transaction hash to the internal invoice ID. That gives you a clear audit trail instead of a messy scavenger hunt at month-end. Payment orchestration platforms can help here by connecting through APIs to ERP systems like SAP, Oracle, and NetSuite and feeding settlement data back for automated reconciliation. [9][13]

Month-end close is where discipline shows up. Wallet-to-ledger reconciliation is a must. Map each company-controlled wallet to a counterparty identity in your system, tie on-chain balances to the general ledger, and use multisig approvals to tighten authorization controls. Tax should come in early as well, since stablecoin-to-fiat conversions may create realized gains or losses, depending on the jurisdiction. [9][3]

Once the ledger is clean, treasury can decide how much stablecoin exposure to hold - and for how long.

Holding stablecoins changes liquidity planning in a pretty direct way. Because settlement runs 24/7/365, treasury can work around bank cut-off times and rely more on just-in-time funding instead of parking extra cash in the system. Policy should spell out which stablecoins are approved, which blockchain networks are allowed, the max allocation caps, and how long balances can stay on-chain. [1][15]

If balances won’t be needed within 24 to 48 hours, excess funds can be moved into short-duration, T-bill-backed instruments. [15]

On the FX side, the usual flow - fiat in, stablecoin transfer, fiat out - can cut exposure to correspondent banking FX spreads and local currency swings. But if funds sit on-chain instead of being converted right away, treasury needs clear rules around approved coins, approved networks, retention periods, and conversion triggers. [1][2][15]

With the controls in place, the next step is figuring out where stablecoins fit best across AP, AR, and treasury.

When a company puts the right controls in place, the clearest upside tends to show up in AP. Stablecoins make the most sense in cross-border corridors where wire transfers are slow, expensive, and hard to predict. In places like Sub-Saharan Africa, Southeast Asia, and Latin America, remittance fees can top 8%, and settlement can take two to five business days. [3][2] That mix makes AP timing tougher and ties up more cash than many finance teams would like.

The cleanest setup, in practice, is to plug stablecoin rails into ERP and treasury systems through APIs and webhooks. That way, AP can keep its approval steps and internal checks while the payment itself settles fast, without leaning on correspondent banks. [3][10][14] The beneficiary gets the full transferred amount before any off-ramp conversion happens. [14]

That can cut the need to keep foreign cash balances sitting around for routine payouts. Instead of leaving money idle overseas, companies can keep more liquidity available for day-to-day use. [1][3][6]

The same rails can help on the AR side too by shortening time to cash. For receivables, the best setup is often a bridge model: fiat in, stablecoin transfer, fiat out. That approach keeps digital asset exposure low and makes tax reporting easier. [2]

Teams can assign virtual IBANs or named accounts to customers, which helps incoming payments match the right open invoice on their own. [3][5] In plain English, that means less manual chasing, less guesswork, and cleaner reconciliation.

Stablecoins are not the right choice for every payment. The best fit depends on the corridor, the payment size, and how often the transaction happens. They tend to work best for repeat cross-border payouts and collections where bank rails add delays or extra cost. [3][2][14]

They usually make less sense for low-value transactions under about $500, where conversion fees can wipe out the savings. [9] That’s the part that matters most in planning: a fast rail is nice, but it still has to make financial sense.

Most of the hard work sits in the orchestration layer. Finance and ops teams need to connect blockchain rails to ERP systems and automate reconciliation so the process works inside normal workflows, not beside them. [3][10] Once those use cases are mapped out, the next move is a phased rollout plan.

Once you know which corridors and use cases make sense, start with a controlled pilot. Pick one high-friction corridor first. U.S. to Mexico, Brazil, or Nigeria are common starting points, especially when current fees are above 3% or settlement often takes two or more days. [8][6][13] This pilot should be treated as a treasury, AP, and AR process test, not a token trial.

Before any live payment goes out, get the groundwork done. Write the accounting policy, confirm U.S. and EU compliance requirements, choose a custody setup, and pick an orchestration partner that connects to your ERP through an API for FX conversion and reconciliation. [8][3][13]

Keep the first test tight:

The point is simple: compare settlement speed, total cost, and reconciliation effort against your current SWIFT baseline. If the numbers hold up, adding more corridors gets much easier. [1][13] And once the pilot proves the model, the next step is figuring out which tools can handle scale.

Three shifts deserve close attention.

First, programmable payouts are moving from idea to day-to-day use. Smart contracts can release funds when a shipment is confirmed or split one payment across several suppliers without manual work. [9][14]

Second, orchestration layers are improving fast. In May 2025, Circle launched the Circle Payments Network (CPN), which connects licensed institutions such as Deutsche Bank, Standard Chartered, and Flutterwave to settle in USDC or EURC on public blockchains. [9] That suggests a near future where much of the blockchain plumbing stays hidden behind regulated orchestration and one API. [3][13]

Third, local-currency stablecoins are cutting out the dollar round-trip in some cases. Tokens pegged to the dirham, euro, or Brazilian real let each side settle on-chain in its own currency, which removes one FX conversion from the flow. [6][13]

At this point, the decision comes down to operating discipline. Stablecoins can improve speed, cost, and visibility. But controls, accounting, and ERP integration decide whether the model works in practice.

Use the same controls already laid out in the guide: whitelisting, screening, custody, and reconciliation. Before scaling, answer four questions:

"The transition has begun. The treasurers and institutions that engage now will shape the standards. Those that wait will adopt them." - Mark Sutton and Thomas Otendal, Zanders [14]

The real test is operational readiness.

Yes. Stablecoin payments are legal for U.S. businesses.

The GENIUS Act, signed into law in July 2025, set a federal framework for payment stablecoins. That framework includes 1:1 reserve requirements and on-demand redemptions.

That said, legality doesn’t mean businesses can skip compliance. Companies still need to handle:

In plain English: a business can accept stablecoin payments, but it still has to treat them with the same care it would give any other regulated payment method.

Once a transaction is confirmed on the blockchain, it’s usually final. That means funds sent to the wrong wallet often can’t be recovered.

To lower that risk, companies should double-check wallet addresses before sending funds, use multi-level approvals, and put strong internal controls in place. That can include wallet limits and automated transfer processes.

Connect stablecoin workflows to your existing ERP and treasury systems so reconciliation happens automatically and in real time.

You can also connect regulated payment providers for on-ramps, off-ramps, virtual IBANs, and multi-currency accounts. Add tools for KYB/KYT screening, sanctions monitoring, and secure approval controls, too.

The result is simple: finance and treasury teams can manage liquidity and audit records with less manual work and fewer handoffs.